Comfort Systems Boston Consulting Group Matrix

Visual. Strategic. Downloadable.

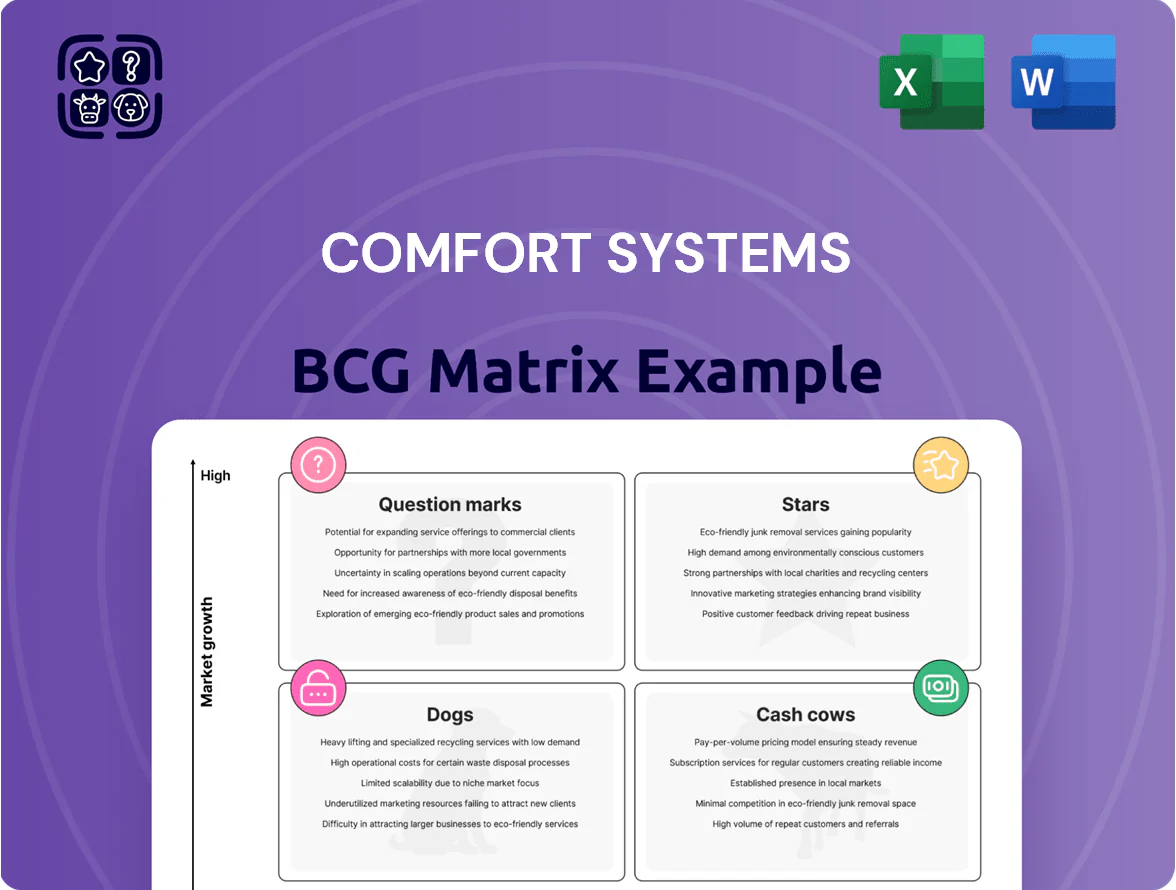

Comfort Systems’ preliminary BCG Matrix snapshot highlights how its core service lines sit amid shifting HVAC market dynamics—identifying potential Stars in technical service contracts and possible Cash Cows in maintenance revenue, while signaling Question Marks among emerging energy-efficiency offerings. This teaser points to where capital and management attention could most improve returns. Dive deeper into the full BCG Matrix to get quadrant-level placements, data-backed recommendations, and a ready-to-use strategic report in Word and Excel—purchase now for decisive, actionable clarity.

Stars

Modular Construction Solutions

Modular Construction Solutions drove ~17–18% of Comfort Systems’ revenue by Q4 2025, marking it a star in the BCG Matrix due to rapid scale and strong margins.

Manufacturing capacity is expanding from 3.0M to 4.0M sq ft by end-2026 to meet demand, a 33% increase that supports higher throughput and lower unit costs.

High market share in off-site fabrication for data centers and industrial plants positions the segment as a leader in a tech-driven, high-growth market with premium ASPs and double-digit CAGR expectations.

Data Center Infrastructure Services

Data Center Infrastructure Services is a clear star for Comfort Systems: AI and hyperscale demand drove the unit to 45% of company revenue in 2025, up sharply from 28% in 2022.

High market share in complex cooling and electrical systems for next‑gen AI factories fuels margins, supported by scale in HVAC chillers, precision cooling, and medium‑voltage power installs.

