China Overseas Grand Oceans Group Porter's Five Forces Analysis

From Overview to Strategy Blueprint

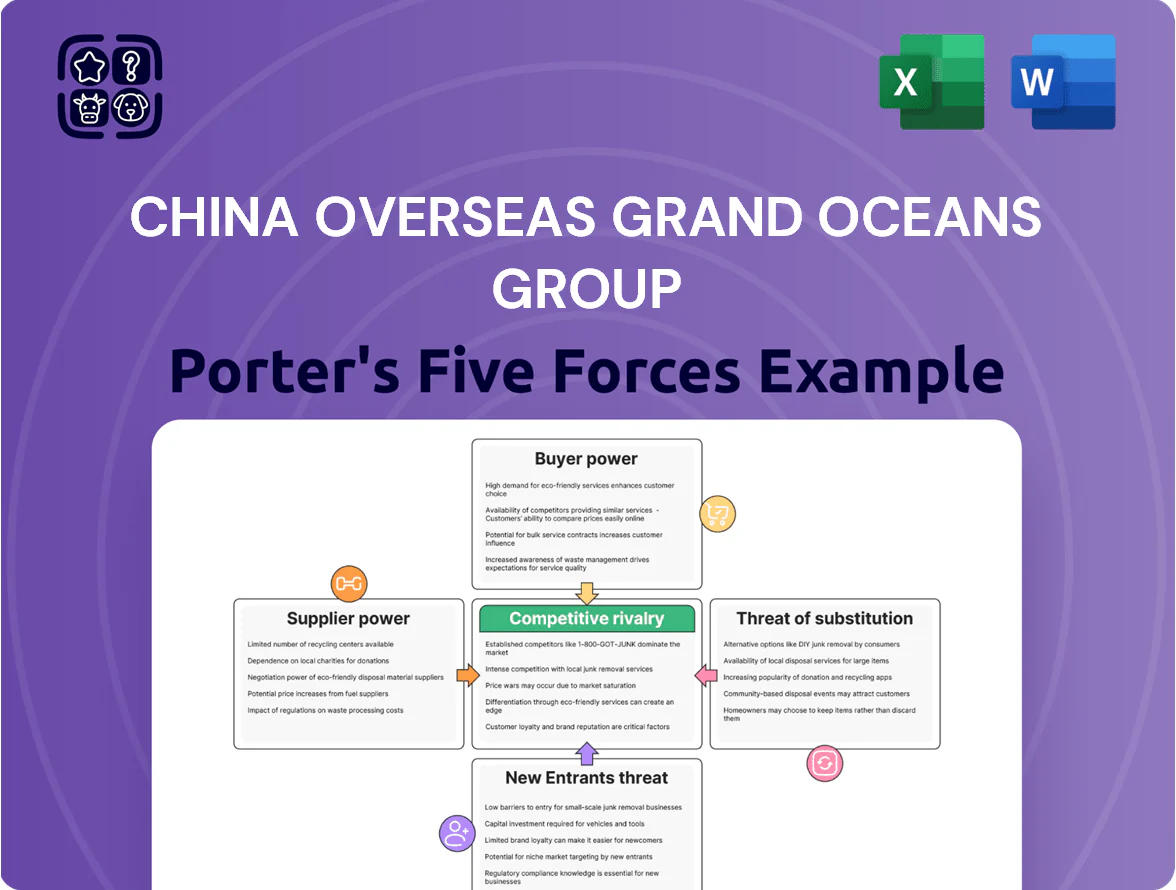

China Overseas Grand Oceans faces moderate supplier power, significant buyer sensitivity to price and service, and rising competitive rivalry amid industry consolidation; barriers to entry are mixed due to capital intensity but supportive policy, while substitutes pose limited near-term threat. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategic insights tailored to China Overseas Grand Oceans Group.

Suppliers Bargaining Power

Concentration of Land Supply

The primary supplier for China Overseas Grand Oceans is the local government, which monopolizes land auctions and urban planning; by late 2025 the centralized land supply system still sets availability and price in Tier‑3/4 cities, where land sales fell 6% YoY in 2024 and average reserve-to-sales ratios tightened to 4.2 months, giving authorities strong leverage over pricing and timelines and squeezing the group’s gross margins by an estimated 120–180 bps.

