Coats Porter's Five Forces Analysis

From Overview to Strategy Blueprint

Suppliers Bargaining Power

Raw Material Commodity Fluctuations

Polyester, nylon and cotton are Coats’ main inputs and remain vulnerable to commodity swings; petrochemical-driven synthetic-fiber costs rose ~18% in 2024–2025, raising input spend materially.

As of Q3 2025, petrochemical price spikes lifted polyester feedstock costs by ~22% year-on-year, forcing hedging and multi-supplier sourcing to protect margins.

During supply tightness and geopolitical stress, base-polymer suppliers gain pricing leverage, potentially adding 3–6 percentage points to Coats’ gross margin volatility.

Sustainability and Compliance Standards

Suppliers now face strict ESG rules from regulators like the EU Textile Strategy and US import measures, cutting viable vendors to ~20–30% who can supply GRS-certified recycled or bio-based inputs as of 2024.

That supply narrowing lets compliant vendors charge a premium; recycled yarn prices ran 8–18% above virgin equivalents in 2024, lifting upstream cost pressure on Coats’ margins.

Energy and Utility Costs

Manufacturing industrial threads uses lots of energy, leaving Coats vulnerable to utility pricing power; in 2024 global industrial electricity prices rose ~18% yoy in key markets, squeezing margins. In many regional hubs local supplier concentration lets higher gas and power costs be passed straight to manufacturers, adding volatility to cost of goods sold. Coats must invest heavily in on-site renewables—solar, wind, CHP—to hedge: a 5–10% capex lift can cut exposure by ~30% over 5 years.

Specialized Chemical Additives

Specialized chemical additives for high-performance and flame-retardant threads come from a handful of global firms, giving suppliers strong bargaining power because formulations are proprietary and technically complex.

Switching suppliers forces lengthy testing and re-certification—often 6–18 months—and can add 2–5% to unit costs, so Coats faces supply risk and cost pressure.

- Few global suppliers; proprietary formulations

- Switching 6–18 months; 2–5% higher unit cost

- High technical lock-in; limited negotiation leverage

Logistics and Freight Dependency

Global distribution relies on a few major carriers: Maersk, MSC, CMA CGM control about 60% of container capacity in 2024–25, giving suppliers strong pricing power over apparel makers like Coats Porter.

Ongoing route disruptions through 2025 raised spot rates by ~45% vs. 2019, so manufacturers face margin pressure unless they lock long-term contracts; fuel surcharges added roughly $150–$300 per FEU in 2024.

Long-term service agreements reduce volatility but can cost 5–10% more annually; without them, delayed inventory and higher landed costs can cut gross margins materially.

- Top 3 carriers ≈60% capacity

- Spot rates +45% vs 2019

- Fuel surcharge $150–$300/FEU (2024)

- Long-term contracts add 5–10% cost but lower volatility

Supplier squeeze: input shocks, premium recycled costs & carrier control tighten margins

Suppliers hold strong power: commodity feedstock swings (polyester +22% y/y Q3 2025), concentrated specialty-chemical providers, and top-3 carriers controlling ~60% capacity raise costs and switching barriers (6–18 months, +2–5% unit cost). ESG-compliant vendors = 20–30% supply, priced 8–18% above virgin inputs; energy and freight volatility add ~3–6pp gross-margin swing.

