Comcast Porter's Five Forces Analysis

From Overview to Strategy Blueprint

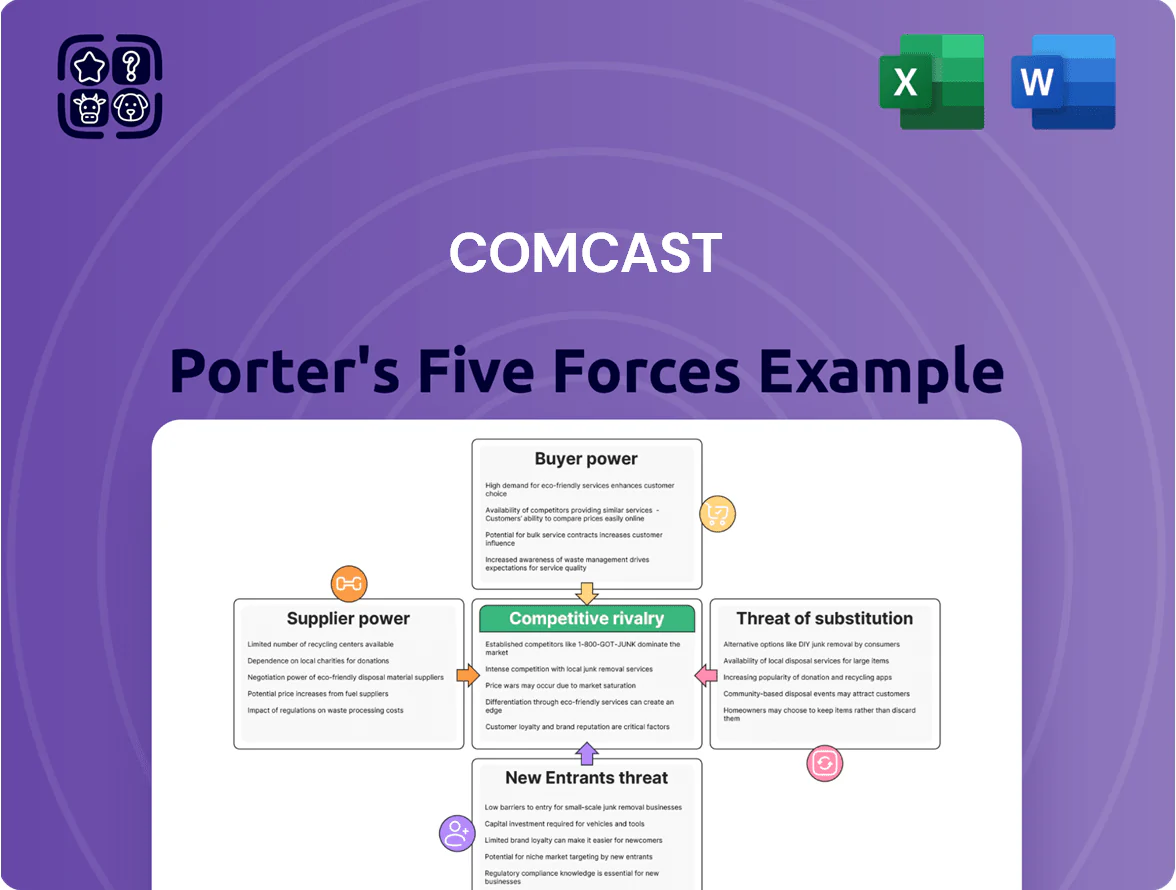

Comcast faces intense rivalry from cable and streaming competitors, moderate supplier leverage from content partners, and rising substitute threats as OTT services expand; buyer power grows with cord-cutting trends while regulatory barriers temper new entrants.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Comcast’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Content Licensing and Sports Rights

The cost of exclusive sports rights pushes supplier power up: Comcast paid about $2.8B annually for NBC Sports regional deals and faces bids where NFL/Amazon deals topped $10B in 2023, forcing higher pay-TV and Peacock licensing spend.

Infrastructure and Network Equipment Vendors

Labor Unions and Specialized Talent

The media and telecom sector is shaped by unions—writers, actors, and engineers—whose strikes in 2023 cost US studios an estimated $1.5–2.0 billion in lost production revenue; that collective leverage raises suppliers’ bargaining power versus Comcast.

Recent SAG-AFTRA and WGA actions secured better residuals and AI protections, pressuring Comcast to raise content spending (NBCUniversal’s 2024 content budget rose ~10% year-over-year) to retain talent.

