Cobra Automotive Technologies SpA Porter's Five Forces Analysis

From Overview to Strategy Blueprint

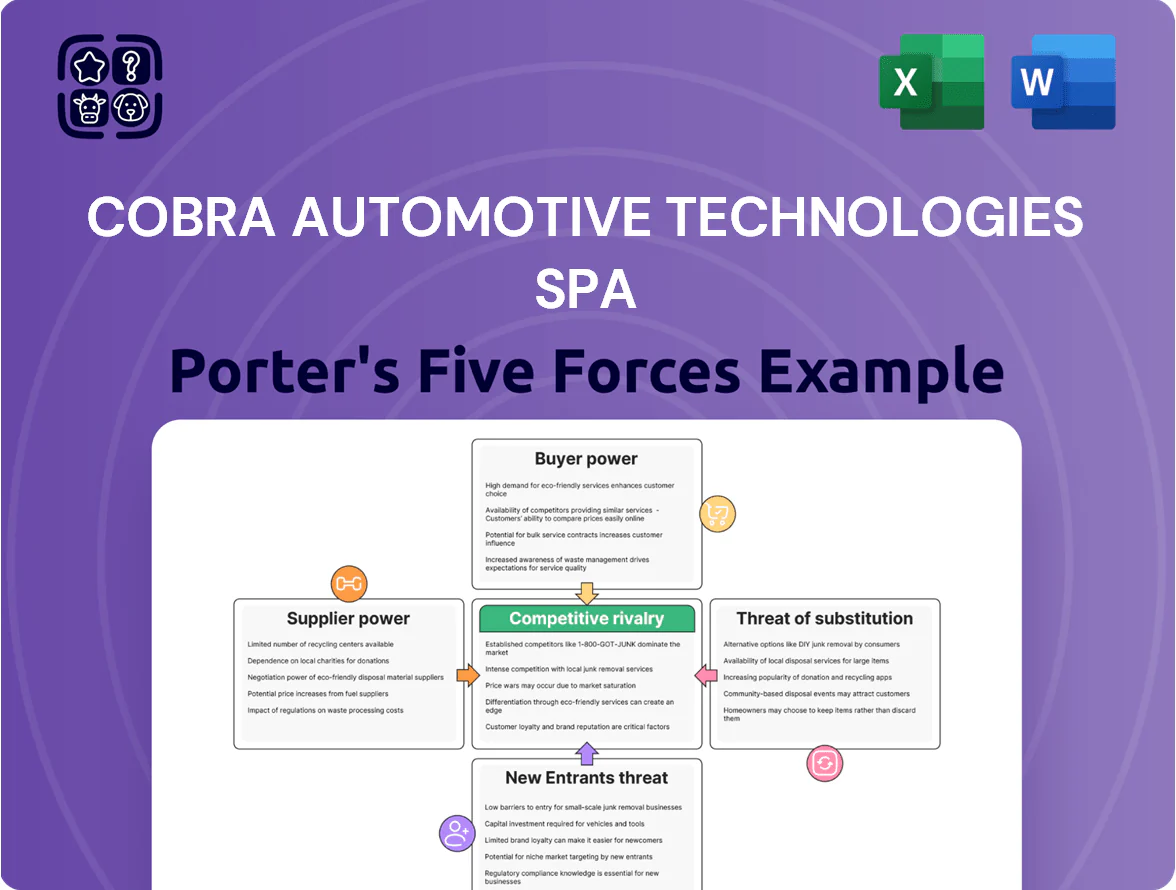

Cobra Automotive Technologies SpA faces moderate supplier power and rising buyer sophistication, while competitive rivalry is intense amid tech-driven differentiation and cost pressures; threats from new entrants and substitutes remain guarded but evolving with EV and connectivity trends. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Cobra Automotive Technologies SpA’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of semiconductor and chipset providers

Automotive electronics depend on a few global chipmakers for automotive-grade MCUs and GNSS modules; by Dec 2025, top suppliers (NXP, Infineon, STMicro) held ~60–70% market share in vehicle microcontrollers, keeping pricing power high.

