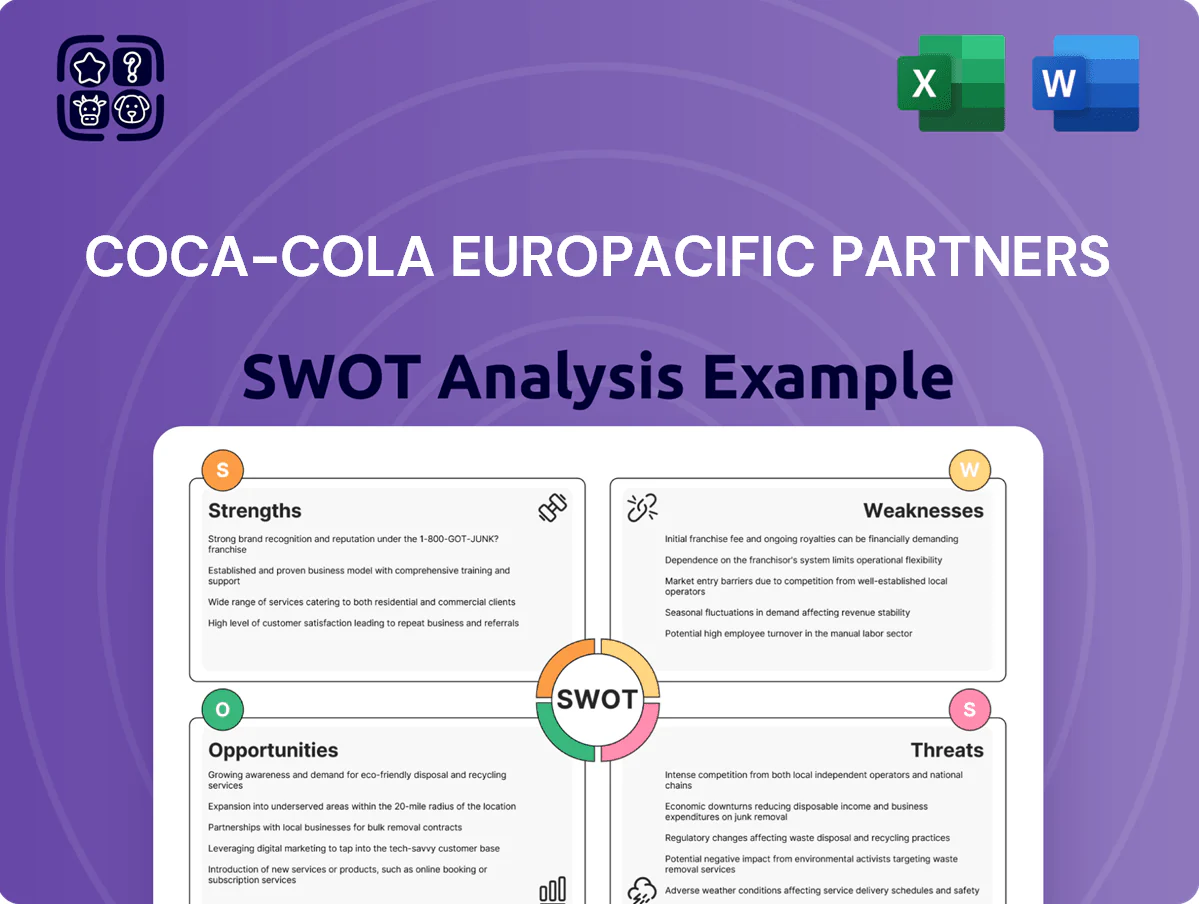

Coca-Cola Europacific Partners SWOT Analysis

Make Insightful Decisions Backed by Expert Research

Coca‑Cola Europacific Partners combines a dominant distribution network and strong brand portfolio with cost-efficiency gains from scale, but faces sugar‑tax pressures, supply-chain risks, and intense local competition.

Our full SWOT unpacks revenue levers, margin sensitivities, and market-specific threats—essential for investors, strategists, and advisors seeking actionable clarity.

