Colgate-Palmolive Porter's Five Forces Analysis

Don't Miss the Bigger Picture

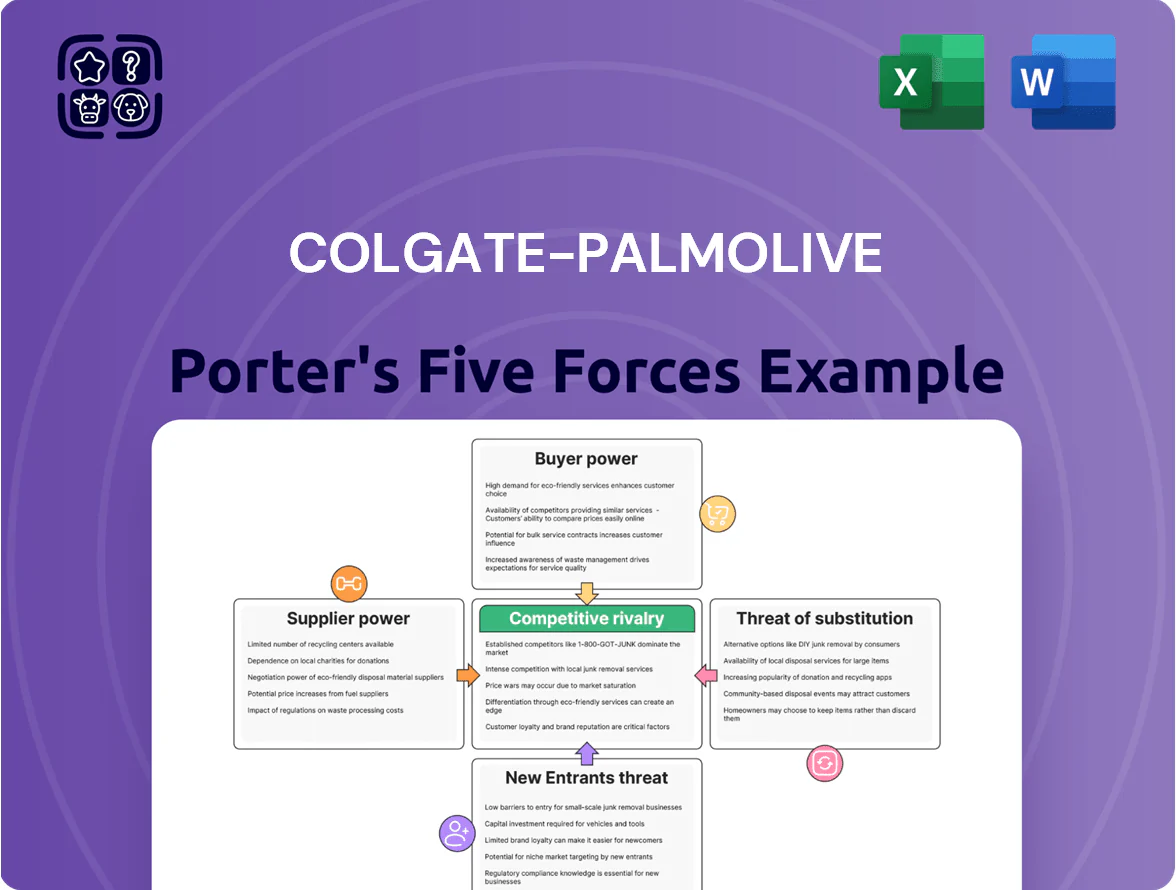

Colgate-Palmolive navigates a mature, branded consumer goods market where supplier leverage is moderate, buyer power is mixed across retail channels, and rivalry is intense due to global competitors and innovation in oral care and personal care.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Colgate-Palmolive’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Commoditization of Raw Materials

The primary inputs for Colgate-Palmolive—chemicals, packaging, and agricultural feeds for Hill’s Pet Nutrition—are largely commoditized, with global supplier pools; in 2024 Colgate spent about $7.8 billion on cost of goods sold, so switching suppliers is feasible and low-cost for many inputs.