Construction Material Price Volatility

Suppliers of steel, cement and glass hold moderate bargaining power, driven by global commodity cycles and China policy; steel spot prices rose ~18% in 2024 and averaged CNY 5,200/ton by Q4 2025, lifting input costs for developers.

Stricter environmental curbs since 2023 cut high‑emission output—cement capacity utilization fell to ~70% in 2024—causing intermittent price spikes that hit margins.

China Overseas Grand Oceans offsets this via multi‑year procurement deals and JV supply partnerships; long‑term contracts covered ~40% of steel needs in 2025, reducing short‑term volatility risk.

Availability of Specialized Labor

China Overseas Grand Oceans faces rising supplier power from specialized labor as China’s working-age population fell by 3.45% between 2015 and 2023, shrinking blue-collar availability; construction wages rose about 6–8% annually in 2023–25 to attract younger workers. Contractors and labor service firms now command higher rates and stricter terms, increasing project costs and scheduling risk. The company’s heavy reliance on third-party crews for quality and deadlines makes labor a key controllable cost, accounting for an estimated 20–30% of project direct costs.

Access to Institutional Financing

Financial institutions are suppliers of capital whose leverage over China Overseas Grand Oceans Group is shaped by People’s Bank of China policy and the Three Red Lines debt controls; bank lending rates averaged 3.65% for corporate loans in 2024, raising borrowing cost pressure.

The company’s state-owned background grants stronger credit access versus private peers—China Overseas Grand Oceans, tied to China State Construction, saw yuan bond issuance of RMB 7.2bn in 2024—yet lenders enforce tight covenants on leverage and cashflow.

Debt cost and bond market access remain external constraints: a 100bp rise in yield would cut project NPV materially, limiting acquisition scale despite parent support.

- Bank loan rate 3.65% (2024)

Technological and Green Building Providers

As China mandates green building standards by 2025, suppliers of energy-efficient systems and smart-home tech wield rising power; proprietary HVAC, BMS (building management systems), and EV-charging solutions drive 15–25% higher fit-out costs but cut operational emissions 30–50% per government pilots in 2023–24.

China Overseas Grand Oceans must source from a small pool of certified high-end vendors to meet state carbon-neutral targets, leaving it dependent on supplier pricing, lead times, and integration expertise; a 2024 industry survey showed 62% of developers report supplier-concentration risks.

Key impacts: higher capex, longer procurement cycles, and potential project delays if supplier capacity tightens—especially in tier-1 cities where green premiums reached 8–12% in 2024.

- 2025 mandate raises supplier leverage

- Proprietary tech increases capex 15–25%

- Operational emissions cut 30–50% (pilots 2023–24)

- 62% developers cite supplier concentration risk (2024)

- Green premium 8–12% in tier-1 cities (2024)

Suppliers exert rising power: land tight, steel surging, labor up, bonds easing finance

Suppliers hold moderate-to-high power: local governments control land supply (reserve-to-sales 4.2 months, land sales -6% YoY 2024), materials saw steel +18% in 2024 (CNY 5,200/ton by Q4 2025) and cement capacity use ~70% in 2024, labor costs rose 6–8% annually 2023–25; multi‑year contracts covered ~40% steel in 2025, yuan bond issuance RMB 7.2bn (2024) eased financing but covenants bind.

| Metric | Value |

|---|---|

| Land reserve-to-sales | 4.2 months (2024) |

| Land sales YoY | -6% (2024) |

| Steel price | CNY 5,200/ton (Q4 2025) |

| Cement utilization | ~70% (2024) |

| Labor wage growth | 6–8% pa (2023–25) |

| Steel long contracts | ~40% (2025) |

| Yuan bonds | RMB 7.2bn (2024) |

What is included in the product

Tailored exclusively for China Overseas Grand Oceans Group, this Porter's Five Forces overview uncovers key competitive drivers, buyer/supplier influence, entry barriers, substitutes, and emerging threats shaping its port and logistics positioning.

A concise Porter's Five Forces snapshot for China Overseas Grand Oceans—quickly identify competitive pressures and strategic levers to relieve pain points.

