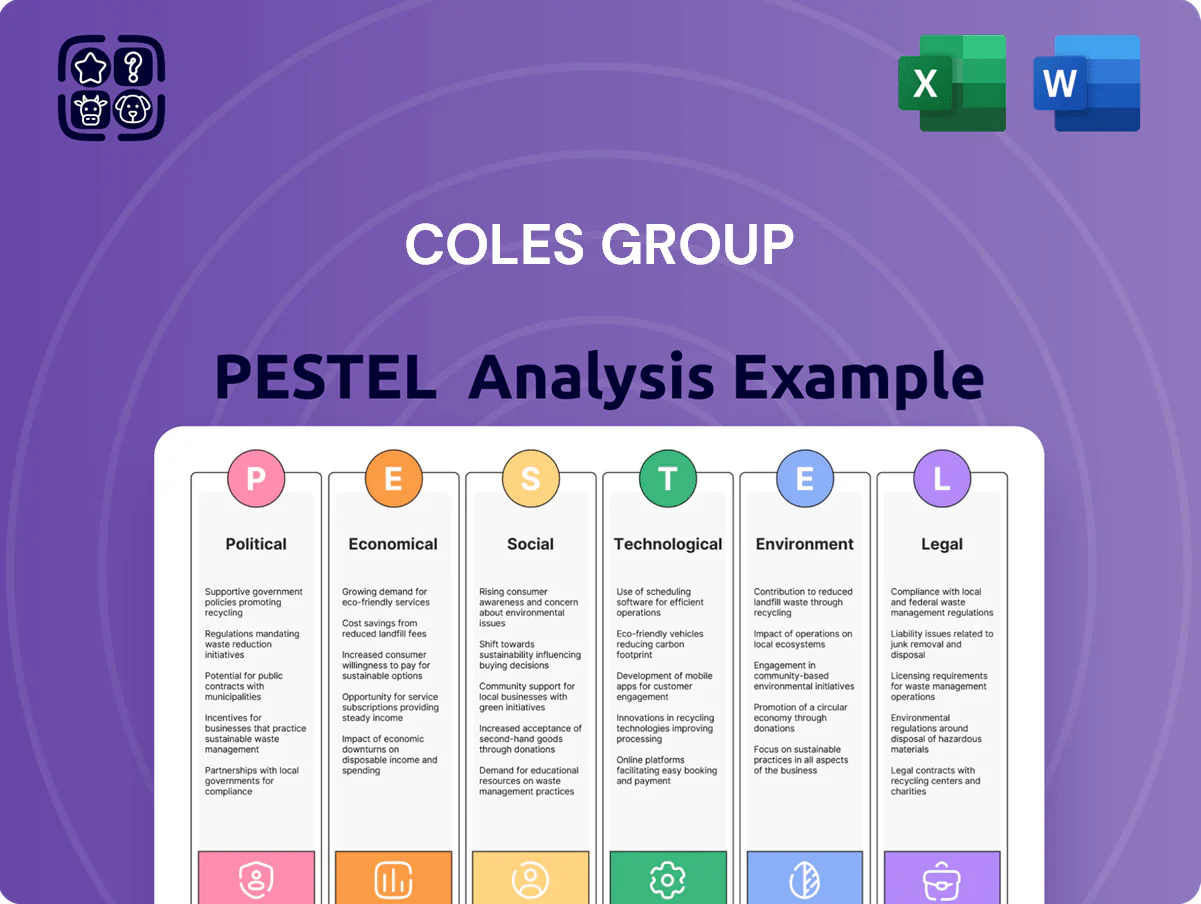

Coles Group PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic trends, and evolving consumer behaviors are shaping Coles Group’s strategic path—our concise PESTLE highlights the key external forces you need to know. Ideal for investors, advisors, and strategists, the full report delivers actionable insights and ready-to-use analysis to inform decisions. Purchase the complete PESTLE now for an instant, editable download and stay ahead of risks and opportunities.

