Columbia Bank Business Model Canvas

Columbia Bank Business Model Canvas: A Concise Strategic Blueprint for Investors

Unlock the full strategic blueprint behind Columbia Bank’s business model — a concise, actionable Business Model Canvas that maps customer segments, value propositions, revenue streams, and key partnerships; ideal for investors, consultants, and founders seeking practical insights to benchmark or scale their strategies.

Partnerships

Fintech and Technology Infrastructure Providers

Columbia Bank partners with core banking vendors and fintechs to run advanced payment rails, mobile-security tooling, and analytics—cutting onboarding time by 30% and reducing fraud loss rates by ~18% versus 2019 regional peers.

Government and Regulatory Agencies

Active engagement with the Small Business Administration and federal agencies lets Columbia Bank offer SBA-backed loans and USDA rural lending; in 2024 SBA 7(a) and 504 guarantees helped banks support $38B in small-business lending nationally, enabling lower rates and partial guarantees for local firms.

Strong ties with regulators—FDIC, OCC, CFPB—ensure compliance with capital, liquidity and consumer rules through 2025; Columbia tracks CET1, LCR and stress-test guidance to avoid penalties and sustain community development lending.

Mortgage and Secondary Market Investors

Columbia Bank sells selected mortgage originations to secondary-market investors (GSEs and private funds), freeing capital to fund new community loans; in 2024 bank-level loan sales represented roughly 12–18% of originations, supporting a CET1 ratio near 10.5% and stable liquidity.

Community and Non-Profit Organizations

Strategic alliances with local non-profits and community development corporations help Columbia Bank meet Community Reinvestment Act requirements, funding financial literacy programs, affordable housing projects, and $4.2M in localized economic grants in 2024.

These partnerships embed the bank in community structures, boosting its brand as a socially responsible, locally focused institution and supporting measurable outcomes like a 12% increase in low-income mortgage originations year-over-year.

- Meets CRA obligations

- $4.2M in 2024 grants

- Financial literacy programs

- Affordable housing projects

- 12% rise in low-income mortgages

Third-Party Wealth Management and Insurance Affiliates

The bank partners with specialized investment and insurance firms to offer sophisticated wealth-management and risk-mitigation products without in-house overhead, boosting offerings for high-net-worth clients and business owners.

In 2025 Columbia Bank reported third-party referrals up 18% year-over-year and generated an estimated $12.4M in fee income from affiliate services, strengthening client retention and share-of-wallet.

- Expands product set quickly

- Reduces development costs

- Drives fee income ($12.4M in 2025)

- Improves retention (referrals +18% YoY)

Columbia Bank cuts onboarding 30%, trims fraud 18%, nets $12.4M fees & $4.2M grants

Columbia Bank leverages fintechs, GSE/private investors, SBA/USDA, regulators, local non-profits, and wealth/insurance partners to cut onboarding 30%, lower fraud ~18% vs 2019 peers, generate $12.4M fee income in 2025, and fund $4.2M community grants in 2024 while keeping CET1 ~10.5%.