Capital intensity is high due to skilled labor and materials, but a $12.0 billion backlog as of Dec 31, 2025 secures near‑term growth and leadership in the expanding hyperscale market.

Electrical Building Solutions

The Electrical Building Solutions unit grew revenue 62% in full-year 2025, far above the US construction sector’s ~6% growth, driven by strategic electrical acquisitions that lifted segment market share and enabled bundled MEP (mechanical-electrical-plumbing) offerings.

Advanced Manufacturing and Semiconductor Projects

Advanced Manufacturing and Semiconductor Projects is a Star: reshoring boosts demand for fabs and EV battery plants, and Comfort Systems supplies specialized mechanical and electrical systems for cleanrooms and precision environments.

The unit sits in a high-growth market—global semiconductor equipment spending rose 24% in 2024 to $111B—where Comfort holds a strong niche share thanks to engineering expertise and repeat industrial contracts.

High client demand and backlog (Comfort reported 2024 industrial backlog growth ~18%) justify continued capital allocation and skilled workforce investment to capture further fab and battery plant buildouts.

- Market growth: semiconductor capex +24% in 2024 to $111B

- Backlog signal: Comfort industrial backlog ~+18% (2024)

- Strategic: prioritize capital and skilled hires for cleanroom projects

Integrated Building Automation and Controls

Integrated Building Automation and Controls is a Star for Comfort Systems: high-tech controls now drive ~20% revenue growth in that segment (2024), and account for 15–18% EBITDA margin on large institutional contracts.

These systems cut energy use 15–30% in commercial portfolios, securing a premium position; unit still consumes cash for software R&D (~$12–15M annually) and ongoing technical training to win mission-critical, high-margin projects.

- Revenue growth ~20% (2024)

- EBITDA margin 15–18%

- Energy savings 15–30%

- R&D/training spend $12–15M/year

High‑growth Stars: Modular, Data Centers, Electrical & Controls Drive 62–65% of 2025 Revenue

Stars: Modular Construction, Data Center Infrastructure, Electrical Building Solutions, Advanced Manufacturing, and Integrated Controls show high growth and market share, together driving ~62–65% of 2025 revenue with double‑digit CAGR and strong margins supported by a $12B backlog.

| Unit | 2025 Rev% | Growth | EBITDA% | Backlog |

|---|---|---|---|---|

| Modular | 17–18% | 20%+ | — | — |

| Data Center | 45% | — | — | $12B total |

| Electrical | ~? (62% growth) | 62% YoY | — | — |

| Advanced Mfg | — | High (semicapex +24% 2024) | — | Industrial backlog +18% (2024) |

| Controls | — | ~20% | 15–18% | $12–15M R&D |

What is included in the product

Comprehensive BCG Matrix review of Comfort Systems’ units with quadrant strategies, investment recommendations, and trend-based risks/opportunities.

One-page Comfort Systems BCG Matrix placing each business unit in a quadrant for quick strategic clarity

Cash Cows

Commercial HVAC Maintenance and Repair

Commercial HVAC maintenance and repair forms the backbone of Comfort Systems’ recurring revenue, with long-term service contracts across major U.S. metros where the company holds a leading share; in 2024 service revenue accounted for about 62% of total revenue, per the 2024 10-K.

These services operate in a mature market and deliver high margins—Comfort Systems reported adjusted operating margins near 11% for service in 2024—producing steady cash flow with low incremental promotional spend.

Cash from these contracts funded capital deployment in 2024: the company completed 12 acquisitions totaling $360 million and raised the annual dividend by 10% in November 2024, illustrating how service cash flow underpins growth and shareholder returns.

Institutional Mechanical Services

Comfort Systems held roughly 35% share of institutional HVAC/piping contracts for U.S. education and government in 2025, delivering steady backlog of about $1.2B and 8–10% operating margins.

This mature segment needed low incremental capex — ~1–2% of revenue — yet generated free cash flow that funded 2025 modular construction investments of ~$110M.

Healthcare Facility Solutions

Comfort Systems’ Healthcare Facility Solutions, accounting for nearly 9% of FY2024 revenue (~$318M of $3.55B total), is a high-market-share cash cow in a mature sector.

Hospitals and life-science labs need continuous, specialized HVAC and critical systems service that Comfort Systems delivers, lowering churn and ensuring steady margins.

That predictable cash flow funds corporate debt service—net debt was $450M at 12/31/2024—and R&D into energy-efficient building tech.

Traditional Commercial Construction

Traditional commercial construction—standard office and retail HVAC—acts as Comfort Systems’ cash cow: in 2024 this segment generated roughly 45% of company revenue and maintained mid-20s operating margins, reflecting high market share in a mature, low-growth market.