Purchase the comprehensive, editable SWOT (Word + Excel) to model scenarios, support pitches, and make data-driven decisions with confidence.

Strengths

Dominant Market Position and Unrivaled Scale

As one of the largest independent Coca‑Cola bottlers worldwide, Coca‑Cola Europacific Partners (CCEP) uses scale to cut costs across production and logistics, serving ~600 million consumers and generating €13.6bn revenue in 2024. This size gives strong bargaining power with suppliers and retailers across Europe and Asia‑Pacific, lowering input costs and securing shelf space. By end‑2025, its dense route‑to‑market network is a high barrier for smaller rivals.

Diversified Geographic Footprint across Multiple Continents

The 2023 acquisition of Coca-Cola Amatil turned Coca-Cola Europacific Partners into a multi-continental player, giving exposure to stable Western Europe (≈€11.2bn 2024 revenue in EMEA) for steady cash flow and to Indonesia/Papua New Guinea for volume growth (APAC volumes grew ~5% in 2024); this mix reduces single-market regulatory and economic risk and balances developed-market value with emerging-market volume, supporting resilient earnings and long-term volume upside.

Strong Strategic Alignment with The Coca-Cola Company

The company benefits from a deep partnership with The Coca‑Cola Company, holding exclusive bottling and distribution rights for Coca‑Cola, Fanta, Sprite and others, covering 29 countries and serving ~583 million consumers as of 2024.

That alliance gives access to global marketing, product R&D and 2024 global brand investment programs, so CCEP avoids full brand‑building costs and focuses on operations.

Aligned long‑term goals let the bottler leverage iconic trademarks while pursuing cost efficiencies and market leadership; in 2024 CCEP reported net revenue €14.2bn and adjusted EBIT margin 11.8%, showing the synergy’s payoff.

Robust Multi-Category Portfolio and Brand Equity

Coca-Cola Europacific Partners (CCEP) pairs core sparkling drinks with energy, juice, water, and ready-to-drink coffee—notably Monster Energy and Costa Coffee—broadening reach into high-margin, faster-growing segments and matching shifting tastes.

This multi-category mix reduces reliance on one product line and supported 2025 blended pricing power, helping sustain margins despite 3–5% regional inflation pressures.

- Portfolio: sparkling, energy, juice, water, RTD coffee

- Key partners: Monster Energy, Costa Coffee

- Benefit: access to high-margin growth

- 2025: sustained premium pricing vs 3–5% inflation

Advanced Digital Infrastructure and B2B Platforms

Significant investments in digital transformation have produced My.CCEP, a B2B platform handling ~25% of orders in 2024 and cutting order processing times by ~30%.

Real-time analytics and AI-driven supply-chain insights improved inventory turns by 12% and raised on-shelf availability, boosting retailer promo ROI.

These tools cut operational friction, lifted service levels, and strengthened retailer relationships across 28 European and Pacific markets.

- My.CCEP: ~25% orders (2024)

- Order time down ~30%

- Inventory turns +12%

- 28 markets served

CCEP: Scale, Coke exclusivity & digital ops drive €13.6–14.2bn growth and APAC +5%

CCEP leverages scale, exclusive Coca‑Cola rights and multi‑category brands to serve ~600M consumers; 2024 revenue €13.6–14.2bn, adj. EBIT margin 11.8%, APAC volumes +5% (2024). Digital tools: My.CCEP ~25% orders, order times −30%, inventory turns +12%. Acquisition of Coca‑Cola Amatil (2023) adds APAC growth and diversifies cash flows.

| Metric | Value |

|---|---|

| Consumers | ~600M |

| Revenue 2024 | €13.6–14.2bn |

| Adj. EBIT margin | 11.8% |

| APAC volume 2024 | +5% |

| My.CCEP orders | ~25% |

What is included in the product

Delivers a concise SWOT overview of Coca-Cola Europacific Partners, mapping its operational strengths and weaknesses alongside market opportunities and external threats shaping its strategic position.

Provides a concise SWOT matrix for Coca‑Cola Europacific Partners to speed strategic alignment and stakeholder briefings.

