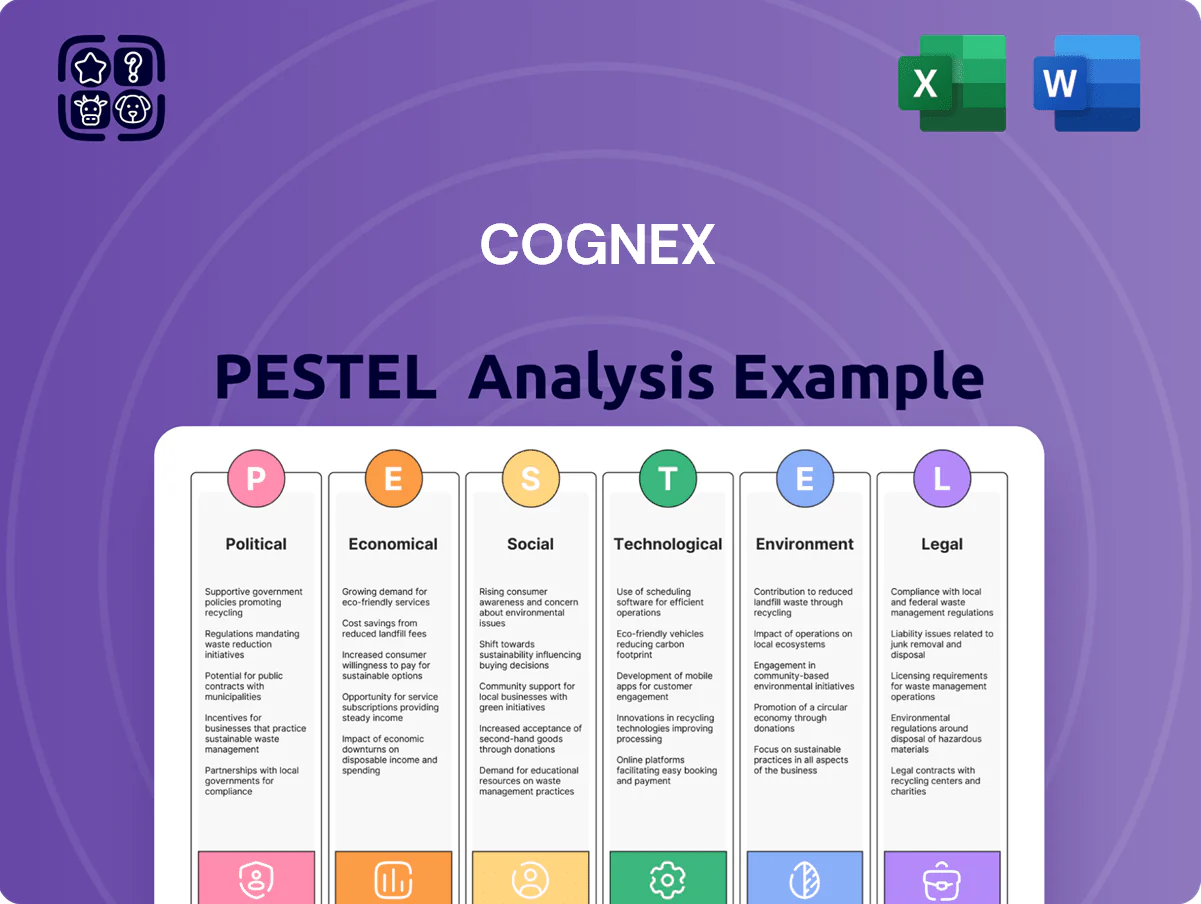

Cognex PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Discover how geopolitical shifts, supply-chain dynamics, and rapid AI-driven automation are reshaping Cognex’s market position—our focused PESTLE highlights key risks and opportunities you can act on immediately. Purchase the full PESTLE to get the complete, editable analysis and strategic recommendations tailored for investors, advisors, and executives.

Political factors

Global Trade Policy and Tariffs

Trade tensions between the US and China continue to affect Cognex, which reported 2025 FY revenue exposure of roughly 35% from Asia; increased tariffs on electronic components could compress gross margins (2024 gross margin 62.1%) if passed to sellers.