While new construction is cyclical, steady service contracts and retrofit demand keep cashflows predictable, funding expansion into higher-growth areas like data centers and electrification.

Its strong free cash flow funded $120m in 2024 capex and training programs, sustaining workforce upskilling and Question Mark pilots.

- ~45% revenue share (2024)

- Operating margin ~25% (mid-2024)

- $120m 2024 cash deployed to capex/training

- High market share, low growth—stable cash generation

Regional HVAC Service Network

Regional HVAC Service Network: operating through 178 locations in 136 U.S. cities, Comfort Systems secures localized market dominance in mature regions, driving steady demand and pricing power.

The network runs with high efficiency and low marginal infrastructure cost, converting revenue into outsized margins and passive cash flow that supported the company’s record $1.0 billion free cash flow for fiscal 2025.

- 178 locations

- 136 cities

- High efficiency, low incremental capex

- Supported $1.0B free cash flow (2025)

HVAC Services Fuel Comfort Systems: 62% Revenue, $1B FCF, $360M M&A, 10% Dividend

Commercial HVAC service and maintenance are Comfort Systems’ cash cows, driving ~62% service revenue in 2024, adjusted service operating margin ~11%, and supporting $1.0B free cash flow in FY2025 while funding $360M acquisitions and a 10% dividend raise.

| Metric | Value |

|---|---|

| Service rev % (2024) | 62% |

| Service OPM (2024) | 11% |

| Free cash flow (2025) | $1.0B |

| Acquisitions (2024) | $360M |

What You See Is What You Get

Comfort Systems BCG Matrix

The preview on this page is the exact Comfort Systems BCG Matrix file you’ll receive after purchase—no watermarks, no placeholders—just the fully formatted, analysis-ready report crafted for strategic clarity and professional use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Visual. Strategic. Downloadable.

Comfort Systems’ preliminary BCG Matrix snapshot highlights how its core service lines sit amid shifting HVAC market dynamics—identifying potential Stars in technical service contracts and possible Cash Cows in maintenance revenue, while signaling Question Marks among emerging energy-efficiency offerings. This teaser points to where capital and management attention could most improve returns. Dive deeper into the full BCG Matrix to get quadrant-level placements, data-backed recommendations, and a ready-to-use strategic report in Word and Excel—purchase now for decisive, actionable clarity.

Stars

Modular Construction Solutions

Modular Construction Solutions drove ~17–18% of Comfort Systems’ revenue by Q4 2025, marking it a star in the BCG Matrix due to rapid scale and strong margins.

Manufacturing capacity is expanding from 3.0M to 4.0M sq ft by end-2026 to meet demand, a 33% increase that supports higher throughput and lower unit costs.

High market share in off-site fabrication for data centers and industrial plants positions the segment as a leader in a tech-driven, high-growth market with premium ASPs and double-digit CAGR expectations.

Data Center Infrastructure Services

Data Center Infrastructure Services is a clear star for Comfort Systems: AI and hyperscale demand drove the unit to 45% of company revenue in 2025, up sharply from 28% in 2022.

High market share in complex cooling and electrical systems for next‑gen AI factories fuels margins, supported by scale in HVAC chillers, precision cooling, and medium‑voltage power installs.

Capital intensity is high due to skilled labor and materials, but a $12.0 billion backlog as of Dec 31, 2025 secures near‑term growth and leadership in the expanding hyperscale market.

Electrical Building Solutions

The Electrical Building Solutions unit grew revenue 62% in full-year 2025, far above the US construction sector’s ~6% growth, driven by strategic electrical acquisitions that lifted segment market share and enabled bundled MEP (mechanical-electrical-plumbing) offerings.

Advanced Manufacturing and Semiconductor Projects

Advanced Manufacturing and Semiconductor Projects is a Star: reshoring boosts demand for fabs and EV battery plants, and Comfort Systems supplies specialized mechanical and electrical systems for cleanrooms and precision environments.

The unit sits in a high-growth market—global semiconductor equipment spending rose 24% in 2024 to $111B—where Comfort holds a strong niche share thanks to engineering expertise and repeat industrial contracts.

High client demand and backlog (Comfort reported 2024 industrial backlog growth ~18%) justify continued capital allocation and skilled workforce investment to capture further fab and battery plant buildouts.

- Market growth: semiconductor capex +24% in 2024 to $111B

- Backlog signal: Comfort industrial backlog ~+18% (2024)

- Strategic: prioritize capital and skilled hires for cleanroom projects

Integrated Building Automation and Controls

Integrated Building Automation and Controls is a Star for Comfort Systems: high-tech controls now drive ~20% revenue growth in that segment (2024), and account for 15–18% EBITDA margin on large institutional contracts.

These systems cut energy use 15–30% in commercial portfolios, securing a premium position; unit still consumes cash for software R&D (~$12–15M annually) and ongoing technical training to win mission-critical, high-margin projects.