Specialized engineers for networks and streaming are scarce; median pay for senior broadcast engineers rose ~8% in 2024, so Comcast faces upward labor-cost pressure while needing continuous original output for Peacock and global channels.

Cloud Computing and Third-Party Data Services

As Comcast shifts more of Peacock and Xfinity to cloud platforms, dependence on AWS, Google Cloud, and Microsoft Azure rises, giving those providers leverage over storage, compute, and CDN costs; in 2024 hyperscalers earned over $700B combined, underscoring scale advantage.

Hybrid architectures reduce some risk, but persistent high data egress fees (often $0.05–0.12/GB) and integration lock-in raise long-term supplier bargaining power and operating expense sensitivity.

- Major suppliers: AWS, Google Cloud, Microsoft Azure

- 2024 hyperscaler revenue > $700B combined

- Typical egress: $0.05–0.12 per GB

- Hybrid use lowers but doesn't remove dependence

Energy and Utility Providers

Comcast's vast network and data centers consume large electricity and cooling; in 2024 its total energy spend exceeded $1.1 billion, leaving it exposed to utility price swings and local energy regulations.

Meeting its 2035 carbon‑neutral target raises reliance on renewable suppliers, pushing short‑term procurement costs up—Comcast bought ~280 MW of renewables contracts by 2025 but still offsets residual emissions.

Supplier power is moderate: utilities hold pricing leverage regionally, while large renewables deals give Comcast some bargaining clout but require capital and long-term commitments.

- 2024 energy spend ~$1.1B

- ~280 MW renewables contracted by 2025

- 2035 carbon‑neutral target increases procurement costs

- Regional utility pricing gives suppliers moderate leverage

Moderate supplier power: $2.8B NBC rights, $1.1B energy, capex sensitivity ~$1.6B

Supplier bargaining power is moderate: concentrated content, cloud, hardware, labor, and energy suppliers can drive costs—NBC sports rights (~$2.8B/yr), hyperscaler egress $0.05–0.12/GB, 2024 energy spend ~$1.1B, ~280 MW renewables by 2025—so supply shocks or price hikes (10% capex impact ≈ $1.6B) materially affect Comcast.

| Metric | 2024–25 |

|---|---|

| NBC regional rights | $2.8B/yr |

| Hyperscaler egress | $0.05–0.12/GB |

| Energy spend | $1.1B |

| Renewables procured | ~280 MW |

| Capex guidance | $16B (2025) |

What is included in the product

Tailored Porter’s Five Forces analysis for Comcast, uncovering key competitive drivers, buyer and supplier power, threats from substitutes and new entrants, and strategic barriers protecting incumbent profitability.

Concise Comcast Porter’s Five Forces snapshot—quickly gauge competitive intensity across content, distribution, and tech to inform strategic moves.

Customers Bargaining Power

Low Switching Costs in Streaming

The shift from multi-year cable deals to month-to-month streaming subscriptions has raised customer bargaining power: in 2024 Peacock cancellations were reversible with one click and U.S. streaming churn averaged ~21% annually, so Comcast must prioritize content and UX to retain subscribers.

Demand for High-Speed Broadband Alternatives

Residential customers now can choose fiber-to-the-home and 5G fixed wireless access from mobile carriers; by end-2024 US fiber coverage reached ~47% of homes and 5G FWA pilots covered >60 metro areas, shrinking Comcast’s geographic monopoly.

This alternative availability forces Comcast to use aggressive promotional pricing—Xfinity reported average revenue per user fell 1.8% in 2024—and to invest in reliability upgrades to keep demanding users.

Enterprise Client Leverage

Enterprise clients—large businesses and government accounts—drive ~25% of Comcast Business revenue and wield strong bargaining power because contracts often exceed $1M annually and span multiple years.

They demand custom SLAs (uptime, latency), dedicated account teams, and volume discounts unavailable to consumers, raising Comcast’s service delivery costs.

Comcast must match competitors on price and tech specs; lost enterprise renewals can cut annual revenue growth by several percentage points.

Pricing Transparency and Comparison Tools

The digital age gives Comcast customers instant price comparisons and reviews; 82% of US broadband shoppers used online tools in 2024 to compare providers, raising churn risk when prices rise.

Armed with competitor promos and aggregator data, subscribers negotiate lower rates or threaten cancellation, constraining Comcast’s ability to push across-the-board price hikes without losing share.

- 82% of broadband shoppers used online comparison tools in 2024

- Comcast lost 349,000 video subscribers in 2024, showing price sensitivity

- Promo-led switching up 14% year-over-year in 2023–24

Advertiser Influence on Media Content

Advertisers in NBCUniversal wield strong leverage, shifting ad dollars to platforms with superior data targeting and ROI; digital ad spend grew 14% to $205B in the US in 2024, raising the stakes for Comcast to match targeting metrics.