Shortages eased after 2023, but demand for high-performance IoT components rose ~12% CAGR to 2025, so Vodafone Automotive faces supplier leverage and limited certified alternatives.

Dependency on global satellite and cellular networks

Cobra Automotive Technologies SpA relies on mobile network operators and satellite constellations for connectivity; these suppliers hold significant bargaining power because coverage and latency directly affect stolen-vehicle recovery and fleet telematics performance.

Vodafone Group ownership gives Cobra negotiated rates in core markets, but third-party roaming in 68 non-core countries (2024 footprint) creates cost-sensitive exposure suppliers can exploit, raising OPEX and service-risk.

Software and cloud infrastructure dominance

The shift to cloud analytics concentrates supplier power with hyperscalers: AWS, Microsoft Azure, and Google Cloud collectively held about 64% of global cloud market in 2024, giving them pricing leverage for telematics workloads.

These platforms provide the scalability to process Cobra’s telematics streams but impose high switching costs via proprietary services and data egress fees—egress can exceed $0.09/GB, inflating margins.

As Cobra converts legacy units to software-defined products, software costs rise as a share of COGS; hyperscaler pricing volatility and reserved-instance commitments can swing operating margin several percentage points annually.

Specialized sensor and component manufacturers

Advanced security systems need high-grade sensors and specialized hardware that meet ISO 26262 and UNECE R155 safety standards; certified suppliers are limited, with the top 10 sensor manufacturers controlling roughly 65% of the ADAS sensor market as of 2025.

This scarcity gives suppliers pricing power—sensor module ASPs rose ~8% YoY in 2024—and pressure OEMs integrating autonomous-ready architectures to accept firm terms to secure supply.

- Top 10 suppliers = ~65% market share (ADAS sensors, 2025)

- Average selling price up ~8% YoY (2024)

- Compliance: ISO 26262, UNECE R155 required

- Supply concentration raises switching costs for OEMs

Labor market for specialized cybersecurity talent

The pool of senior software engineers and cybersecurity experts for automotive protocols was still shallow in 2025, with estimates showing a global shortfall of ~40–50% for such niche roles versus demand in OEMs and Tier-1 suppliers.

These professionals act as critical intellectual-capital suppliers, driving rising wage bills (median total compensation up ~22% 2021–2025) and longer time-to-hire, which pressures Cobra Automotive Technologies SpA’s R&D spend and timelines.

Because continuous access to this expertise is required to maintain vehicle-security leadership, these specialists hold high bargaining power that can materially influence hiring budgets, contract terms, and project scope.

- ~40–50% global shortfall in niche auto-cyber roles (2025)

- Median comp +22% from 2021–2025 for senior specialists

- Longer hires → R&D schedule and cost pressure

- High influence on R&D budget and contract terms

High supplier power squeezes Cobra: concentrated chips, cloud, sensors & cyber talent

Suppliers hold high bargaining power for Cobra: key chipmakers (NXP, Infineon, STMicro) held ~60–70% MCU share by Dec 2025, ADAS sensor top 10 ≈65% (2025), hyperscalers (AWS/Azure/GCP) 64% cloud share (2024) with egress >$0.09/GB, and niche cyber talent shortfall ~40–50% (2025), all driving higher input costs, limited alternatives, and switching friction.

| Metric | Value |

|---|---|

| MCU share (top 3) | 60–70% (Dec 2025) |

| ADAS sensors (top 10) | ≈65% (2025) |

| Hyperscaler cloud share | 64% (2024) |

| Data egress cost | >$0.09/GB |

| Cyber talent gap | 40–50% shortfall (2025) |

What is included in the product

Tailored Porter's Five Forces analysis for Cobra Automotive Technologies SpA, uncovering competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and strategic vulnerabilities shaping its market position.

A concise Porter's Five Forces sheet for Cobra Automotive Technologies SpA—distilling supplier, buyer, rivalry, entrant, and substitute pressures into one actionable snapshot for faster strategic decisions.