Political factors

Government Scrutiny of Grocery Pricing

The Australian government intensified scrutiny on supermarket pricing after 2024 inquiries, with ACCC and federal treasury probes into competition and transparency; Coles faces regulatory risk as the ACCC investigated major grocers through 2024–25. Coles reported FY25 comparable sales growth of 3.1% and a 4.8% gross margin in FY25, tying pricing moves to political sensitivity. Heightened oversight limits aggressive margin expansion to avoid fines, mandatory pricing reforms or reputational damage.

Competition Policy and Regulatory Reform

Legislative changes strengthening the Food and Grocery Code of Conduct were ratified by late 2025, imposing stricter supplier protections that affect Coles’ supply contracts; in FY2024 Coles reported A$41.5bn revenue, so compliance risks could materially impact margins if procurement practices shift. Reforms require fairer payment terms and dispute mechanisms for primary producers, forcing Coles to adjust sourcing and contract terms to retain its social license.

Industrial Relations and Labor Laws

The political push for secure work and higher minimum wages in Australia affects Coles’ ~120,000 employees, raising labor costs after the 2024 national minimum wage rise of 8.6% and sector awards adjustments; updated Fair Work Act provisions force management of complex enterprise bargaining covering thousands of staff while protecting margins (Coles reported FY25 labour expenses up ~6.2% YoY); policy moves to extend protections to gig workers could increase last‑mile delivery costs by an estimated 5–10%.

International Trade and Geopolitical Stability

As a major importer of household goods and private-label components, Coles is exposed to Australia’s trade relations with China, Vietnam and the US; in FY25 imports accounted for approximately 28% of cost of goods sold, making tariffs or bans materially impactful.

Political tensions or new non-tariff barriers could raise landed costs—a 5% tariff on key categories would add ~A$90–120m annual COGS pressure based on FY25 import spend.

Coles monitors geopolitical shifts and shipping risks (Suez/Strait of Malacca disruptions, container rates) to protect margins and inventory flow.

- FY25 imports ≈28% of COGS

- Estimated A$90–120m impact from 5% tariff

- Focus: China, Vietnam, US trade relations

Liquor Licensing and Public Health Policy

State-level liquor licensing and secondary supply laws materially impact Coles Liquor; in FY2024 liquor sales represented about 8% of Coles Group revenue (≈A$5.0bn), making regulatory changes financially significant.

Proposals for floor pricing and tighter advertising—part of 2024–25 public health debates—could reduce margins for Liquorland and First Choice and compress category growth.

Management needs active policy engagement and targeted community programs to protect sales while aligning with health expectations.

- FY2024 liquor revenue ≈A$5.0bn (≈8% of group)

- Potential floor pricing could cut high-margin promotional sales

- Advertising limits risk lower brand visibility and customer acquisition

- Policy engagement and community initiatives mitigate regulatory risk

Coles faces margin squeeze: political scrutiny, wage pressures & tariff risks

Political scrutiny after 2024 inquiries raised regulatory risk for Coles, limiting margin expansion; FY25 comparable sales +3.1% and gross margin 4.8%. Strengthened Food & Grocery Code (late 2025) forces fairer supplier terms; Coles FY24 revenue A$41.5bn so procurement shifts can hit margins. Labor policy and 2024 wage rise (+8.6%) increased FY25 labour costs ~6.2% YoY; imports ≈28% of COGS, a 5% tariff ≈A$90–120m COGS impact.

| Metric | Value |

|---|---|

| Group revenue FY24 | A$41.5bn |

| Comparable sales FY25 | +3.1% |

| Gross margin FY25 | 4.8% |

| Labor cost rise FY25 | ~6.2% YoY |

| Imports of COGS | ≈28% |

| 5% tariff impact | ≈A$90–120m |

What is included in the product

Explores how political, economic, social, technological, environmental, and legal forces uniquely affect Coles Group, using current market and regulatory dynamics in Australia to identify risks and opportunities for strategy and investment.

