Coastal Community Bank Business Model Canvas

Coastal Community Bank: Strategic Business Model Canvas Revealed

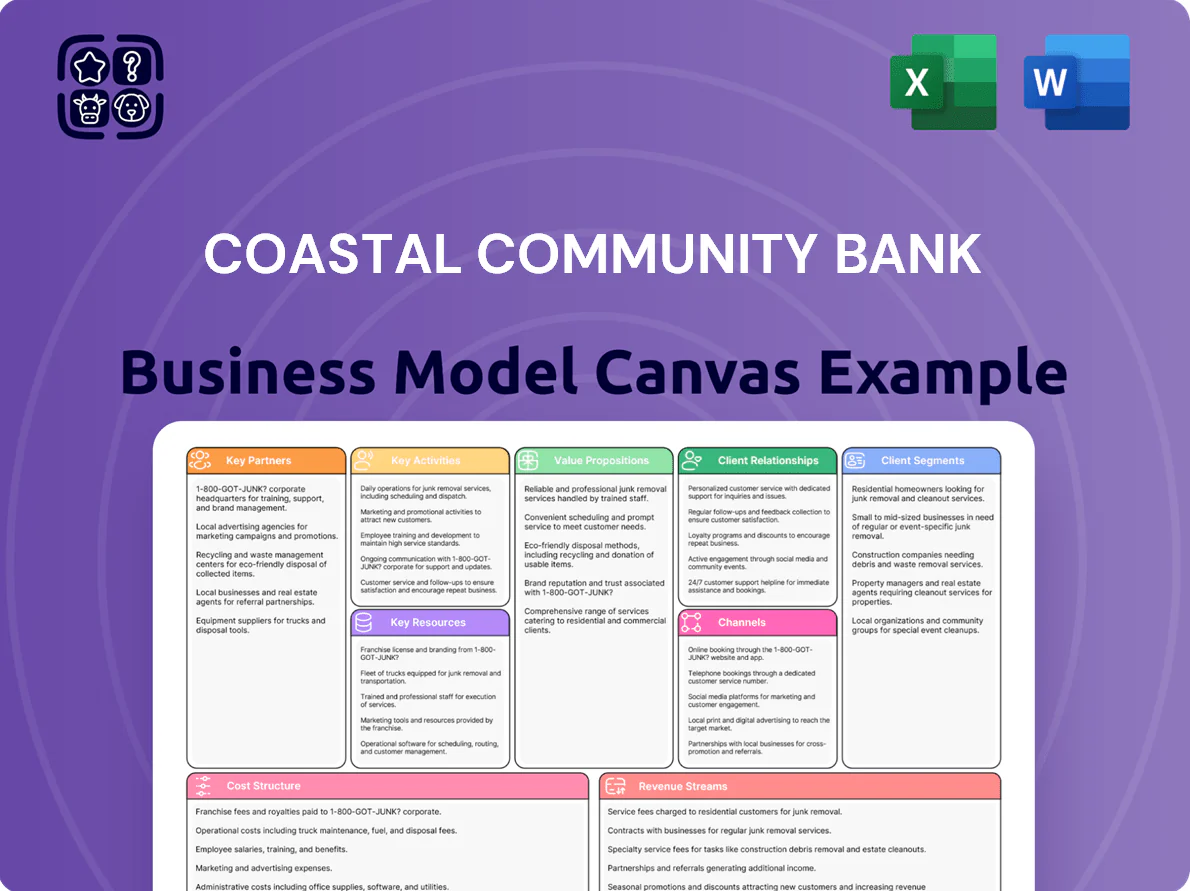

Unlock the full strategic blueprint behind Coastal Community Bank’s business model—this concise Business Model Canvas maps customer segments, value propositions, key activities, and revenue streams to reveal how the bank competes and scales in regional markets.

Partnerships

Fintech and BaaS Partners

Coastal Community Bank’s CCBX division partners with fintechs to deliver banking-as-a-service, enabling partners to issue branded deposits and payments using CCB’s charter; by YE 2024 CCBX helped originate over $2.1B in partner deposits and generated ~$38M in fee income, scaling balances without new branches. This model raised CCB’s noninterest income share to ~28% of total revenue in 2024 and cut marginal cost per account versus branch onboarding.

