Coca-Cola PESTLE Analysis

Your Competitive Advantage Starts with This Report

Coca-Cola faces intensifying regulatory scrutiny, shifting consumer tastes toward healthier options, and supply-chain volatility—while digital marketing and sustainability investments create new growth avenues; our PESTLE distills these forces into strategic insights. Purchase the full PESTLE Analysis to get a comprehensive, actionable breakdown that informs investment theses, competitive strategy, and risk management. Download now for ready-to-use, expert research.

Political factors

Geopolitical Trade Tensions

Ongoing trade disputes and protectionist measures in markets like China and the EU raised input costs for Coca-Cola, contributing to a 3.8% increase in cost of goods sold in 2024 versus 2023 and pressuring margins in its concentrates segment.

By late 2025 shifting tariffs and renegotiated trade terms affected cross-border concentrate shipments, with international operating margins varying by up to 220 basis points across regions.

Stable diplomatic relations remain critical: disruptions risk supply-chain delays and sudden freight cost spikes that could erode the company’s global distribution efficiency and dilute its 2024 global net revenue of $46.0 billion.

Taxation on Sugar-Sweetened Beverages

Regulatory Scrutiny in Emerging Markets

Political instability in regions such as the Middle East and parts of Africa elevates operational risk for Coca-Cola’s bottlers and logistics; for example, disruptions in 2023 reduced distribution in some African markets by an estimated 7–10%, impacting local revenues. Coca-Cola’s localized model demands continual engagement with authorities to secure licenses and workforce safety—the company spent $120–150 million annually on compliance and community programs in 2024–2025 across emerging markets. Sudden leadership changes can trigger abrupt regulatory shifts on land use or water rights, risking production interruptions given that up to 60% of local plant inputs are region-specific.

Plastic Waste Legislation

Political mandates on Extended Producer Responsibility now force beverage makers to fund packaging end-of-life; EU rules target 30% recycled PET in bottles by 2025 and collection rates of 90% for single-use plastic bottles, while several US states ramp EPR schemes with fees up to $0.20–$0.40 per unit.

Coca-Cola must increase recycled-content sourcing and step up lobbying/compliance to avoid fines and potential $100s of millions in EPR fees and capital for recycling infrastructure.

- EU: 30% recycled PET by 2025; 90% collection target

- US: state EPR fees $0.20–$0.40/unit; expanding mandates

- Financial impact: potential hundreds of millions for compliance and fees

Labor and Employment Regulations

Rising minimum wages and strengthened labor-rights laws across markets—e.g., US federal push for $15+ and EU wage indexation trends—raise bottlers’ labor costs, squeezing Coca-Cola’s margins and increasing concentrate pricing pressure; 2024 bottling labor disputes contributed to estimated regional production slowdowns of up to 4–6% in isolated markets.

Political campaigns for collective bargaining and enhanced worker protections force Coca-Cola to sustain stringent ESG and supplier-audit programs; failure risks reputational losses and retail delistings that can cut local sales by several percentage points.

Navigating diverse labor regimes is essential to prevent strikes and ensure supply continuity: proactive labor engagement and contingency capacity planning helped the company avoid major global disruptions during 2023–2025, limiting lost production to under 1% annually.

- Higher minimum wages and labor protections raise bottler operating costs and margin pressure

- Stronger collective-bargaining movements demand robust ESG/supplier audits to protect brand

- Effective labor relations and contingency planning minimized global disruption to <1% lost production (2023–2025)

Coca-Cola faces rising costs, taxes and tariffs; $46B revenue but margins squeezed

Political risks—trade disputes, sugar taxes, EPR mandates, wage hikes, and regional instability—raised Coca-Cola’s 2024–25 costs and pressured margins: COGS +3.8% (2024), global revenue $46.0B (2024), tariffs drove ±220bps margin variance (2025), SSB taxes in 70+ jurisdictions affecting ~$12B sales, EPR compliance risk in the hundreds of millions.

