Comfort Systems SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Comfort Systems shows resilient revenue streams from commercial HVAC services and a scalable regional footprint, but faces margin pressure from material costs and labor shortages while pursuing growth via acquisitions and tech-enabled maintenance—discover how these dynamics shape strategic risk and opportunity. Purchase the full SWOT analysis for a professionally formatted Word report and editable Excel matrix to plan, pitch, or invest with confidence.

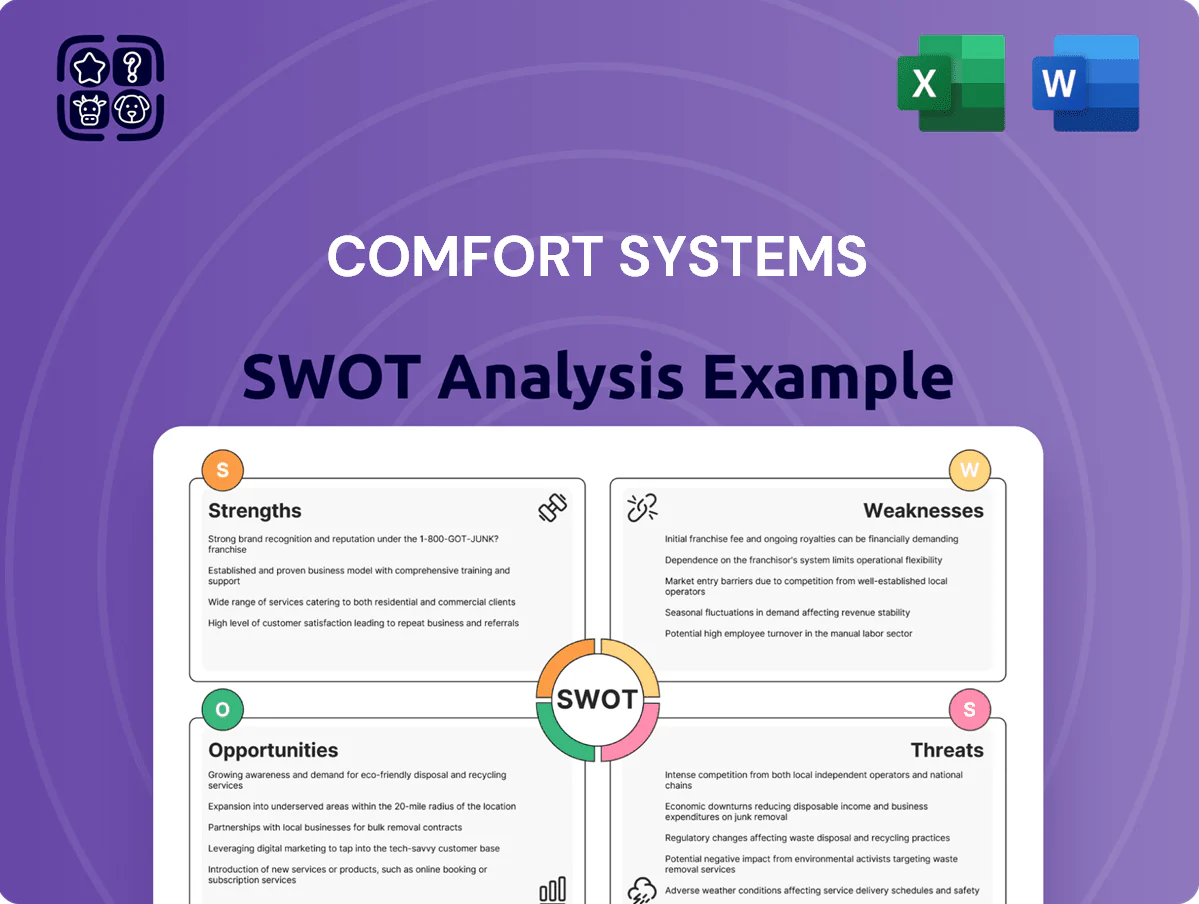

Strengths

Dominant Market Position

Comfort Systems USA operates over 190 regional companies and reported $6.1 billion in revenue for fiscal 2024, backing its position as a premier US mechanical and electrical services provider.

Its decentralized network keeps local crews close to clients while corporate scale delivers shared procurement and technology, cutting costs and raising margins—2024 adjusted EBITDA margin was about 9.8%.

Strong brand recognition in commercial and industrial sectors supports repeat revenues and a backlog near $2.3 billion at end-2024, reducing near-term demand risk.

Modular Construction Leadership

Comfort Systems’ multi-year investment in off-site modular construction cut on-site labor by ~30% and reduced project durations by 20% on average in 2024, driving a gross margin premium of ~250 basis points versus traditional builds.