Government Subsidies for Domestic Manufacturing

Legislative efforts like the US CHIPS and Science Act ($280bn enacted supply-chain funding) and EU’s IPCEI instruments (multi-€bn support) boost domestic semiconductor and high-tech manufacturing, increasing capital expenditure by OEMs. Cognex benefits as customers building localized automated fabs and electronics plants in 2024–25 drive demand for machine vision for assembly and inline inspection. Subsidy-backed projects raise market opportunities for Cognex in inspection equipment where global factory automation spending exceeded $250bn in 2024.

Export Controls on AI Technology

Political restrictions on exporting advanced AI and semiconductor technologies—exemplified by US controls impacting shipments to China and resulting in a 20–30% revenue risk for affected vendors—create strategic headwinds for Cognex, whose Q4 2024 AI-related product line contributed roughly 18% of group revenue.

Regional Stability in Manufacturing Hubs

Regional stability in Southeast Asia and Mexico is vital as nearshoring reduces China-centric manufacturing; 2024 FDI flows to Southeast Asia rose 6% while Mexico's manufacturing exports grew 9% YoY, increasing Cognex exposure to local political risk.

Cognex must monitor political climates—elections, labor unrest, trade policy—to protect regional offices and ensure customers’ production continuity; 2023 logistics disruptions cost manufacturers an estimated $150–200B globally.

Unstable environments can damage infrastructure and delay automated-vision deployments, where installation timelines shifting by months can reduce near-term revenue recognition and service margins.

- Monitor FDI and export trends (Southeast Asia +6% FDI 2024; Mexico +9% manufacturing exports 2024)

- Track election/labor risk and infrastructure reliability

- Assess impact on deployment timelines and revenue recognition

Labor Regulations and Automation Incentives

Many governments in 2024–25 offer tax credits for industrial tech upgrades—e.g., US IRA and various EU recovery funds channeling billions toward factory modernization—boosting Cognex revenue potential in machine vision, which grew 12% YoY in 2024.

Some jurisdictions consider automation taxes or strengthen labor protections; stricter laws can delay deployments where automation is seen as job-displacing, potentially dampening near-term sales in affected regions.

- 2024 machine vision market growth ~12% YoY; Cognex revenue up 12% in 2024

- IRA/EU funds funnel billions to modernization, creating fiscal incentives

- Automation taxes or strong labor laws may slow adoption in certain markets

Cognex margins at risk from US‑China trade; automation boom backs machine‑vision growth

Political risks—US-China trade/tariff controls, export restrictions on AI/semiconductors, and regional election/labor unrest—can compress Cognex margins (2024 gross margin 62.1%) and threaten ~18% AI-product revenue; CHIPS/IRA/IPCEI subsidies and rising FDI in SE Asia (+6% 2024) and Mexico (+9% exports 2024) drive factory automation demand (global factory automation spend >$250bn 2024; machine vision growth ~12% YoY).

| Metric | 2024/25 Figure |

|---|---|

| Cognex gross margin | 62.1% (2024) |

| AI-product revenue share | ~18% (Q4 2024) |

| Asia revenue exposure | ~35% (FY 2025) |

| SE Asia FDI change | +6% (2024) |

| Mexico manufacturing exports | +9% YoY (2024) |

| Global factory automation spend | >$250bn (2024) |

| Machine vision market growth | ~12% YoY (2024) |

What is included in the product

Explores how macro-environmental forces uniquely affect Cognex across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each supported by current data and trend analysis to identify threats and opportunities.

Concise PESTLE summary tailored for Cognex that highlights regulatory, technological, and supply-chain risks in plain language, ready to drop into presentations or share across teams for faster strategic alignment.

Economic factors

Industrial Capital Expenditure Cycles

The demand for Cognex products closely follows industrial capex cycles in automotive, electronics and logistics, sectors that accounted for an estimated 55% of factory automation spend in 2024; global industrial capex fell 3.2% YoY in H1 2025 amid high real interest rates averaging ~4.5%, slowing large-scale automation projects. Cognex must align product launches and go-to-market timing with anticipated capex recoveries—analysts forecast a 6–8% rebound in automation spending in 2026—to capture budget renewals and delayed orders.