If Comcast lacks advanced ad-tech or hit programming, advertisers can move budgets to Meta, Google, or Netflix, pressuring NBCU to innovate its ad platform and audience measurement.

Here’s the quick math: losing 5% of national ad spend (~$10B) would cut NBCU revenue materially, so continuous product upgrades are mandatory.

- Advertisers favor platforms with granular targeting and measurable ROI

- US digital ad market $205B in 2024, up 14%

- Comcast must invest in ad-tech and high-engagement content

- Small share shifts can cost NBCU billions annually

Comcast faces churn, ARPU pressure and ad-tech squeeze as fiber/5G competition rises

Customers hold high bargaining power: streaming churn ~21% in 2024 and Peacock one-click cancellations; US fiber reached ~47% homes and 5G FWA pilots >60 metros by end-2024, forcing promos and ARPU pressure (Xfinity ARPU down 1.8% in 2024). Enterprise clients (≈25% of Comcast Business revenue) demand custom SLAs and volume discounts. Advertisers shifted spend—US digital ad market $205B in 2024—pressuring NBCU ad-tech investment.

| Metric | 2024 |

|---|---|

| Streaming churn | ~21% |

| US fiber coverage | ≈47% homes |

| 5G FWA metros | >60 |

| Xfinity ARPU change | -1.8% |

| Comcast Business rev from enterprise | ≈25% |

| US digital ad market | $205B (+14%) |

Preview Before You Purchase

Comcast Porter's Five Forces Analysis

This preview shows the exact Comcast Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples; the full, professionally formatted document is ready for download and use the moment you buy.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Comcast faces intense rivalry from cable and streaming competitors, moderate supplier leverage from content partners, and rising substitute threats as OTT services expand; buyer power grows with cord-cutting trends while regulatory barriers temper new entrants.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Comcast’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Content Licensing and Sports Rights

The cost of exclusive sports rights pushes supplier power up: Comcast paid about $2.8B annually for NBC Sports regional deals and faces bids where NFL/Amazon deals topped $10B in 2023, forcing higher pay-TV and Peacock licensing spend.

Infrastructure and Network Equipment Vendors

Labor Unions and Specialized Talent

The media and telecom sector is shaped by unions—writers, actors, and engineers—whose strikes in 2023 cost US studios an estimated $1.5–2.0 billion in lost production revenue; that collective leverage raises suppliers’ bargaining power versus Comcast.

Recent SAG-AFTRA and WGA actions secured better residuals and AI protections, pressuring Comcast to raise content spending (NBCUniversal’s 2024 content budget rose ~10% year-over-year) to retain talent.

Specialized engineers for networks and streaming are scarce; median pay for senior broadcast engineers rose ~8% in 2024, so Comcast faces upward labor-cost pressure while needing continuous original output for Peacock and global channels.

Cloud Computing and Third-Party Data Services

As Comcast shifts more of Peacock and Xfinity to cloud platforms, dependence on AWS, Google Cloud, and Microsoft Azure rises, giving those providers leverage over storage, compute, and CDN costs; in 2024 hyperscalers earned over $700B combined, underscoring scale advantage.

Hybrid architectures reduce some risk, but persistent high data egress fees (often $0.05–0.12/GB) and integration lock-in raise long-term supplier bargaining power and operating expense sensitivity.

- Major suppliers: AWS, Google Cloud, Microsoft Azure

- 2024 hyperscaler revenue > $700B combined

- Typical egress: $0.05–0.12 per GB

- Hybrid use lowers but doesn't remove dependence

Energy and Utility Providers

Comcast's vast network and data centers consume large electricity and cooling; in 2024 its total energy spend exceeded $1.1 billion, leaving it exposed to utility price swings and local energy regulations.

Meeting its 2035 carbon‑neutral target raises reliance on renewable suppliers, pushing short‑term procurement costs up—Comcast bought ~280 MW of renewables contracts by 2025 but still offsets residual emissions.

Supplier power is moderate: utilities hold pricing leverage regionally, while large renewables deals give Comcast some bargaining clout but require capital and long-term commitments.