| Metric | Value |

|---|---|

| 2024 global revenue | $46.0B |

| COGS change 2024 vs 2023 | +3.8% |

| Regional margin variance (2025) | ±220bps |

| SSB-affected sales | $12B |

| EPR cost risk | $100sM |

What is included in the product

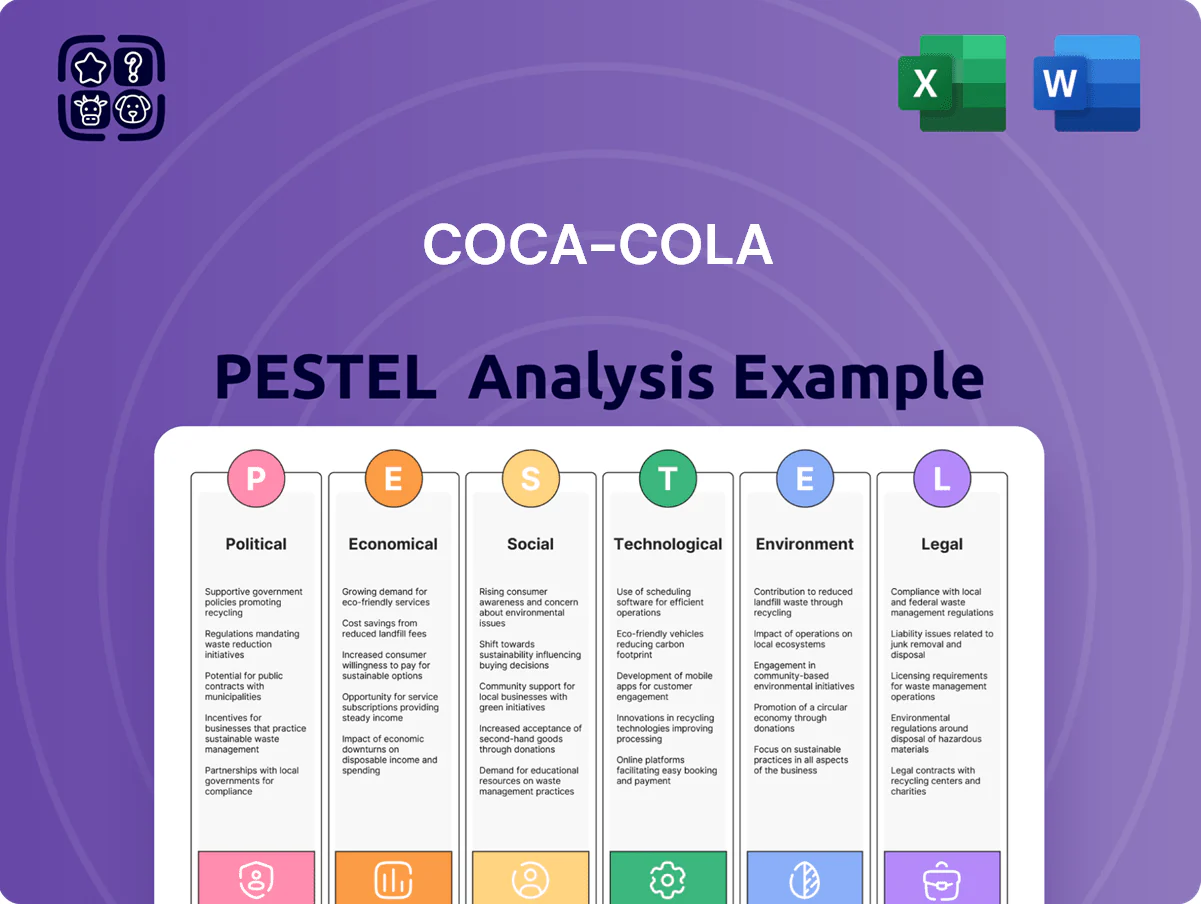

Explores how external macro-environmental factors uniquely affect Coca-Cola across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, consultants, and investors.

Clean, segmented PESTLE highlights that quickly pinpoint regulatory, economic, sociocultural, technological and environmental risks for Coca‑Cola, ready to drop into presentations or shared across teams to streamline strategy discussions and client reports.