| Partnership | Key 2024–25 Metric |

|---|---|

| Fintechs/core vendors | Onboarding −30% |

| Fraud tools | Loss −18% vs 2019 |

| SBA/USDA | Supports $38B national SBA lending (2024) |

| Secondary market | Loan sales 12–18% orig. |

| Community partners | $4.2M grants; +12% low‑income mortgages |

| Wealth/insurance partners | $12.4M fees; referrals +18% YoY (2025) |

| Regulators | CET1 ≈10.5%; LCR/compliance through 2025 |

What is included in the product

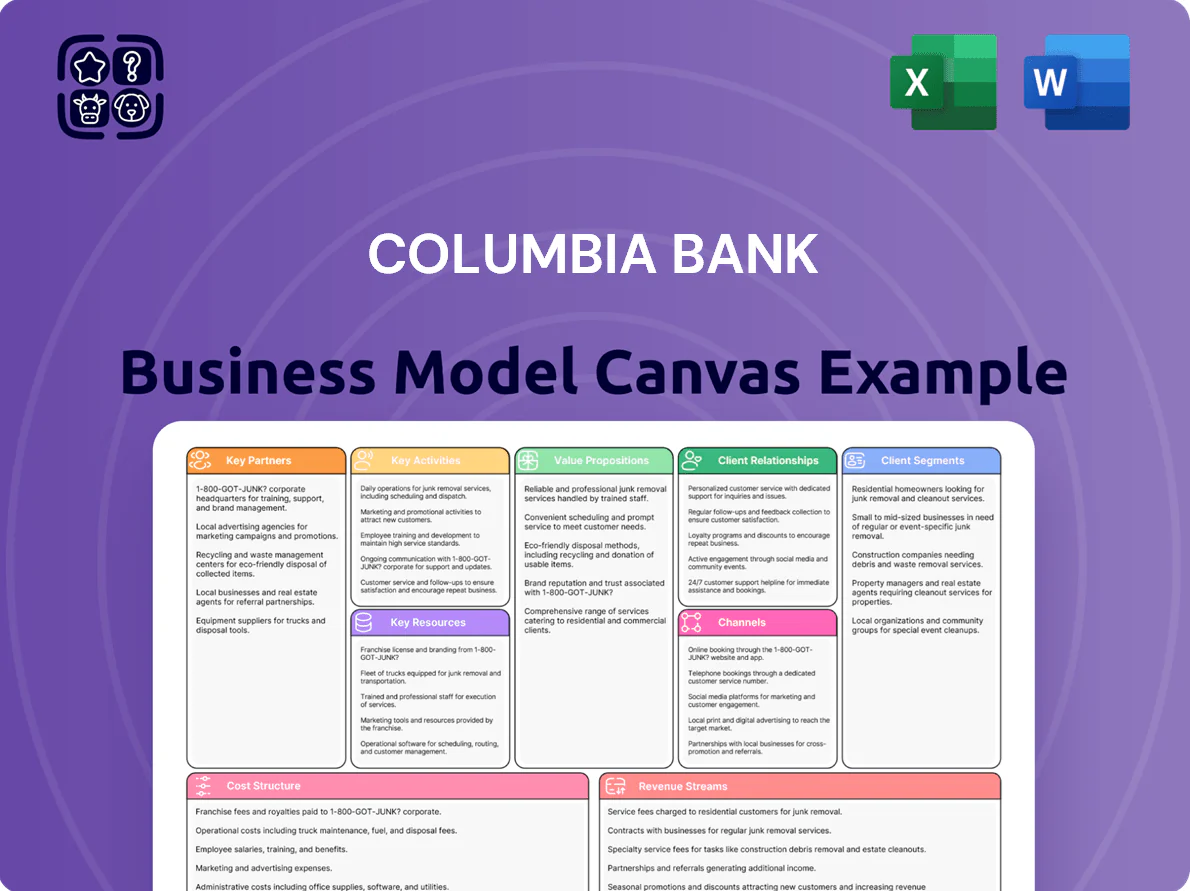

A concise, pre-written Business Model Canvas for Columbia Bank outlining customer segments, channels, value propositions, key activities, resources, partners, cost structure, and revenue streams with practical insights and competitive analysis for presentations, funding, and strategic decision-making.

Condenses Columbia Bank’s strategy into a digestible one-page Business Model Canvas, saving hours of setup and making it easy for teams to brainstorm, compare models, and present a clean, editable snapshot for meetings or executive summaries.

Activities

Commercial and Industrial Lending Operations

Columbia Bank underwrites and services C&I loans for West Coast SMBs, targeting expansion, equipment, and working capital; as of Q4 2025 their commercial loan book stood near $11.2B with $1.8B in SMB exposures. Rigorous credit analysis, covenant monitoring, and quarterly stress tests keep nonperforming assets low—NPL ratio ~0.45%—supporting portfolio quality and targeted loss reserves.

Deposit Gathering and Liquidity Management

Columbia Bank actively manages checking, savings, and CD products—$18.4 billion in deposits as of Q4 2025—to fund loans while targeting a lower cost of funds via mix optimization. Efficient liquidity management keeps cash and liquid securities above regulatory needs (liquid assets ~12% of assets) so customer withdrawals and stress scenarios are covered.

Digital Banking Innovation and Maintenance

Columbia Bank continuously updates mobile and online platforms—improving interfaces, adding biometric login, and rolling out real-time payments—to meet modern customer expectations; in 2024, banks with similar programs saw mobile adoption rise 14% and digital transactions grow 22% year-over-year, so Columbia targets 95% uptime and sub-2s page load for omnichannel access across mobile, web, and branch kiosks.

Risk Management and Regulatory Compliance

The bank deploys extensive monitoring of market, credit, and operational risks—using quarterly stress tests and monthly internal audits—to protect depositors and shareholders; in 2025 Columbia Bank reported a 95% pass rate on regulatory exams and a CET1 ratio of 12.8% as of Q1 2025.

Compliance enforces AML and KYC protocols, reducing SAR filing lag to 48 hours and supporting the bank’s license and market reputation.