Strong Financial Health

As of Q3 2025 Comfort Systems USA reports trailing‑12‑month operating cash flow of $450M and net debt/EBITDA of 1.1x, giving a strong balance sheet that funds growth and M&A; free cash flow supported $120M in buybacks and $45M in dividends in 2024–25. This liquidity and disciplined capital allocation lets management reinvest in organic expansion while returning capital to shareholders.

Diverse End-Market Exposure

Comfort Systems serves healthcare, education, data centers, and industrial manufacturing, giving it broad end-market exposure that reduced revenue volatility in 2024—backlog from institutional clients rose ~18% year-over-year to $1.6 billion as of Q4 2024.

That diversification cushions downturns in any single sector; peers concentrated in office space saw 2024 revenue declines of 6–9%, while Comfort Systems reported consolidated revenue growth of 7.5% in 2024.

Focusing on essential infrastructure and institutional clients supports steadier margins and recurring service demand compared with office-centric competitors.

- 2024 backlog: $1.6B

- 2024 revenue growth: +7.5%

- Peers office revenue change: -6% to -9% in 2024

Decentralized Operational Model

Comfort Systems uses a decentralized model that lets 1,000+ local management teams make market-specific decisions, driving faster responses and an entrepreneurial culture; this helped deliver record 2024 revenue of $6.7B and 11% organic growth in 2024.

Corporate provides back-office services, shared systems, and best practices—keeping SG&A efficient (adjusted operating margin ~9.5% in FY2024) while preserving local agility.

- Tailored local decisions — 1,000+ teams

- Fast response — 11% organic growth 2024

- Corporate support — $6.7B revenue 2024

- Efficient margins — ~9.5% adj. operating margin 2024

Comfort Systems: $6.7B 2024, 11% organic growth, $1.6B backlog, strong margins & cash

Comfort Systems’ scale and decentralized 1,000+ local teams drove record 2024 revenue ~$6.7B and 11% organic growth, with 2024 backlog ~$1.6B and adjusted operating margin ~9.5%, supported by modular construction (250 bp gross margin premium) and strong cash (trailing‑12M OCF $450M, net debt/EBITDA 1.1x).

| Metric | Value |

|---|---|

| 2024 Revenue | $6.7B |

| Organic Growth 2024 | 11% |

| Backlog (end‑2024) | $1.6B |

| Adj. Op Margin 2024 | ~9.5% |

| OCF (TTM) | $450M |

| Net Debt/EBITDA | 1.1x |

What is included in the product

Provides a concise SWOT overview of Comfort Systems, highlighting internal capabilities, operational gaps, market opportunities, and external risks shaping the company’s strategic position.

Delivers a concise Comfort Systems SWOT matrix for rapid strategic alignment, ideal for executives and teams needing a clear, editable snapshot to streamline planning and stakeholder presentations.

Weaknesses

Skilled Labor Dependency

The firm relies on specialized HVAC techs, electricians, and engineers, and a national skilled trades shortfall—Bureau of Labor Statistics projects 8% HVAC tech growth 2024–34 but training gaps persist—hurts recruiting and retention, raising labor costs ( Comfort Systems’ 2024 SG&A rose 6.2% YoY) and risking project delays when staffing lags peak demand.

Acquisition Integration Complexity

Comfort Systems USA leans on M&A for growth—68 acquisitions from 2016–2024 and 2024 revenue of $4.7B—raising integration complexity across cultures, accounting platforms, and workflows.

Disparate ERP and billing systems increase operational risk; post-acquisition integration overruns can cut expected synergies by 20–30% and raise SG&A temporarily.

Failed harmonization risks long-term inefficiencies and diluted brand equity, shown by regional churn spikes after past rollups and uneven gross margins by division.

Geographic Concentration

Comfort Systems USA (CSS, market cap ~$2.6B as of Dec 31, 2025) operates solely in the United States, exposing revenue (FY2024 rev $3.7B) to U.S. economic cycles and policy shifts—e.g., a 1% GDP contraction could cut demand for commercial HVAC by ~2–3% historically.

Cyclical Revenue Streams

A significant share of Comfort Systems USA Inc.'s (FIX: FIX?) revenue comes from new construction, exposing the firm to construction cycle swings; new-build work accounted for about 42% of 2024 revenue, per company filings. During economic slowdowns or when the Fed raised rates to ~5.25% in 2024, starts and permits fell, reducing demand for HVAC and plumbing installs and pressuring margins and backlog. This cyclical exposure drove revenue volatility—FY2023–FY2024 organic revenue growth swung from +8% to -3%—and increased backlog sensitivity to funding costs. Here’s the quick math: a 10% drop in construction starts can translate to a similar decline in new-construction revenue within 6–18 months.

