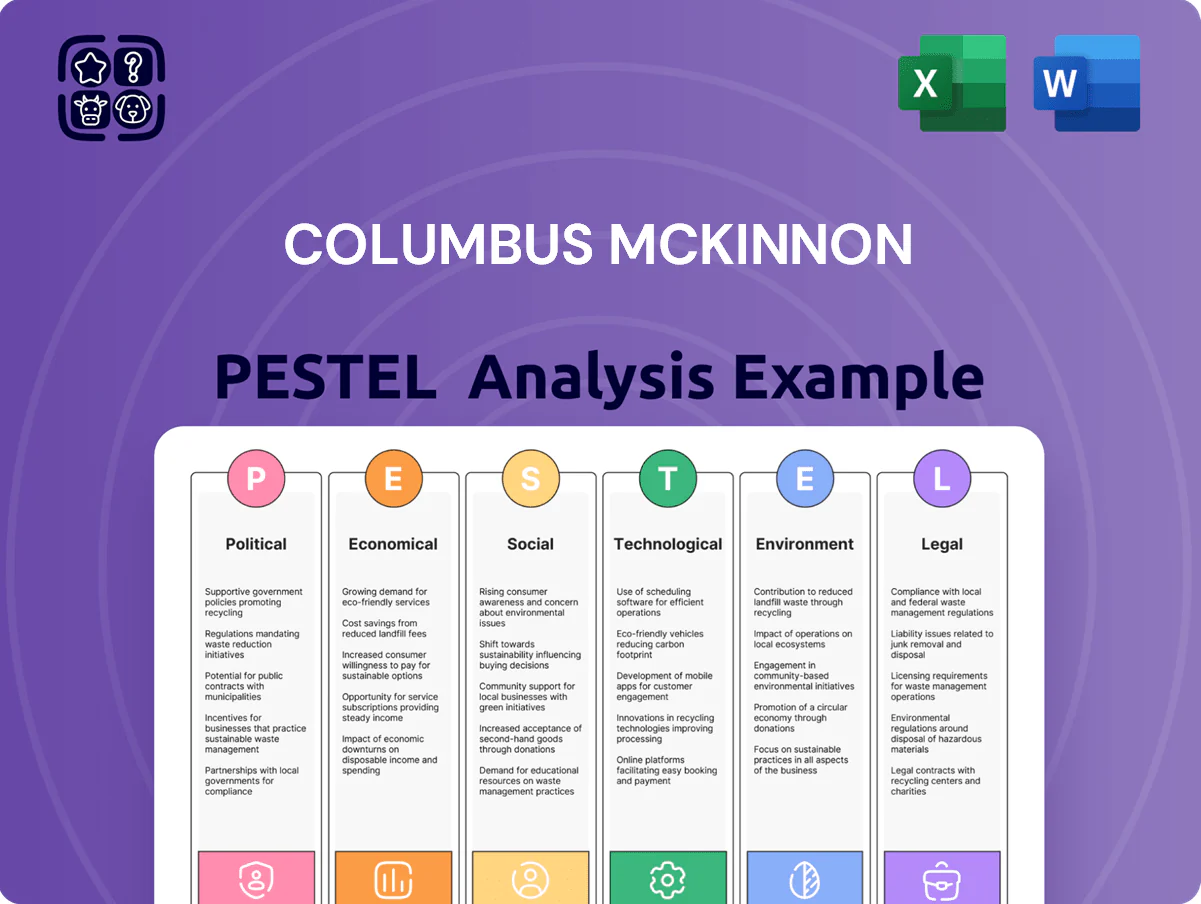

Columbus McKinnon PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Navigate political headwinds, supply-chain shifts, and tech disruption with our targeted PESTLE Analysis of Columbus McKinnon—concise, actionable, and industry-focused to sharpen your strategic decisions. Purchase the full report for the complete external-risk map, editable charts, and foresight you can deploy immediately.