Economic factors

Currency Exchange Rate Volatility

As a company operating in over 200 countries, Coca-Cola is highly exposed to fluctuations in the US dollar versus local currencies; a 10% average devaluation across key emerging markets in 2025 could cut reported revenue in dollar terms by roughly $1.5–2.0 billion based on 2024's $44.7 billion comparable concentrate sales base. Significant devaluations during 2025 have already pressured reported net income and reduced local consumers' purchasing power, lowering volume growth in several EMs by mid-single digits. Coca-Cola uses complex hedging, currency forwards and natural hedges through local sourcing to mitigate FX effects, but prolonged weakness versus the dollar remains a primary economic headwind that could erode margins and free cash flow in 2025.

Global Inflationary Pressures

Persistent inflation in energy, logistics, and inputs such as aluminum and high-fructose corn syrup raised Coca-Cola's cost of goods sold by an estimated 6–8% year-over-year through Q3 2025, compressing operating margins despite revenue growth. Coca-Cola's brand equity and pricing power allowed price realizations to rise about 4% globally in 2025, but management notes elasticity risks as volume declined ~1.5% in some developed markets. The company must balance further price increases with promotions and mix shifts toward premium SKUs to protect market share and margins.

Consumer Disposable Income Trends

Economic downturns and stagnating wage growth in markets like the US, Eurozone and parts of LATAM push consumers toward private-label drinks; US real median household income fell 2.3% in 2023 and remained flat into 2024, raising substitution risk for Coca-Cola.

In 2025 uneven recoveries—IMF projects global growth 3.0% in 2025 with Emerging Markets weaker—require Coca-Cola to expand lower-priced SKUs and smaller pack sizes in price-sensitive regions.

Close monitoring of CPI, unemployment and real wage trends enables dynamic shifts in Coca-Cola’s portfolio mix between sparkling and still beverages to protect volume and margin.

Interest Rate Environment

The US Federal Reserve policy tightening through 2024–2025 lifted benchmark rates to around 5.25–5.50% by end-2025, raising Coca-Cola’s effective borrowing costs and pressuring financing for bottling CAPEX and M&A.

Higher rates make large-scale infrastructure financing more expensive, shifting management toward prioritizing digital transformation and sustainable packaging investments with careful ROI thresholds versus share buybacks.

- End-2025 Fed funds ~5.25–5.50%

- Rising debt service increases WACC, tightening CAPEX ROI hurdles

- Trade-off: buybacks downweight if financing cost > expected returns on reinvestment

Growth in Emerging Economies

Coca‑Cola faces FX, inflation and rate squeeze—EM deval could cut $1.5–2bn revenue

Coca-Cola faces FX risk—10% EM currency devaluation in 2025 could cut reported revenue by $1.5–2.0bn versus 2024; hedges help but prolonged dollar strength erodes margins. Inflation lifted COGS ~6–8% through Q3 2025; price realizations rose ~4% but volume fell ~1.5% in some developed markets. Higher rates (Fed funds ~5.25–5.50% end‑2025) raise WACC and capex costs while growing middle classes in India/Africa drive long‑term demand.

| Metric | Value |

|---|---|

| 2024 comparable sales base | $44.7bn |

| Potential revenue hit (10% EM deval) | $1.5–2.0bn |

| COGS increase (YTD 2025) | 6–8% |

| Price realization (2025) | ~4% |

| Volume decline (developed markets) | ~1.5% |

| Fed funds (end‑2025) | 5.25–5.50% |

| India middle class by 2030 | ~600m |

Full Version Awaits

Coca-Cola PESTLE Analysis

The preview shown here is the exact Coca‑Cola PESTLE document you’ll receive after purchase—fully formatted and ready to use. This file contains the same analysis, structure, and visuals displayed in the preview, covering Political, Economic, Social, Technological, Legal, and Environmental factors. No placeholders or teasers—what you see is the final, professionally structured report. You’ll be able to download this exact document immediately after payment.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Coca-Cola faces intensifying regulatory scrutiny, shifting consumer tastes toward healthier options, and supply-chain volatility—while digital marketing and sustainability investments create new growth avenues; our PESTLE distills these forces into strategic insights. Purchase the full PESTLE Analysis to get a comprehensive, actionable breakdown that informs investment theses, competitive strategy, and risk management. Download now for ready-to-use, expert research.

