Coinbase Boston Consulting Group Matrix

Download Your Competitive Advantage

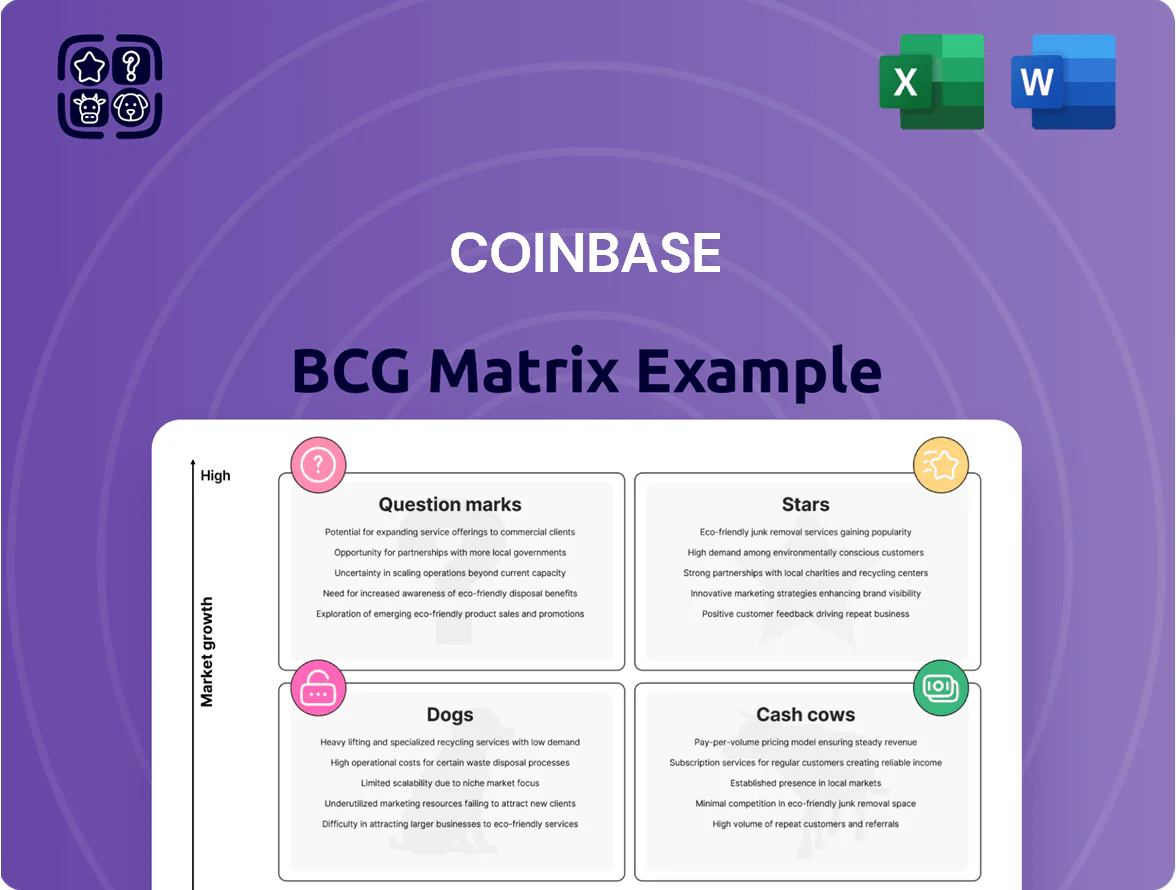

Coinbase’s BCG Matrix preview highlights where core offerings—spot trading, custody, staking, and new product experiments—likely fall among Stars, Cash Cows, Question Marks, or Dogs given market share and growth dynamics in crypto; it teases strategic implications for capital allocation and portfolio focus. This sneak peek is useful, but the full BCG Matrix delivers quadrant-by-quadrant data, executable recommendations, and editable Word + Excel files so you can prioritize investments with confidence—purchase the complete report for instant access.

Stars

Base Layer 2 Network

By end-2025 Base had become the leading Ethereum Layer 2, handling ~22% of L2 TVL ($6.8B) and ~18% of daily L2 txs (avg 1.2M/day), driven by 45k active dapps and 1,200 weekly dev commits. It leverages deep Coinbase integration—on‑ramps, custody, and tooling—helping sustain ~35% share of Coinbase-linked DeFi flows. Continued capex for sequencer redundancy and fraud-proof tooling is needed to defend vs optimistic and zk rollups.

Institutional Custody Services

Coinbase Institutional Custody is the primary custodian for most US spot crypto ETFs, holding roughly 60–70% of institutional crypto assets by AUM, and safeguarding an estimated $150–200 billion as of Dec 2025.

