Compagnie de l'Odet Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

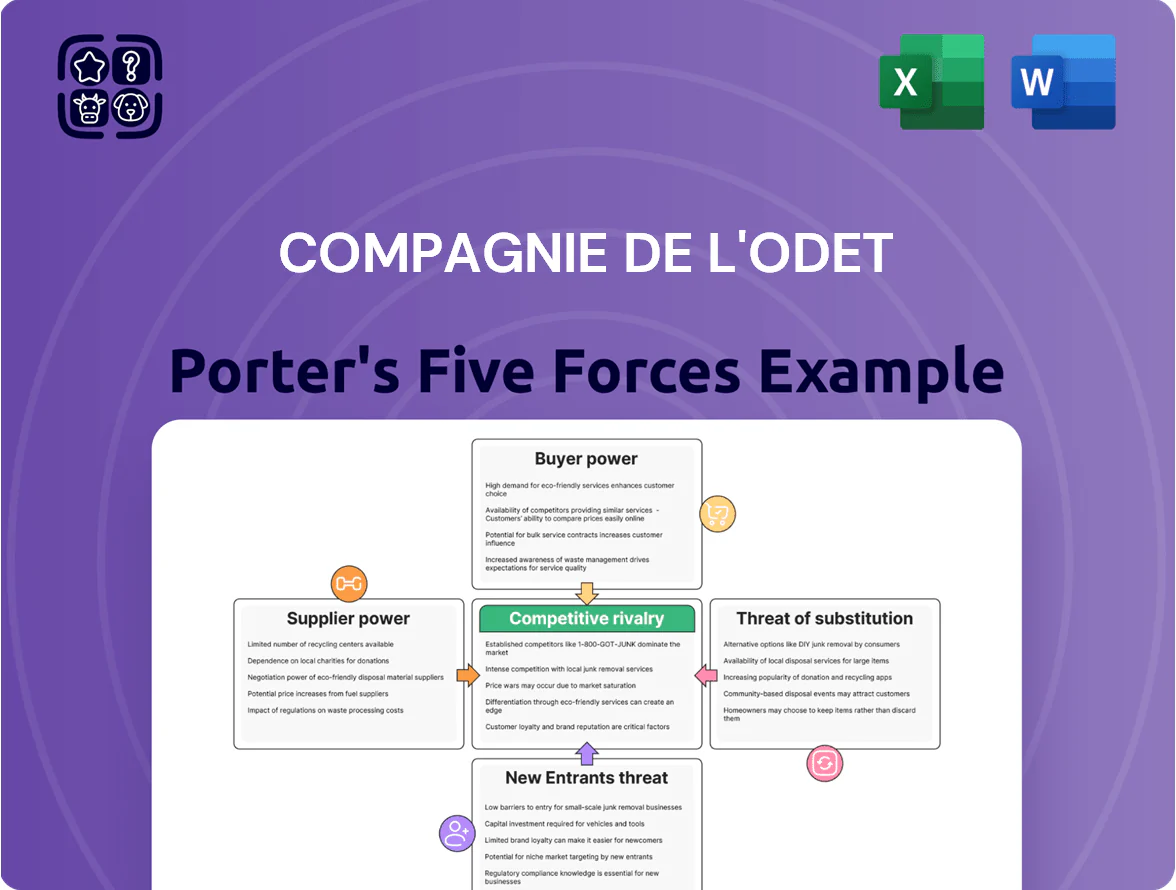

Compagnie de l'Odet faces moderate supplier power and niche customer segments, while barriers to entry and substitute threats shape a competitive but navigable landscape.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Compagnie de l'Odet’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Content Licensing and Sports Rights

Canal+, the media arm of Compagnie de l'Odet, relies heavily on external suppliers for premium films and sports rights; in 2024 Canal+ paid roughly €1.2bn for sports rights, up 8% year-on-year, showing supplier leverage.

Major leagues (UEFA, Ligue 1) and studios command essential content that drives subscriptions, letting suppliers push prices and contract terms that reduce EBITDA margins—Canal+ reported media EBITDA margin fell to ~11% in 2024.

Energy Commodity Volatility

Bolloré Energy is a price taker in global oil markets, buying crude and refined products from major producers and refiners and passing market moves to customers; Brent averaged 86.3 USD/bbl in 2025 Q1, so input costs drive margins.

Dependence on large suppliers leaves Bolloré exposed to geopolitics and supply shocks—Russian supply cuts in 2022 and 2024 Libya unrest pushed regional wholesale spreads up 6–12%.

The firm has limited ability to influence base prices, so hedging and logistics control are key; Bolloré reported fuel trading exposure of EUR 1.2bn on its balance sheet in 2024.