Political factors

Geopolitical Trade Tensions

Ongoing trade disputes and protectionist measures in markets like China and the EU raised input costs for Coca-Cola, contributing to a 3.8% increase in cost of goods sold in 2024 versus 2023 and pressuring margins in its concentrates segment.

By late 2025 shifting tariffs and renegotiated trade terms affected cross-border concentrate shipments, with international operating margins varying by up to 220 basis points across regions.

Stable diplomatic relations remain critical: disruptions risk supply-chain delays and sudden freight cost spikes that could erode the company’s global distribution efficiency and dilute its 2024 global net revenue of $46.0 billion.

Taxation on Sugar-Sweetened Beverages

Regulatory Scrutiny in Emerging Markets

Political instability in regions such as the Middle East and parts of Africa elevates operational risk for Coca-Cola’s bottlers and logistics; for example, disruptions in 2023 reduced distribution in some African markets by an estimated 7–10%, impacting local revenues. Coca-Cola’s localized model demands continual engagement with authorities to secure licenses and workforce safety—the company spent $120–150 million annually on compliance and community programs in 2024–2025 across emerging markets. Sudden leadership changes can trigger abrupt regulatory shifts on land use or water rights, risking production interruptions given that up to 60% of local plant inputs are region-specific.

Plastic Waste Legislation

Political mandates on Extended Producer Responsibility now force beverage makers to fund packaging end-of-life; EU rules target 30% recycled PET in bottles by 2025 and collection rates of 90% for single-use plastic bottles, while several US states ramp EPR schemes with fees up to $0.20–$0.40 per unit.

Coca-Cola must increase recycled-content sourcing and step up lobbying/compliance to avoid fines and potential $100s of millions in EPR fees and capital for recycling infrastructure.

- EU: 30% recycled PET by 2025; 90% collection target

- US: state EPR fees $0.20–$0.40/unit; expanding mandates

- Financial impact: potential hundreds of millions for compliance and fees

Labor and Employment Regulations

Rising minimum wages and strengthened labor-rights laws across markets—e.g., US federal push for $15+ and EU wage indexation trends—raise bottlers’ labor costs, squeezing Coca-Cola’s margins and increasing concentrate pricing pressure; 2024 bottling labor disputes contributed to estimated regional production slowdowns of up to 4–6% in isolated markets.

Political campaigns for collective bargaining and enhanced worker protections force Coca-Cola to sustain stringent ESG and supplier-audit programs; failure risks reputational losses and retail delistings that can cut local sales by several percentage points.

Navigating diverse labor regimes is essential to prevent strikes and ensure supply continuity: proactive labor engagement and contingency capacity planning helped the company avoid major global disruptions during 2023–2025, limiting lost production to under 1% annually.

- Higher minimum wages and labor protections raise bottler operating costs and margin pressure

- Stronger collective-bargaining movements demand robust ESG/supplier audits to protect brand

- Effective labor relations and contingency planning minimized global disruption to <1% lost production (2023–2025)

Coca-Cola faces rising costs, taxes and tariffs; $46B revenue but margins squeezed

Political risks—trade disputes, sugar taxes, EPR mandates, wage hikes, and regional instability—raised Coca-Cola’s 2024–25 costs and pressured margins: COGS +3.8% (2024), global revenue $46.0B (2024), tariffs drove ±220bps margin variance (2025), SSB taxes in 70+ jurisdictions affecting ~$12B sales, EPR compliance risk in the hundreds of millions.

| Metric | Value |

|---|---|

| 2024 global revenue | $46.0B |

| COGS change 2024 vs 2023 | +3.8% |

| Regional margin variance (2025) | ±220bps |

| SSB-affected sales | $12B |

| EPR cost risk | $100sM |

What is included in the product

Explores how external macro-environmental factors uniquely affect Coca-Cola across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, consultants, and investors.