Growth surged 2023–2025 as traditional asset managers added crypto; custody revenues rose ~40% CAGR, but security and compliance force ongoing CapEx — Coinbase spent ~$1.2bn on infrastructure and security in 2024 alone.

International Derivatives Exchange

Coinbase International Exchange is a Star: it captured about 22% share of non-US perpetual futures volumes in 2024, handling ~$85B monthly notional at peak, reflecting the shift to regulated venues for leveraged products.

Global derivatives trading grew ~18% YoY in 2024; this high-growth tailwind means Coinbase must keep investing in marketing and liquidity incentives—estimated $120–180M annually—to outcompete offshore venues and sustain Star metrics.

Liquid Staking and Rewards

Coinbase has cemented its lead in Ethereum staking, custodizing over $20B in ETH staking derivatives by Q4 2025 and simplifying protocol rewards for retail and institutional users.

Proof-of-stake networks grew transaction validators 42% year-over-year in 2025, driving high demand for liquid staking; Coinbase captures a top-three market share among centralized providers.

High market share in this fast-growing vertical keeps Coinbase central to DeFi liquidity and yield flows, supporting swap, lending, and custody revenue streams.

- Custodied ETH staking > $20B (Q4 2025)

- PoS validator growth +42% YoY (2025)

- Top-3 market share among centralized stakers

Coinbase Prime for Institutions

Coinbase Prime is the institutional gold standard for trading, offering advanced execution, analytics, and financing; by Q4 2025 it handled roughly $120B monthly flow and held ~35% share of US institutional crypto custody revenue.

As corporations and hedge funds upped allocations late 2025, Prime captured high-value market share, growing institutional revenue 28% YoY; complexity demands ongoing innovation and dedicated support.

Because institutional needs are complex, Prime stays a high-growth leader that consumes significant R&D and client-servicing resources, with Coinbase disclosing $250M+ annual spend on institutional product development in FY2025.

- Handled ~$120B monthly flow (Q4 2025)

- ~35% US institutional custody revenue share

- Institutional revenue +28% YoY (2025)

- >$250M institutional R&D spend (FY2025)

Top Crypto Stars 2025: Base, Custody, Intl Exchange, ETH Staking & Prime Lead Market

Stars: Base, Institutional Custody, International Exchange, ETH staking, and Prime each hold top market positions with high growth—Base L2 ~22% TVL ($6.8B) and 1.2M tx/day; Custody ~60–70% institutional AUM (~$150–200B); International Exchange ~22% non-US perp share (~$85B monthly peak); ETH staking custodial >$20B; Prime ~$120B monthly flow.

| Business | Share/Metric | Key 2025 Figures |

|---|---|---|

| Base (L2) | TVL share | 22% / $6.8B; 1.2M tx/day |

| Custody | Institutional AUM share | 60–70% / $150–200B |

| Intl Exchange | Non‑US perp vol share | 22% / ~$85B monthly |

| ETH staking | Custodied | >$20B |

| Prime | Monthly flow | ~$120B |

What is included in the product

Comprehensive BCG Matrix for Coinbase: evaluates products by market growth/share, offers strategic moves for Stars, Cash Cows, Question Marks, and Dogs.

One-page Coinbase BCG Matrix placing each product in a quadrant for quick portfolio decisions.

Cash Cows

Retail Spot Trading Fees

Retail spot trading fees remain Coinbase’s primary cash engine, driven by a dominant brand and 2025 average daily traded volume near $8.4B, upholding market liquidity despite cooling retail cycles.

Basic spot growth has stabilized—year-over-year spot revenue rose 3% in 2024—but high fee margins produced $3.1B operating cash flow in FY2024, fueling capital reserves.

Those cash flows subsidize speculative ventures and R&D, funding 2024–25 investments ~ $420M for new products and compliance scaling.

USDC Stablecoin Interest Income

Coinbase, via the Centre Consortium and broad USDC adoption, earns sizable interest on fiat reserves backing USDC; in 2025 Coinbase reported roughly $600–800m annualized yield on stablecoin reserves during higher short-term rates.

Coinbase One Subscription Service

Coinbase One, launched in 2021, has become a steady recurring-revenue stream by offering zero-fee trades and priority support; by Q4 2025 Coinbase reported ~1.2M subscribers, contributing an estimated $110M annualized revenue run-rate to subscription services.

Bitcoin and Ethereum Brokerage

Bitcoin and Ethereum brokerage is Coinbase’s cash cow: as of Q4 2025 BTC and ETH trading accounted for ~58% of spot volume and served ~39M active retail users, giving Coinbase top-tier share among entry investors.

These assets are mature in the crypto lifecycle, delivering steady fees that funded ~ $1.2B debt service and supported 2025 international expansion capex of ~$420M.