Regulatory and Compliance Authorities

As a highly regulated bank, Coastal Community Bank partners with the FDIC and Washington State regulators to ensure operational integrity; by late 2025 intensified oversight of third‑party fintechs means monthly compliance attestations rose 40% year‑over‑year.

The bank pilots new risk frameworks with regulators—joining three 2024–25 supervisory sandboxes—to keep partner deposits classified as safe harbor assets and limit regulatory capital add‑ons.

Technology Infrastructure Providers

Coastal Community Bank depends on core processors and cloud providers to run its CCBX platform, delivering >99.95% uptime and processing millions of transactions monthly (CCBX served ~120,000 digital users in 2025).

Ongoing integration with third-party APIs powers real-time payments, fraud detection, and fintech links, helping the bank scale secure data processing and stay competitive as digital deposits grew ~18% year-over-year in 2025.

Payment and Card Networks

Partnerships with Visa and Mastercard supply the transaction rails and interchange that power Coastal Community Bank’s debit and credit cards, generating fee income—interchange averaged 1.25% of card volume in 2024; card volume grew 14% YoY to $1.1B.

By 2025 these ties include real-time payment rails (RTP, tokenization) to enable instant settlements for retail and fintech partners, reducing float and improving customer experience.

- Visa, Mastercard provide processing rails

- Interchange ~1.25% of card volume (2024)

- Card volume $1.1B, +14% YoY (2024)

- 2025: added RTP and tokenization

Local Community and Business Organizations

The bank partners with Puget Sound chambers of commerce and nonprofits to source local lending deals and meet Community Reinvestment Act (CRA) targets; in 2024 these partnerships helped generate roughly 18% of small-business loan originations in its Washington footprint, supporting CRA-reportable lending and affordable-housing projects.

These engagements bolster the bank’s community brand and regional insight, contributing to a 7% year-over-year deposit growth in King and Pierce counties as of Dec 31, 2024.

- 18% of small-business loans from local partnerships (2024)

- Supports CRA lending and affordable-housing projects

- 7% deposit growth in King/Pierce counties (2024)

CCBX: $2.1B partner deposits, $38M fees, 120k digital users—noninterest income 28%

CCBX fintech partnerships originated $2.1B partner deposits by YE2024 and ~$38M fee income; noninterest income ≈28% of 2024 revenue. Core processors/clouds deliver >99.95% uptime; CCBX served ~120,000 digital users in 2025. Card volume $1.1B (+14% YoY 2024), interchange ~1.25%. Local partners drove 18% of small‑business loans and 7% deposit growth in King/Pierce (2024).

| Metric | Value |

|---|---|

| Partner deposits (YE2024) | $2.1B |

| Fee income (2024) | $38M |

| Noninterest income share (2024) | ~28% |

| Digital users (2025) | ~120,000 |

| Card volume (2024) | $1.1B |

| Interchange (2024) | ~1.25% |

| Small‑biz loans from partners (2024) | 18% |

| Deposit growth King/Pierce (2024) | 7% |

What is included in the product

A concise, pre-written Business Model Canvas for Coastal Community Bank covering customer segments, value propositions, channels, revenue streams, key activities, resources, partnerships, cost structure, and risk factors, reflecting real-world operations and competitive advantages for presentations and strategic decision-making.

Condenses Coastal Community Bank’s strategy into a digestible one-page Business Model Canvas, saving hours of structuring while enabling quick comparison, team collaboration, and board-ready insights for strategic decision-making.

Activities

Risk Management and Compliance Oversight

Commercial and Retail Loan Underwriting

The bank underwrites a diversified loan book—commercial real estate, small business, and consumer loans—totaling about $6.2 billion on the balance sheet as of Q4 2025; expert credit analysts stress-test portfolios and keep nonperforming loans near 0.9% to protect long-term stability. This underwriting turns deposits from 45 branches and fintech partners into yield-generating assets, targeting a 3.6% net interest margin.

BaaS Platform Maintenance and Innovation

Coastal Community Bank invests in ongoing API engineering and security, running a 24/7 DevOps squad that cut partner onboarding time from 45 to 12 days in 2024 and supports a 99.95% API uptime SLA; annual BaaS R&D spend reached $8.6M in 2024 to scale connections for 72 fintech partners and handle 3.2M monthly API calls while meeting SOC 2 and PCI-DSS controls.