Weaknesses

Significant Concentration Risk and Dependency

The business model is structurally dependent on The Coca-Cola Company via licensing and brand health; in 2024 CCEP derived ~98% of revenue from Coca-Cola branded concentrates and syrup agreements, amplifying concentration risk. Any strategic shift or reputational hit to Coca-Cola would materially affect CCEP’s volumes and margins—CCEP’s EV/EBITDA moved 9% in 2024 on brand-related volume volatility. The bottler lacks control over core marketing and formulation, leaving valuation sensitive to decisions in Atlanta rather than CCEP’s own operations.

High Debt Profile Following Major Acquisitions

The financing of large Asia-Pacific acquisitions pushed net debt to about €9.8bn as of year-end 2024, leaving CCEP reliant on steady free cash flow to cover interest and maintain target leverage around 2.0x net debt/EBITDA.

High rates raise annual interest expense—each 100bp rise adds roughly €98m—so service costs climb and deleveraging plans slow, tightening budget headroom for capex and marketing.

This debt commitment constrains near-term ability to pursue further large M&A, unless sell-downs or equity raises materially cut leverage.

Vulnerability to Mature Market Stagnation

Operational Complexity in Emerging Markets

Expanding into Indonesia exposes CCEP to fragmented retail and logistics across 17,000+ islands, raising distribution costs; Indonesia accounted for about 7% of group volume in 2024, but per-unit logistics costs there are estimated 20–30% higher than Europe.

Different regulations, wide income gaps, and strong local rivals force tailored pricing and promotions, pressuring margins and adding earnings volatility; managing 10,000+ local staff segments increases HR complexity and compliance risk.

- Higher logistics cost: +20–30% vs Europe

- Market scale: 17,000+ islands

- 2024 volume share ~7%

- Large local workforce & regulatory variance

Exposure to Input Cost Inflation and Supply Chain Disruptions

Coca-Cola Europacific Partners (CCEP) is highly exposed to aluminum, sugar and PET price swings; in 2024 aluminum rose ~35% YoY and PET feedstock up ~22%, pressuring CCEP’s gross margins despite hedges. Prolonged commodity inflation that cannot be passed to consumers risks margin compression; CCEP reported input cost headwinds of ~€550m in 2023–24. Geopolitical and climate-driven supply shocks also disrupt production and distribution, challenging price competitiveness.

- Aluminum +35% (2024)

- PET feedstock +22% (2024)

- Input cost headwind ≈ €550m (2023–24)

- Hedging mitigates but may not offset prolonged spikes

CCEP: Coca‑Cola dependency, €9.8bn debt, commodity shock wipes €550m

CCEP depends on The Coca‑Cola Company for ~98% of 2024 revenue, concentrating brand and formulation risk; EV/EBITDA swung ~9% in 2024 on brand-driven volumes. Net debt ≈ €9.8bn YE‑2024 (target leverage ~2.0x), with each 100bp hike adding ~€98m in interest; higher rates and debt limit M&A and capex. Western Europe ≈55% revenue, low single‑digit volume growth; Indonesia ≈7% volume with 20–30% higher logistics costs. Commodity shocks (Al +35%, PET +22% in 2024) created ≈€550m input headwinds.

| Metric | 2024/Note |

|---|---|

| Coca‑Cola revenue share | ~98% |

| Net debt | €9.8bn |

| Leverage target | ~2.0x ND/EBITDA |

| Rate sensitivity | €98m per 100bp |

| Western Europe rev share | ~55% |

| Indonesia vol share | ~7% |

| Logistics premium (Indonesia) | +20–30% |

| Aluminum change | +35% YoY |

| PET feedstock change | +22% YoY |

| Input cost headwind | ≈€550m (2023–24) |

Same Document Delivered

Coca-Cola Europacific Partners SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, editable content included in your download. Buy now to unlock the complete, in-depth Coca-Cola Europacific Partners SWOT analysis for immediate use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Insightful Decisions Backed by Expert Research

Coca‑Cola Europacific Partners combines a dominant distribution network and strong brand portfolio with cost-efficiency gains from scale, but faces sugar‑tax pressures, supply-chain risks, and intense local competition.