- ~58% spot volume (Q4 2025)

- ~39M active retail users

- $1.2B debt service funded

- $420M 2025 international capex

Ancillary Custody Fees

Ancillary custody fees: Coinbase’s long-term storage services produce steady, low-growth revenue—about $120–160m in annual custody fees estimated for 2024, given industry custody AUM trends and Coinbase’s ~10% institutional market share.

Operating in a mature segment with established security protocols, these fees are high-margin and require minimal promotional spend, contributing to platform EBITDA stability.

- Low growth, high margin

- Estimated $120–160m revenue (2024)

- Minimal marketing spend

- Security-heavy, low operational churn

Coinbase: $3.1B FY24 cash flow, 39M users, 1.2M One subs, 58% BTC/ETH spot share

Retail spot trading (BTC/ETH) and Coinbase One subscriptions are the cash cows, generating ~$3.1B operating cash flow FY2024, ~1.2M Coinbase One subs (Q4 2025), ~39M active retail users (Q4 2025), and ~58% spot volume share (Q4 2025); custody fees add $120–160M yearly.

| Metric | Value |

|---|---|

| FY2024 op cash flow | $3.1B |

| Coinbase One subs (Q4 2025) | 1.2M |

| Active retail users (Q4 2025) | 39M |

| BTC/ETH spot volume share (Q4 2025) | 58% |

| Custody fees (est. 2024) | $120–160M |

What You See Is What You Get

Coinbase BCG Matrix

The file you're previewing is the exact Coinbase BCG Matrix report you'll receive after purchase—no watermarks, no demo placeholders—just a fully formatted, analysis-ready document crafted for strategic clarity and professional presentation.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Download Your Competitive Advantage

Coinbase’s BCG Matrix preview highlights where core offerings—spot trading, custody, staking, and new product experiments—likely fall among Stars, Cash Cows, Question Marks, or Dogs given market share and growth dynamics in crypto; it teases strategic implications for capital allocation and portfolio focus. This sneak peek is useful, but the full BCG Matrix delivers quadrant-by-quadrant data, executable recommendations, and editable Word + Excel files so you can prioritize investments with confidence—purchase the complete report for instant access.

Stars

Base Layer 2 Network

By end-2025 Base had become the leading Ethereum Layer 2, handling ~22% of L2 TVL ($6.8B) and ~18% of daily L2 txs (avg 1.2M/day), driven by 45k active dapps and 1,200 weekly dev commits. It leverages deep Coinbase integration—on‑ramps, custody, and tooling—helping sustain ~35% share of Coinbase-linked DeFi flows. Continued capex for sequencer redundancy and fraud-proof tooling is needed to defend vs optimistic and zk rollups.

Institutional Custody Services

Coinbase Institutional Custody is the primary custodian for most US spot crypto ETFs, holding roughly 60–70% of institutional crypto assets by AUM, and safeguarding an estimated $150–200 billion as of Dec 2025.

Growth surged 2023–2025 as traditional asset managers added crypto; custody revenues rose ~40% CAGR, but security and compliance force ongoing CapEx — Coinbase spent ~$1.2bn on infrastructure and security in 2024 alone.

International Derivatives Exchange

Coinbase International Exchange is a Star: it captured about 22% share of non-US perpetual futures volumes in 2024, handling ~$85B monthly notional at peak, reflecting the shift to regulated venues for leveraged products.

Global derivatives trading grew ~18% YoY in 2024; this high-growth tailwind means Coinbase must keep investing in marketing and liquidity incentives—estimated $120–180M annually—to outcompete offshore venues and sustain Star metrics.

Liquid Staking and Rewards

Coinbase has cemented its lead in Ethereum staking, custodizing over $20B in ETH staking derivatives by Q4 2025 and simplifying protocol rewards for retail and institutional users.

Proof-of-stake networks grew transaction validators 42% year-over-year in 2025, driving high demand for liquid staking; Coinbase captures a top-three market share among centralized providers.

High market share in this fast-growing vertical keeps Coinbase central to DeFi liquidity and yield flows, supporting swap, lending, and custody revenue streams.

- Custodied ETH staking > $20B (Q4 2025)

- PoS validator growth +42% YoY (2025)

- Top-3 market share among centralized stakers

Coinbase Prime for Institutions

Coinbase Prime is the institutional gold standard for trading, offering advanced execution, analytics, and financing; by Q4 2025 it handled roughly $120B monthly flow and held ~35% share of US institutional crypto custody revenue.

As corporations and hedge funds upped allocations late 2025, Prime captured high-value market share, growing institutional revenue 28% YoY; complexity demands ongoing innovation and dedicated support.