Raw Materials for Battery Production

Suppliers of lithium and specialized polymers wield strong bargaining power for Compagnie de l'Odet’s Blue division because solid-state battery inputs are narrow and global EV demand lifted lithium prices ~85% from 2020–2022 and kept spodumene FOB at ~US$600–900/ton in 2024; a single-quarter supply disruption can delay production and raise COGS by several percentage points for the electricity storage segment.

Human Capital in Advertising and Media

Havas and its media units depend on senior creative and tech staff whose switching costs are low; top talent in advertising commands premium pay—global agency salary surveys in 2024 show 12–25% higher wages for senior creatives, and Havas reported 2024 personnel costs rising 9% to €1.3bn, so the group must spend more on retention and bonuses to avoid poaching by rivals.

- Top talent wage premium: 12–25% (2024 surveys)

- Havas personnel costs 2024: €1.3bn (+9%)

- High turnover raises client risk and hiring costs

Technology and Infrastructure Providers

The group depends on a few dominant cloud and telecom providers—AWS, Microsoft Azure, Google Cloud and major carriers—who control standardized pricing and SLAs; global cloud IaaS spending rose 21% in 2024 to about $229bn, keeping bargaining power with suppliers.

These vendors set non-negotiable contract terms and volume discounts that favor large platform customers, making it hard for Compagnie de l'Odet to lower costs or alter service terms.

Reliance on those platforms creates a material operational risk: outages, price increases or data-policy changes could disrupt the group's communication and logistics services and hit revenue and margins.

- Major suppliers: AWS, Azure, Google Cloud, top telcos

- Global cloud spend 2024: ~$229bn (+21%)

- Standardized terms limit negotiation

- High outage/price-change operational risk

Supplier power squeezes margins: sports, fuel, cloud and talent drive costs up

Suppliers across Canal+ (sports/studios), Bolloré Energy (crude/refined), Blue (lithium/polymers), Havas (talent) and cloud carriers hold strong leverage, driving costs and squeezing margins; Canal+ paid ~€1.2bn for sports rights in 2024 and media EBITDA fell to ~11%. Brent averaged $86.3/bbl in 2025 Q1; Bolloré disclosed €1.2bn fuel trading exposure in 2024. Cloud IaaS spend hit ~$229bn (+21%) in 2024, and Havas personnel costs rose to €1.3bn (+9%).

| Supplier | Key 2024–25 metric |

|---|---|

| Canal+ sports rights | €1.2bn (2024) |

| Media EBITDA | ~11% (2024) |

| Brent | $86.3/bbl (2025 Q1) |

| Fuel exposure | €1.2bn (2024) |

| Lithium/spodumene | $600–900/t FOB (2024) |

| Havas personnel costs | €1.3bn (+9%, 2024) |

| Cloud IaaS | $229bn (+21%, 2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Compagnie de l'Odet that uncovers key competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and highlights disruptive forces and strategic protections for profitability.

A concise, one-sheet Porter's Five Forces summary for Compagnie de l'Odet—ideal for swift strategic decisions and boardroom slides.

Customers Bargaining Power

Subscription Choice and Churn

Individual consumers of Canal+ face many alternatives—from free-to-air channels to Netflix, Amazon Prime Video, and Disney+—so churn risk is high; France’s SVOD penetration hit 66% in 2024, raising switching pressure.

Subscribers can cancel quickly if price rises or content lags; Canal+ lost about 200,000 subscribers in 2023 after price adjustments, showing sensitivity to value perception.

To retain customers, Canal+ must invest in exclusive local and sport rights and originals—content spend was €1.6bn in 2024—to sustain loyalty and reduce churn.

Corporate Client Sensitivity

Havas serves multinational clients whose marketing budgets often exceed €100m, giving them strong bargaining power through formal RFPs and price pressure; in 2024, global ad buying by top 200 advertisers grew 6.2% so competition for those accounts intensified. Clients demand transparent KPIs and ROI reporting, citing benchmarks like CPM and ROAS, and can switch to rival networks with low vendor lock-in, raising churn risk and compressing margins.

Energy Market Price Transparency

Customers in energy distribution—residential and commercial—are highly price-sensitive; in France 2024 retail oil buyers switched suppliers 12% more year-over-year as price transparency rose, per CRE data.

Online comparison tools list fuel and heating-oil prices from 200+ suppliers in regions, so brand loyalty is often secondary to cost; 63% of households say price drives choice (IFOP, 2023).

This forces Compagnie de l'Odet to sustain lean operations: a 5–8% margin cushion is typical in 2024 wholesale-retail spreads, so efficiency directly enables competitive pricing in a transparent market.

B2B Logistics and Storage Demands

Large industrial and commercial clients using Compagnie de l'Odet's logistics and storage services demand high efficiency and tailored solutions, forcing the group to offer customized SLAs and value-added services.