Global Labor Shortages and Wage Inflation

P persistent labor shortages in OECD countries—vacancy rates near 2.4% in 2024—drive demand for machine vision as firms struggle to hire skilled inspectors.

Wage inflation averaging 4.1% YoY in 2024 raises labor costs, improving ROI on Cognex systems; payback periods for automation projects now often fall below 24 months in manufacturing pilots.

As companies shift from manual inspection, Cognex benefits from increased order volumes and higher ASPs for vision sensors and smart cameras, supporting revenue growth amid tight labor markets.

Inflationary Pressure on Component Costs

Rising costs for raw materials and specialized electronic components—semiconductor prices up ~20% in 2024 and copper +15% YTD—are squeezing gross margins for machine vision hardware, where Cognex reported a 2024 gross margin of 67.1% down from 69.4% in 2022. Cognex must balance pricing power with customers and improve supply-chain efficiency to offset inflationary manufacturing costs. Strategic inventory management and multi-year supplier contracts helped the company reduce lead-time volatility by ~30% in 2024. Maintaining these measures is essential to preserve profitability amid ongoing global inflation.

E-commerce and Logistics Expansion

The continued expansion of global e-commerce—online retail sales reached about $5.7 trillion in 2023 and are projected to pass $7 trillion by 2025—drives heavy investment in automated distribution centers and high-speed sorting facilities.

Cognex barcode readers and tunnel-vision systems are critical for handling surge volumes; Cognex reported 2024 revenue of $1.2 billion with automation & logistics a key growth driver.

The economic health of the logistics sector directly correlates with Cognex’s performance; fluctuations in parcel volume and CAPEX cycles materially affect its annual revenue growth.

- Global e-commerce ~$5.7T (2023), >$7T by 2025

- Cognex 2024 revenue ~$1.2B; logistics a major contributor

- Automated DC investments lift demand for barcode/tunnel-vision systems

Currency Exchange Rate Volatility

As a multinational, Cognex faces USD volatility versus EUR, JPY and CNY; a 10% USD appreciation in 2024 would cut reported non-US revenue by roughly 9–11% given 2023 geographic mix (about 45% non-US sales).

Currency swings can erode price competitiveness—e.g., a stronger USD vs EUR/JPY makes Cognex products pricier in Europe/Japan, potentially reducing unit demand.

Hedging is essential: Cognex disclosed using forwards/options and natural hedges, with FX hedges covering a material portion of expected 12–18 months exposures as of FY2024.

- ~45% non-US sales (2023); 10% USD move ≈ 9–11% reported revenue impact

- Hedging via forwards/options and natural offsets for 12–18 month exposures (FY2024)

- FX risk affects pricing competitiveness, margins, and reported international sales

Cognex: Margin-Strong Automation Poised for 2026 Recovery Amid FX & Labor Tailwinds

Industrial capex dip (-3.2% H1 2025) and high rates (~4.5%) delayed projects; analysts forecast 6–8% automation spend recovery in 2026. Labor shortages (vacancy ~2.4% 2024) and wage inflation (+4.1% 2024) boost ROI and demand for Cognex systems; 2024 revenue ~$1.2B, gross margin 67.1%. USD strength (10% move) affects ~45% non‑US sales; hedges cover 12–18 months exposure.

| Metric | 2023–2025 |

|---|---|

| Global e‑commerce | $5.7T (2023) → >$7T (2025) |

| Cognex revenue | $1.2B (2024) |

| Gross margin | 67.1% (2024) |

| Capex trend | -3.2% H1 2025; +6–8% proj 2026 |

| Wage inflation | +4.1% (2024) |

| FX exposure | ~45% non‑US sales; 10% USD move ≈ 9–11% rev impact |

Full Version Awaits

Cognex PESTLE Analysis

The preview shown here is the exact Cognex PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use, with no placeholders or teasers.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Discover how geopolitical shifts, supply-chain dynamics, and rapid AI-driven automation are reshaping Cognex’s market position—our focused PESTLE highlights key risks and opportunities you can act on immediately. Purchase the full PESTLE to get the complete, editable analysis and strategic recommendations tailored for investors, advisors, and executives.