Scale-Driven Negotiation Leverage

As a global buyer, Colgate-Palmolive’s $18.0 billion 2024 revenue gives it scale-driven negotiation leverage, letting procurement secure volume discounts and extended credit; suppliers often accept thinner margins for steady orders—Colgate reported inventory purchases concentrated in a few large suppliers, enabling it to offset price inflation by ~1.2–1.8% through contractual rebates and bulk pricing in 2023–24.

Diversified Global Supplier Base

Colgate-Palmolive maintains a diversified supplier network across 40+ countries, reducing exposure to localized disruptions and limiting single-vendor risk.

By avoiding dependence on one region or supplier, Colgate can re-source quickly if vendors try to hike prices, protecting gross margin—gross margin was 53.2% in FY2024.

As of 2025 this diversification acts as a buffer against supplier-driven cost inflation, lowering procurement volatility and supporting stable COGS.

Vertical Integration Capabilities

Colgate-Palmolive (market cap $72.5B as of Dec 31, 2025) has the cash flow and technical R&D to vertically integrate into packaging or select chemical inputs, making backward integration credible.

This threat pressures suppliers to keep prices and innovation competitive, since in 2024 Colgate spent $1.1B on R&D and capital investments that could be reallocated to in-house production.

- Market cap $72.5B (Dec 31, 2025)

- $1.1B R&D/capex (2024)

- Credible backward integration deters supplier price hikes

Impact of Sustainability Requirements

While most Colgate-Palmolive suppliers have limited leverage, providers of patented green tech or certified sustainable ingredients exert slightly higher bargaining power amid stricter regs and consumer demand.

Meeting its 2025 sustainability goals may raise procurement costs; in 2024 Colgate spent about $850m on R&D and sustainability initiatives, enabling collaboration or in-house alternatives to limit supplier power.

- Specialized suppliers = higher leverage

- Patented green inputs can raise costs

- $850m R&D helps build alternatives

- Supplier power remains contained

Colgate's scale and $1.1B R&D/capex neutralize supplier power; 53.2% gross margin

Suppliers have limited power: commoditized inputs, global sourcing across 40+ countries, and Colgate’s $18.0B 2024 revenue and $1.1B 2024 R&D/capex give strong leverage and credible backward-integration threat; gross margin 53.2% (FY2024) and supplier rebates cut inflation impact ~1.2–1.8%. Specialized green/patented inputs carry higher leverage.

| Metric | Value |

|---|---|

| Revenue 2024 | $18.0B |

| Gross margin FY2024 | 53.2% |

| COGS 2024 | $7.8B |

| R&D/capex 2024 | $1.1B |

What is included in the product

Tailored exclusively for Colgate-Palmolive, this Porter's Five Forces overview uncovers key drivers of competition, buyer and supplier power, threats from substitutes and new entrants, and highlights disruptive forces and market dynamics that affect pricing, profitability, and market share.

A concise Porter's Five Forces snapshot for Colgate-Palmolive—instantly highlights competitive threats, supplier/buyer leverage, and substitution risk to speed strategic decisions and deck-ready insights.

Customers Bargaining Power

Consolidation of Retail Giants

Massive retailers such as Walmart, Amazon, and Target accounted for roughly 28–32% of Colgate‑Palmolive’s global sales by end‑2025, concentrating buying power and forcing the company to accept lower wholesale prices and deeper promotions.

These chains can demand prime shelf placement and co‑funded advertising; losing any would cut Colgate‑Palmolive’s revenue sharply, so the company concedes margins to retain access.

Low Consumer Switching Costs

Individual consumers face almost zero financial cost switching from Colgate toothpaste or Palmolive dish soap to rivals, so Colgate-Palmolive must spend to keep share; the company spent about $1.9 billion on advertising and marketing in full-year 2024 to support brand loyalty.

Growth of Private Label Brands

Retailers pushed private-label share for oral-care to about 14% in the US by 2024, and continued 2025 price pressure has raised private-label penetration in mass channels to ~16%, directly undercutting national brands like Colgate. These store brands match perceived quality at lower prices, competing for shelf space and promotional slots, which lets retailers demand deeper trade discounts from manufacturers. As consumers traded down during 2025 inflation, retailer leverage grew, squeezing Colgate-Palmolive gross margins—Colgate reported a 60 bps margin decline in 2024 tied partly to trade spend. Retailers’ control of assortments and promotions amplifies buyer bargaining power against Colgate.