A concise, shareable Coles Group PESTLE summary that’s visually segmented for quick interpretation, ideal for drop-in slides, meeting briefs, or team alignment to streamline discussions on external risks and market positioning.

Economic factors

Interest Rate Environment and Consumer Spending

By end-2025, lagging effects of prior RBA rate cycles keep household budgets squeezed, with average variable mortgage rates near 6.5% and housing-interest payments consuming a record share of disposable income; this has driven retail CPI for food at home up ~4.0% YoY to mid-2025. High repayment costs have curtailed discretionary spend, prompting trading down from premium to value ranges. Coles amplifies its private-label value tier, which grew low-single digits in market share in 2024–25, to capture budget-conscious shoppers.

Inflationary Pressures on Operating Costs

While Australian headline CPI eased to 3.4% y/y in Dec 2025, Coles continues to face elevated energy, logistics and labour costs—fuel and transport inflation ran near 8% in 2024–25 and wage pressures lifted retail labour costs ~4–5% in FY25. The group uses commodity hedges and multi‑year supplier contracts (covering ~30–40% of key inputs) to smooth volatility, but careful cost pass‑through is required to defend FY25 gross margin of ~22% without losing price‑sensitive shoppers.

Real Disposable Income Trends

Labor Market Tightness and Wage Growth

The Australian unemployment rate was 3.8% in Dec 2025, keeping competition high for tech and logistics talent; Coles must offer market-rate salaries—median warehouse supervisor pay ~AUD 95,000 (2025)—to staff automated distribution centres and reduce turnover.

Mandatory superannuation rose to 12% from 1 July 2025, increasing long-term labour costs; Coles reported FY25 labour expenses of ~AUD 3.2bn, exposing it to higher fixed workforce overheads.

- Unemployment 3.8% (Dec 2025) — tight market

- Median warehouse supervisor pay ~AUD 95,000 (2025)

- Superannuation at 12% from Jul 2025

- Coles FY25 labour expenses ~AUD 3.2bn

Exchange Rate Volatility

Fluctuations in the Australian dollar affect Coles' import costs and export competitiveness; AUD fell about 6% vs USD in 2024, raising import bills for private-label goods sourced abroad.

A weaker AUD can squeeze margins on Coles' own brands as global sourcing costs rise; Coles reported 2024 overseas procurement exposure that management hedges actively.

Coles' treasury uses FX derivatives to stabilize shelf prices—hedging reduced realized FX volatility by an estimated mid-single-digit percentage in FY2024.

- Weaker AUD increases import costs for private labels

- ~6% AUD decline vs USD in 2024 raised sourcing expenses

- Coles uses FX derivatives to limit margin impact and protect consumer prices

Coles faces FY25 margin squeeze: inflation, wage pressure and AUD-driven import costs

RBA rate carry-over and mortgage burden cut discretionary spend; food-at-home CPI ~4.0% YoY (mid-2025), Coles grows private-label share low-single digits. Energy/transport inflation ~8% (2024–25) and retail wages +4–5% pushed FY25 gross margin pressure; Coles hedges ~30–40% key inputs. Unemployment 3.8% (Dec 2025); FY25 labour costs ~AUD 3.2bn; AUD -6% vs USD (2024) raised import costs.

| Metric | Value |

|---|---|

| Food-at-home CPI | ~4.0% YoY (mid-2025) |

| Energy/transport inflation | ~8% (2024–25) |

| Retail wage growth | ~4–5% (FY25) |

| Unemployment | 3.8% (Dec 2025) |

| Coles labour expense | ~AUD 3.2bn (FY25) |

| AUD vs USD | -6% (2024) |

| Private-label hedge coverage | ~30–40% key inputs |

Same Document Delivered

Coles Group PESTLE Analysis

The preview shown here is the exact Coles Group PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Discover how political shifts, economic trends, and evolving consumer behaviors are shaping Coles Group’s strategic path—our concise PESTLE highlights the key external forces you need to know. Ideal for investors, advisors, and strategists, the full report delivers actionable insights and ready-to-use analysis to inform decisions. Purchase the complete PESTLE now for an instant, editable download and stay ahead of risks and opportunities.

