Cognex Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

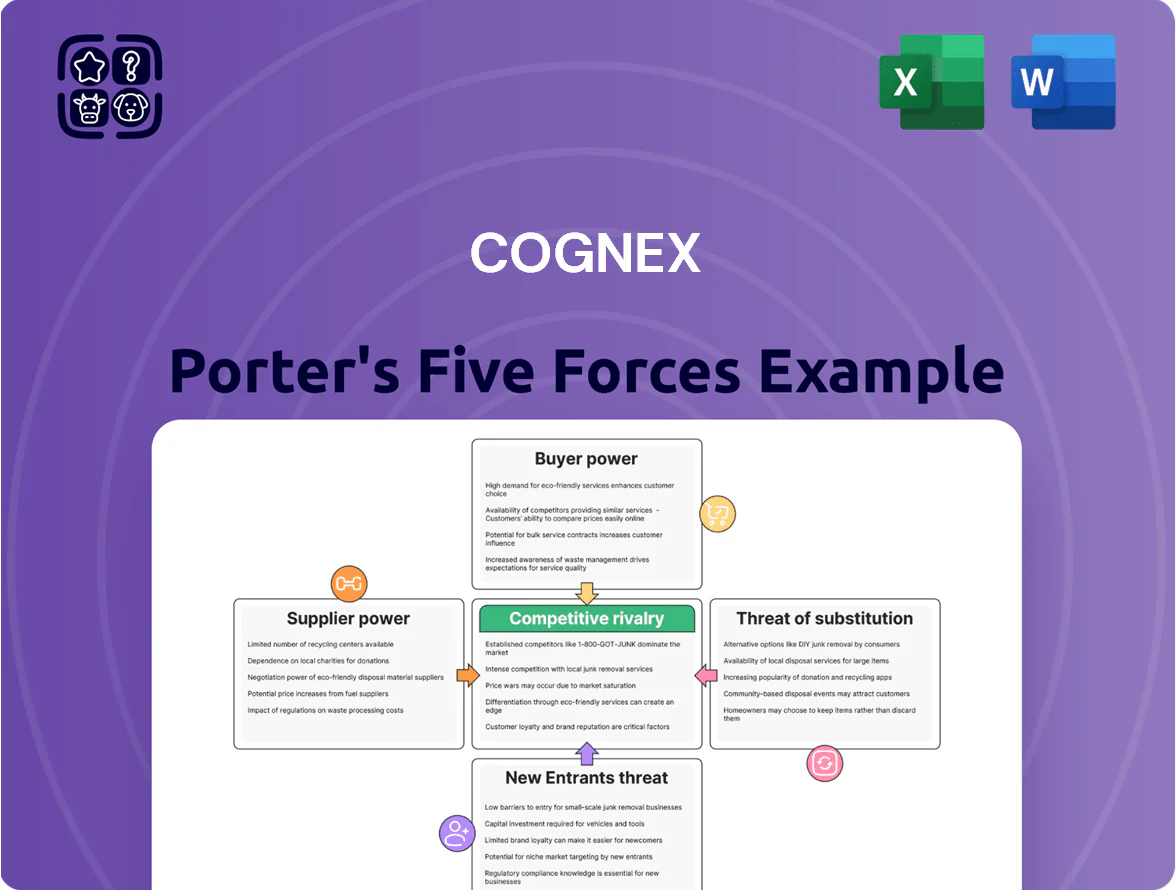

Cognex operates in a high-tech vision systems market where supplier specialization, moderate buyer leverage, and steady threat from substitutes shape margins and innovation incentives.

This snapshot highlights competitive intensity, technological barriers, and scale advantages but only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable strategy recommendations tailored to Cognex.

Suppliers Bargaining Power

Specialized semiconductor and sensor components

Cognex depends on specialized image sensors and high-performance processors made by few global foundries, giving suppliers moderate leverage over pricing and lead times; in 2024 global semiconductor capacity utilization hit ~85%, raising risk of delays.

Although Cognex designs proprietary ASICs, wafer fabrication is outsourced, so supplier constraints can cause production bottlenecks and affect gross margin—Cognex reported 71.6% gross margin in FY2024, so a 2–3% margin hit from shortages would be material.

Software and AI talent pool

The primary input for Cognex's value is engineers in deep learning and computer vision; by 2025 global AI specialist demand grew ~40% year-over-year, keeping supplier (talent) bargaining power high and pushing R&D wage bills up — Cognex reported R&D expense of $155m in FY2024, up 18% from 2023. Retention/recruiting costs remain material: average US AI engineer pay exceeded $180k in 2025, so Cognex must invest heavily to stay competitive in a tight global market.