Customers Bargaining Power

Concentration of major automotive OEMs

Major OEMs—Porsche, Audi, Volkswagen—account for a large share of factory-fitted security and telematics demand; VW Group alone sold 8.7 million vehicles in 2024, concentrating buying power and letting them push prices and specs.

Their order volumes and strict technical standards force suppliers like Cobra Automotive Technologies SpA to accept thin margins or co-develop to stay competitive.

If one OEM in the top five switches suppliers or internalizes development, revenue could drop by 20–40% for a single-contract-dependent vendor.

Low switching costs for aftermarket consumers

In Cobra Automotive Technologies SpA’s aftermarket retail segment, low switching costs let vehicle owners hop between security and tracking brands easily, with 68% of buyers using online comparison before purchase (2024 UK consumer survey) so price and reputation drive choice; transparent feature/pricing displays force margins down—average aftermarket device ASPs fell 9% YoY in 2023—and customers can abandon ecosystems after initial contracts, boosting buyer power.

Insurance company influence on telematics adoption

Insurance companies are major institutional buyers driving UBI and stolen-vehicle recovery adoption, with global UBI policies rising 28% in 2024 and insurers controlling ~60% of telematics procurement decisions; they pick preferred tech partners and can move whole portfolios to rivals, forcing rapid migrations. Their emphasis on data accuracy and cost per policy pressures telematics service fees down—average per-policy telematics fees fell 12% in 2023—squeezing margins for suppliers like Cobra.

Fleet manager demands for integrated data

Large fleet operators (clients with 1,000+ vehicles) demand end-to-end telematics that plug into ERP systems like SAP and Oracle, giving them leverage to request bespoke APIs and lower unit pricing for deployments often exceeding €1m; in 2024 global fleet telematics procurement shifted 18% toward integrated-platform contracts, raising service expectations.

Their buying power forces Vodafone Automotive (Cobra Automotive Technologies SpA brand partner) to match rivals such as Verizon Connect and Trimble with continuous feature releases and SLAs; 70% of large fleets cited integration and uptime as top vendor selection criteria in a 2025 industry survey.

- Clients: 1,000+ vehicles

- Typical contract: €1m+ deployments

- 2024 trend: 18% rise in integrated-platform deals

- 2025 survey: 70% prioritize integration and uptime

Price sensitivity in the budget vehicle segment

- Telematics adoption up 18% in subcompacts (IHS, 2024)

- WTP for premium security < €2/month (survey, 2024)

- Target subs price: €3–4/month to stay competitive

- Focus: reduce BOM and OPEX to protect margin

Buyer consolidation forces Cobra into low-margin deals, integration, and €3–4 subs

OEMs (VW Group 8.7M cars in 2024) and insurers (UBI +28% in 2024; ~60% procurement share) concentrate buying power, forcing Cobra to accept low margins or co-develop; large fleets (1,000+ vehicles; €1m+ deals) demand integration and lower unit prices, while aftermarket price sensitivity (ASP -9% YoY 2023; WTP <€2/month) compresses subscriptions to ~€3–4/month.

| Buyer | Key stat | Impact |

|---|---|---|

| OEMs | VW 8.7M cars (2024) | Price/spec leverage |

| Insurers | UBI +28% (2024) | Procurement control ~60% |

| Fleets | €1m+ deals | Integration demands |

| Aftermarket | ASP -9% (2023) | Price pressure |

Full Version Awaits

Cobra Automotive Technologies SpA Porter's Five Forces Analysis

This preview shows the exact Cobra Automotive Technologies SpA Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the same professionally written, fully formatted analysis file ready for immediate download and use the moment you buy. You're looking at the actual deliverable: complete, actionable, and ready for inclusion in reports or presentations. No mockups or samples—what you see is what you get.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Cobra Automotive Technologies SpA faces moderate supplier power and rising buyer sophistication, while competitive rivalry is intense amid tech-driven differentiation and cost pressures; threats from new entrants and substitutes remain guarded but evolving with EV and connectivity trends. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Cobra Automotive Technologies SpA’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of semiconductor and chipset providers

Automotive electronics depend on a few global chipmakers for automotive-grade MCUs and GNSS modules; by Dec 2025, top suppliers (NXP, Infineon, STMicro) held ~60–70% market share in vehicle microcontrollers, keeping pricing power high.