| Metric | 2024–25 |

|---|---|

| Polyester cost change | +22% y/y Q3 2025 |

| Recycled premium | +8–18% |

| Top-3 carrier share | ~60% |

| Switch time/cost | 6–18 months; +2–5% |

What is included in the product

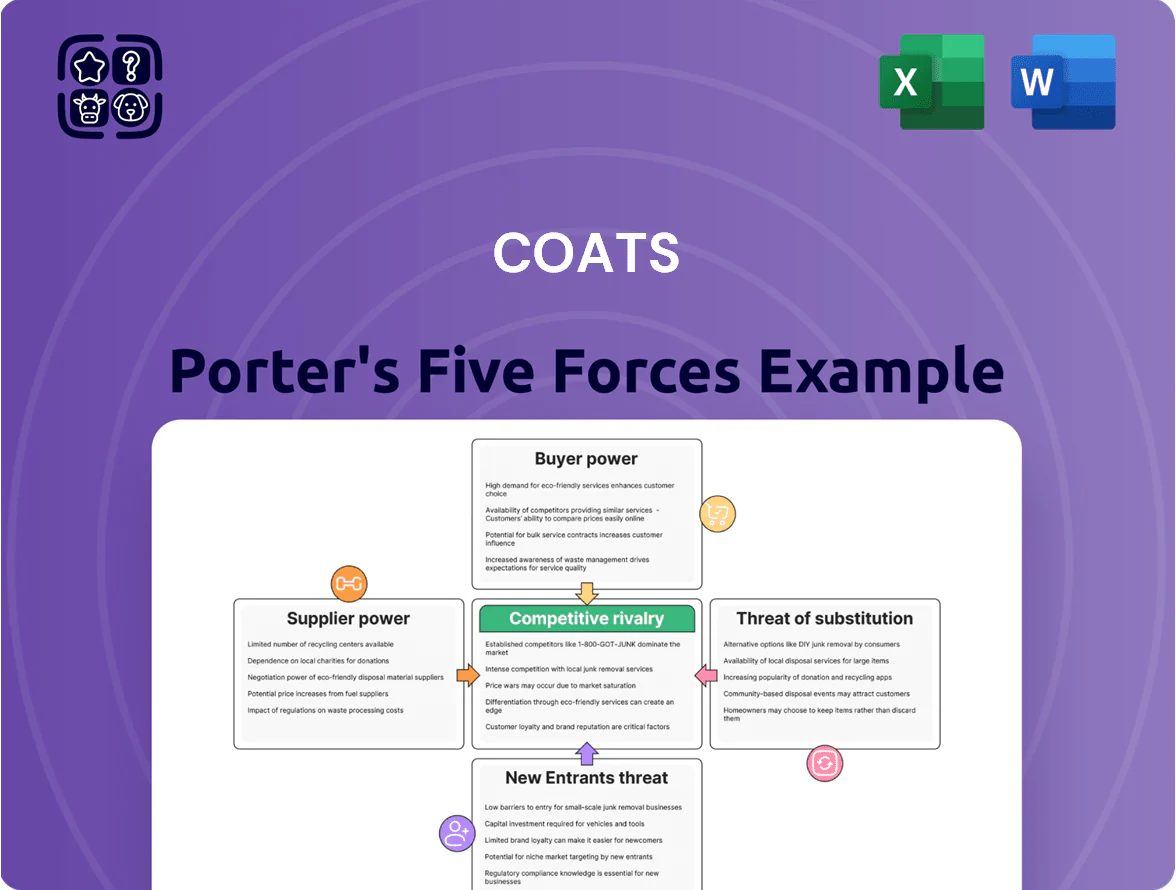

Concise Porter’s Five Forces analysis tailored to Coats, identifying competitive rivalry, supplier and buyer power, threats from new entrants and substitutes, plus disruptive trends and strategic implications for pricing, margins, and market positioning.

A concise, one-sheet Porter’s Five Forces for Coats—instantly highlights competitive pressures and strategic levers to accelerate decision-making.

Customers Bargaining Power

Concentration of Global Apparel Brands

A large share of Coats plc revenue comes from a few global footwear and apparel giants; in FY2024 about 45% of group sales were tied to top 20 customers, concentrating bargaining power. These buyers use bulk orders—often millions of metres of thread annually—to force 5–10% lower prices and extended 60–90 day payment terms. Their ability to switch contracts quickly among suppliers raises price pressure and margin risk for Coats.

Demand for Circularity and Recycled Content

By end-2025 major retailers (eg, H&M, Inditex) require 50–70% recycled content in trims and threads, shifting specs to buyers; this raises customers' bargaining power over Coats by forcing product redesigns and higher CAPEX for recycled feedstocks.

Low Switching Costs for Commodity Products

For standard apparel threads, switching costs are low, letting buyers shift to cheaper suppliers when tensile strength and colorfastness match; in 2024 global sewing thread imports rose 3.6% to $2.1bn, signaling price sensitivity. Customers routinely multi-source—surveys show 68% of mid-sized garment makers use 3+ thread vendors—to avoid single-supplier risk. This transparency keeps price competition intense for commodity components, pressuring margins.

Technical Integration in Automotive and Specialty Sectors

Customers in automotive and protective wear have lower bargaining power than apparel buyers because threads must meet strict UNECE, ISO and NFPA safety specs, raising switching costs and re-validation time to months or years.

Coats uses its technical R&D and lab certifications to command stable pricing and multi-year contracts; 2024 sales to industrial segments grew ~6%, showing stickier demand.

- Higher specs → higher switching costs

- Re-validation months–years

- Stable pricing, multi-year deals

- 2024 industrial sales +6%

Digitalization of the Supply Chain

Digital platforms let customers compare prices and track suppliers in real time; 78% of procurement teams used e-sourcing tools in 2024, raising service and speed demands on Coats.

