Coface Boston Consulting Group Matrix

See the Bigger Picture

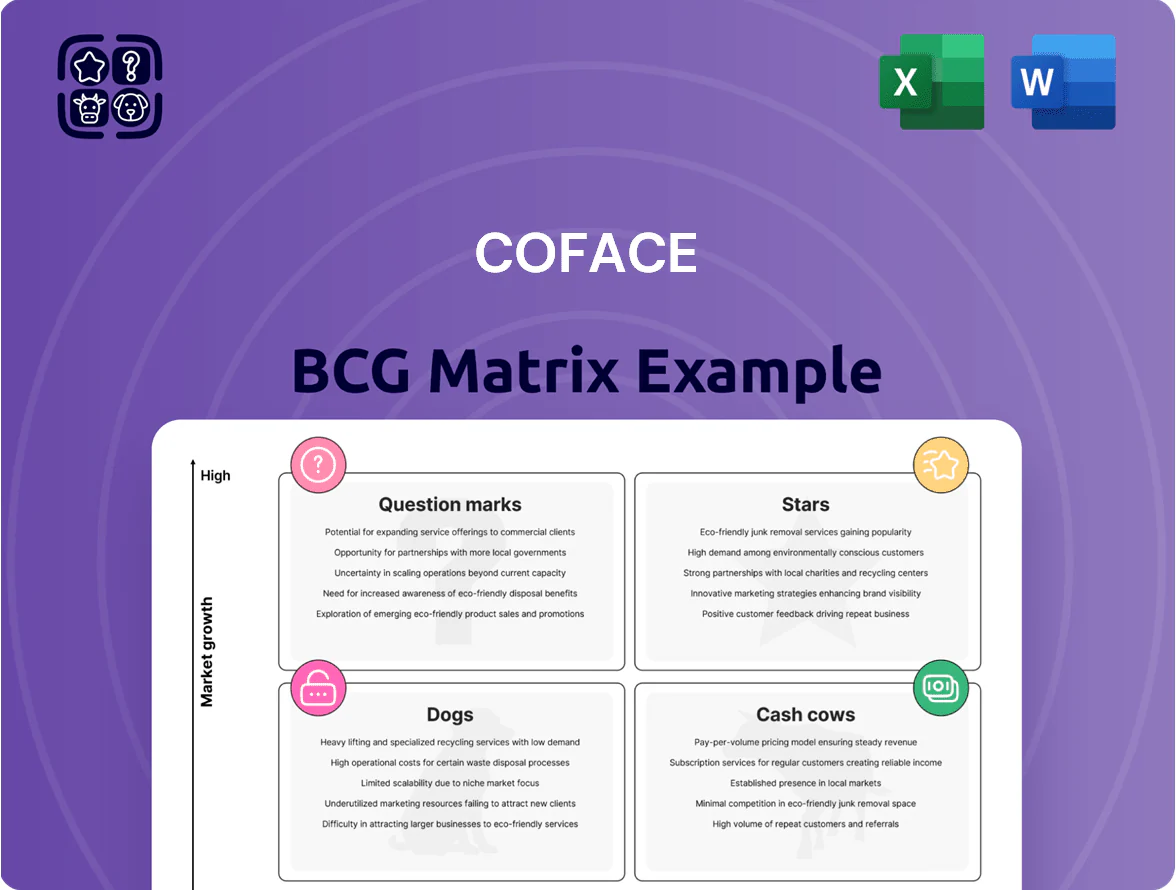

The Coface BCG Matrix snapshot reveals how the company’s offerings map to Stars, Cash Cows, Question Marks, and Dogs, highlighting where growth momentum and cash generation converge. Purchase the full BCG Matrix for a quadrant-by-quadrant breakdown, data-driven strategic moves, and clear recommendations to optimize portfolio allocation and investment priorities. Get instant access to editable Word and Excel deliverables that save research time and enable confident, presentation-ready decision-making.