Political factors

Global Trade Tariffs and Protectionism

Columbus McKinnon depends on international supply chains and cross-border sales, making it vulnerable to shifting U.S.-China-EU trade policies; in 2024 roughly 28% of global crane component steel flowed through affected trade lanes. Increased tariffs on steel or aluminum—tariff hikes of 10–25% seen in recent actions—could raise raw material costs materially, given steel is ~18–22% of BOM for hoists. Geopolitical tensions have pushed peers to reconfigure manufacturing hubs, and CMCO reported 15% of production already shifted regionally by 2025 to mitigate trade-barrier risks.

Government Infrastructure Spending Programs

The 2021 Infrastructure Investment and Jobs Act allocates about $550 billion to transportation and utilities, boosting demand for material-handling equipment used in construction and grid upgrades—Columbus McKinnon (CMCO) stands to benefit from increased lifting-equipment orders in these sectors.

Buy American provisions and Buy America requirements for federally funded projects favor domestic suppliers; CMCO’s US manufacturing footprint and $476.8 million 2024 revenue support competitive positioning for government contracts.

Shifts in federal budget allocations or state-level reprioritizations could compress the multi-year sales pipeline for heavy-duty lifting solutions; a 10% slowdown in infrastructure spend would materially affect backlog-sensitive OEMs like CMCO.

Stability in Emerging Markets

Expansion into Southeast Asia and Latin America exposes Columbus McKinnon to political volatility and regulatory shifts; IMF data shows these regions accounted for about 18% of global GDP growth in 2024, but country risk ratings vary widely, with several markets having sovereign risk scores below investment grade.

Local unrest or abrupt leadership changes can disrupt operations, delay project approvals, and raise security costs—incident-related downtime in the region averaged 4–6% of annual operating days in 2023–24 for industrial firms.

Strategic planning should incorporate political risk profiles, country limits and insurance costs, noting that political risk insurance premiums rose roughly 12% globally in 2024, to protect consistent revenue streams.

Defense and Aerospace Regulations

As a provider of motion solutions for sensitive industries, Columbus McKinnon must navigate stringent government procurement policies and export controls, with US defense procurement funding at roughly $918 billion in FY2024 influencing contract availability.

Compliance with International Traffic in Arms Regulations (ITAR) is critical to retain defense and aerospace contracts; noncompliance risks fines, delistings, and lost revenue—US export enforcement actions led to over $1.2 billion in penalties in recent years.

Political decisions on military spending and aerospace R&D drive demand for high-margin specialized equipment, with global aerospace R&D investment exceeding $90 billion in 2023, directly affecting order volumes for engineered lifting and motion systems.

- Must comply with ITAR to keep defense contracts

- US defense budget ($918B FY2024) shapes procurement opportunity

- Export enforcement penalties can exceed billions

- Aerospace R&D spending (~$90B+ global 2023) impacts specialized equipment orders

Labor Union Relations and Legislation

- Potential 5–10% rise in labor costs

- 22% of operating costs = labor (FY2024)

- 40% production in union-prone facilities

- Strikes risk 3–7% monthly output loss

Political risks—tariffs, Buy America, unions & defense shifts threaten CMCO costs & supply

Political risks—trade tariffs (10–25%), Buy America rules, ITAR/export controls, defense budget ($918B FY2024), and unionization—directly affect CMCO costs, contracts, and supply chains; 2024/25 data: steel = 18–22% BOM, US revenue $476.8M, 40% production in union-prone facilities, labor = 22% of operating costs, 15% production shifted by 2025, political risk insurance +12% (2024).

| Metric | Value |

|---|---|

| Steel % of BOM | 18–22% |

| US Revenue (2024) | $476.8M |

| Defense Budget FY2024 | $918B |

| Labor % of Op Costs | 22% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Columbus McKinnon across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and forward-looking scenarios to identify risks and opportunities for executives and investors.

A concise, visually segmented PESTLE summary of Columbus McKinnon that can be dropped into presentations or planning sessions to align teams quickly and support risk‑focused discussions.

