Compass Porter's Five Forces Analysis

From Overview to Strategy Blueprint

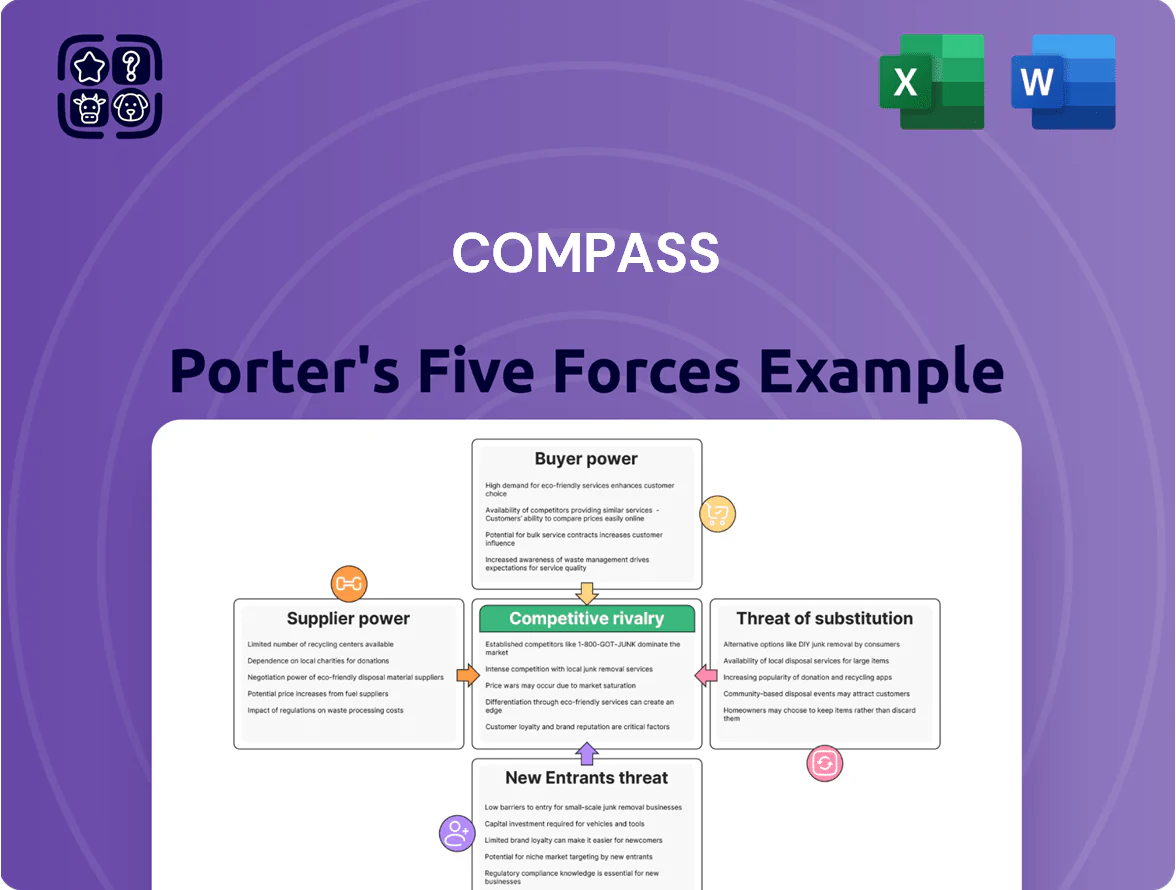

Compass faces moderate buyer power, rising competitive rivalry from tech-enabled brokerages, and increasing regulatory scrutiny that together shape pricing and expansion strategies; suppliers and substitutes exert mixed pressure depending on market segment. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Compass’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

High-Performing Real Estate Agents

Compass depends on high-performing agents as primary suppliers of listings and client relationships, which drive ~85% of closed transactions at US brokerages; top agents’ books are highly portable, giving them strong leverage to join rivals or go independent.

By late 2025 Compass must keep investing in its tech platform (agent productivity tools, CRM, AI pricing) and pay competitive splits/incentives—agent retention costs rose ~10–15% industrywide in 2024–25—else key agents may defect.

Cloud Infrastructure and SaaS Providers

Compass’s end-to-end platform depends on major cloud hosts (AWS, Google Cloud, Azure) and analytics SaaS; global cloud infrastructure spend hit $200B in 2024, so suppliers hold moderate leverage because migrating multi-petabyte, microservice-based systems is costly and slow.

Supplier disruptions or price increases feed directly into Compass’s margins—cloud costs represented ~12–18% of property-tech peers’ OPEX in 2023—so a 15% price hike could cut gross margin by several percentage points and harm platform SLAs.

Multiple Listing Service Data Access

Access to localized Multiple Listing Service (MLS) data is non-negotiable for brokerages; in the US over 600 MLSs collectively cover ~90% of listings, making them crucial suppliers for Compass’s platform.