Customers Bargaining Power

Shift Toward Buyer Market Dynamics

By end-2025 China’s housing stock overhang hit about 18 months of sales in lower-tier cities, shifting bargaining power to buyers; individual purchasers now routinely secure 5–15% price discounts and demand higher-spec finishes, raising rework risk and margin pressure for China Overseas Grand Oceans Group. The firm must prioritize on-time delivery, upgraded fit-outs, and post-sale service—areas where 1–3% margin recovery is achievable if customer satisfaction rises above industry average.

Impact of Mortgage Interest Rates

Customer purchasing power ties closely to mortgage rates and state bank lending; China Household Loan rate averaged 4.65% for new mortgages in 2024 and downpayment rules vary by city.

Beijing and Shanghai eased policies through 2025, but national outstanding mortgage growth slowed to 3.2% YoY in 2024, so buyers stay rate-sensitive.

If mortgage rates rise 100 bps or lending tightens, eligible buyers could fall by ~15–25%, forcing developers like China Overseas Grand Oceans to increase incentives and price discounts.

Rise of Secondary Market Competition

The growing inventory of pre-owned homes in China—estimated at a 12% annual rise in secondhand listings in 2024 in major coastal cities—gives buyers a ready alternative and strengthens their bargaining power against China Overseas Grand Oceans Group. Buyers weigh immediate availability and lower contingency risk of secondary units versus delivery delays in new builds, which averaged 9–14 months late in some provinces in 2023. To respond, the developer must highlight superior amenities, smart-home systems, and 20–30% better energy-efficiency claims versus typical older stock.

Information Transparency and Digital Platforms

The rise of platforms like Lianjia, Fang.com and Beike has cut info asymmetry: 2024 surveys show 68% of Chinese homebuyers used online reviews and delivery-history data when choosing developers, letting buyers compare prices and on-time delivery rates across cities.

This forces China Overseas Grand Oceans Group to protect brand reputation—developers with >90% positive delivery records command price premiums of 6–10% in Tier-1/2 markets.

- 68% buyers use platforms (2024)

- Compare delivery records city-wide

- Positive delivery = 6–10% price premium

- Brand reputation now critical

Government Price Guidance and Controls

Local governments often set price caps on new homes to keep affordability; in 2024 over 50 major Chinese cities had resale or new-build price guidance, constraining developers’ list prices and acting like strong customer bargaining power.

China Overseas Grand Oceans must meet these ceilings while hitting margins; for example, a 2024 Shanghai cap limited unit prices in peripheral projects to ~RMB 55,000/sqm, squeezing gross margins and shifting focus to cost control and differentiation.

- Price caps in 50+ cities, 2024

- Example: Shanghai cap ~RMB 55,000/sqm, 2024

- Effect: limits pricing, raises need for cost and value play

Buyers in Control: Discounts, 18‑Month Overhang & Rate Sensitivity Squeeze Demand

Buyers hold strong leverage: 5–15% routine discounts, 18-month stock overhang (end-2025), 3.2% mortgage growth (2024), 4.65% avg new mortgage rate (2024), 12% rise in secondhand listings (2024), 68% use online platforms, >50 cities had price caps (2024). Developers with >90% delivery records earn 6–10% premiums; a 100bp rate rise cuts eligible buyers ~15–25%.

| Metric | Value |

|---|---|

| Stock overhang | 18 months (end-2025) |

| Mortgage growth | 3.2% YoY (2024) |

| Avg new mortgage rate | 4.65% (2024) |

| 2ndhand listings rise | 12% (2024) |

| Online platform use | 68% (2024) |

| Cities with price caps | 50+ (2024) |

Preview Before You Purchase

China Overseas Grand Oceans Group Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for China Overseas Grand Oceans Group that you’ll receive upon purchase—fully formatted, professionally written, and ready for immediate use; no samples, no placeholders. The document presents competitive rivalry, threat of new entrants, bargaining power of suppliers and buyers, and threat of substitutes with concise insights and actionable implications tailored to investors and strategists.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

China Overseas Grand Oceans faces moderate supplier power, significant buyer sensitivity to price and service, and rising competitive rivalry amid industry consolidation; barriers to entry are mixed due to capital intensity but supportive policy, while substitutes pose limited near-term threat. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategic insights tailored to China Overseas Grand Oceans Group.