Shortages eased after 2023, but demand for high-performance IoT components rose ~12% CAGR to 2025, so Vodafone Automotive faces supplier leverage and limited certified alternatives.

Dependency on global satellite and cellular networks

Cobra Automotive Technologies SpA relies on mobile network operators and satellite constellations for connectivity; these suppliers hold significant bargaining power because coverage and latency directly affect stolen-vehicle recovery and fleet telematics performance.

Vodafone Group ownership gives Cobra negotiated rates in core markets, but third-party roaming in 68 non-core countries (2024 footprint) creates cost-sensitive exposure suppliers can exploit, raising OPEX and service-risk.

Software and cloud infrastructure dominance

The shift to cloud analytics concentrates supplier power with hyperscalers: AWS, Microsoft Azure, and Google Cloud collectively held about 64% of global cloud market in 2024, giving them pricing leverage for telematics workloads.

These platforms provide the scalability to process Cobra’s telematics streams but impose high switching costs via proprietary services and data egress fees—egress can exceed $0.09/GB, inflating margins.

As Cobra converts legacy units to software-defined products, software costs rise as a share of COGS; hyperscaler pricing volatility and reserved-instance commitments can swing operating margin several percentage points annually.

Specialized sensor and component manufacturers

Advanced security systems need high-grade sensors and specialized hardware that meet ISO 26262 and UNECE R155 safety standards; certified suppliers are limited, with the top 10 sensor manufacturers controlling roughly 65% of the ADAS sensor market as of 2025.

This scarcity gives suppliers pricing power—sensor module ASPs rose ~8% YoY in 2024—and pressure OEMs integrating autonomous-ready architectures to accept firm terms to secure supply.

- Top 10 suppliers = ~65% market share (ADAS sensors, 2025)

- Average selling price up ~8% YoY (2024)

- Compliance: ISO 26262, UNECE R155 required

- Supply concentration raises switching costs for OEMs

Labor market for specialized cybersecurity talent

The pool of senior software engineers and cybersecurity experts for automotive protocols was still shallow in 2025, with estimates showing a global shortfall of ~40–50% for such niche roles versus demand in OEMs and Tier-1 suppliers.

These professionals act as critical intellectual-capital suppliers, driving rising wage bills (median total compensation up ~22% 2021–2025) and longer time-to-hire, which pressures Cobra Automotive Technologies SpA’s R&D spend and timelines.

Because continuous access to this expertise is required to maintain vehicle-security leadership, these specialists hold high bargaining power that can materially influence hiring budgets, contract terms, and project scope.

- ~40–50% global shortfall in niche auto-cyber roles (2025)

- Median comp +22% from 2021–2025 for senior specialists

- Longer hires → R&D schedule and cost pressure

- High influence on R&D budget and contract terms

High supplier power squeezes Cobra: concentrated chips, cloud, sensors & cyber talent

Suppliers hold high bargaining power for Cobra: key chipmakers (NXP, Infineon, STMicro) held ~60–70% MCU share by Dec 2025, ADAS sensor top 10 ≈65% (2025), hyperscalers (AWS/Azure/GCP) 64% cloud share (2024) with egress >$0.09/GB, and niche cyber talent shortfall ~40–50% (2025), all driving higher input costs, limited alternatives, and switching friction.

| Metric | Value |

|---|---|

| MCU share (top 3) | 60–70% (Dec 2025) |

| ADAS sensors (top 10) | ≈65% (2025) |

| Hyperscaler cloud share | 64% (2024) |

| Data egress cost | >$0.09/GB |

| Cyber talent gap | 40–50% shortfall (2025) |

What is included in the product

Tailored Porter's Five Forces analysis for Cobra Automotive Technologies SpA, uncovering competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and strategic vulnerabilities shaping its market position.