Deposit Gathering and Liquidity Management

Coastal Community Bank targets low-cost deposits via 80+ branches and digital banking, keeping deposit beta low; as of 2025 it reported $6.2B in deposits, with core retail making ~65% and fintech-sourced deposits ~20% of total.

Management must balance fintech inflows against stable local deposits to keep liquidity ratios healthy; Q4 2025 liquidity coverage ratio (LCR) target ~110% and net stable funding ratio (NSFR) >100% guide treasury actions.

- Deposits: $6.2B (2025)

- Retail share: ~65%

- Fintech share: ~20%

- Target LCR: ~110%

- NSFR goal: >100%

Community Relationship Building

Staff engage in proactive outreach to Washington small businesses via monthly networking events, quarterly financial workshops (avg attendance 40–120), and bespoke consulting for complex loans—efforts that helped originations rise 11% in 2024, strengthening brand equity vs national banks.

- Monthly events: 12/year

- Workshops: 4/year, 40–120 attendees

- Consulting: drives 11% loan growth (2024)

Coastal Community Bank: $6.2B deposits, 3.6% NIM target, 99.2% AML hits, 12‑day onboarding

| Metric | Value (2025) |

|---|---|

| Deposits | $6.2B |

| Loan book | $6.2B |

| AML high-risk hit rate | 99.2% |

| Partner onboarding | 12 days |

| API uptime SLA | 99.95% |

| NIM target | 3.6% |

| LCR | ~110% |

| NSFR | >100% |

Preview Before You Purchase

Business Model Canvas

The preview you see is the actual Coastal Community Bank Business Model Canvas—not a mockup—and it reflects the exact content and layout you’ll receive after purchase.

When you complete your order, you’ll instantly download the same professional, fully editable document, formatted and ready for presentation or editing in Word and Excel.

No placeholders or marketing samples: this is the real deliverable, complete and unchanged from the preview.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Coastal Community Bank: Strategic Business Model Canvas Revealed

Unlock the full strategic blueprint behind Coastal Community Bank’s business model—this concise Business Model Canvas maps customer segments, value propositions, key activities, and revenue streams to reveal how the bank competes and scales in regional markets.

Partnerships

Fintech and BaaS Partners

Coastal Community Bank’s CCBX division partners with fintechs to deliver banking-as-a-service, enabling partners to issue branded deposits and payments using CCB’s charter; by YE 2024 CCBX helped originate over $2.1B in partner deposits and generated ~$38M in fee income, scaling balances without new branches. This model raised CCB’s noninterest income share to ~28% of total revenue in 2024 and cut marginal cost per account versus branch onboarding.

Regulatory and Compliance Authorities

As a highly regulated bank, Coastal Community Bank partners with the FDIC and Washington State regulators to ensure operational integrity; by late 2025 intensified oversight of third‑party fintechs means monthly compliance attestations rose 40% year‑over‑year.

The bank pilots new risk frameworks with regulators—joining three 2024–25 supervisory sandboxes—to keep partner deposits classified as safe harbor assets and limit regulatory capital add‑ons.

Technology Infrastructure Providers

Coastal Community Bank depends on core processors and cloud providers to run its CCBX platform, delivering >99.95% uptime and processing millions of transactions monthly (CCBX served ~120,000 digital users in 2025).

Ongoing integration with third-party APIs powers real-time payments, fraud detection, and fintech links, helping the bank scale secure data processing and stay competitive as digital deposits grew ~18% year-over-year in 2025.

Payment and Card Networks

Partnerships with Visa and Mastercard supply the transaction rails and interchange that power Coastal Community Bank’s debit and credit cards, generating fee income—interchange averaged 1.25% of card volume in 2024; card volume grew 14% YoY to $1.1B.

By 2025 these ties include real-time payment rails (RTP, tokenization) to enable instant settlements for retail and fintech partners, reducing float and improving customer experience.

- Visa, Mastercard provide processing rails

- Interchange ~1.25% of card volume (2024)

- Card volume $1.1B, +14% YoY (2024)

- 2025: added RTP and tokenization

Local Community and Business Organizations

The bank partners with Puget Sound chambers of commerce and nonprofits to source local lending deals and meet Community Reinvestment Act (CRA) targets; in 2024 these partnerships helped generate roughly 18% of small-business loan originations in its Washington footprint, supporting CRA-reportable lending and affordable-housing projects.

These engagements bolster the bank’s community brand and regional insight, contributing to a 7% year-over-year deposit growth in King and Pierce counties as of Dec 31, 2024.