These buyers, representing up to 40% of segment revenue in similar French port logistics markets (2024 data), have the scale to negotiate lower rates and stricter KPIs, increasing customer bargaining power.

To retain high-volume accounts the group must prove superior reliability—99.5% on-time handling targets—and seamless IT integration (WMS/TMS) to avoid churn and margin erosion.

- Key fact: major clients can claim 10–20% discount leverage

- Retention hinges on 99%+ uptime and API-based system links

- Customized SLAs drive higher margins but add operational complexity

Audience Influence on Advertising Rates

- Global digital ad spend 2024: 619 billion USD

- Traditional TV CPM decline: ~6–8% annually (2021–24)

- Key metric to defend rates: cost per completed view

Customers Hold Strong Leverage: SVOD 66%, $619bn Ad Spend, 10–20% Discount Power

Customers across Canal+, advertising, energy retail and port logistics hold strong bargaining power due to abundant alternatives, price transparency, and scale: SVOD penetration 66% (France, 2024); global digital ad spend $619bn (2024); retail supplier switching +12% y/y (France, 2024); large logistics clients ≈40% segment revenue and 10–20% discount leverage.

| Metric | Value |

|---|---|

| SVOD penetration France (2024) | 66% |

| Global digital ad spend (2024) | $619bn |

| Retail supplier switching growth (France, 2024) | +12% y/y |

| Large clients share (logistics) | ≈40% revenue |

| Discount leverage by major clients | 10–20% |

Same Document Delivered

Compagnie de l'Odet Porter's Five Forces Analysis

This preview shows the exact Compagnie de l'Odet Porter’s Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for download with no placeholders or samples.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

Compagnie de l'Odet faces moderate supplier power and niche customer segments, while barriers to entry and substitute threats shape a competitive but navigable landscape.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Compagnie de l'Odet’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Content Licensing and Sports Rights

Canal+, the media arm of Compagnie de l'Odet, relies heavily on external suppliers for premium films and sports rights; in 2024 Canal+ paid roughly €1.2bn for sports rights, up 8% year-on-year, showing supplier leverage.

Major leagues (UEFA, Ligue 1) and studios command essential content that drives subscriptions, letting suppliers push prices and contract terms that reduce EBITDA margins—Canal+ reported media EBITDA margin fell to ~11% in 2024.

Energy Commodity Volatility

Bolloré Energy is a price taker in global oil markets, buying crude and refined products from major producers and refiners and passing market moves to customers; Brent averaged 86.3 USD/bbl in 2025 Q1, so input costs drive margins.

Dependence on large suppliers leaves Bolloré exposed to geopolitics and supply shocks—Russian supply cuts in 2022 and 2024 Libya unrest pushed regional wholesale spreads up 6–12%.

The firm has limited ability to influence base prices, so hedging and logistics control are key; Bolloré reported fuel trading exposure of EUR 1.2bn on its balance sheet in 2024.

Raw Materials for Battery Production

Suppliers of lithium and specialized polymers wield strong bargaining power for Compagnie de l'Odet’s Blue division because solid-state battery inputs are narrow and global EV demand lifted lithium prices ~85% from 2020–2022 and kept spodumene FOB at ~US$600–900/ton in 2024; a single-quarter supply disruption can delay production and raise COGS by several percentage points for the electricity storage segment.

Human Capital in Advertising and Media

Havas and its media units depend on senior creative and tech staff whose switching costs are low; top talent in advertising commands premium pay—global agency salary surveys in 2024 show 12–25% higher wages for senior creatives, and Havas reported 2024 personnel costs rising 9% to €1.3bn, so the group must spend more on retention and bonuses to avoid poaching by rivals.

- Top talent wage premium: 12–25% (2024 surveys)

- Havas personnel costs 2024: €1.3bn (+9%)

- High turnover raises client risk and hiring costs

Technology and Infrastructure Providers

The group depends on a few dominant cloud and telecom providers—AWS, Microsoft Azure, Google Cloud and major carriers—who control standardized pricing and SLAs; global cloud IaaS spending rose 21% in 2024 to about $229bn, keeping bargaining power with suppliers.

These vendors set non-negotiable contract terms and volume discounts that favor large platform customers, making it hard for Compagnie de l'Odet to lower costs or alter service terms.

Reliance on those platforms creates a material operational risk: outages, price increases or data-policy changes could disrupt the group's communication and logistics services and hit revenue and margins.