High Price Sensitivity and Transparency

- Amazon market share for oral care ~28% (2024)

E-commerce and Direct-to-Consumer Shift

The rise of digital marketplaces has cut into traditional brand dominance; global e‑commerce sales hit 5.7 trillion USD in 2023 and food/household online penetration rose ~18% in 2024, giving consumers many niche and DTC options versus Colgate‑Palmolive.

Colgate’s direct channels (over 10% of sales in some regions by 2024) still face competition from indie brands, forcing faster product updates and active social listening to retain share.

- E‑commerce 5.7T USD (2023)

- Household online penetration ~18% (2024)

- Colgate DTC >10% sales in some regions (2024)

Retailer Power Erodes Colgate Margins: Rising Private Label, Bigger Trade Discounts

Buyers—large retailers (Walmart, Amazon, Target) accounting for ~28–32% of Colgate‑Palmolive sales by end‑2025—concentrate purchase power, demand prime placement and co‑funded promotions, and push private‑label penetration (US oral‑care private‑label ~14% in 2024, ~16% in mass by 2025), forcing deeper trade discounts and squeezing margins despite Colgate’s $1.9B marketing spend in 2024.

| Metric | Value |

|---|---|

| Retailer share of sales (2025) | 28–32% |

| Colgate marketing spend (2024) | $1.9B |

| US oral‑care private‑label (2024) | 14% |

| Private‑label mass (2025) | ~16% |

What You See Is What You Get

Colgate-Palmolive Porter's Five Forces Analysis

This preview shows the exact Colgate‑Palmolive Porter’s Five Forces analysis you’ll receive after purchase—fully formatted, complete, and ready for immediate download; no placeholders or mockups.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Colgate-Palmolive navigates a mature, branded consumer goods market where supplier leverage is moderate, buyer power is mixed across retail channels, and rivalry is intense due to global competitors and innovation in oral care and personal care.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Colgate-Palmolive’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Commoditization of Raw Materials

The primary inputs for Colgate-Palmolive—chemicals, packaging, and agricultural feeds for Hill’s Pet Nutrition—are largely commoditized, with global supplier pools; in 2024 Colgate spent about $7.8 billion on cost of goods sold, so switching suppliers is feasible and low-cost for many inputs.

Scale-Driven Negotiation Leverage

As a global buyer, Colgate-Palmolive’s $18.0 billion 2024 revenue gives it scale-driven negotiation leverage, letting procurement secure volume discounts and extended credit; suppliers often accept thinner margins for steady orders—Colgate reported inventory purchases concentrated in a few large suppliers, enabling it to offset price inflation by ~1.2–1.8% through contractual rebates and bulk pricing in 2023–24.

Diversified Global Supplier Base

Colgate-Palmolive maintains a diversified supplier network across 40+ countries, reducing exposure to localized disruptions and limiting single-vendor risk.

By avoiding dependence on one region or supplier, Colgate can re-source quickly if vendors try to hike prices, protecting gross margin—gross margin was 53.2% in FY2024.

As of 2025 this diversification acts as a buffer against supplier-driven cost inflation, lowering procurement volatility and supporting stable COGS.

Vertical Integration Capabilities

Colgate-Palmolive (market cap $72.5B as of Dec 31, 2025) has the cash flow and technical R&D to vertically integrate into packaging or select chemical inputs, making backward integration credible.

This threat pressures suppliers to keep prices and innovation competitive, since in 2024 Colgate spent $1.1B on R&D and capital investments that could be reallocated to in-house production.

- Market cap $72.5B (Dec 31, 2025)

- $1.1B R&D/capex (2024)

- Credible backward integration deters supplier price hikes

Impact of Sustainability Requirements

While most Colgate-Palmolive suppliers have limited leverage, providers of patented green tech or certified sustainable ingredients exert slightly higher bargaining power amid stricter regs and consumer demand.

Meeting its 2025 sustainability goals may raise procurement costs; in 2024 Colgate spent about $850m on R&D and sustainability initiatives, enabling collaboration or in-house alternatives to limit supplier power.