Political factors

Government Scrutiny of Grocery Pricing

The Australian government intensified scrutiny on supermarket pricing after 2024 inquiries, with ACCC and federal treasury probes into competition and transparency; Coles faces regulatory risk as the ACCC investigated major grocers through 2024–25. Coles reported FY25 comparable sales growth of 3.1% and a 4.8% gross margin in FY25, tying pricing moves to political sensitivity. Heightened oversight limits aggressive margin expansion to avoid fines, mandatory pricing reforms or reputational damage.

Competition Policy and Regulatory Reform

Legislative changes strengthening the Food and Grocery Code of Conduct were ratified by late 2025, imposing stricter supplier protections that affect Coles’ supply contracts; in FY2024 Coles reported A$41.5bn revenue, so compliance risks could materially impact margins if procurement practices shift. Reforms require fairer payment terms and dispute mechanisms for primary producers, forcing Coles to adjust sourcing and contract terms to retain its social license.

Industrial Relations and Labor Laws

The political push for secure work and higher minimum wages in Australia affects Coles’ ~120,000 employees, raising labor costs after the 2024 national minimum wage rise of 8.6% and sector awards adjustments; updated Fair Work Act provisions force management of complex enterprise bargaining covering thousands of staff while protecting margins (Coles reported FY25 labour expenses up ~6.2% YoY); policy moves to extend protections to gig workers could increase last‑mile delivery costs by an estimated 5–10%.

International Trade and Geopolitical Stability

As a major importer of household goods and private-label components, Coles is exposed to Australia’s trade relations with China, Vietnam and the US; in FY25 imports accounted for approximately 28% of cost of goods sold, making tariffs or bans materially impactful.

Political tensions or new non-tariff barriers could raise landed costs—a 5% tariff on key categories would add ~A$90–120m annual COGS pressure based on FY25 import spend.

Coles monitors geopolitical shifts and shipping risks (Suez/Strait of Malacca disruptions, container rates) to protect margins and inventory flow.

- FY25 imports ≈28% of COGS

- Estimated A$90–120m impact from 5% tariff

- Focus: China, Vietnam, US trade relations

Liquor Licensing and Public Health Policy

State-level liquor licensing and secondary supply laws materially impact Coles Liquor; in FY2024 liquor sales represented about 8% of Coles Group revenue (≈A$5.0bn), making regulatory changes financially significant.

Proposals for floor pricing and tighter advertising—part of 2024–25 public health debates—could reduce margins for Liquorland and First Choice and compress category growth.

Management needs active policy engagement and targeted community programs to protect sales while aligning with health expectations.

- FY2024 liquor revenue ≈A$5.0bn (≈8% of group)

- Potential floor pricing could cut high-margin promotional sales

- Advertising limits risk lower brand visibility and customer acquisition

- Policy engagement and community initiatives mitigate regulatory risk

Coles faces margin squeeze: political scrutiny, wage pressures & tariff risks

Political scrutiny after 2024 inquiries raised regulatory risk for Coles, limiting margin expansion; FY25 comparable sales +3.1% and gross margin 4.8%. Strengthened Food & Grocery Code (late 2025) forces fairer supplier terms; Coles FY24 revenue A$41.5bn so procurement shifts can hit margins. Labor policy and 2024 wage rise (+8.6%) increased FY25 labour costs ~6.2% YoY; imports ≈28% of COGS, a 5% tariff ≈A$90–120m COGS impact.

| Metric | Value |

|---|---|

| Group revenue FY24 | A$41.5bn |

| Comparable sales FY25 | +3.1% |

| Gross margin FY25 | 4.8% |

| Labor cost rise FY25 | ~6.2% YoY |

| Imports of COGS | ≈28% |

| 5% tariff impact | ≈A$90–120m |

What is included in the product

Explores how political, economic, social, technological, environmental, and legal forces uniquely affect Coles Group, using current market and regulatory dynamics in Australia to identify risks and opportunities for strategy and investment.