Economic factors

Cyclical Nature of Industrial Production

Demand for Columbus McKinnon material handling products tracks industrial output; US industrial production fell 0.1% in 2024 Q3 year-over-year, pressuring orders as manufacturers cut capex.

During downturns customers defer investments—global crane and hoist shipments fell about 6% in 2023—reducing new equipment sales and aftermarket revenue for CMCO.

Conversely, manufacturing PMI recovery (US PMI ~51.5 in Dec 2024) and e‑commerce warehouse expansion drove renewed demand, supporting backlog growth into 2025.

Fluctuations in Raw Material Costs

The profitability of Columbus McKinnon is sensitive to steel, copper and specialized electronic component prices; steel rose ~18% in 2024 and copper averaged $8,400/ton in 2025, elevating input costs for FY2024-25.

Volatility in global commodity markets can compress margins if surcharges lag; CMCO reported gross margin of 26.1% in FY2024, down from 28.4% in FY2023, partly reflecting material inflation.

Strategic hedging and multi-year supplier contracts are deployed to stabilize costs; management indicated in 2025 that hedges and long-term agreements covered roughly 40–60% of key inputs to mitigate short-term price shocks.

Interest Rate Environment and Capital Access

High interest rates raise borrowing costs for Columbus McKinnon and its customers, which in 2024 saw the US Federal Funds rate at 5.25–5.50%, likely dampening large infrastructure projects and order velocity for heavy-lift equipment.

Currency Exchange Rate Volatility

As a global manufacturer, Columbus McKinnon faces FX risk repatriating earnings; in 2025 roughly 18% of revenue came from outside the U.S., amplifying exposure to currency moves.

A strong U.S. dollar in 2024-25 compressed reported international sales and made exports pricier in key markets like Europe and China.

Management actively uses derivatives—forward contracts and options—to hedge major currencies (notably EUR and CNY), reducing reported FX volatility.

- ~18% FY2025 revenue from international operations

- Hedging program targets EUR and CNY

- Strong USD lowers foreign-reported sales and export competitiveness

Energy Prices and Operational Costs

The cost of energy drives Columbus McKinnon’s manufacturing and global logistics: in 2024 US industrial electricity averaged about 9.9 cents/kWh and diesel averaged roughly $4.15/gal, raising factory operating costs and carrier rates for heavy machinery shipments.

Higher fuel and electricity increased total ownership costs, pressuring margins; energy-efficient initiatives (LED, motor drives, process heat recovery) and a 3–5% reduction in energy intensity targets help sustain competitiveness amid 4–6% inflation in manufacturing input costs (2023–2024).

- 2024 US industrial electricity ~9.9 cents/kWh

- 2024 diesel ~$4.15/gal impacting shipping

- Manufacturing input inflation ~4–6% (2023–24)

- Energy-efficiency targets: 3–5% energy intensity reduction

CMCO margins squeezed as industrial demand lags, input costs surge and FX risk rises

Industrial demand drives CMCO: US industrial production fell 0.1% in 2024 Q3 while US PMI ~51.5 in Dec 2024; material costs rose (steel +18% in 2024; copper ~$8,400/ton in 2025) compressing gross margin to 26.1% in FY2024; FY2025 ~18% revenue ex‑US exposes FX risk amid strong USD and Fed funds 5.25–5.50% in 2024 raising financing costs.

| Metric | Value |

|---|---|

| US industrial prod. (2024 Q3) | -0.1% |

| US PMI (Dec 2024) | 51.5 |

| Steel (2024) | +18% |

| Copper (2025) | $8,400/ton |

| Gross margin FY2024 | 26.1% |

| Intl rev FY2025 | ~18% |

| Fed funds (2024) | 5.25–5.50% |

Preview the Actual Deliverable

Columbus McKinnon PESTLE Analysis

The preview shown here is the exact Columbus McKinnon PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Navigate political headwinds, supply-chain shifts, and tech disruption with our targeted PESTLE Analysis of Columbus McKinnon—concise, actionable, and industry-focused to sharpen your strategic decisions. Purchase the full report for the complete external-risk map, editable charts, and foresight you can deploy immediately.