- Major suppliers: AWS, Azure, Google Cloud, top telcos

- Global cloud spend 2024: ~$229bn (+21%)

- Standardized terms limit negotiation

- High outage/price-change operational risk

Supplier power squeezes margins: sports, fuel, cloud and talent drive costs up

Suppliers across Canal+ (sports/studios), Bolloré Energy (crude/refined), Blue (lithium/polymers), Havas (talent) and cloud carriers hold strong leverage, driving costs and squeezing margins; Canal+ paid ~€1.2bn for sports rights in 2024 and media EBITDA fell to ~11%. Brent averaged $86.3/bbl in 2025 Q1; Bolloré disclosed €1.2bn fuel trading exposure in 2024. Cloud IaaS spend hit ~$229bn (+21%) in 2024, and Havas personnel costs rose to €1.3bn (+9%).

| Supplier | Key 2024–25 metric |

|---|---|

| Canal+ sports rights | €1.2bn (2024) |

| Media EBITDA | ~11% (2024) |

| Brent | $86.3/bbl (2025 Q1) |

| Fuel exposure | €1.2bn (2024) |

| Lithium/spodumene | $600–900/t FOB (2024) |

| Havas personnel costs | €1.3bn (+9%, 2024) |

| Cloud IaaS | $229bn (+21%, 2024) |

What is included in the product

Tailored Porter's Five Forces analysis for Compagnie de l'Odet that uncovers key competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and highlights disruptive forces and strategic protections for profitability.

A concise, one-sheet Porter's Five Forces summary for Compagnie de l'Odet—ideal for swift strategic decisions and boardroom slides.

Customers Bargaining Power

Subscription Choice and Churn

Individual consumers of Canal+ face many alternatives—from free-to-air channels to Netflix, Amazon Prime Video, and Disney+—so churn risk is high; France’s SVOD penetration hit 66% in 2024, raising switching pressure.

Subscribers can cancel quickly if price rises or content lags; Canal+ lost about 200,000 subscribers in 2023 after price adjustments, showing sensitivity to value perception.

To retain customers, Canal+ must invest in exclusive local and sport rights and originals—content spend was €1.6bn in 2024—to sustain loyalty and reduce churn.

Corporate Client Sensitivity

Havas serves multinational clients whose marketing budgets often exceed €100m, giving them strong bargaining power through formal RFPs and price pressure; in 2024, global ad buying by top 200 advertisers grew 6.2% so competition for those accounts intensified. Clients demand transparent KPIs and ROI reporting, citing benchmarks like CPM and ROAS, and can switch to rival networks with low vendor lock-in, raising churn risk and compressing margins.

Energy Market Price Transparency

Customers in energy distribution—residential and commercial—are highly price-sensitive; in France 2024 retail oil buyers switched suppliers 12% more year-over-year as price transparency rose, per CRE data.

Online comparison tools list fuel and heating-oil prices from 200+ suppliers in regions, so brand loyalty is often secondary to cost; 63% of households say price drives choice (IFOP, 2023).

This forces Compagnie de l'Odet to sustain lean operations: a 5–8% margin cushion is typical in 2024 wholesale-retail spreads, so efficiency directly enables competitive pricing in a transparent market.

B2B Logistics and Storage Demands

Large industrial and commercial clients using Compagnie de l'Odet's logistics and storage services demand high efficiency and tailored solutions, forcing the group to offer customized SLAs and value-added services.

These buyers, representing up to 40% of segment revenue in similar French port logistics markets (2024 data), have the scale to negotiate lower rates and stricter KPIs, increasing customer bargaining power.

To retain high-volume accounts the group must prove superior reliability—99.5% on-time handling targets—and seamless IT integration (WMS/TMS) to avoid churn and margin erosion.

- Key fact: major clients can claim 10–20% discount leverage

- Retention hinges on 99%+ uptime and API-based system links

- Customized SLAs drive higher margins but add operational complexity

Audience Influence on Advertising Rates

- Global digital ad spend 2024: 619 billion USD

- Traditional TV CPM decline: ~6–8% annually (2021–24)

- Key metric to defend rates: cost per completed view

Customers Hold Strong Leverage: SVOD 66%, $619bn Ad Spend, 10–20% Discount Power

Customers across Canal+, advertising, energy retail and port logistics hold strong bargaining power due to abundant alternatives, price transparency, and scale: SVOD penetration 66% (France, 2024); global digital ad spend $619bn (2024); retail supplier switching +12% y/y (France, 2024); large logistics clients ≈40% segment revenue and 10–20% discount leverage.

| Metric | Value |

|---|---|

| SVOD penetration France (2024) | 66% |

| Global digital ad spend (2024) | $619bn |

| Retail supplier switching growth (France, 2024) | +12% y/y |

| Large clients share (logistics) | ≈40% revenue |

| Discount leverage by major clients | 10–20% |

Same Document Delivered

Compagnie de l'Odet Porter's Five Forces Analysis

This preview shows the exact Compagnie de l'Odet Porter’s Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready for download with no placeholders or samples.