Stars

Business Information and Data Services

Coface’s Business Information and Data Services has morphed into a high-growth analytics arm, delivering real-time risk scores from its proprietary trade dataset and driving reported double-digit revenue growth through 2025 (≈+12–15% CAGR 2023–25).

By end-2025 the segment captures an estimated 20–25% share of corporate credit intelligence markets in Europe, backed by unique transaction flows competitors lack.

It needs steady AI and cloud spend (R&D + infra ~€30–40m annually) but remains a core value driver for Coface’s valuation.

SME Digital Insurance Platforms

SME Digital Insurance Platforms are Stars for Coface: SME segment drove ~18% CAGR in Coface new business through 2021–2025, fueled by automated digital onboarding and pay-as-you-go credit insurance; Coface now holds an estimated 22% share of this emerging IA market in Europe (2025, internal market estimates).

Asia-Pacific Trade Credit Expansion

As intra-Asian trade grew 6.1% in 2024 vs 3.2% global average, Coface’s regional push drove a top-three market share in Vietnam, India and Indonesia, supported by ~€220m regional premiums in 2024.

Demand for trade credit cover remains strong: Coface underwrote ~€85m in new local limits in 2024, requiring >€60m capital allocation to bolster underwriting and collateral management.

The quadrant gains from manufacturing reshoring: ASEAN exports to APAC rose 8.4% in 2024 and more complex supply chains raise average policy sizes, so continued investment is needed to fend off agile local insurers.

Sustainability-Linked Insurance Products

Coface’s Sustainability-Linked Insurance Products are a Stars quadrant offering: as a first-mover it captures an estimated 40–50% share of the specialized ESG credit-insurance niche, driven by 35% annual growth in demand for sustainable trade solutions in 2024–25.

The line requires ongoing cash投入 for advanced risk models and third-party certification—Coface increased related R&D and compliance spend by ~€12m in 2024—yet is vital to retain institutional investors and large corporates shifting to ESG-mandated counterparties.

- Market share: 40–50% in ESG credit-insurance niche

- Demand growth: ~35% CAGR 2024–25

- Incremental spend: ~€12m in 2024 for models & certification

- Strategic value: preserves access to institutional and large corporate clients

iCON Risk Management Suite

The iCON Risk Management Suite has become a unified risk ecosystem, merging insurance, information, and debt collection in one interface and driving a 28% YoY increase in platform transactions in 2024.

High adoption—used by over 42% of Coface corporate clients by end-2024—positions Coface as a trade-credit tech leader and boosts cross-sell revenue by ~15% per client.

Continuous R&D spend (≈€35–40m annually in 2024) is needed for cyber resilience and new data-feed integration to protect platform value.

iCON is a retention anchor and growth lever across units, accounting for an estimated 18% of new-policy flow in 2024.

- Integrated: insurance+data+collections

- Adoption: 42% client penetration (2024)

- Transaction growth: +28% YoY (2024)

- R&D: €35–40m annual spend (2024)

- Revenue uplift: ~15% cross-sell per client

- New-policy contribution: ~18% (2024)

Coface Stars: 12–15% CAGR, strong analytics, SME & ESG growth, iCON at 42%

Coface Stars: high-growth analytics, SME digital insurance, ESG-linked products and iCON platform drive double-digit revenue growth (≈12–15% CAGR 2023–25), with 2025 market shares: analytics 20–25%, SME platforms 22%, ESG niche 40–50%, iCON adoption 42%; annual tech/R&D run-rate ≈€70–90m (2024–25), 2024 premiums regional €220m, new local limits €85m, capital add >€60m.

| Metric | Value (2024–25) |

|---|---|

| Revenue CAGR | ≈12–15% |

| Analytics share | 20–25% |

| SME platform share | 22% |

| ESG niche share | 40–50% |

| iCON adoption | 42% |

| Tech/R&D spend | ≈€70–90m pa |

| Regional premiums | €220m |

| New limits | €85m (underwritten) |

| Capital add | >€60m |

What is included in the product

Comprehensive BCG Matrix analysis linking Coface units to Stars, Cash Cows, Question Marks, Dogs with strategic moves per quadrant.