Clean, segmented PESTLE highlights that quickly pinpoint regulatory, economic, sociocultural, technological and environmental risks for Coca‑Cola, ready to drop into presentations or shared across teams to streamline strategy discussions and client reports.

Economic factors

Currency Exchange Rate Volatility

As a company operating in over 200 countries, Coca-Cola is highly exposed to fluctuations in the US dollar versus local currencies; a 10% average devaluation across key emerging markets in 2025 could cut reported revenue in dollar terms by roughly $1.5–2.0 billion based on 2024's $44.7 billion comparable concentrate sales base. Significant devaluations during 2025 have already pressured reported net income and reduced local consumers' purchasing power, lowering volume growth in several EMs by mid-single digits. Coca-Cola uses complex hedging, currency forwards and natural hedges through local sourcing to mitigate FX effects, but prolonged weakness versus the dollar remains a primary economic headwind that could erode margins and free cash flow in 2025.

Global Inflationary Pressures

Persistent inflation in energy, logistics, and inputs such as aluminum and high-fructose corn syrup raised Coca-Cola's cost of goods sold by an estimated 6–8% year-over-year through Q3 2025, compressing operating margins despite revenue growth. Coca-Cola's brand equity and pricing power allowed price realizations to rise about 4% globally in 2025, but management notes elasticity risks as volume declined ~1.5% in some developed markets. The company must balance further price increases with promotions and mix shifts toward premium SKUs to protect market share and margins.

Consumer Disposable Income Trends

Economic downturns and stagnating wage growth in markets like the US, Eurozone and parts of LATAM push consumers toward private-label drinks; US real median household income fell 2.3% in 2023 and remained flat into 2024, raising substitution risk for Coca-Cola.

In 2025 uneven recoveries—IMF projects global growth 3.0% in 2025 with Emerging Markets weaker—require Coca-Cola to expand lower-priced SKUs and smaller pack sizes in price-sensitive regions.

Close monitoring of CPI, unemployment and real wage trends enables dynamic shifts in Coca-Cola’s portfolio mix between sparkling and still beverages to protect volume and margin.

Interest Rate Environment

The US Federal Reserve policy tightening through 2024–2025 lifted benchmark rates to around 5.25–5.50% by end-2025, raising Coca-Cola’s effective borrowing costs and pressuring financing for bottling CAPEX and M&A.

Higher rates make large-scale infrastructure financing more expensive, shifting management toward prioritizing digital transformation and sustainable packaging investments with careful ROI thresholds versus share buybacks.

- End-2025 Fed funds ~5.25–5.50%

- Rising debt service increases WACC, tightening CAPEX ROI hurdles

- Trade-off: buybacks downweight if financing cost > expected returns on reinvestment

Growth in Emerging Economies

Coca‑Cola faces FX, inflation and rate squeeze—EM deval could cut $1.5–2bn revenue

Coca-Cola faces FX risk—10% EM currency devaluation in 2025 could cut reported revenue by $1.5–2.0bn versus 2024; hedges help but prolonged dollar strength erodes margins. Inflation lifted COGS ~6–8% through Q3 2025; price realizations rose ~4% but volume fell ~1.5% in some developed markets. Higher rates (Fed funds ~5.25–5.50% end‑2025) raise WACC and capex costs while growing middle classes in India/Africa drive long‑term demand.

| Metric | Value |

|---|---|

| 2024 comparable sales base | $44.7bn |

| Potential revenue hit (10% EM deval) | $1.5–2.0bn |

| COGS increase (YTD 2025) | 6–8% |

| Price realization (2025) | ~4% |

| Volume decline (developed markets) | ~1.5% |

| Fed funds (end‑2025) | 5.25–5.50% |

| India middle class by 2030 | ~600m |

Full Version Awaits

Coca-Cola PESTLE Analysis

The preview shown here is the exact Coca‑Cola PESTLE document you’ll receive after purchase—fully formatted and ready to use. This file contains the same analysis, structure, and visuals displayed in the preview, covering Political, Economic, Social, Technological, Legal, and Environmental factors. No placeholders or teasers—what you see is the final, professionally structured report. You’ll be able to download this exact document immediately after payment.