Suppliers Bargaining Power

Concentration of Land Supply

The primary supplier for China Overseas Grand Oceans is the local government, which monopolizes land auctions and urban planning; by late 2025 the centralized land supply system still sets availability and price in Tier‑3/4 cities, where land sales fell 6% YoY in 2024 and average reserve-to-sales ratios tightened to 4.2 months, giving authorities strong leverage over pricing and timelines and squeezing the group’s gross margins by an estimated 120–180 bps.

Construction Material Price Volatility

Suppliers of steel, cement and glass hold moderate bargaining power, driven by global commodity cycles and China policy; steel spot prices rose ~18% in 2024 and averaged CNY 5,200/ton by Q4 2025, lifting input costs for developers.

Stricter environmental curbs since 2023 cut high‑emission output—cement capacity utilization fell to ~70% in 2024—causing intermittent price spikes that hit margins.

China Overseas Grand Oceans offsets this via multi‑year procurement deals and JV supply partnerships; long‑term contracts covered ~40% of steel needs in 2025, reducing short‑term volatility risk.

Availability of Specialized Labor

China Overseas Grand Oceans faces rising supplier power from specialized labor as China’s working-age population fell by 3.45% between 2015 and 2023, shrinking blue-collar availability; construction wages rose about 6–8% annually in 2023–25 to attract younger workers. Contractors and labor service firms now command higher rates and stricter terms, increasing project costs and scheduling risk. The company’s heavy reliance on third-party crews for quality and deadlines makes labor a key controllable cost, accounting for an estimated 20–30% of project direct costs.

Access to Institutional Financing

Financial institutions are suppliers of capital whose leverage over China Overseas Grand Oceans Group is shaped by People’s Bank of China policy and the Three Red Lines debt controls; bank lending rates averaged 3.65% for corporate loans in 2024, raising borrowing cost pressure.

The company’s state-owned background grants stronger credit access versus private peers—China Overseas Grand Oceans, tied to China State Construction, saw yuan bond issuance of RMB 7.2bn in 2024—yet lenders enforce tight covenants on leverage and cashflow.

Debt cost and bond market access remain external constraints: a 100bp rise in yield would cut project NPV materially, limiting acquisition scale despite parent support.

- Bank loan rate 3.65% (2024)

Technological and Green Building Providers

As China mandates green building standards by 2025, suppliers of energy-efficient systems and smart-home tech wield rising power; proprietary HVAC, BMS (building management systems), and EV-charging solutions drive 15–25% higher fit-out costs but cut operational emissions 30–50% per government pilots in 2023–24.

China Overseas Grand Oceans must source from a small pool of certified high-end vendors to meet state carbon-neutral targets, leaving it dependent on supplier pricing, lead times, and integration expertise; a 2024 industry survey showed 62% of developers report supplier-concentration risks.

Key impacts: higher capex, longer procurement cycles, and potential project delays if supplier capacity tightens—especially in tier-1 cities where green premiums reached 8–12% in 2024.

- 2025 mandate raises supplier leverage

- Proprietary tech increases capex 15–25%

- Operational emissions cut 30–50% (pilots 2023–24)

- 62% developers cite supplier concentration risk (2024)

- Green premium 8–12% in tier-1 cities (2024)

Suppliers exert rising power: land tight, steel surging, labor up, bonds easing finance

Suppliers hold moderate-to-high power: local governments control land supply (reserve-to-sales 4.2 months, land sales -6% YoY 2024), materials saw steel +18% in 2024 (CNY 5,200/ton by Q4 2025) and cement capacity use ~70% in 2024, labor costs rose 6–8% annually 2023–25; multi‑year contracts covered ~40% steel in 2025, yuan bond issuance RMB 7.2bn (2024) eased financing but covenants bind.

| Metric | Value |

|---|---|

| Land reserve-to-sales | 4.2 months (2024) |

| Land sales YoY | -6% (2024) |

| Steel price | CNY 5,200/ton (Q4 2025) |

| Cement utilization | ~70% (2024) |

| Labor wage growth | 6–8% pa (2023–25) |

| Steel long contracts | ~40% (2025) |

| Yuan bonds | RMB 7.2bn (2024) |

What is included in the product

Tailored exclusively for China Overseas Grand Oceans Group, this Porter's Five Forces overview uncovers key competitive drivers, buyer/supplier influence, entry barriers, substitutes, and emerging threats shaping its port and logistics positioning.