- ~42% revenue from new construction (2024)

- Fed funds ~5.25% in 2024 raised financing costs

- Organic growth swing +8% to -3% (2023–2024)

- 10% drop in starts → ~10% revenue hit in 6–18 months

Margin Sensitivity

Skilled-labor squeeze, M&A headaches and rate sensitivity threaten margins and growth

Heavy reliance on scarce skilled trades raises labor costs and delay risk (SG&A +6.2% YoY 2024); M&A-driven growth (68 deals 2016–24) creates integration complexity and ERP fragmentation that can cut expected synergies 20–30%; 42% of 2024 revenue from new construction and sensitivity to Fed rates (~5.25% 2024) causes revenue volatility (organic growth +8% to -3% 2023–24); raw materials ~18–25% COGS, 10% price rise → ~2–3ppt margin hit.

| Metric | Value |

|---|---|

| SG&A change 2024 | +6.2% |

| Acquisitions 2016–24 | 68 |

| 2024 revenue from new construction | 42% |

| Fed funds 2024 | ~5.25% |

| Raw materials of COGS | 18–25% |

| Margin impact from 10% raw spike | ~2–3 ppt |

What You See Is What You Get

Comfort Systems SWOT Analysis

This preview is taken directly from the full Comfort Systems SWOT analysis document you'll receive upon purchase—no surprises, just professional quality and structured insights.

The content shown here is the real excerpt from the complete report; buying unlocks the entire, editable version with detailed strengths, weaknesses, opportunities, and threats.

Purchase grants immediate access to the full, ready-to-use SWOT file for strategic planning and decision-making.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Dive Deeper Into the Company’s Strategic Blueprint

Comfort Systems shows resilient revenue streams from commercial HVAC services and a scalable regional footprint, but faces margin pressure from material costs and labor shortages while pursuing growth via acquisitions and tech-enabled maintenance—discover how these dynamics shape strategic risk and opportunity. Purchase the full SWOT analysis for a professionally formatted Word report and editable Excel matrix to plan, pitch, or invest with confidence.

Strengths

Dominant Market Position

Comfort Systems USA operates over 190 regional companies and reported $6.1 billion in revenue for fiscal 2024, backing its position as a premier US mechanical and electrical services provider.

Its decentralized network keeps local crews close to clients while corporate scale delivers shared procurement and technology, cutting costs and raising margins—2024 adjusted EBITDA margin was about 9.8%.

Strong brand recognition in commercial and industrial sectors supports repeat revenues and a backlog near $2.3 billion at end-2024, reducing near-term demand risk.

Modular Construction Leadership

Comfort Systems’ multi-year investment in off-site modular construction cut on-site labor by ~30% and reduced project durations by 20% on average in 2024, driving a gross margin premium of ~250 basis points versus traditional builds.

Strong Financial Health

As of Q3 2025 Comfort Systems USA reports trailing‑12‑month operating cash flow of $450M and net debt/EBITDA of 1.1x, giving a strong balance sheet that funds growth and M&A; free cash flow supported $120M in buybacks and $45M in dividends in 2024–25. This liquidity and disciplined capital allocation lets management reinvest in organic expansion while returning capital to shareholders.

Diverse End-Market Exposure

Comfort Systems serves healthcare, education, data centers, and industrial manufacturing, giving it broad end-market exposure that reduced revenue volatility in 2024—backlog from institutional clients rose ~18% year-over-year to $1.6 billion as of Q4 2024.

That diversification cushions downturns in any single sector; peers concentrated in office space saw 2024 revenue declines of 6–9%, while Comfort Systems reported consolidated revenue growth of 7.5% in 2024.

Focusing on essential infrastructure and institutional clients supports steadier margins and recurring service demand compared with office-centric competitors.

- 2024 backlog: $1.6B

- 2024 revenue growth: +7.5%

- Peers office revenue change: -6% to -9% in 2024

Decentralized Operational Model

Comfort Systems uses a decentralized model that lets 1,000+ local management teams make market-specific decisions, driving faster responses and an entrepreneurial culture; this helped deliver record 2024 revenue of $6.7B and 11% organic growth in 2024.

Corporate provides back-office services, shared systems, and best practices—keeping SG&A efficient (adjusted operating margin ~9.5% in FY2024) while preserving local agility.