That transparency lets buyers push for shorter lead times and higher service levels, increasing churn risk if Coats cannot match digital benchmarks.

Coats must invest in digital tools—client portals, real-time tracking, predictive lead-time analytics—to sell services beyond thread, mirroring a 12–18% premium peers captured in 2023.

- 78% procurement use e-sourcing (2024)

- Buyers demand faster delivery, higher SLAs

- Peers captured 12–18% service premium (2023)

- Invest in portals, real-time tracking, predictive analytics

Concentrated buyers squeeze prices and terms; industrial sales and e‑sourcing boost stickiness

Large buyers concentrate power: top 20 customers = ~45% of Coats FY2024 sales, forcing 5–10% price cuts and 60–90 day terms; apparel threads face low switching costs and multi-sourcing (68% use 3+ vendors), keeping margins tight. Industrial and automotive segments have higher switching costs due to UNECE/ISO/NFPA specs, making sales stickier (industrial sales +6% in 2024). E-sourcing use 78% (2024), pushing service digitalization; peers captured 12–18% service premium (2023).

| Metric | Value |

|---|---|

| Top-20 customer share | ~45% (FY2024) |

| Price pressure | 5–10% cuts |

| Payment terms | 60–90 days |

| Multi-sourcing | 68% use 3+ vendors |

| E-sourcing adoption | 78% (2024) |

| Industrial sales growth | +6% (2024) |

| Service premium peers | 12–18% (2023) |

What You See Is What You Get

Coats Porter's Five Forces Analysis

This preview shows the exact Coats Porter Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The document displayed is the full, professionally formatted analysis ready for download and use the moment you buy. You're viewing the actual deliverable; once payment is complete, you’ll get instant access to this same file with no further setup required.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Suppliers Bargaining Power

Raw Material Commodity Fluctuations

Polyester, nylon and cotton are Coats’ main inputs and remain vulnerable to commodity swings; petrochemical-driven synthetic-fiber costs rose ~18% in 2024–2025, raising input spend materially.

As of Q3 2025, petrochemical price spikes lifted polyester feedstock costs by ~22% year-on-year, forcing hedging and multi-supplier sourcing to protect margins.

During supply tightness and geopolitical stress, base-polymer suppliers gain pricing leverage, potentially adding 3–6 percentage points to Coats’ gross margin volatility.

Sustainability and Compliance Standards

Suppliers now face strict ESG rules from regulators like the EU Textile Strategy and US import measures, cutting viable vendors to ~20–30% who can supply GRS-certified recycled or bio-based inputs as of 2024.

That supply narrowing lets compliant vendors charge a premium; recycled yarn prices ran 8–18% above virgin equivalents in 2024, lifting upstream cost pressure on Coats’ margins.

Energy and Utility Costs

Manufacturing industrial threads uses lots of energy, leaving Coats vulnerable to utility pricing power; in 2024 global industrial electricity prices rose ~18% yoy in key markets, squeezing margins. In many regional hubs local supplier concentration lets higher gas and power costs be passed straight to manufacturers, adding volatility to cost of goods sold. Coats must invest heavily in on-site renewables—solar, wind, CHP—to hedge: a 5–10% capex lift can cut exposure by ~30% over 5 years.

Specialized Chemical Additives

Specialized chemical additives for high-performance and flame-retardant threads come from a handful of global firms, giving suppliers strong bargaining power because formulations are proprietary and technically complex.

Switching suppliers forces lengthy testing and re-certification—often 6–18 months—and can add 2–5% to unit costs, so Coats faces supply risk and cost pressure.

- Few global suppliers; proprietary formulations

- Switching 6–18 months; 2–5% higher unit cost

- High technical lock-in; limited negotiation leverage

Logistics and Freight Dependency

Global distribution relies on a few major carriers: Maersk, MSC, CMA CGM control about 60% of container capacity in 2024–25, giving suppliers strong pricing power over apparel makers like Coats Porter.

Ongoing route disruptions through 2025 raised spot rates by ~45% vs. 2019, so manufacturers face margin pressure unless they lock long-term contracts; fuel surcharges added roughly $150–$300 per FEU in 2024.

Long-term service agreements reduce volatility but can cost 5–10% more annually; without them, delayed inventory and higher landed costs can cut gross margins materially.