- Specialized suppliers = higher leverage

- Patented green inputs can raise costs

- $850m R&D helps build alternatives

- Supplier power remains contained

Colgate's scale and $1.1B R&D/capex neutralize supplier power; 53.2% gross margin

Suppliers have limited power: commoditized inputs, global sourcing across 40+ countries, and Colgate’s $18.0B 2024 revenue and $1.1B 2024 R&D/capex give strong leverage and credible backward-integration threat; gross margin 53.2% (FY2024) and supplier rebates cut inflation impact ~1.2–1.8%. Specialized green/patented inputs carry higher leverage.

| Metric | Value |

|---|---|

| Revenue 2024 | $18.0B |

| Gross margin FY2024 | 53.2% |

| COGS 2024 | $7.8B |

| R&D/capex 2024 | $1.1B |

What is included in the product

Tailored exclusively for Colgate-Palmolive, this Porter's Five Forces overview uncovers key drivers of competition, buyer and supplier power, threats from substitutes and new entrants, and highlights disruptive forces and market dynamics that affect pricing, profitability, and market share.

A concise Porter's Five Forces snapshot for Colgate-Palmolive—instantly highlights competitive threats, supplier/buyer leverage, and substitution risk to speed strategic decisions and deck-ready insights.

Customers Bargaining Power

Consolidation of Retail Giants

Massive retailers such as Walmart, Amazon, and Target accounted for roughly 28–32% of Colgate‑Palmolive’s global sales by end‑2025, concentrating buying power and forcing the company to accept lower wholesale prices and deeper promotions.

These chains can demand prime shelf placement and co‑funded advertising; losing any would cut Colgate‑Palmolive’s revenue sharply, so the company concedes margins to retain access.

Low Consumer Switching Costs

Individual consumers face almost zero financial cost switching from Colgate toothpaste or Palmolive dish soap to rivals, so Colgate-Palmolive must spend to keep share; the company spent about $1.9 billion on advertising and marketing in full-year 2024 to support brand loyalty.

Growth of Private Label Brands

Retailers pushed private-label share for oral-care to about 14% in the US by 2024, and continued 2025 price pressure has raised private-label penetration in mass channels to ~16%, directly undercutting national brands like Colgate. These store brands match perceived quality at lower prices, competing for shelf space and promotional slots, which lets retailers demand deeper trade discounts from manufacturers. As consumers traded down during 2025 inflation, retailer leverage grew, squeezing Colgate-Palmolive gross margins—Colgate reported a 60 bps margin decline in 2024 tied partly to trade spend. Retailers’ control of assortments and promotions amplifies buyer bargaining power against Colgate.

High Price Sensitivity and Transparency

- Amazon market share for oral care ~28% (2024)

E-commerce and Direct-to-Consumer Shift

The rise of digital marketplaces has cut into traditional brand dominance; global e‑commerce sales hit 5.7 trillion USD in 2023 and food/household online penetration rose ~18% in 2024, giving consumers many niche and DTC options versus Colgate‑Palmolive.

Colgate’s direct channels (over 10% of sales in some regions by 2024) still face competition from indie brands, forcing faster product updates and active social listening to retain share.

- E‑commerce 5.7T USD (2023)

- Household online penetration ~18% (2024)

- Colgate DTC >10% sales in some regions (2024)

Retailer Power Erodes Colgate Margins: Rising Private Label, Bigger Trade Discounts

Buyers—large retailers (Walmart, Amazon, Target) accounting for ~28–32% of Colgate‑Palmolive sales by end‑2025—concentrate purchase power, demand prime placement and co‑funded promotions, and push private‑label penetration (US oral‑care private‑label ~14% in 2024, ~16% in mass by 2025), forcing deeper trade discounts and squeezing margins despite Colgate’s $1.9B marketing spend in 2024.

| Metric | Value |

|---|---|

| Retailer share of sales (2025) | 28–32% |

| Colgate marketing spend (2024) | $1.9B |

| US oral‑care private‑label (2024) | 14% |

| Private‑label mass (2025) | ~16% |

What You See Is What You Get

Colgate-Palmolive Porter's Five Forces Analysis

This preview shows the exact Colgate‑Palmolive Porter’s Five Forces analysis you’ll receive after purchase—fully formatted, complete, and ready for immediate download; no placeholders or mockups.