Proprietary optical hardware assembly

The manufacturing of high-precision lenses and optical housings relies on a narrow set of specialized vendors that meet strict industrial-quality standards, making supplier selection critical for Cognex (CGNX). Because lenses materially affect system accuracy, a supplier failure can trigger switching costs including requalification, recalls, and up to several months of lost shipments; Cognex reported 2024 revenue of $1.1B, so disruptions could hit material margins quickly. This dependency concentrates bargaining power with few high-quality optics makers who also understand industrial automation tolerances and certification needs. As a result, supplier leverage raises input risk and can pressure lead times and pricing.

Geopolitical supply chain risks

- 62% of critical-part spend in East Asia (2024 audit)

- Diversified sourcing to North America/Europe since 2022

- Single-territory concentration raises price and lead-time risk

Low volume relative to consumer electronics

Cognex sells far fewer units than consumer electronics giants (Apple shipped ~220M iPhones in 2024), so Tier‑1 component makers give priority to larger buyers, reducing Cognex’s bargaining leverage and driving higher per‑unit costs.

During 2023–24 capacity tightness for semiconductors, Cognex reported longer lead times and worked up inventories to cover ~6–9 months of supply or paid spot premiums of 10–25% for key generic parts.

- Lower volumes → less supplier leverage

- Suppliers favor high‑volume clients

- Inventory 6–9 months or pay 10–25% premiums

Cognex supplier risks: East Asia concentration, chip capacity tightness, rising input costs

Cognex faces moderate-to-high supplier power: 62% of critical-part spend tied to East Asia (2024), semiconductor capacity use ~85% (2024), FY2024 gross margin 71.6% and R&D $155M; shortages previously forced 6–9 months inventory or 10–25% spot premiums, and US AI engineer pay >$180k (2025), all raising input cost and lead‑time risk.

| Metric | Value |

|---|---|

| East Asia spend (2024) | 62% |

| Semiconductor capacity (2024) | ~85% |

| Gross margin (FY2024) | 71.6% |

| R&D (FY2024) | $155M |

| Inventory cover / premiums (2023–24) | 6–9 months / 10–25% |

| Avg US AI engineer pay (2025) | >$180k |

What is included in the product

Tailored Porter's Five Forces analysis for Cognex that uncovers competitive intensity, buyer/supplier power, substitution risks, and entry barriers, highlighting disruptive threats, pricing influence, and strategic levers to protect market share.

A concise Porter's Five Forces snapshot for Cognex—visualize competitive pressures and buy-side/supplier risks at a glance to speed strategic decisions.

Customers Bargaining Power

Concentration in automotive and logistics sectors

A large share of Cognex’s revenue comes from major automotive and logistics clients; in 2024 roughly 45% of machine vision demand tied to automotive/warehouse automation concentrated buying power, so these customers can push price and custom specs.

Large contracts (often >$1m) let buyers demand tailored systems and longer payment terms, squeezing margins and product roadmaps. If a top logistics customer delays or reroutes automation spend, Cognex’s quarterly revenue can swing several percentage points.

High switching costs for integrated systems

Once a factory or distribution center embeds Cognex machine vision into PLCs and conveyors, switching costs rise sharply—estimates show industrial vision retrofit can cost $50k–$300k per line plus 2–6 weeks downtime. Deep integration and bespoke operator training create technical lock-in, so existing clients wield less bargaining power than new prospects. In 2025 Cognex reported recurring software-enabled revenue growth, reinforcing sticky customer relationships.

Price sensitivity in commoditized segments

In commoditized barcode scanners and low-end vision sensors, buyers face low switching costs and high price sensitivity, which compresses margins; IDC reported 2024 unit-price declines of ~6% YoY for basic barcode scanners. Competitors supply 'good enough' hardware, forcing Cognex to defend pricing on features and service, while competitive bidding is common—Procurement RFQs often cut hardware spend by 10–25% in industrial accounts.

Demand for comprehensive ROI and performance

Sophisticated buyers now demand quantifiable ROI—typically a 15–30% throughput lift or a 40–70% drop in error rates—before greenlighting large Cognex deployments, raising the bar for proof points.

As AI-enabled vision spreads, customers benchmark Cognex vs rivals on KPIs like read rates and processing speed; third-party tests in 2024 showed top read-rate gaps of 3–8 percentage points, enabling performance-based comparisons.

This KPI transparency strengthens buyer leverage, letting them negotiate price or service credits tied to performance-to-price ratios and SLAs.