- 2024 energy spend ~$1.1B

- ~280 MW renewables contracted by 2025

- 2035 carbon‑neutral target increases procurement costs

- Regional utility pricing gives suppliers moderate leverage

Moderate supplier power: $2.8B NBC rights, $1.1B energy, capex sensitivity ~$1.6B

Supplier bargaining power is moderate: concentrated content, cloud, hardware, labor, and energy suppliers can drive costs—NBC sports rights (~$2.8B/yr), hyperscaler egress $0.05–0.12/GB, 2024 energy spend ~$1.1B, ~280 MW renewables by 2025—so supply shocks or price hikes (10% capex impact ≈ $1.6B) materially affect Comcast.

| Metric | 2024–25 |

|---|---|

| NBC regional rights | $2.8B/yr |

| Hyperscaler egress | $0.05–0.12/GB |

| Energy spend | $1.1B |

| Renewables procured | ~280 MW |

| Capex guidance | $16B (2025) |

What is included in the product

Tailored Porter’s Five Forces analysis for Comcast, uncovering key competitive drivers, buyer and supplier power, threats from substitutes and new entrants, and strategic barriers protecting incumbent profitability.

Concise Comcast Porter’s Five Forces snapshot—quickly gauge competitive intensity across content, distribution, and tech to inform strategic moves.

Customers Bargaining Power

Low Switching Costs in Streaming

The shift from multi-year cable deals to month-to-month streaming subscriptions has raised customer bargaining power: in 2024 Peacock cancellations were reversible with one click and U.S. streaming churn averaged ~21% annually, so Comcast must prioritize content and UX to retain subscribers.

Demand for High-Speed Broadband Alternatives

Residential customers now can choose fiber-to-the-home and 5G fixed wireless access from mobile carriers; by end-2024 US fiber coverage reached ~47% of homes and 5G FWA pilots covered >60 metro areas, shrinking Comcast’s geographic monopoly.

This alternative availability forces Comcast to use aggressive promotional pricing—Xfinity reported average revenue per user fell 1.8% in 2024—and to invest in reliability upgrades to keep demanding users.

Enterprise Client Leverage

Enterprise clients—large businesses and government accounts—drive ~25% of Comcast Business revenue and wield strong bargaining power because contracts often exceed $1M annually and span multiple years.

They demand custom SLAs (uptime, latency), dedicated account teams, and volume discounts unavailable to consumers, raising Comcast’s service delivery costs.

Comcast must match competitors on price and tech specs; lost enterprise renewals can cut annual revenue growth by several percentage points.

Pricing Transparency and Comparison Tools

The digital age gives Comcast customers instant price comparisons and reviews; 82% of US broadband shoppers used online tools in 2024 to compare providers, raising churn risk when prices rise.

Armed with competitor promos and aggregator data, subscribers negotiate lower rates or threaten cancellation, constraining Comcast’s ability to push across-the-board price hikes without losing share.

- 82% of broadband shoppers used online comparison tools in 2024

- Comcast lost 349,000 video subscribers in 2024, showing price sensitivity

- Promo-led switching up 14% year-over-year in 2023–24

Advertiser Influence on Media Content

Advertisers in NBCUniversal wield strong leverage, shifting ad dollars to platforms with superior data targeting and ROI; digital ad spend grew 14% to $205B in the US in 2024, raising the stakes for Comcast to match targeting metrics.

If Comcast lacks advanced ad-tech or hit programming, advertisers can move budgets to Meta, Google, or Netflix, pressuring NBCU to innovate its ad platform and audience measurement.

Here’s the quick math: losing 5% of national ad spend (~$10B) would cut NBCU revenue materially, so continuous product upgrades are mandatory.

- Advertisers favor platforms with granular targeting and measurable ROI

- US digital ad market $205B in 2024, up 14%

- Comcast must invest in ad-tech and high-engagement content

- Small share shifts can cost NBCU billions annually

Comcast faces churn, ARPU pressure and ad-tech squeeze as fiber/5G competition rises

Customers hold high bargaining power: streaming churn ~21% in 2024 and Peacock one-click cancellations; US fiber reached ~47% homes and 5G FWA pilots >60 metros by end-2024, forcing promos and ARPU pressure (Xfinity ARPU down 1.8% in 2024). Enterprise clients (≈25% of Comcast Business revenue) demand custom SLAs and volume discounts. Advertisers shifted spend—US digital ad market $205B in 2024—pressuring NBCU ad-tech investment.

| Metric | 2024 |

|---|---|

| Streaming churn | ~21% |

| US fiber coverage | ≈47% homes |

| 5G FWA metros | >60 |

| Xfinity ARPU change | -1.8% |

| Comcast Business rev from enterprise | ≈25% |

| US digital ad market | $205B (+14%) |

Preview Before You Purchase

Comcast Porter's Five Forces Analysis

This preview shows the exact Comcast Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples; the full, professionally formatted document is ready for download and use the moment you buy.