- Top 3 carriers ≈60% capacity

- Spot rates +45% vs 2019

- Fuel surcharge $150–$300/FEU (2024)

- Long-term contracts add 5–10% cost but lower volatility

Supplier squeeze: input shocks, premium recycled costs & carrier control tighten margins

Suppliers hold strong power: commodity feedstock swings (polyester +22% y/y Q3 2025), concentrated specialty-chemical providers, and top-3 carriers controlling ~60% capacity raise costs and switching barriers (6–18 months, +2–5% unit cost). ESG-compliant vendors = 20–30% supply, priced 8–18% above virgin inputs; energy and freight volatility add ~3–6pp gross-margin swing.

| Metric | 2024–25 |

|---|---|

| Polyester cost change | +22% y/y Q3 2025 |

| Recycled premium | +8–18% |

| Top-3 carrier share | ~60% |

| Switch time/cost | 6–18 months; +2–5% |

What is included in the product

Concise Porter’s Five Forces analysis tailored to Coats, identifying competitive rivalry, supplier and buyer power, threats from new entrants and substitutes, plus disruptive trends and strategic implications for pricing, margins, and market positioning.

A concise, one-sheet Porter’s Five Forces for Coats—instantly highlights competitive pressures and strategic levers to accelerate decision-making.

Customers Bargaining Power

Concentration of Global Apparel Brands

A large share of Coats plc revenue comes from a few global footwear and apparel giants; in FY2024 about 45% of group sales were tied to top 20 customers, concentrating bargaining power. These buyers use bulk orders—often millions of metres of thread annually—to force 5–10% lower prices and extended 60–90 day payment terms. Their ability to switch contracts quickly among suppliers raises price pressure and margin risk for Coats.

Demand for Circularity and Recycled Content

By end-2025 major retailers (eg, H&M, Inditex) require 50–70% recycled content in trims and threads, shifting specs to buyers; this raises customers' bargaining power over Coats by forcing product redesigns and higher CAPEX for recycled feedstocks.

Low Switching Costs for Commodity Products

For standard apparel threads, switching costs are low, letting buyers shift to cheaper suppliers when tensile strength and colorfastness match; in 2024 global sewing thread imports rose 3.6% to $2.1bn, signaling price sensitivity. Customers routinely multi-source—surveys show 68% of mid-sized garment makers use 3+ thread vendors—to avoid single-supplier risk. This transparency keeps price competition intense for commodity components, pressuring margins.

Technical Integration in Automotive and Specialty Sectors

Customers in automotive and protective wear have lower bargaining power than apparel buyers because threads must meet strict UNECE, ISO and NFPA safety specs, raising switching costs and re-validation time to months or years.

Coats uses its technical R&D and lab certifications to command stable pricing and multi-year contracts; 2024 sales to industrial segments grew ~6%, showing stickier demand.

- Higher specs → higher switching costs

- Re-validation months–years

- Stable pricing, multi-year deals

- 2024 industrial sales +6%

Digitalization of the Supply Chain

Digital platforms let customers compare prices and track suppliers in real time; 78% of procurement teams used e-sourcing tools in 2024, raising service and speed demands on Coats.

That transparency lets buyers push for shorter lead times and higher service levels, increasing churn risk if Coats cannot match digital benchmarks.

Coats must invest in digital tools—client portals, real-time tracking, predictive lead-time analytics—to sell services beyond thread, mirroring a 12–18% premium peers captured in 2023.

- 78% procurement use e-sourcing (2024)

- Buyers demand faster delivery, higher SLAs

- Peers captured 12–18% service premium (2023)

- Invest in portals, real-time tracking, predictive analytics

Concentrated buyers squeeze prices and terms; industrial sales and e‑sourcing boost stickiness

Large buyers concentrate power: top 20 customers = ~45% of Coats FY2024 sales, forcing 5–10% price cuts and 60–90 day terms; apparel threads face low switching costs and multi-sourcing (68% use 3+ vendors), keeping margins tight. Industrial and automotive segments have higher switching costs due to UNECE/ISO/NFPA specs, making sales stickier (industrial sales +6% in 2024). E-sourcing use 78% (2024), pushing service digitalization; peers captured 12–18% service premium (2023).

| Metric | Value |

|---|---|

| Top-20 customer share | ~45% (FY2024) |

| Price pressure | 5–10% cuts |

| Payment terms | 60–90 days |

| Multi-sourcing | 68% use 3+ vendors |

| E-sourcing adoption | 78% (2024) |

| Industrial sales growth | +6% (2024) |

| Service premium peers | 12–18% (2023) |

What You See Is What You Get

Coats Porter's Five Forces Analysis

This preview shows the exact Coats Porter Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The document displayed is the full, professionally formatted analysis ready for download and use the moment you buy. You're viewing the actual deliverable; once payment is complete, you’ll get instant access to this same file with no further setup required.