- Buyers expect 15–30% throughput gains

- Expect 40–70% error reduction

- 2024 tests: 3–8pp read-rate gaps

- Negotiation via performance-linked pricing

Direct vs. Distribution channel dynamics

Cognex sells via a direct sales force and ~200 global distributors/integrators, letting direct enterprise buyers (higher revenue per account; >$1M deals) exert strong price and service demands while distributors aggregate hundreds of smaller OEMs with near-zero individual bargaining power.

The dual-channel mix supported Cognex’s 2024 gross margin of 74.6%, keeping margins higher across segments by routing low-value, price-sensitive orders through distributors and reserving direct engagement for high-margin, custom deployments.

- Direct sales: high leverage, large deals (> $1M)

- Distributors: aggregate small buyers, low bargaining power

- ~200 distributors globally (integrators included)

- 2024 gross margin: 74.6% (source: Cognex 2024 10-K)

Cognex: Strong margins amid big-account leverage and falling scanner prices

Cognex faces mixed customer bargaining power: large automotive/logistics accounts (45% of market demand in 2024) and >$1M contracts exert strong price/spec leverage, while embedded systems create high switching costs (~$50k–$300k per line). Commodity scanners drive price pressure (2024 unit-price decline ~6%). 2024 gross margin: 74.6%.

| Metric | Value |

|---|---|

| Top-sector share | 45% (2024) |

| Switch cost per line | $50k–$300k |

| Scanner price decline | ~6% YoY (2024) |

| Gross margin | 74.6% (2024) |

Same Document Delivered

Cognex Porter's Five Forces Analysis

This preview shows the exact Cognex Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professional, and ready for use without surprises or placeholders.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Cognex operates in a high-tech vision systems market where supplier specialization, moderate buyer leverage, and steady threat from substitutes shape margins and innovation incentives.

This snapshot highlights competitive intensity, technological barriers, and scale advantages but only scratches the surface—unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable strategy recommendations tailored to Cognex.

Suppliers Bargaining Power

Specialized semiconductor and sensor components

Cognex depends on specialized image sensors and high-performance processors made by few global foundries, giving suppliers moderate leverage over pricing and lead times; in 2024 global semiconductor capacity utilization hit ~85%, raising risk of delays.

Although Cognex designs proprietary ASICs, wafer fabrication is outsourced, so supplier constraints can cause production bottlenecks and affect gross margin—Cognex reported 71.6% gross margin in FY2024, so a 2–3% margin hit from shortages would be material.

Software and AI talent pool

The primary input for Cognex's value is engineers in deep learning and computer vision; by 2025 global AI specialist demand grew ~40% year-over-year, keeping supplier (talent) bargaining power high and pushing R&D wage bills up — Cognex reported R&D expense of $155m in FY2024, up 18% from 2023. Retention/recruiting costs remain material: average US AI engineer pay exceeded $180k in 2025, so Cognex must invest heavily to stay competitive in a tight global market.

Proprietary optical hardware assembly

The manufacturing of high-precision lenses and optical housings relies on a narrow set of specialized vendors that meet strict industrial-quality standards, making supplier selection critical for Cognex (CGNX). Because lenses materially affect system accuracy, a supplier failure can trigger switching costs including requalification, recalls, and up to several months of lost shipments; Cognex reported 2024 revenue of $1.1B, so disruptions could hit material margins quickly. This dependency concentrates bargaining power with few high-quality optics makers who also understand industrial automation tolerances and certification needs. As a result, supplier leverage raises input risk and can pressure lead times and pricing.

Geopolitical supply chain risks

- 62% of critical-part spend in East Asia (2024 audit)

- Diversified sourcing to North America/Europe since 2022

- Single-territory concentration raises price and lead-time risk

Low volume relative to consumer electronics

Cognex sells far fewer units than consumer electronics giants (Apple shipped ~220M iPhones in 2024), so Tier‑1 component makers give priority to larger buyers, reducing Cognex’s bargaining leverage and driving higher per‑unit costs.

During 2023–24 capacity tightness for semiconductors, Cognex reported longer lead times and worked up inventories to cover ~6–9 months of supply or paid spot premiums of 10–25% for key generic parts.