Our full SWOT unpacks revenue levers, margin sensitivities, and market-specific threats—essential for investors, strategists, and advisors seeking actionable clarity.

Purchase the comprehensive, editable SWOT (Word + Excel) to model scenarios, support pitches, and make data-driven decisions with confidence.

Strengths

Dominant Market Position and Unrivaled Scale

As one of the largest independent Coca‑Cola bottlers worldwide, Coca‑Cola Europacific Partners (CCEP) uses scale to cut costs across production and logistics, serving ~600 million consumers and generating €13.6bn revenue in 2024. This size gives strong bargaining power with suppliers and retailers across Europe and Asia‑Pacific, lowering input costs and securing shelf space. By end‑2025, its dense route‑to‑market network is a high barrier for smaller rivals.

Diversified Geographic Footprint across Multiple Continents

The 2023 acquisition of Coca-Cola Amatil turned Coca-Cola Europacific Partners into a multi-continental player, giving exposure to stable Western Europe (≈€11.2bn 2024 revenue in EMEA) for steady cash flow and to Indonesia/Papua New Guinea for volume growth (APAC volumes grew ~5% in 2024); this mix reduces single-market regulatory and economic risk and balances developed-market value with emerging-market volume, supporting resilient earnings and long-term volume upside.

Strong Strategic Alignment with The Coca-Cola Company

The company benefits from a deep partnership with The Coca‑Cola Company, holding exclusive bottling and distribution rights for Coca‑Cola, Fanta, Sprite and others, covering 29 countries and serving ~583 million consumers as of 2024.

That alliance gives access to global marketing, product R&D and 2024 global brand investment programs, so CCEP avoids full brand‑building costs and focuses on operations.

Aligned long‑term goals let the bottler leverage iconic trademarks while pursuing cost efficiencies and market leadership; in 2024 CCEP reported net revenue €14.2bn and adjusted EBIT margin 11.8%, showing the synergy’s payoff.

Robust Multi-Category Portfolio and Brand Equity

Coca-Cola Europacific Partners (CCEP) pairs core sparkling drinks with energy, juice, water, and ready-to-drink coffee—notably Monster Energy and Costa Coffee—broadening reach into high-margin, faster-growing segments and matching shifting tastes.

This multi-category mix reduces reliance on one product line and supported 2025 blended pricing power, helping sustain margins despite 3–5% regional inflation pressures.

- Portfolio: sparkling, energy, juice, water, RTD coffee

- Key partners: Monster Energy, Costa Coffee

- Benefit: access to high-margin growth

- 2025: sustained premium pricing vs 3–5% inflation

Advanced Digital Infrastructure and B2B Platforms

Significant investments in digital transformation have produced My.CCEP, a B2B platform handling ~25% of orders in 2024 and cutting order processing times by ~30%.

Real-time analytics and AI-driven supply-chain insights improved inventory turns by 12% and raised on-shelf availability, boosting retailer promo ROI.

These tools cut operational friction, lifted service levels, and strengthened retailer relationships across 28 European and Pacific markets.

- My.CCEP: ~25% orders (2024)

- Order time down ~30%

- Inventory turns +12%

- 28 markets served

CCEP: Scale, Coke exclusivity & digital ops drive €13.6–14.2bn growth and APAC +5%

CCEP leverages scale, exclusive Coca‑Cola rights and multi‑category brands to serve ~600M consumers; 2024 revenue €13.6–14.2bn, adj. EBIT margin 11.8%, APAC volumes +5% (2024). Digital tools: My.CCEP ~25% orders, order times −30%, inventory turns +12%. Acquisition of Coca‑Cola Amatil (2023) adds APAC growth and diversifies cash flows.

| Metric | Value |

|---|---|

| Consumers | ~600M |

| Revenue 2024 | €13.6–14.2bn |

| Adj. EBIT margin | 11.8% |

| APAC volume 2024 | +5% |

| My.CCEP orders | ~25% |

What is included in the product

Delivers a concise SWOT overview of Coca-Cola Europacific Partners, mapping its operational strengths and weaknesses alongside market opportunities and external threats shaping its strategic position.