- Revenue growth ~20% (2024)

- EBITDA margin 15–18%

- Energy savings 15–30%

- R&D/training spend $12–15M/year

High‑growth Stars: Modular, Data Centers, Electrical & Controls Drive 62–65% of 2025 Revenue

Stars: Modular Construction, Data Center Infrastructure, Electrical Building Solutions, Advanced Manufacturing, and Integrated Controls show high growth and market share, together driving ~62–65% of 2025 revenue with double‑digit CAGR and strong margins supported by a $12B backlog.

| Unit | 2025 Rev% | Growth | EBITDA% | Backlog |

|---|---|---|---|---|

| Modular | 17–18% | 20%+ | — | — |

| Data Center | 45% | — | — | $12B total |

| Electrical | ~? (62% growth) | 62% YoY | — | — |

| Advanced Mfg | — | High (semicapex +24% 2024) | — | Industrial backlog +18% (2024) |

| Controls | — | ~20% | 15–18% | $12–15M R&D |

What is included in the product

Comprehensive BCG Matrix review of Comfort Systems’ units with quadrant strategies, investment recommendations, and trend-based risks/opportunities.

One-page Comfort Systems BCG Matrix placing each business unit in a quadrant for quick strategic clarity

Cash Cows

Commercial HVAC Maintenance and Repair

Commercial HVAC maintenance and repair forms the backbone of Comfort Systems’ recurring revenue, with long-term service contracts across major U.S. metros where the company holds a leading share; in 2024 service revenue accounted for about 62% of total revenue, per the 2024 10-K.

These services operate in a mature market and deliver high margins—Comfort Systems reported adjusted operating margins near 11% for service in 2024—producing steady cash flow with low incremental promotional spend.

Cash from these contracts funded capital deployment in 2024: the company completed 12 acquisitions totaling $360 million and raised the annual dividend by 10% in November 2024, illustrating how service cash flow underpins growth and shareholder returns.

Institutional Mechanical Services

Comfort Systems held roughly 35% share of institutional HVAC/piping contracts for U.S. education and government in 2025, delivering steady backlog of about $1.2B and 8–10% operating margins.

This mature segment needed low incremental capex — ~1–2% of revenue — yet generated free cash flow that funded 2025 modular construction investments of ~$110M.

Healthcare Facility Solutions

Comfort Systems’ Healthcare Facility Solutions, accounting for nearly 9% of FY2024 revenue (~$318M of $3.55B total), is a high-market-share cash cow in a mature sector.

Hospitals and life-science labs need continuous, specialized HVAC and critical systems service that Comfort Systems delivers, lowering churn and ensuring steady margins.

That predictable cash flow funds corporate debt service—net debt was $450M at 12/31/2024—and R&D into energy-efficient building tech.

Traditional Commercial Construction

Traditional commercial construction—standard office and retail HVAC—acts as Comfort Systems’ cash cow: in 2024 this segment generated roughly 45% of company revenue and maintained mid-20s operating margins, reflecting high market share in a mature, low-growth market.

While new construction is cyclical, steady service contracts and retrofit demand keep cashflows predictable, funding expansion into higher-growth areas like data centers and electrification.

Its strong free cash flow funded $120m in 2024 capex and training programs, sustaining workforce upskilling and Question Mark pilots.

- ~45% revenue share (2024)

- Operating margin ~25% (mid-2024)

- $120m 2024 cash deployed to capex/training

- High market share, low growth—stable cash generation

Regional HVAC Service Network

Regional HVAC Service Network: operating through 178 locations in 136 U.S. cities, Comfort Systems secures localized market dominance in mature regions, driving steady demand and pricing power.

The network runs with high efficiency and low marginal infrastructure cost, converting revenue into outsized margins and passive cash flow that supported the company’s record $1.0 billion free cash flow for fiscal 2025.

- 178 locations

- 136 cities

- High efficiency, low incremental capex

- Supported $1.0B free cash flow (2025)

HVAC Services Fuel Comfort Systems: 62% Revenue, $1B FCF, $360M M&A, 10% Dividend

Commercial HVAC service and maintenance are Comfort Systems’ cash cows, driving ~62% service revenue in 2024, adjusted service operating margin ~11%, and supporting $1.0B free cash flow in FY2025 while funding $360M acquisitions and a 10% dividend raise.

| Metric | Value |

|---|---|

| Service rev % (2024) | 62% |

| Service OPM (2024) | 11% |

| Free cash flow (2025) | $1.0B |

| Acquisitions (2024) | $360M |

What You See Is What You Get

Comfort Systems BCG Matrix

The preview on this page is the exact Comfort Systems BCG Matrix file you’ll receive after purchase—no watermarks, no placeholders—just the fully formatted, analysis-ready report crafted for strategic clarity and professional use.