Political factors

Global Trade Tariffs and Protectionism

Columbus McKinnon depends on international supply chains and cross-border sales, making it vulnerable to shifting U.S.-China-EU trade policies; in 2024 roughly 28% of global crane component steel flowed through affected trade lanes. Increased tariffs on steel or aluminum—tariff hikes of 10–25% seen in recent actions—could raise raw material costs materially, given steel is ~18–22% of BOM for hoists. Geopolitical tensions have pushed peers to reconfigure manufacturing hubs, and CMCO reported 15% of production already shifted regionally by 2025 to mitigate trade-barrier risks.

Government Infrastructure Spending Programs

The 2021 Infrastructure Investment and Jobs Act allocates about $550 billion to transportation and utilities, boosting demand for material-handling equipment used in construction and grid upgrades—Columbus McKinnon (CMCO) stands to benefit from increased lifting-equipment orders in these sectors.

Buy American provisions and Buy America requirements for federally funded projects favor domestic suppliers; CMCO’s US manufacturing footprint and $476.8 million 2024 revenue support competitive positioning for government contracts.

Shifts in federal budget allocations or state-level reprioritizations could compress the multi-year sales pipeline for heavy-duty lifting solutions; a 10% slowdown in infrastructure spend would materially affect backlog-sensitive OEMs like CMCO.

Stability in Emerging Markets

Expansion into Southeast Asia and Latin America exposes Columbus McKinnon to political volatility and regulatory shifts; IMF data shows these regions accounted for about 18% of global GDP growth in 2024, but country risk ratings vary widely, with several markets having sovereign risk scores below investment grade.

Local unrest or abrupt leadership changes can disrupt operations, delay project approvals, and raise security costs—incident-related downtime in the region averaged 4–6% of annual operating days in 2023–24 for industrial firms.

Strategic planning should incorporate political risk profiles, country limits and insurance costs, noting that political risk insurance premiums rose roughly 12% globally in 2024, to protect consistent revenue streams.

Defense and Aerospace Regulations

As a provider of motion solutions for sensitive industries, Columbus McKinnon must navigate stringent government procurement policies and export controls, with US defense procurement funding at roughly $918 billion in FY2024 influencing contract availability.

Compliance with International Traffic in Arms Regulations (ITAR) is critical to retain defense and aerospace contracts; noncompliance risks fines, delistings, and lost revenue—US export enforcement actions led to over $1.2 billion in penalties in recent years.

Political decisions on military spending and aerospace R&D drive demand for high-margin specialized equipment, with global aerospace R&D investment exceeding $90 billion in 2023, directly affecting order volumes for engineered lifting and motion systems.

- Must comply with ITAR to keep defense contracts

- US defense budget ($918B FY2024) shapes procurement opportunity

- Export enforcement penalties can exceed billions

- Aerospace R&D spending (~$90B+ global 2023) impacts specialized equipment orders

Labor Union Relations and Legislation

- Potential 5–10% rise in labor costs

- 22% of operating costs = labor (FY2024)

- 40% production in union-prone facilities

- Strikes risk 3–7% monthly output loss

Political risks—tariffs, Buy America, unions & defense shifts threaten CMCO costs & supply

Political risks—trade tariffs (10–25%), Buy America rules, ITAR/export controls, defense budget ($918B FY2024), and unionization—directly affect CMCO costs, contracts, and supply chains; 2024/25 data: steel = 18–22% BOM, US revenue $476.8M, 40% production in union-prone facilities, labor = 22% of operating costs, 15% production shifted by 2025, political risk insurance +12% (2024).

| Metric | Value |

|---|---|

| Steel % of BOM | 18–22% |

| US Revenue (2024) | $476.8M |

| Defense Budget FY2024 | $918B |

| Labor % of Op Costs | 22% |

What is included in the product

Explores how external macro-environmental factors uniquely affect Columbus McKinnon across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven insights and forward-looking scenarios to identify risks and opportunities for executives and investors.