A concise Porter's Five Forces snapshot for China Overseas Grand Oceans—quickly identify competitive pressures and strategic levers to relieve pain points.

Customers Bargaining Power

Shift Toward Buyer Market Dynamics

By end-2025 China’s housing stock overhang hit about 18 months of sales in lower-tier cities, shifting bargaining power to buyers; individual purchasers now routinely secure 5–15% price discounts and demand higher-spec finishes, raising rework risk and margin pressure for China Overseas Grand Oceans Group. The firm must prioritize on-time delivery, upgraded fit-outs, and post-sale service—areas where 1–3% margin recovery is achievable if customer satisfaction rises above industry average.

Impact of Mortgage Interest Rates

Customer purchasing power ties closely to mortgage rates and state bank lending; China Household Loan rate averaged 4.65% for new mortgages in 2024 and downpayment rules vary by city.

Beijing and Shanghai eased policies through 2025, but national outstanding mortgage growth slowed to 3.2% YoY in 2024, so buyers stay rate-sensitive.

If mortgage rates rise 100 bps or lending tightens, eligible buyers could fall by ~15–25%, forcing developers like China Overseas Grand Oceans to increase incentives and price discounts.

Rise of Secondary Market Competition

The growing inventory of pre-owned homes in China—estimated at a 12% annual rise in secondhand listings in 2024 in major coastal cities—gives buyers a ready alternative and strengthens their bargaining power against China Overseas Grand Oceans Group. Buyers weigh immediate availability and lower contingency risk of secondary units versus delivery delays in new builds, which averaged 9–14 months late in some provinces in 2023. To respond, the developer must highlight superior amenities, smart-home systems, and 20–30% better energy-efficiency claims versus typical older stock.

Information Transparency and Digital Platforms

The rise of platforms like Lianjia, Fang.com and Beike has cut info asymmetry: 2024 surveys show 68% of Chinese homebuyers used online reviews and delivery-history data when choosing developers, letting buyers compare prices and on-time delivery rates across cities.

This forces China Overseas Grand Oceans Group to protect brand reputation—developers with >90% positive delivery records command price premiums of 6–10% in Tier-1/2 markets.

- 68% buyers use platforms (2024)

- Compare delivery records city-wide

- Positive delivery = 6–10% price premium

- Brand reputation now critical

Government Price Guidance and Controls

Local governments often set price caps on new homes to keep affordability; in 2024 over 50 major Chinese cities had resale or new-build price guidance, constraining developers’ list prices and acting like strong customer bargaining power.

China Overseas Grand Oceans must meet these ceilings while hitting margins; for example, a 2024 Shanghai cap limited unit prices in peripheral projects to ~RMB 55,000/sqm, squeezing gross margins and shifting focus to cost control and differentiation.

- Price caps in 50+ cities, 2024

- Example: Shanghai cap ~RMB 55,000/sqm, 2024

- Effect: limits pricing, raises need for cost and value play

Buyers in Control: Discounts, 18‑Month Overhang & Rate Sensitivity Squeeze Demand

Buyers hold strong leverage: 5–15% routine discounts, 18-month stock overhang (end-2025), 3.2% mortgage growth (2024), 4.65% avg new mortgage rate (2024), 12% rise in secondhand listings (2024), 68% use online platforms, >50 cities had price caps (2024). Developers with >90% delivery records earn 6–10% premiums; a 100bp rate rise cuts eligible buyers ~15–25%.

| Metric | Value |

|---|---|

| Stock overhang | 18 months (end-2025) |

| Mortgage growth | 3.2% YoY (2024) |

| Avg new mortgage rate | 4.65% (2024) |

| 2ndhand listings rise | 12% (2024) |

| Online platform use | 68% (2024) |

| Cities with price caps | 50+ (2024) |

Preview Before You Purchase

China Overseas Grand Oceans Group Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for China Overseas Grand Oceans Group that you’ll receive upon purchase—fully formatted, professionally written, and ready for immediate use; no samples, no placeholders. The document presents competitive rivalry, threat of new entrants, bargaining power of suppliers and buyers, and threat of substitutes with concise insights and actionable implications tailored to investors and strategists.