- 18% of small-business loans from local partnerships (2024)

- Supports CRA lending and affordable-housing projects

- 7% deposit growth in King/Pierce counties (2024)

CCBX: $2.1B partner deposits, $38M fees, 120k digital users—noninterest income 28%

CCBX fintech partnerships originated $2.1B partner deposits by YE2024 and ~$38M fee income; noninterest income ≈28% of 2024 revenue. Core processors/clouds deliver >99.95% uptime; CCBX served ~120,000 digital users in 2025. Card volume $1.1B (+14% YoY 2024), interchange ~1.25%. Local partners drove 18% of small‑business loans and 7% deposit growth in King/Pierce (2024).

| Metric | Value |

|---|---|

| Partner deposits (YE2024) | $2.1B |

| Fee income (2024) | $38M |

| Noninterest income share (2024) | ~28% |

| Digital users (2025) | ~120,000 |

| Card volume (2024) | $1.1B |

| Interchange (2024) | ~1.25% |

| Small‑biz loans from partners (2024) | 18% |

| Deposit growth King/Pierce (2024) | 7% |

What is included in the product

A concise, pre-written Business Model Canvas for Coastal Community Bank covering customer segments, value propositions, channels, revenue streams, key activities, resources, partnerships, cost structure, and risk factors, reflecting real-world operations and competitive advantages for presentations and strategic decision-making.

Condenses Coastal Community Bank’s strategy into a digestible one-page Business Model Canvas, saving hours of structuring while enabling quick comparison, team collaboration, and board-ready insights for strategic decision-making.

Activities

Risk Management and Compliance Oversight

Commercial and Retail Loan Underwriting

The bank underwrites a diversified loan book—commercial real estate, small business, and consumer loans—totaling about $6.2 billion on the balance sheet as of Q4 2025; expert credit analysts stress-test portfolios and keep nonperforming loans near 0.9% to protect long-term stability. This underwriting turns deposits from 45 branches and fintech partners into yield-generating assets, targeting a 3.6% net interest margin.

BaaS Platform Maintenance and Innovation

Coastal Community Bank invests in ongoing API engineering and security, running a 24/7 DevOps squad that cut partner onboarding time from 45 to 12 days in 2024 and supports a 99.95% API uptime SLA; annual BaaS R&D spend reached $8.6M in 2024 to scale connections for 72 fintech partners and handle 3.2M monthly API calls while meeting SOC 2 and PCI-DSS controls.

Deposit Gathering and Liquidity Management

Coastal Community Bank targets low-cost deposits via 80+ branches and digital banking, keeping deposit beta low; as of 2025 it reported $6.2B in deposits, with core retail making ~65% and fintech-sourced deposits ~20% of total.

Management must balance fintech inflows against stable local deposits to keep liquidity ratios healthy; Q4 2025 liquidity coverage ratio (LCR) target ~110% and net stable funding ratio (NSFR) >100% guide treasury actions.

- Deposits: $6.2B (2025)

- Retail share: ~65%

- Fintech share: ~20%

- Target LCR: ~110%

- NSFR goal: >100%

Community Relationship Building

Staff engage in proactive outreach to Washington small businesses via monthly networking events, quarterly financial workshops (avg attendance 40–120), and bespoke consulting for complex loans—efforts that helped originations rise 11% in 2024, strengthening brand equity vs national banks.

- Monthly events: 12/year

- Workshops: 4/year, 40–120 attendees

- Consulting: drives 11% loan growth (2024)

Coastal Community Bank: $6.2B deposits, 3.6% NIM target, 99.2% AML hits, 12‑day onboarding

| Metric | Value (2025) |

|---|---|

| Deposits | $6.2B |

| Loan book | $6.2B |

| AML high-risk hit rate | 99.2% |

| Partner onboarding | 12 days |

| API uptime SLA | 99.95% |

| NIM target | 3.6% |

| LCR | ~110% |

| NSFR | >100% |

Preview Before You Purchase

Business Model Canvas

The preview you see is the actual Coastal Community Bank Business Model Canvas—not a mockup—and it reflects the exact content and layout you’ll receive after purchase.

When you complete your order, you’ll instantly download the same professional, fully editable document, formatted and ready for presentation or editing in Word and Excel.

No placeholders or marketing samples: this is the real deliverable, complete and unchanged from the preview.