Provides a concise SWOT matrix for Coca‑Cola Europacific Partners to speed strategic alignment and stakeholder briefings.

Weaknesses

Significant Concentration Risk and Dependency

The business model is structurally dependent on The Coca-Cola Company via licensing and brand health; in 2024 CCEP derived ~98% of revenue from Coca-Cola branded concentrates and syrup agreements, amplifying concentration risk. Any strategic shift or reputational hit to Coca-Cola would materially affect CCEP’s volumes and margins—CCEP’s EV/EBITDA moved 9% in 2024 on brand-related volume volatility. The bottler lacks control over core marketing and formulation, leaving valuation sensitive to decisions in Atlanta rather than CCEP’s own operations.

High Debt Profile Following Major Acquisitions

The financing of large Asia-Pacific acquisitions pushed net debt to about €9.8bn as of year-end 2024, leaving CCEP reliant on steady free cash flow to cover interest and maintain target leverage around 2.0x net debt/EBITDA.

High rates raise annual interest expense—each 100bp rise adds roughly €98m—so service costs climb and deleveraging plans slow, tightening budget headroom for capex and marketing.

This debt commitment constrains near-term ability to pursue further large M&A, unless sell-downs or equity raises materially cut leverage.

Vulnerability to Mature Market Stagnation

Operational Complexity in Emerging Markets

Expanding into Indonesia exposes CCEP to fragmented retail and logistics across 17,000+ islands, raising distribution costs; Indonesia accounted for about 7% of group volume in 2024, but per-unit logistics costs there are estimated 20–30% higher than Europe.

Different regulations, wide income gaps, and strong local rivals force tailored pricing and promotions, pressuring margins and adding earnings volatility; managing 10,000+ local staff segments increases HR complexity and compliance risk.

- Higher logistics cost: +20–30% vs Europe

- Market scale: 17,000+ islands

- 2024 volume share ~7%

- Large local workforce & regulatory variance

Exposure to Input Cost Inflation and Supply Chain Disruptions

Coca-Cola Europacific Partners (CCEP) is highly exposed to aluminum, sugar and PET price swings; in 2024 aluminum rose ~35% YoY and PET feedstock up ~22%, pressuring CCEP’s gross margins despite hedges. Prolonged commodity inflation that cannot be passed to consumers risks margin compression; CCEP reported input cost headwinds of ~€550m in 2023–24. Geopolitical and climate-driven supply shocks also disrupt production and distribution, challenging price competitiveness.

- Aluminum +35% (2024)

- PET feedstock +22% (2024)

- Input cost headwind ≈ €550m (2023–24)

- Hedging mitigates but may not offset prolonged spikes

CCEP: Coca‑Cola dependency, €9.8bn debt, commodity shock wipes €550m

CCEP depends on The Coca‑Cola Company for ~98% of 2024 revenue, concentrating brand and formulation risk; EV/EBITDA swung ~9% in 2024 on brand-driven volumes. Net debt ≈ €9.8bn YE‑2024 (target leverage ~2.0x), with each 100bp hike adding ~€98m in interest; higher rates and debt limit M&A and capex. Western Europe ≈55% revenue, low single‑digit volume growth; Indonesia ≈7% volume with 20–30% higher logistics costs. Commodity shocks (Al +35%, PET +22% in 2024) created ≈€550m input headwinds.

| Metric | 2024/Note |

|---|---|

| Coca‑Cola revenue share | ~98% |

| Net debt | €9.8bn |

| Leverage target | ~2.0x ND/EBITDA |

| Rate sensitivity | €98m per 100bp |

| Western Europe rev share | ~55% |

| Indonesia vol share | ~7% |

| Logistics premium (Indonesia) | +20–30% |

| Aluminum change | +35% YoY |

| PET feedstock change | +22% YoY |

| Input cost headwind | ≈€550m (2023–24) |

Same Document Delivered

Coca-Cola Europacific Partners SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, editable content included in your download. Buy now to unlock the complete, in-depth Coca-Cola Europacific Partners SWOT analysis for immediate use.