- Lower volumes → less supplier leverage

- Suppliers favor high‑volume clients

- Inventory 6–9 months or pay 10–25% premiums

Cognex supplier risks: East Asia concentration, chip capacity tightness, rising input costs

Cognex faces moderate-to-high supplier power: 62% of critical-part spend tied to East Asia (2024), semiconductor capacity use ~85% (2024), FY2024 gross margin 71.6% and R&D $155M; shortages previously forced 6–9 months inventory or 10–25% spot premiums, and US AI engineer pay >$180k (2025), all raising input cost and lead‑time risk.

| Metric | Value |

|---|---|

| East Asia spend (2024) | 62% |

| Semiconductor capacity (2024) | ~85% |

| Gross margin (FY2024) | 71.6% |

| R&D (FY2024) | $155M |

| Inventory cover / premiums (2023–24) | 6–9 months / 10–25% |

| Avg US AI engineer pay (2025) | >$180k |

What is included in the product

Tailored Porter's Five Forces analysis for Cognex that uncovers competitive intensity, buyer/supplier power, substitution risks, and entry barriers, highlighting disruptive threats, pricing influence, and strategic levers to protect market share.

A concise Porter's Five Forces snapshot for Cognex—visualize competitive pressures and buy-side/supplier risks at a glance to speed strategic decisions.

Customers Bargaining Power

Concentration in automotive and logistics sectors

A large share of Cognex’s revenue comes from major automotive and logistics clients; in 2024 roughly 45% of machine vision demand tied to automotive/warehouse automation concentrated buying power, so these customers can push price and custom specs.

Large contracts (often >$1m) let buyers demand tailored systems and longer payment terms, squeezing margins and product roadmaps. If a top logistics customer delays or reroutes automation spend, Cognex’s quarterly revenue can swing several percentage points.

High switching costs for integrated systems

Once a factory or distribution center embeds Cognex machine vision into PLCs and conveyors, switching costs rise sharply—estimates show industrial vision retrofit can cost $50k–$300k per line plus 2–6 weeks downtime. Deep integration and bespoke operator training create technical lock-in, so existing clients wield less bargaining power than new prospects. In 2025 Cognex reported recurring software-enabled revenue growth, reinforcing sticky customer relationships.

Price sensitivity in commoditized segments

In commoditized barcode scanners and low-end vision sensors, buyers face low switching costs and high price sensitivity, which compresses margins; IDC reported 2024 unit-price declines of ~6% YoY for basic barcode scanners. Competitors supply 'good enough' hardware, forcing Cognex to defend pricing on features and service, while competitive bidding is common—Procurement RFQs often cut hardware spend by 10–25% in industrial accounts.

Demand for comprehensive ROI and performance

Sophisticated buyers now demand quantifiable ROI—typically a 15–30% throughput lift or a 40–70% drop in error rates—before greenlighting large Cognex deployments, raising the bar for proof points.

As AI-enabled vision spreads, customers benchmark Cognex vs rivals on KPIs like read rates and processing speed; third-party tests in 2024 showed top read-rate gaps of 3–8 percentage points, enabling performance-based comparisons.

This KPI transparency strengthens buyer leverage, letting them negotiate price or service credits tied to performance-to-price ratios and SLAs.

- Buyers expect 15–30% throughput gains

- Expect 40–70% error reduction

- 2024 tests: 3–8pp read-rate gaps

- Negotiation via performance-linked pricing

Direct vs. Distribution channel dynamics

Cognex sells via a direct sales force and ~200 global distributors/integrators, letting direct enterprise buyers (higher revenue per account; >$1M deals) exert strong price and service demands while distributors aggregate hundreds of smaller OEMs with near-zero individual bargaining power.

The dual-channel mix supported Cognex’s 2024 gross margin of 74.6%, keeping margins higher across segments by routing low-value, price-sensitive orders through distributors and reserving direct engagement for high-margin, custom deployments.

- Direct sales: high leverage, large deals (> $1M)

- Distributors: aggregate small buyers, low bargaining power

- ~200 distributors globally (integrators included)

- 2024 gross margin: 74.6% (source: Cognex 2024 10-K)

Cognex: Strong margins amid big-account leverage and falling scanner prices

Cognex faces mixed customer bargaining power: large automotive/logistics accounts (45% of market demand in 2024) and >$1M contracts exert strong price/spec leverage, while embedded systems create high switching costs (~$50k–$300k per line). Commodity scanners drive price pressure (2024 unit-price decline ~6%). 2024 gross margin: 74.6%.

| Metric | Value |

|---|---|

| Top-sector share | 45% (2024) |

| Switch cost per line | $50k–$300k |

| Scanner price decline | ~6% YoY (2024) |

| Gross margin | 74.6% (2024) |

Same Document Delivered

Cognex Porter's Five Forces Analysis

This preview shows the exact Cognex Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professional, and ready for use without surprises or placeholders.