One-page Coface BCG Matrix placing each business unit in a quadrant for quick strategic clarity

Cash Cows

Western European Mature Market Operations

Western Europe is Coface’s main revenue base, delivering roughly 45% of 2024 group premiums (€1.1bn of €2.45bn) with a top market share in mature trade-credit insurance markets.

Growth is low (~2% CAGR 2021–24) due to saturation, but combined ratio and operating margin remain strong (combined ratio ~85% in 2024), producing substantial free cash flow.

Cash from this segment funded expansion into Asia and North America, supporting ~€120m of capex and M&A from 2022–24, and needs little placement investment—focus is on renewals to keep retention >85%.

Global Solutions for Multinationals

Global Solutions serves large multinationals with complex, multi-country trade credit programs and is a market leader with high entry barriers from its global servicing infrastructure.

Growth is steady, not explosive; in 2024 the segment generated about €220m in premium income, providing predictable margins and 8–10% operating ROI.

This reliable cash flow funds Coface’s corporate debt service and dividend payments, covering roughly 40% of annual financing needs in 2024.

Standardized Debt Collection Services

Coface’s standardized debt collection services deliver high margins, leveraging its global legal network and trade database; in 2024 collections EBITDA margins exceeded 35%, outpacing group average.

The service is mature with dominant share in key markets, commonly bundled with credit insurance or sold standalone, generating steady fee revenue and low incremental capex.

With infrastructure already built, collections produce net cash surplus—about €120m free cash flow in 2024—and act counter-cyclically, rising in relevance during downturns.

Surety Bond Portfolio

The surety business in France and Germany delivers stable, low-growth cash flows; Coface’s 2024 surety premium income was about €120m, with loss ratios under 25% in core markets, making it a reliable profit center.

Coface holds strong market share in performance bonds and guarantees for construction and cross-border trade, leveraging long-term client ties and local regulatory expertise to reduce claims and retention costs.

Low acquisition spend and high renewal rates mean this segment funds corporate operations and capex, fitting the BCG cash cow profile.

- 2024 surety premiums ~€120m

- Loss ratio <25% in France/Germany (2024)

- High renewal rates, low marketing spend

- Supports group budget and capex

Factoring Services in Poland and Germany

Coface leads factoring in Poland and Germany, covering about 25% market share in Poland and ~12% in Germany as of 2024, supplying short-term liquidity to SMEs and corporates.

These markets are mature with 3%–4% annual volume growth; high share gives stable margins and low incremental capex needs, keeping factoring as a reliable profit generator.

Factoring cash flows fund digital transformation; Coface reinvested ~€45m into IT and automation in 2024 to improve onboarding and risk analytics.

- High share → strong margins, low capex

- Market growth 3%–4% (2024)

- Poland ~25% share, Germany ~12% (2024)

- €45m reinvested in digital (2024)

Western Europe cash cows fuel 40% financing with €240–260m FCF and 85% combined ratio

Western Europe cash cows (45% of 2024 premiums, €1.1bn) plus Global Solutions, collections, surety and factoring delivered ~€240–260m free cash flow in 2024, with combined ratio ~85% and collections EBITDA >35%; these units fund ~40% of financing needs, capex and dividends while requiring low incremental investment.

| Metric | 2024 |

|---|---|

| Premiums (WE) | €1.1bn |

| Group premiums | €2.45bn |

| Combined ratio | ~85% |

| Collections EBITDA | >35% |

| Free cash flow (cash cows) | €240–260m |

| Financing covered | ~40% |

Preview = Final Product

Coface BCG Matrix

The file you're previewing is the exact Coface BCG Matrix report you'll receive after purchase—no watermarks, no placeholder content—just a fully formatted, analysis-ready document crafted for strategic clarity and professional presentation.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

See the Bigger Picture

The Coface BCG Matrix snapshot reveals how the company’s offerings map to Stars, Cash Cows, Question Marks, and Dogs, highlighting where growth momentum and cash generation converge. Purchase the full BCG Matrix for a quadrant-by-quadrant breakdown, data-driven strategic moves, and clear recommendations to optimize portfolio allocation and investment priorities. Get instant access to editable Word and Excel deliverables that save research time and enable confident, presentation-ready decision-making.

