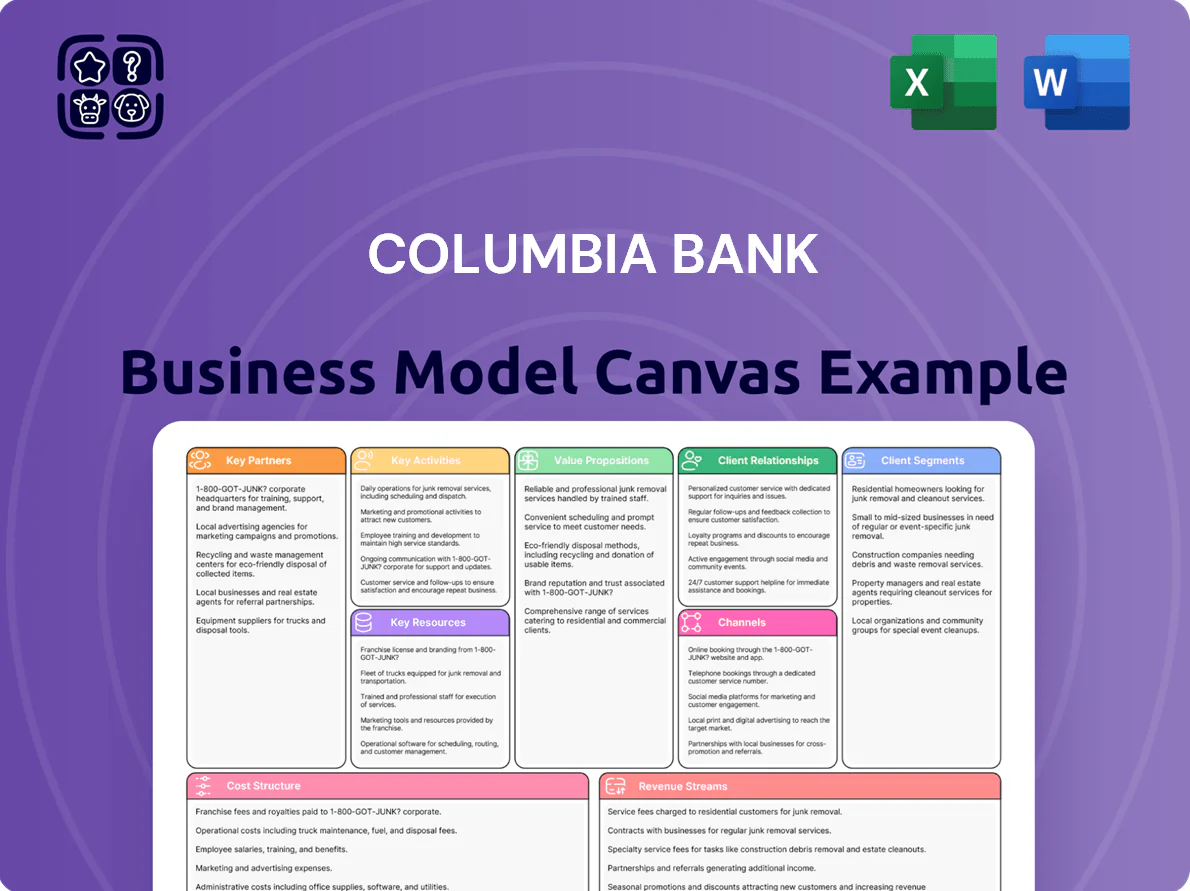

Columbia Bank Business Model Canvas

Columbia Bank BMC: Strategic Blueprint for Value, Customers & Revenue

Unlock the full strategic blueprint behind Columbia Bank’s business model—mapped across all nine BMC blocks with practical insights on value propositions, customer segments, and revenue levers.

Partnerships

Fintech and Technology Providers

Columbia Bank partners with fintechs to add digital banking and security features, supporting 24/7 mobile and online services that processed 62% of retail transactions in 2024; outsourcing APIs and cloud security lets the bank focus on client relationships while cutting platform development costs an estimated 18% year-over-year.