- Quarterly stress tests

- Monthly internal audits

- CET1 12.8% (Q1 2025)

- 95% regulatory exam pass rate (2025)

- SAR filing lag 48 hours

Relationship Management and Advisory Services

Personalized relationship management drives Columbia Bank’s model: relationship managers proactively contact business and individual clients, delivering strategic advice on cash management, succession planning, and personal wealth goals to deepen lifetime value.

This advisory approach helped Columbia Banking System report 2025 fee income growth of 7.2% year-over-year and raised client retention above 89%, shifting revenue mix toward higher-margin advisory services.

- Proactive outreach to businesses and households

- Advice: cash management, succession, wealth goals

- 2025 fee income +7.2% YoY

- Client retention ~89%

Columbia Bank: $13B C&I book, $18.4B deposits, 12.8% CET1, low NPLs, +7.2% fee growth

Columbia Bank underwrites C&I loans (commercial book ~$11.2B, SMB ~$1.8B), manages deposits ($18.4B), maintains CET1 12.8% and NPL ~0.45%, runs quarterly stress tests and monthly audits, and grows fee income (+7.2% YoY) with ~89% retention.

| Metric | Value |

|---|---|

| Commercial loans | $11.2B |

| SMB loans | $1.8B |

| Deposits | $18.4B |

| CET1 | 12.8% |

| NPL | 0.45% |

| Fee income growth | +7.2% YoY |

| Retention | 89% |

Preview Before You Purchase

Business Model Canvas

The preview you see is the actual Columbia Bank Business Model Canvas—not a mockup—and it exactly matches the file you’ll receive after purchase.

When you complete your order, you’ll instantly get this same professional, ready-to-edit document in full, formatted for immediate use with no changes or missing sections.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Columbia Bank Business Model Canvas: A Concise Strategic Blueprint for Investors

Unlock the full strategic blueprint behind Columbia Bank’s business model — a concise, actionable Business Model Canvas that maps customer segments, value propositions, revenue streams, and key partnerships; ideal for investors, consultants, and founders seeking practical insights to benchmark or scale their strategies.

Partnerships

Fintech and Technology Infrastructure Providers

Columbia Bank partners with core banking vendors and fintechs to run advanced payment rails, mobile-security tooling, and analytics—cutting onboarding time by 30% and reducing fraud loss rates by ~18% versus 2019 regional peers.

Government and Regulatory Agencies

Active engagement with the Small Business Administration and federal agencies lets Columbia Bank offer SBA-backed loans and USDA rural lending; in 2024 SBA 7(a) and 504 guarantees helped banks support $38B in small-business lending nationally, enabling lower rates and partial guarantees for local firms.

Strong ties with regulators—FDIC, OCC, CFPB—ensure compliance with capital, liquidity and consumer rules through 2025; Columbia tracks CET1, LCR and stress-test guidance to avoid penalties and sustain community development lending.

Mortgage and Secondary Market Investors

Columbia Bank sells selected mortgage originations to secondary-market investors (GSEs and private funds), freeing capital to fund new community loans; in 2024 bank-level loan sales represented roughly 12–18% of originations, supporting a CET1 ratio near 10.5% and stable liquidity.

Community and Non-Profit Organizations

Strategic alliances with local non-profits and community development corporations help Columbia Bank meet Community Reinvestment Act requirements, funding financial literacy programs, affordable housing projects, and $4.2M in localized economic grants in 2024.

These partnerships embed the bank in community structures, boosting its brand as a socially responsible, locally focused institution and supporting measurable outcomes like a 12% increase in low-income mortgage originations year-over-year.

- Meets CRA obligations

- $4.2M in 2024 grants

- Financial literacy programs

- Affordable housing projects

- 12% rise in low-income mortgages

Third-Party Wealth Management and Insurance Affiliates

The bank partners with specialized investment and insurance firms to offer sophisticated wealth-management and risk-mitigation products without in-house overhead, boosting offerings for high-net-worth clients and business owners.

In 2025 Columbia Bank reported third-party referrals up 18% year-over-year and generated an estimated $12.4M in fee income from affiliate services, strengthening client retention and share-of-wallet.