- Tailored local decisions — 1,000+ teams

- Fast response — 11% organic growth 2024

- Corporate support — $6.7B revenue 2024

- Efficient margins — ~9.5% adj. operating margin 2024

Comfort Systems: $6.7B 2024, 11% organic growth, $1.6B backlog, strong margins & cash

Comfort Systems’ scale and decentralized 1,000+ local teams drove record 2024 revenue ~$6.7B and 11% organic growth, with 2024 backlog ~$1.6B and adjusted operating margin ~9.5%, supported by modular construction (250 bp gross margin premium) and strong cash (trailing‑12M OCF $450M, net debt/EBITDA 1.1x).

| Metric | Value |

|---|---|

| 2024 Revenue | $6.7B |

| Organic Growth 2024 | 11% |

| Backlog (end‑2024) | $1.6B |

| Adj. Op Margin 2024 | ~9.5% |

| OCF (TTM) | $450M |

| Net Debt/EBITDA | 1.1x |

What is included in the product

Provides a concise SWOT overview of Comfort Systems, highlighting internal capabilities, operational gaps, market opportunities, and external risks shaping the company’s strategic position.

Delivers a concise Comfort Systems SWOT matrix for rapid strategic alignment, ideal for executives and teams needing a clear, editable snapshot to streamline planning and stakeholder presentations.

Weaknesses

Skilled Labor Dependency

The firm relies on specialized HVAC techs, electricians, and engineers, and a national skilled trades shortfall—Bureau of Labor Statistics projects 8% HVAC tech growth 2024–34 but training gaps persist—hurts recruiting and retention, raising labor costs ( Comfort Systems’ 2024 SG&A rose 6.2% YoY) and risking project delays when staffing lags peak demand.

Acquisition Integration Complexity

Comfort Systems USA leans on M&A for growth—68 acquisitions from 2016–2024 and 2024 revenue of $4.7B—raising integration complexity across cultures, accounting platforms, and workflows.

Disparate ERP and billing systems increase operational risk; post-acquisition integration overruns can cut expected synergies by 20–30% and raise SG&A temporarily.

Failed harmonization risks long-term inefficiencies and diluted brand equity, shown by regional churn spikes after past rollups and uneven gross margins by division.

Geographic Concentration

Comfort Systems USA (CSS, market cap ~$2.6B as of Dec 31, 2025) operates solely in the United States, exposing revenue (FY2024 rev $3.7B) to U.S. economic cycles and policy shifts—e.g., a 1% GDP contraction could cut demand for commercial HVAC by ~2–3% historically.

Cyclical Revenue Streams

A significant share of Comfort Systems USA Inc.'s (FIX: FIX?) revenue comes from new construction, exposing the firm to construction cycle swings; new-build work accounted for about 42% of 2024 revenue, per company filings. During economic slowdowns or when the Fed raised rates to ~5.25% in 2024, starts and permits fell, reducing demand for HVAC and plumbing installs and pressuring margins and backlog. This cyclical exposure drove revenue volatility—FY2023–FY2024 organic revenue growth swung from +8% to -3%—and increased backlog sensitivity to funding costs. Here’s the quick math: a 10% drop in construction starts can translate to a similar decline in new-construction revenue within 6–18 months.

- ~42% revenue from new construction (2024)

- Fed funds ~5.25% in 2024 raised financing costs

- Organic growth swing +8% to -3% (2023–2024)

- 10% drop in starts → ~10% revenue hit in 6–18 months

Margin Sensitivity

Skilled-labor squeeze, M&A headaches and rate sensitivity threaten margins and growth

Heavy reliance on scarce skilled trades raises labor costs and delay risk (SG&A +6.2% YoY 2024); M&A-driven growth (68 deals 2016–24) creates integration complexity and ERP fragmentation that can cut expected synergies 20–30%; 42% of 2024 revenue from new construction and sensitivity to Fed rates (~5.25% 2024) causes revenue volatility (organic growth +8% to -3% 2023–24); raw materials ~18–25% COGS, 10% price rise → ~2–3ppt margin hit.

| Metric | Value |

|---|---|

| SG&A change 2024 | +6.2% |

| Acquisitions 2016–24 | 68 |

| 2024 revenue from new construction | 42% |

| Fed funds 2024 | ~5.25% |

| Raw materials of COGS | 18–25% |

| Margin impact from 10% raw spike | ~2–3 ppt |

What You See Is What You Get

Comfort Systems SWOT Analysis

This preview is taken directly from the full Comfort Systems SWOT analysis document you'll receive upon purchase—no surprises, just professional quality and structured insights.

The content shown here is the real excerpt from the complete report; buying unlocks the entire, editable version with detailed strengths, weaknesses, opportunities, and threats.

Purchase grants immediate access to the full, ready-to-use SWOT file for strategic planning and decision-making.