A concise, shareable Coles Group PESTLE summary that’s visually segmented for quick interpretation, ideal for drop-in slides, meeting briefs, or team alignment to streamline discussions on external risks and market positioning.

Economic factors

Interest Rate Environment and Consumer Spending

By end-2025, lagging effects of prior RBA rate cycles keep household budgets squeezed, with average variable mortgage rates near 6.5% and housing-interest payments consuming a record share of disposable income; this has driven retail CPI for food at home up ~4.0% YoY to mid-2025. High repayment costs have curtailed discretionary spend, prompting trading down from premium to value ranges. Coles amplifies its private-label value tier, which grew low-single digits in market share in 2024–25, to capture budget-conscious shoppers.

Inflationary Pressures on Operating Costs

While Australian headline CPI eased to 3.4% y/y in Dec 2025, Coles continues to face elevated energy, logistics and labour costs—fuel and transport inflation ran near 8% in 2024–25 and wage pressures lifted retail labour costs ~4–5% in FY25. The group uses commodity hedges and multi‑year supplier contracts (covering ~30–40% of key inputs) to smooth volatility, but careful cost pass‑through is required to defend FY25 gross margin of ~22% without losing price‑sensitive shoppers.

Real Disposable Income Trends

Labor Market Tightness and Wage Growth

The Australian unemployment rate was 3.8% in Dec 2025, keeping competition high for tech and logistics talent; Coles must offer market-rate salaries—median warehouse supervisor pay ~AUD 95,000 (2025)—to staff automated distribution centres and reduce turnover.

Mandatory superannuation rose to 12% from 1 July 2025, increasing long-term labour costs; Coles reported FY25 labour expenses of ~AUD 3.2bn, exposing it to higher fixed workforce overheads.

- Unemployment 3.8% (Dec 2025) — tight market

- Median warehouse supervisor pay ~AUD 95,000 (2025)

- Superannuation at 12% from Jul 2025

- Coles FY25 labour expenses ~AUD 3.2bn

Exchange Rate Volatility

Fluctuations in the Australian dollar affect Coles' import costs and export competitiveness; AUD fell about 6% vs USD in 2024, raising import bills for private-label goods sourced abroad.

A weaker AUD can squeeze margins on Coles' own brands as global sourcing costs rise; Coles reported 2024 overseas procurement exposure that management hedges actively.

Coles' treasury uses FX derivatives to stabilize shelf prices—hedging reduced realized FX volatility by an estimated mid-single-digit percentage in FY2024.

- Weaker AUD increases import costs for private labels

- ~6% AUD decline vs USD in 2024 raised sourcing expenses

- Coles uses FX derivatives to limit margin impact and protect consumer prices

Coles faces FY25 margin squeeze: inflation, wage pressure and AUD-driven import costs

RBA rate carry-over and mortgage burden cut discretionary spend; food-at-home CPI ~4.0% YoY (mid-2025), Coles grows private-label share low-single digits. Energy/transport inflation ~8% (2024–25) and retail wages +4–5% pushed FY25 gross margin pressure; Coles hedges ~30–40% key inputs. Unemployment 3.8% (Dec 2025); FY25 labour costs ~AUD 3.2bn; AUD -6% vs USD (2024) raised import costs.

| Metric | Value |

|---|---|

| Food-at-home CPI | ~4.0% YoY (mid-2025) |

| Energy/transport inflation | ~8% (2024–25) |

| Retail wage growth | ~4–5% (FY25) |

| Unemployment | 3.8% (Dec 2025) |

| Coles labour expense | ~AUD 3.2bn (FY25) |

| AUD vs USD | -6% (2024) |

| Private-label hedge coverage | ~30–40% key inputs |

Same Document Delivered

Coles Group PESTLE Analysis

The preview shown here is the exact Coles Group PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.