Regulatory and Government Agencies

The bank partners with the Federal Reserve, FDIC, and New York State Department of Financial Services to maintain its charter, meet Basel III-related capital ratios, and access liquidity tools like the Fed’s discount window; as of Q4 2025 Columbia Bank reported a CET1 ratio of 11.8% and insured deposits of $22.4 billion.

Credit Bureaus and Data Providers

Strategic alliances with major credit bureaus (Equifax, Experian, TransUnion) and specialty data providers give Columbia Bank real-time credit scores, payment histories, and small-business cash-flow signals—cutting underwriting time by ~30% and supporting a 2024-era default rate target below 0.8% on SBA and commercial loans. These feeds let underwriters assess borrower creditworthiness quickly and keep the loan portfolio healthy.

Community and Non-Profit Organizations

Collaborations with local community groups and non-profits help Columbia Bank meet Community Reinvestment Act obligations and boost local presence through financial literacy programs, community development loans, and event sponsorships—Columbia reported $412 million in community lending and investments in 2024.

These partnerships reinforce Columbia Bank’s community-centric brand and support regional economic growth, with over 120 nonprofit partnerships and 4,500 participants in financial education programs in 2024.

- 412 million community lending (2024)

- 120+ nonprofit partners (2024)

- 4,500 program participants (2024)

Mortgage Secondary Market Investors

Columbia Bank sells originated mortgages to government-sponsored enterprises (Fannie Mae, Freddie Mac) and private investors, which in 2024 funded roughly 40–60% of its mortgage originations, freeing capital to issue new loans and generating fee income per loan typically 0.5–1.25%.

This secondary-market flow trims long-term rate exposure and improves liquidity; for example, selling $500M of loans can free ~7–8% CET1-equivalent capital and reduce duration risk materially.

- Partners: Fannie Mae, Freddie Mac, private MBS buyers

- Fee income: ~0.5–1.25% per loan

- 2024 funding share: ~40–60% of originations

- Capital relief: ~7–8% CET1-equivalent on $500M sales

Columbia Bank scales digital lending, boosts community loans, preserves capital

Columbia Bank leverages fintechs, regulators, credit bureaus, nonprofits, and GSE/private mortgage buyers to scale digital services, manage liquidity and credit risk, meet CRA goals, and free capital—key 2024–Q4 2025 metrics: 62% digital transactions (2024), $412M community lending (2024), CET1 11.8% (Q4 2025), 40–60% mortgages sold (2024), fee income 0.5–1.25% per loan.

| Metric | Value |

|---|---|

| Digital tx share (2024) | 62% |

| Community lending (2024) | $412M |

| CET1 (Q4 2025) | 11.8% |

| Mortgages sold (2024) | 40–60% |

| Fee income per loan | 0.5–1.25% |

What is included in the product

A concise, ready-to-use Business Model Canvas for Columbia Bank detailing customer segments, channels, value propositions, key activities, resources, partners, cost structure, and revenue streams aligned with real-world operations and strategic goals.

High-level business model snapshot for Columbia Bank with editable cells to quickly pinpoint strategic strengths, customer segments, and revenue levers—ideal for boardrooms, team collaboration, or rapid competitive comparisons.

Activities

Commercial and Consumer Lending

Columbia Bank underwrites, originates, and services small business, commercial real estate, and consumer loans, evaluating credit, collateral, and cash flow to manage risk; lending drove 2024 asset growth to $30.8 billion and net interest income of $639 million through Sept 30, 2024.

Deposit and Liquidity Management

Managing a stable base of low-cost deposits funds Columbia Bank’s lending; as of Q4 2025 the bank reported $18.4 billion in deposits, with checking and savings making up ~62% of core balances, supporting net interest margin targets. The team oversees retail and commercial checking, savings, and CDs while optimizing liquidity and competitive rates to keep cost of funds low and meet regulatory LCR (liquidity coverage ratio) requirements.

Treasury and Cash Management Services

Columbia Bank offers treasury and cash-management tools—ACH, same-day ACH, wire transfers, payroll services, and swept accounts—to help SMEs manage daily cash flow; in 2024 treasury fees and commercial deposit balances drove ~22% of noninterest income, strengthening recurring revenue.

Risk Management and Compliance

Continuous monitoring of market, credit, and operational risks underpins Columbia Bank’s viability; in 2025 the bank reported a CET1 ratio of 11.8% and reduced nonperforming loans to 0.6% through tighter credit controls.