- Expands product set quickly

- Reduces development costs

- Drives fee income ($12.4M in 2025)

- Improves retention (referrals +18% YoY)

Columbia Bank cuts onboarding 30%, trims fraud 18%, nets $12.4M fees & $4.2M grants

Columbia Bank leverages fintechs, GSE/private investors, SBA/USDA, regulators, local non-profits, and wealth/insurance partners to cut onboarding 30%, lower fraud ~18% vs 2019 peers, generate $12.4M fee income in 2025, and fund $4.2M community grants in 2024 while keeping CET1 ~10.5%.

| Partnership | Key 2024–25 Metric |

|---|---|

| Fintechs/core vendors | Onboarding −30% |

| Fraud tools | Loss −18% vs 2019 |

| SBA/USDA | Supports $38B national SBA lending (2024) |

| Secondary market | Loan sales 12–18% orig. |

| Community partners | $4.2M grants; +12% low‑income mortgages |

| Wealth/insurance partners | $12.4M fees; referrals +18% YoY (2025) |

| Regulators | CET1 ≈10.5%; LCR/compliance through 2025 |

What is included in the product

A concise, pre-written Business Model Canvas for Columbia Bank outlining customer segments, channels, value propositions, key activities, resources, partners, cost structure, and revenue streams with practical insights and competitive analysis for presentations, funding, and strategic decision-making.

Condenses Columbia Bank’s strategy into a digestible one-page Business Model Canvas, saving hours of setup and making it easy for teams to brainstorm, compare models, and present a clean, editable snapshot for meetings or executive summaries.

Activities

Commercial and Industrial Lending Operations

Columbia Bank underwrites and services C&I loans for West Coast SMBs, targeting expansion, equipment, and working capital; as of Q4 2025 their commercial loan book stood near $11.2B with $1.8B in SMB exposures. Rigorous credit analysis, covenant monitoring, and quarterly stress tests keep nonperforming assets low—NPL ratio ~0.45%—supporting portfolio quality and targeted loss reserves.

Deposit Gathering and Liquidity Management

Columbia Bank actively manages checking, savings, and CD products—$18.4 billion in deposits as of Q4 2025—to fund loans while targeting a lower cost of funds via mix optimization. Efficient liquidity management keeps cash and liquid securities above regulatory needs (liquid assets ~12% of assets) so customer withdrawals and stress scenarios are covered.

Digital Banking Innovation and Maintenance

Columbia Bank continuously updates mobile and online platforms—improving interfaces, adding biometric login, and rolling out real-time payments—to meet modern customer expectations; in 2024, banks with similar programs saw mobile adoption rise 14% and digital transactions grow 22% year-over-year, so Columbia targets 95% uptime and sub-2s page load for omnichannel access across mobile, web, and branch kiosks.

Risk Management and Regulatory Compliance

The bank deploys extensive monitoring of market, credit, and operational risks—using quarterly stress tests and monthly internal audits—to protect depositors and shareholders; in 2025 Columbia Bank reported a 95% pass rate on regulatory exams and a CET1 ratio of 12.8% as of Q1 2025.

Compliance enforces AML and KYC protocols, reducing SAR filing lag to 48 hours and supporting the bank’s license and market reputation.

- Quarterly stress tests

- Monthly internal audits

- CET1 12.8% (Q1 2025)

- 95% regulatory exam pass rate (2025)

- SAR filing lag 48 hours

Relationship Management and Advisory Services

Personalized relationship management drives Columbia Bank’s model: relationship managers proactively contact business and individual clients, delivering strategic advice on cash management, succession planning, and personal wealth goals to deepen lifetime value.

This advisory approach helped Columbia Banking System report 2025 fee income growth of 7.2% year-over-year and raised client retention above 89%, shifting revenue mix toward higher-margin advisory services.

- Proactive outreach to businesses and households

- Advice: cash management, succession, wealth goals

- 2025 fee income +7.2% YoY

- Client retention ~89%

Columbia Bank: $13B C&I book, $18.4B deposits, 12.8% CET1, low NPLs, +7.2% fee growth

Columbia Bank underwrites C&I loans (commercial book ~$11.2B, SMB ~$1.8B), manages deposits ($18.4B), maintains CET1 12.8% and NPL ~0.45%, runs quarterly stress tests and monthly audits, and grows fee income (+7.2% YoY) with ~89% retention.

| Metric | Value |

|---|---|

| Commercial loans | $11.2B |

| SMB loans | $1.8B |

| Deposits | $18.4B |

| CET1 | 12.8% |

| NPL | 0.45% |

| Fee income growth | +7.2% YoY |

| Retention | 89% |

Preview Before You Purchase

Business Model Canvas

The preview you see is the actual Columbia Bank Business Model Canvas—not a mockup—and it exactly matches the file you’ll receive after purchase.

When you complete your order, you’ll instantly get this same professional, ready-to-edit document in full, formatted for immediate use with no changes or missing sections.