A concise Porter's Five Forces sheet for Cobra Automotive Technologies SpA—distilling supplier, buyer, rivalry, entrant, and substitute pressures into one actionable snapshot for faster strategic decisions.

Customers Bargaining Power

Concentration of major automotive OEMs

Major OEMs—Porsche, Audi, Volkswagen—account for a large share of factory-fitted security and telematics demand; VW Group alone sold 8.7 million vehicles in 2024, concentrating buying power and letting them push prices and specs.

Their order volumes and strict technical standards force suppliers like Cobra Automotive Technologies SpA to accept thin margins or co-develop to stay competitive.

If one OEM in the top five switches suppliers or internalizes development, revenue could drop by 20–40% for a single-contract-dependent vendor.

Low switching costs for aftermarket consumers

In Cobra Automotive Technologies SpA’s aftermarket retail segment, low switching costs let vehicle owners hop between security and tracking brands easily, with 68% of buyers using online comparison before purchase (2024 UK consumer survey) so price and reputation drive choice; transparent feature/pricing displays force margins down—average aftermarket device ASPs fell 9% YoY in 2023—and customers can abandon ecosystems after initial contracts, boosting buyer power.

Insurance company influence on telematics adoption

Insurance companies are major institutional buyers driving UBI and stolen-vehicle recovery adoption, with global UBI policies rising 28% in 2024 and insurers controlling ~60% of telematics procurement decisions; they pick preferred tech partners and can move whole portfolios to rivals, forcing rapid migrations. Their emphasis on data accuracy and cost per policy pressures telematics service fees down—average per-policy telematics fees fell 12% in 2023—squeezing margins for suppliers like Cobra.

Fleet manager demands for integrated data

Large fleet operators (clients with 1,000+ vehicles) demand end-to-end telematics that plug into ERP systems like SAP and Oracle, giving them leverage to request bespoke APIs and lower unit pricing for deployments often exceeding €1m; in 2024 global fleet telematics procurement shifted 18% toward integrated-platform contracts, raising service expectations.

Their buying power forces Vodafone Automotive (Cobra Automotive Technologies SpA brand partner) to match rivals such as Verizon Connect and Trimble with continuous feature releases and SLAs; 70% of large fleets cited integration and uptime as top vendor selection criteria in a 2025 industry survey.

- Clients: 1,000+ vehicles

- Typical contract: €1m+ deployments

- 2024 trend: 18% rise in integrated-platform deals

- 2025 survey: 70% prioritize integration and uptime

Price sensitivity in the budget vehicle segment

- Telematics adoption up 18% in subcompacts (IHS, 2024)

- WTP for premium security < €2/month (survey, 2024)

- Target subs price: €3–4/month to stay competitive

- Focus: reduce BOM and OPEX to protect margin

Buyer consolidation forces Cobra into low-margin deals, integration, and €3–4 subs

OEMs (VW Group 8.7M cars in 2024) and insurers (UBI +28% in 2024; ~60% procurement share) concentrate buying power, forcing Cobra to accept low margins or co-develop; large fleets (1,000+ vehicles; €1m+ deals) demand integration and lower unit prices, while aftermarket price sensitivity (ASP -9% YoY 2023; WTP <€2/month) compresses subscriptions to ~€3–4/month.

| Buyer | Key stat | Impact |

|---|---|---|

| OEMs | VW 8.7M cars (2024) | Price/spec leverage |

| Insurers | UBI +28% (2024) | Procurement control ~60% |

| Fleets | €1m+ deals | Integration demands |

| Aftermarket | ASP -9% (2023) | Price pressure |

Full Version Awaits

Cobra Automotive Technologies SpA Porter's Five Forces Analysis

This preview shows the exact Cobra Automotive Technologies SpA Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the same professionally written, fully formatted analysis file ready for immediate download and use the moment you buy. You're looking at the actual deliverable: complete, actionable, and ready for inclusion in reports or presentations. No mockups or samples—what you see is what you get.