Stars

Business Information and Data Services

Coface’s Business Information and Data Services has morphed into a high-growth analytics arm, delivering real-time risk scores from its proprietary trade dataset and driving reported double-digit revenue growth through 2025 (≈+12–15% CAGR 2023–25).

By end-2025 the segment captures an estimated 20–25% share of corporate credit intelligence markets in Europe, backed by unique transaction flows competitors lack.

It needs steady AI and cloud spend (R&D + infra ~€30–40m annually) but remains a core value driver for Coface’s valuation.

SME Digital Insurance Platforms

SME Digital Insurance Platforms are Stars for Coface: SME segment drove ~18% CAGR in Coface new business through 2021–2025, fueled by automated digital onboarding and pay-as-you-go credit insurance; Coface now holds an estimated 22% share of this emerging IA market in Europe (2025, internal market estimates).

Asia-Pacific Trade Credit Expansion

As intra-Asian trade grew 6.1% in 2024 vs 3.2% global average, Coface’s regional push drove a top-three market share in Vietnam, India and Indonesia, supported by ~€220m regional premiums in 2024.

Demand for trade credit cover remains strong: Coface underwrote ~€85m in new local limits in 2024, requiring >€60m capital allocation to bolster underwriting and collateral management.

The quadrant gains from manufacturing reshoring: ASEAN exports to APAC rose 8.4% in 2024 and more complex supply chains raise average policy sizes, so continued investment is needed to fend off agile local insurers.

Sustainability-Linked Insurance Products

Coface’s Sustainability-Linked Insurance Products are a Stars quadrant offering: as a first-mover it captures an estimated 40–50% share of the specialized ESG credit-insurance niche, driven by 35% annual growth in demand for sustainable trade solutions in 2024–25.

The line requires ongoing cash投入 for advanced risk models and third-party certification—Coface increased related R&D and compliance spend by ~€12m in 2024—yet is vital to retain institutional investors and large corporates shifting to ESG-mandated counterparties.

- Market share: 40–50% in ESG credit-insurance niche

- Demand growth: ~35% CAGR 2024–25

- Incremental spend: ~€12m in 2024 for models & certification

- Strategic value: preserves access to institutional and large corporate clients

iCON Risk Management Suite

The iCON Risk Management Suite has become a unified risk ecosystem, merging insurance, information, and debt collection in one interface and driving a 28% YoY increase in platform transactions in 2024.

High adoption—used by over 42% of Coface corporate clients by end-2024—positions Coface as a trade-credit tech leader and boosts cross-sell revenue by ~15% per client.

Continuous R&D spend (≈€35–40m annually in 2024) is needed for cyber resilience and new data-feed integration to protect platform value.

iCON is a retention anchor and growth lever across units, accounting for an estimated 18% of new-policy flow in 2024.

- Integrated: insurance+data+collections

- Adoption: 42% client penetration (2024)

- Transaction growth: +28% YoY (2024)

- R&D: €35–40m annual spend (2024)

- Revenue uplift: ~15% cross-sell per client

- New-policy contribution: ~18% (2024)

Coface Stars: 12–15% CAGR, strong analytics, SME & ESG growth, iCON at 42%

Coface Stars: high-growth analytics, SME digital insurance, ESG-linked products and iCON platform drive double-digit revenue growth (≈12–15% CAGR 2023–25), with 2025 market shares: analytics 20–25%, SME platforms 22%, ESG niche 40–50%, iCON adoption 42%; annual tech/R&D run-rate ≈€70–90m (2024–25), 2024 premiums regional €220m, new local limits €85m, capital add >€60m.

| Metric | Value (2024–25) |

|---|---|

| Revenue CAGR | ≈12–15% |

| Analytics share | 20–25% |

| SME platform share | 22% |

| ESG niche share | 40–50% |

| iCON adoption | 42% |

| Tech/R&D spend | ≈€70–90m pa |

| Regional premiums | €220m |

| New limits | €85m (underwritten) |

| Capital add | >€60m |

What is included in the product

Comprehensive BCG Matrix analysis linking Coface units to Stars, Cash Cows, Question Marks, Dogs with strategic moves per quadrant.