Anti-money laundering protocols, enhanced cybersecurity defenses, and quarterly internal audits—run by dedicated risk teams—cut potential loss exposure; Columbia allocates ~1.2% of revenue to compliance and security functions.

- Market/credit/ops monitoring daily

- AML, cyber, audits quarterly

- CET1 ratio 11.8% (2025)

- NPLs 0.6% (2025)

- Compliance spend ≈1.2% revenue

Digital Platform Development

- Annual IT spend: $45–60M

- Uptime target: 99.95%

- Y/Y digital growth: +28% (2024)

- Security: SOC 2 Type II, regular pen tests

- Release cadence: biweekly mobile updates

Scaling a $30.8B Bank: $45–60M IT Spend Drives 99.95% Uptime & 28% Digital Growth

Underwrite, originate, and service loans; manage deposits and liquidity; run treasury services; monitor credit/ops risk; maintain AML/cyber compliance; invest $45–60M/yr in digital platforms to hit 99.95% uptime and scale digital growth (+28% y/y).

| Metric | Value |

|---|---|

| Assets (2024) | $30.8B |

| Deposits (Q4 2025) | $18.4B |

| NII thru 9/30/24 | $639M |

| CET1 (2025) | 11.8% |

| NPLs (2025) | 0.6% |

| IT spend | $45–60M/yr |

| Uptime target | 99.95% |

Full Version Awaits

Business Model Canvas

The preview shown here is the exact Columbia Bank Business Model Canvas you will receive—no mockups or samples. Upon purchase, you’ll instantly download the complete, editable file formatted exactly as seen, ready for use in planning, presenting, or customizing. What you see is what you get—full content, no surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Columbia Bank BMC: Strategic Blueprint for Value, Customers & Revenue

Unlock the full strategic blueprint behind Columbia Bank’s business model—mapped across all nine BMC blocks with practical insights on value propositions, customer segments, and revenue levers.

Partnerships

Fintech and Technology Providers

Columbia Bank partners with fintechs to add digital banking and security features, supporting 24/7 mobile and online services that processed 62% of retail transactions in 2024; outsourcing APIs and cloud security lets the bank focus on client relationships while cutting platform development costs an estimated 18% year-over-year.

Regulatory and Government Agencies

The bank partners with the Federal Reserve, FDIC, and New York State Department of Financial Services to maintain its charter, meet Basel III-related capital ratios, and access liquidity tools like the Fed’s discount window; as of Q4 2025 Columbia Bank reported a CET1 ratio of 11.8% and insured deposits of $22.4 billion.

Credit Bureaus and Data Providers

Strategic alliances with major credit bureaus (Equifax, Experian, TransUnion) and specialty data providers give Columbia Bank real-time credit scores, payment histories, and small-business cash-flow signals—cutting underwriting time by ~30% and supporting a 2024-era default rate target below 0.8% on SBA and commercial loans. These feeds let underwriters assess borrower creditworthiness quickly and keep the loan portfolio healthy.

Community and Non-Profit Organizations

Collaborations with local community groups and non-profits help Columbia Bank meet Community Reinvestment Act obligations and boost local presence through financial literacy programs, community development loans, and event sponsorships—Columbia reported $412 million in community lending and investments in 2024.

These partnerships reinforce Columbia Bank’s community-centric brand and support regional economic growth, with over 120 nonprofit partnerships and 4,500 participants in financial education programs in 2024.

- 412 million community lending (2024)

- 120+ nonprofit partners (2024)

- 4,500 program participants (2024)

Mortgage Secondary Market Investors

Columbia Bank sells originated mortgages to government-sponsored enterprises (Fannie Mae, Freddie Mac) and private investors, which in 2024 funded roughly 40–60% of its mortgage originations, freeing capital to issue new loans and generating fee income per loan typically 0.5–1.25%.

This secondary-market flow trims long-term rate exposure and improves liquidity; for example, selling $500M of loans can free ~7–8% CET1-equivalent capital and reduce duration risk materially.