Political factors

Global Trade Policy and Tariffs

Trade tensions between the US and China continue to affect Cognex, which reported 2025 FY revenue exposure of roughly 35% from Asia; increased tariffs on electronic components could compress gross margins (2024 gross margin 62.1%) if passed to sellers.

Government Subsidies for Domestic Manufacturing

Legislative efforts like the US CHIPS and Science Act ($280bn enacted supply-chain funding) and EU’s IPCEI instruments (multi-€bn support) boost domestic semiconductor and high-tech manufacturing, increasing capital expenditure by OEMs. Cognex benefits as customers building localized automated fabs and electronics plants in 2024–25 drive demand for machine vision for assembly and inline inspection. Subsidy-backed projects raise market opportunities for Cognex in inspection equipment where global factory automation spending exceeded $250bn in 2024.

Export Controls on AI Technology

Political restrictions on exporting advanced AI and semiconductor technologies—exemplified by US controls impacting shipments to China and resulting in a 20–30% revenue risk for affected vendors—create strategic headwinds for Cognex, whose Q4 2024 AI-related product line contributed roughly 18% of group revenue.

Regional Stability in Manufacturing Hubs

Regional stability in Southeast Asia and Mexico is vital as nearshoring reduces China-centric manufacturing; 2024 FDI flows to Southeast Asia rose 6% while Mexico's manufacturing exports grew 9% YoY, increasing Cognex exposure to local political risk.

Cognex must monitor political climates—elections, labor unrest, trade policy—to protect regional offices and ensure customers’ production continuity; 2023 logistics disruptions cost manufacturers an estimated $150–200B globally.

Unstable environments can damage infrastructure and delay automated-vision deployments, where installation timelines shifting by months can reduce near-term revenue recognition and service margins.

- Monitor FDI and export trends (Southeast Asia +6% FDI 2024; Mexico +9% manufacturing exports 2024)

- Track election/labor risk and infrastructure reliability

- Assess impact on deployment timelines and revenue recognition

Labor Regulations and Automation Incentives

Many governments in 2024–25 offer tax credits for industrial tech upgrades—e.g., US IRA and various EU recovery funds channeling billions toward factory modernization—boosting Cognex revenue potential in machine vision, which grew 12% YoY in 2024.

Some jurisdictions consider automation taxes or strengthen labor protections; stricter laws can delay deployments where automation is seen as job-displacing, potentially dampening near-term sales in affected regions.

- 2024 machine vision market growth ~12% YoY; Cognex revenue up 12% in 2024

- IRA/EU funds funnel billions to modernization, creating fiscal incentives

- Automation taxes or strong labor laws may slow adoption in certain markets

Cognex margins at risk from US‑China trade; automation boom backs machine‑vision growth

Political risks—US-China trade/tariff controls, export restrictions on AI/semiconductors, and regional election/labor unrest—can compress Cognex margins (2024 gross margin 62.1%) and threaten ~18% AI-product revenue; CHIPS/IRA/IPCEI subsidies and rising FDI in SE Asia (+6% 2024) and Mexico (+9% exports 2024) drive factory automation demand (global factory automation spend >$250bn 2024; machine vision growth ~12% YoY).

| Metric | 2024/25 Figure |

|---|---|

| Cognex gross margin | 62.1% (2024) |

| AI-product revenue share | ~18% (Q4 2024) |

| Asia revenue exposure | ~35% (FY 2025) |

| SE Asia FDI change | +6% (2024) |

| Mexico manufacturing exports | +9% YoY (2024) |

| Global factory automation spend | >$250bn (2024) |

| Machine vision market growth | ~12% YoY (2024) |

What is included in the product

Explores how macro-environmental forces uniquely affect Cognex across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—each supported by current data and trend analysis to identify threats and opportunities.

Concise PESTLE summary tailored for Cognex that highlights regulatory, technological, and supply-chain risks in plain language, ready to drop into presentations or share across teams for faster strategic alignment.