Because institutional needs are complex, Prime stays a high-growth leader that consumes significant R&D and client-servicing resources, with Coinbase disclosing $250M+ annual spend on institutional product development in FY2025.

- Handled ~$120B monthly flow (Q4 2025)

- ~35% US institutional custody revenue share

- Institutional revenue +28% YoY (2025)

- >$250M institutional R&D spend (FY2025)

Top Crypto Stars 2025: Base, Custody, Intl Exchange, ETH Staking & Prime Lead Market

Stars: Base, Institutional Custody, International Exchange, ETH staking, and Prime each hold top market positions with high growth—Base L2 ~22% TVL ($6.8B) and 1.2M tx/day; Custody ~60–70% institutional AUM (~$150–200B); International Exchange ~22% non-US perp share (~$85B monthly peak); ETH staking custodial >$20B; Prime ~$120B monthly flow.

| Business | Share/Metric | Key 2025 Figures |

|---|---|---|

| Base (L2) | TVL share | 22% / $6.8B; 1.2M tx/day |

| Custody | Institutional AUM share | 60–70% / $150–200B |

| Intl Exchange | Non‑US perp vol share | 22% / ~$85B monthly |

| ETH staking | Custodied | >$20B |

| Prime | Monthly flow | ~$120B |

What is included in the product

Comprehensive BCG Matrix for Coinbase: evaluates products by market growth/share, offers strategic moves for Stars, Cash Cows, Question Marks, and Dogs.

One-page Coinbase BCG Matrix placing each product in a quadrant for quick portfolio decisions.

Cash Cows

Retail Spot Trading Fees

Retail spot trading fees remain Coinbase’s primary cash engine, driven by a dominant brand and 2025 average daily traded volume near $8.4B, upholding market liquidity despite cooling retail cycles.

Basic spot growth has stabilized—year-over-year spot revenue rose 3% in 2024—but high fee margins produced $3.1B operating cash flow in FY2024, fueling capital reserves.

Those cash flows subsidize speculative ventures and R&D, funding 2024–25 investments ~ $420M for new products and compliance scaling.

USDC Stablecoin Interest Income

Coinbase, via the Centre Consortium and broad USDC adoption, earns sizable interest on fiat reserves backing USDC; in 2025 Coinbase reported roughly $600–800m annualized yield on stablecoin reserves during higher short-term rates.

Coinbase One Subscription Service

Coinbase One, launched in 2021, has become a steady recurring-revenue stream by offering zero-fee trades and priority support; by Q4 2025 Coinbase reported ~1.2M subscribers, contributing an estimated $110M annualized revenue run-rate to subscription services.

Bitcoin and Ethereum Brokerage

Bitcoin and Ethereum brokerage is Coinbase’s cash cow: as of Q4 2025 BTC and ETH trading accounted for ~58% of spot volume and served ~39M active retail users, giving Coinbase top-tier share among entry investors.

These assets are mature in the crypto lifecycle, delivering steady fees that funded ~ $1.2B debt service and supported 2025 international expansion capex of ~$420M.

- ~58% spot volume (Q4 2025)

- ~39M active retail users

- $1.2B debt service funded

- $420M 2025 international capex

Ancillary Custody Fees

Ancillary custody fees: Coinbase’s long-term storage services produce steady, low-growth revenue—about $120–160m in annual custody fees estimated for 2024, given industry custody AUM trends and Coinbase’s ~10% institutional market share.

Operating in a mature segment with established security protocols, these fees are high-margin and require minimal promotional spend, contributing to platform EBITDA stability.

- Low growth, high margin

- Estimated $120–160m revenue (2024)

- Minimal marketing spend

- Security-heavy, low operational churn

Coinbase: $3.1B FY24 cash flow, 39M users, 1.2M One subs, 58% BTC/ETH spot share

Retail spot trading (BTC/ETH) and Coinbase One subscriptions are the cash cows, generating ~$3.1B operating cash flow FY2024, ~1.2M Coinbase One subs (Q4 2025), ~39M active retail users (Q4 2025), and ~58% spot volume share (Q4 2025); custody fees add $120–160M yearly.

| Metric | Value |

|---|---|

| FY2024 op cash flow | $3.1B |

| Coinbase One subs (Q4 2025) | 1.2M |

| Active retail users (Q4 2025) | 39M |

| BTC/ETH spot volume share (Q4 2025) | 58% |

| Custody fees (est. 2024) | $120–160M |

What You See Is What You Get

Coinbase BCG Matrix

The file you're previewing is the exact Coinbase BCG Matrix report you'll receive after purchase—no watermarks, no demo placeholders—just a fully formatted, analysis-ready document crafted for strategic clarity and professional presentation.