- Partners: Fannie Mae, Freddie Mac, private MBS buyers

- Fee income: ~0.5–1.25% per loan

- 2024 funding share: ~40–60% of originations

- Capital relief: ~7–8% CET1-equivalent on $500M sales

Columbia Bank scales digital lending, boosts community loans, preserves capital

Columbia Bank leverages fintechs, regulators, credit bureaus, nonprofits, and GSE/private mortgage buyers to scale digital services, manage liquidity and credit risk, meet CRA goals, and free capital—key 2024–Q4 2025 metrics: 62% digital transactions (2024), $412M community lending (2024), CET1 11.8% (Q4 2025), 40–60% mortgages sold (2024), fee income 0.5–1.25% per loan.

| Metric | Value |

|---|---|

| Digital tx share (2024) | 62% |

| Community lending (2024) | $412M |

| CET1 (Q4 2025) | 11.8% |

| Mortgages sold (2024) | 40–60% |

| Fee income per loan | 0.5–1.25% |

What is included in the product

A concise, ready-to-use Business Model Canvas for Columbia Bank detailing customer segments, channels, value propositions, key activities, resources, partners, cost structure, and revenue streams aligned with real-world operations and strategic goals.

High-level business model snapshot for Columbia Bank with editable cells to quickly pinpoint strategic strengths, customer segments, and revenue levers—ideal for boardrooms, team collaboration, or rapid competitive comparisons.

Activities

Commercial and Consumer Lending

Columbia Bank underwrites, originates, and services small business, commercial real estate, and consumer loans, evaluating credit, collateral, and cash flow to manage risk; lending drove 2024 asset growth to $30.8 billion and net interest income of $639 million through Sept 30, 2024.

Deposit and Liquidity Management

Managing a stable base of low-cost deposits funds Columbia Bank’s lending; as of Q4 2025 the bank reported $18.4 billion in deposits, with checking and savings making up ~62% of core balances, supporting net interest margin targets. The team oversees retail and commercial checking, savings, and CDs while optimizing liquidity and competitive rates to keep cost of funds low and meet regulatory LCR (liquidity coverage ratio) requirements.

Treasury and Cash Management Services

Columbia Bank offers treasury and cash-management tools—ACH, same-day ACH, wire transfers, payroll services, and swept accounts—to help SMEs manage daily cash flow; in 2024 treasury fees and commercial deposit balances drove ~22% of noninterest income, strengthening recurring revenue.

Risk Management and Compliance

Continuous monitoring of market, credit, and operational risks underpins Columbia Bank’s viability; in 2025 the bank reported a CET1 ratio of 11.8% and reduced nonperforming loans to 0.6% through tighter credit controls.

Anti-money laundering protocols, enhanced cybersecurity defenses, and quarterly internal audits—run by dedicated risk teams—cut potential loss exposure; Columbia allocates ~1.2% of revenue to compliance and security functions.

- Market/credit/ops monitoring daily

- AML, cyber, audits quarterly

- CET1 ratio 11.8% (2025)

- NPLs 0.6% (2025)

- Compliance spend ≈1.2% revenue

Digital Platform Development

- Annual IT spend: $45–60M

- Uptime target: 99.95%

- Y/Y digital growth: +28% (2024)

- Security: SOC 2 Type II, regular pen tests

- Release cadence: biweekly mobile updates

Scaling a $30.8B Bank: $45–60M IT Spend Drives 99.95% Uptime & 28% Digital Growth

Underwrite, originate, and service loans; manage deposits and liquidity; run treasury services; monitor credit/ops risk; maintain AML/cyber compliance; invest $45–60M/yr in digital platforms to hit 99.95% uptime and scale digital growth (+28% y/y).

| Metric | Value |

|---|---|

| Assets (2024) | $30.8B |

| Deposits (Q4 2025) | $18.4B |

| NII thru 9/30/24 | $639M |

| CET1 (2025) | 11.8% |

| NPLs (2025) | 0.6% |

| IT spend | $45–60M/yr |

| Uptime target | 99.95% |

Full Version Awaits

Business Model Canvas

The preview shown here is the exact Columbia Bank Business Model Canvas you will receive—no mockups or samples. Upon purchase, you’ll instantly download the complete, editable file formatted exactly as seen, ready for use in planning, presenting, or customizing. What you see is what you get—full content, no surprises.