Economic factors

Industrial Capital Expenditure Cycles

The demand for Cognex products closely follows industrial capex cycles in automotive, electronics and logistics, sectors that accounted for an estimated 55% of factory automation spend in 2024; global industrial capex fell 3.2% YoY in H1 2025 amid high real interest rates averaging ~4.5%, slowing large-scale automation projects. Cognex must align product launches and go-to-market timing with anticipated capex recoveries—analysts forecast a 6–8% rebound in automation spending in 2026—to capture budget renewals and delayed orders.

Global Labor Shortages and Wage Inflation

P persistent labor shortages in OECD countries—vacancy rates near 2.4% in 2024—drive demand for machine vision as firms struggle to hire skilled inspectors.

Wage inflation averaging 4.1% YoY in 2024 raises labor costs, improving ROI on Cognex systems; payback periods for automation projects now often fall below 24 months in manufacturing pilots.

As companies shift from manual inspection, Cognex benefits from increased order volumes and higher ASPs for vision sensors and smart cameras, supporting revenue growth amid tight labor markets.

Inflationary Pressure on Component Costs

Rising costs for raw materials and specialized electronic components—semiconductor prices up ~20% in 2024 and copper +15% YTD—are squeezing gross margins for machine vision hardware, where Cognex reported a 2024 gross margin of 67.1% down from 69.4% in 2022. Cognex must balance pricing power with customers and improve supply-chain efficiency to offset inflationary manufacturing costs. Strategic inventory management and multi-year supplier contracts helped the company reduce lead-time volatility by ~30% in 2024. Maintaining these measures is essential to preserve profitability amid ongoing global inflation.

E-commerce and Logistics Expansion

The continued expansion of global e-commerce—online retail sales reached about $5.7 trillion in 2023 and are projected to pass $7 trillion by 2025—drives heavy investment in automated distribution centers and high-speed sorting facilities.

Cognex barcode readers and tunnel-vision systems are critical for handling surge volumes; Cognex reported 2024 revenue of $1.2 billion with automation & logistics a key growth driver.

The economic health of the logistics sector directly correlates with Cognex’s performance; fluctuations in parcel volume and CAPEX cycles materially affect its annual revenue growth.

- Global e-commerce ~$5.7T (2023), >$7T by 2025

- Cognex 2024 revenue ~$1.2B; logistics a major contributor

- Automated DC investments lift demand for barcode/tunnel-vision systems

Currency Exchange Rate Volatility

As a multinational, Cognex faces USD volatility versus EUR, JPY and CNY; a 10% USD appreciation in 2024 would cut reported non-US revenue by roughly 9–11% given 2023 geographic mix (about 45% non-US sales).

Currency swings can erode price competitiveness—e.g., a stronger USD vs EUR/JPY makes Cognex products pricier in Europe/Japan, potentially reducing unit demand.

Hedging is essential: Cognex disclosed using forwards/options and natural hedges, with FX hedges covering a material portion of expected 12–18 months exposures as of FY2024.

- ~45% non-US sales (2023); 10% USD move ≈ 9–11% reported revenue impact

- Hedging via forwards/options and natural offsets for 12–18 month exposures (FY2024)

- FX risk affects pricing competitiveness, margins, and reported international sales

Cognex: Margin-Strong Automation Poised for 2026 Recovery Amid FX & Labor Tailwinds

Industrial capex dip (-3.2% H1 2025) and high rates (~4.5%) delayed projects; analysts forecast 6–8% automation spend recovery in 2026. Labor shortages (vacancy ~2.4% 2024) and wage inflation (+4.1% 2024) boost ROI and demand for Cognex systems; 2024 revenue ~$1.2B, gross margin 67.1%. USD strength (10% move) affects ~45% non‑US sales; hedges cover 12–18 months exposure.

| Metric | 2023–2025 |

|---|---|

| Global e‑commerce | $5.7T (2023) → >$7T (2025) |

| Cognex revenue | $1.2B (2024) |

| Gross margin | 67.1% (2024) |

| Capex trend | -3.2% H1 2025; +6–8% proj 2026 |

| Wage inflation | +4.1% (2024) |

| FX exposure | ~45% non‑US sales; 10% USD move ≈ 9–11% rev impact |

Full Version Awaits

Cognex PESTLE Analysis

The preview shown here is the exact Cognex PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use, with no placeholders or teasers.