A concise, visually segmented PESTLE summary of Columbus McKinnon that can be dropped into presentations or planning sessions to align teams quickly and support risk‑focused discussions.

Economic factors

Cyclical Nature of Industrial Production

Demand for Columbus McKinnon material handling products tracks industrial output; US industrial production fell 0.1% in 2024 Q3 year-over-year, pressuring orders as manufacturers cut capex.

During downturns customers defer investments—global crane and hoist shipments fell about 6% in 2023—reducing new equipment sales and aftermarket revenue for CMCO.

Conversely, manufacturing PMI recovery (US PMI ~51.5 in Dec 2024) and e‑commerce warehouse expansion drove renewed demand, supporting backlog growth into 2025.

Fluctuations in Raw Material Costs

The profitability of Columbus McKinnon is sensitive to steel, copper and specialized electronic component prices; steel rose ~18% in 2024 and copper averaged $8,400/ton in 2025, elevating input costs for FY2024-25.

Volatility in global commodity markets can compress margins if surcharges lag; CMCO reported gross margin of 26.1% in FY2024, down from 28.4% in FY2023, partly reflecting material inflation.

Strategic hedging and multi-year supplier contracts are deployed to stabilize costs; management indicated in 2025 that hedges and long-term agreements covered roughly 40–60% of key inputs to mitigate short-term price shocks.

Interest Rate Environment and Capital Access

High interest rates raise borrowing costs for Columbus McKinnon and its customers, which in 2024 saw the US Federal Funds rate at 5.25–5.50%, likely dampening large infrastructure projects and order velocity for heavy-lift equipment.

Currency Exchange Rate Volatility

As a global manufacturer, Columbus McKinnon faces FX risk repatriating earnings; in 2025 roughly 18% of revenue came from outside the U.S., amplifying exposure to currency moves.

A strong U.S. dollar in 2024-25 compressed reported international sales and made exports pricier in key markets like Europe and China.

Management actively uses derivatives—forward contracts and options—to hedge major currencies (notably EUR and CNY), reducing reported FX volatility.

- ~18% FY2025 revenue from international operations

- Hedging program targets EUR and CNY

- Strong USD lowers foreign-reported sales and export competitiveness

Energy Prices and Operational Costs

The cost of energy drives Columbus McKinnon’s manufacturing and global logistics: in 2024 US industrial electricity averaged about 9.9 cents/kWh and diesel averaged roughly $4.15/gal, raising factory operating costs and carrier rates for heavy machinery shipments.

Higher fuel and electricity increased total ownership costs, pressuring margins; energy-efficient initiatives (LED, motor drives, process heat recovery) and a 3–5% reduction in energy intensity targets help sustain competitiveness amid 4–6% inflation in manufacturing input costs (2023–2024).

- 2024 US industrial electricity ~9.9 cents/kWh

- 2024 diesel ~$4.15/gal impacting shipping

- Manufacturing input inflation ~4–6% (2023–24)

- Energy-efficiency targets: 3–5% energy intensity reduction

CMCO margins squeezed as industrial demand lags, input costs surge and FX risk rises

Industrial demand drives CMCO: US industrial production fell 0.1% in 2024 Q3 while US PMI ~51.5 in Dec 2024; material costs rose (steel +18% in 2024; copper ~$8,400/ton in 2025) compressing gross margin to 26.1% in FY2024; FY2025 ~18% revenue ex‑US exposes FX risk amid strong USD and Fed funds 5.25–5.50% in 2024 raising financing costs.

| Metric | Value |

|---|---|

| US industrial prod. (2024 Q3) | -0.1% |

| US PMI (Dec 2024) | 51.5 |

| Steel (2024) | +18% |

| Copper (2025) | $8,400/ton |

| Gross margin FY2024 | 26.1% |

| Intl rev FY2025 | ~18% |

| Fed funds (2024) | 5.25–5.50% |

Preview the Actual Deliverable

Columbus McKinnon PESTLE Analysis

The preview shown here is the exact Columbus McKinnon PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.