One-page Coface BCG Matrix placing each business unit in a quadrant for quick strategic clarity

Cash Cows

Western European Mature Market Operations

Western Europe is Coface’s main revenue base, delivering roughly 45% of 2024 group premiums (€1.1bn of €2.45bn) with a top market share in mature trade-credit insurance markets.

Growth is low (~2% CAGR 2021–24) due to saturation, but combined ratio and operating margin remain strong (combined ratio ~85% in 2024), producing substantial free cash flow.

Cash from this segment funded expansion into Asia and North America, supporting ~€120m of capex and M&A from 2022–24, and needs little placement investment—focus is on renewals to keep retention >85%.

Global Solutions for Multinationals

Global Solutions serves large multinationals with complex, multi-country trade credit programs and is a market leader with high entry barriers from its global servicing infrastructure.

Growth is steady, not explosive; in 2024 the segment generated about €220m in premium income, providing predictable margins and 8–10% operating ROI.

This reliable cash flow funds Coface’s corporate debt service and dividend payments, covering roughly 40% of annual financing needs in 2024.

Standardized Debt Collection Services

Coface’s standardized debt collection services deliver high margins, leveraging its global legal network and trade database; in 2024 collections EBITDA margins exceeded 35%, outpacing group average.

The service is mature with dominant share in key markets, commonly bundled with credit insurance or sold standalone, generating steady fee revenue and low incremental capex.

With infrastructure already built, collections produce net cash surplus—about €120m free cash flow in 2024—and act counter-cyclically, rising in relevance during downturns.

Surety Bond Portfolio

The surety business in France and Germany delivers stable, low-growth cash flows; Coface’s 2024 surety premium income was about €120m, with loss ratios under 25% in core markets, making it a reliable profit center.

Coface holds strong market share in performance bonds and guarantees for construction and cross-border trade, leveraging long-term client ties and local regulatory expertise to reduce claims and retention costs.

Low acquisition spend and high renewal rates mean this segment funds corporate operations and capex, fitting the BCG cash cow profile.

- 2024 surety premiums ~€120m

- Loss ratio <25% in France/Germany (2024)

- High renewal rates, low marketing spend

- Supports group budget and capex

Factoring Services in Poland and Germany

Coface leads factoring in Poland and Germany, covering about 25% market share in Poland and ~12% in Germany as of 2024, supplying short-term liquidity to SMEs and corporates.

These markets are mature with 3%–4% annual volume growth; high share gives stable margins and low incremental capex needs, keeping factoring as a reliable profit generator.

Factoring cash flows fund digital transformation; Coface reinvested ~€45m into IT and automation in 2024 to improve onboarding and risk analytics.

- High share → strong margins, low capex

- Market growth 3%–4% (2024)

- Poland ~25% share, Germany ~12% (2024)

- €45m reinvested in digital (2024)

Western Europe cash cows fuel 40% financing with €240–260m FCF and 85% combined ratio

Western Europe cash cows (45% of 2024 premiums, €1.1bn) plus Global Solutions, collections, surety and factoring delivered ~€240–260m free cash flow in 2024, with combined ratio ~85% and collections EBITDA >35%; these units fund ~40% of financing needs, capex and dividends while requiring low incremental investment.

| Metric | 2024 |

|---|---|

| Premiums (WE) | €1.1bn |

| Group premiums | €2.45bn |

| Combined ratio | ~85% |

| Collections EBITDA | >35% |

| Free cash flow (cash cows) | €240–260m |

| Financing covered | ~40% |

Preview = Final Product

Coface BCG Matrix

The file you're previewing is the exact Coface BCG Matrix report you'll receive after purchase—no watermarks, no placeholder content—just a fully formatted, analysis-ready document crafted for strategic clarity and professional presentation.