MLSs wield power via rule-based data feeds and governance—Compass must comply with hundreds of differing policies, licensing fees (often $10s–$100s per agent annually), and IDX/VTB restrictions to keep listings authoritative.

While many MLSs cooperate, enforcement actions and feed throttling pose real risks to Compass’s inventory reliability and go-to-market speed.

Marketing and Lead Generation Vendors

Compass relies on external vendors for high-end photography, digital marketing, and lead generation to sustain its luxury brand appeal; these suppliers directly affect listing speed and price realization, with premium shoots raising average listing price by ~3–5% per industry studies (NAR, 2024).

Many vendors exist, but firms that can scale nationally and deliver consistent luxury-grade work command pricing power; top-tier marketing agencies report gross margins of 20–35% and often charge retainers or performance fees, giving them leverage over large brokerages like Compass.

Switching costs are moderate—Compass can change vendors—but brand risk and integration effort make procurement selective, so supplier bargaining power is elevated for specialized, scalable partners.

- Premium vendor impact: +3–5% on listing price (NAR 2024)

- Top agency margins: 20–35% (industry 2024)

- Many vendors, few scalable luxury specialists

- Moderate switching cost but high brand-risk

Specialized Tech Talent Recruitment

- Essential human capital: proprietary platform depends on specialists

- High leverage: median AI/ML pay ~$180k (2025)

- Competitive rivals: Big Tech + well-funded startups

- Impact: higher costs, slower innovation if hires slip

Suppliers Hold the Cards: Top Agents, MLSs & Cloud/AI Costs Threaten Margins

Suppliers wield moderate-to-strong power: top agents supply ~85% of transactions and can defect; cloud/analytics vendors (cloud spend $200B in 2024) and MLSs (600+ covering ~90% listings) add lock-in; specialized luxury vendors and AI/ML hires (median pay ~$180k in 2025) increase costs—a 15% cloud price rise could cut gross margin several points.

| Supplier | Key stat | Leverage |

|---|---|---|

| Top agents | ~85% transactions | High |

| Cloud providers | $200B global spend (2024) | Moderate |

| MLSs | 600+ MLS, ~90% listings | High |

| AI/ML hires | Median $180k (2025) | High |

What is included in the product

Tailored Porter’s Five Forces analysis for Compass, identifying competitive pressures, supplier and buyer influence, threat of substitutes and new entrants, and strategic levers to protect market share and profitability.

Interactive Porter's Five Forces in a single view—quickly pinpoint and relieve strategic pressure points for faster, confident decisions.

Customers Bargaining Power

End-User Home Buyers and Sellers

End-user buyers and sellers hold strong bargaining power as online listings and MLS transparency have raised market information; by Q4 2025, 78% of US homebuyers used online tools for pricing and comps per NAR surveys, enabling tougher commission negotiation.

With average seller-paid commission pressure down to ~5.1% in 2025 from 5.5% in 2019, Compass agents must prove value via platform tech — proprietary market-matching, real-time comps, and agent productivity tools — to justify fees.

Commission Rate Sensitivities

Following 2024–25 industry settlements that capped or reformed certain commission practices, sellers now push for listing fees down by 10–25% and buyers scrutinize reps’ pay; this raised customer bargaining power and forced Compass to adopt more flexible, transparent pricing—Compass reported in FY2025 gross commission income pressure with average take-rates falling ~12% year-over-year—so competitive survival needs clear, tiered fee options and published service breakouts.

Low Switching Costs for Clients

For most US buyers/sellers, switching from a Compass agent is low-cost before listing—real estate is infrequent, so 72% of consumers report choosing agents per transaction rather than brand loyalty (NAR 2024); Compass faces little sticky demand compared with subscription services.

This forces Compass to win each deal on service and tech: in 2024 Compass closed ~37,000 transactions, so marginal losses to aggressive local brokers can quickly erode share unless every agent delivers an exceptional experience.

Institutional Investor Influence

Demand for Integrated Digital Experiences

Modern buyers demand seamless, end-to-end digital journeys like in finance or retail; 70% of home hunters use mobile apps for searches and 52% expect instant messaging support, raising churn risk if Compass lags.

If Compass fails to match rivals—Redfin, Zillow—customers can switch to brokerages offering superior tech, pressuring Compass to invest in UX; Compass spent $160M on technology in 2024, showing this arms race.

- 70% use mobile apps

- 52% expect instant support

- $160M Compass tech spend 2024

- High churn vs Redfin/Zillow

Online pricing, shrinking commissions & Compass churn risk as institutions demand ROI

Buyers/sellers gained strong leverage from online transparency—78% used pricing tools by Q4 2025 (NAR); seller-paid commissions fell to ~5.1% in 2025, forcing Compass to justify fees with proprietary tech and tiers; institutional clients (>$10T holdings in 2024) demand bulk discounts and ROI analytics; Compass tech spend $160M in 2024 but FY2025 take-rates fell ~12%, so switching costs are low and churn risk high.

| Metric | Value |

|---|---|

| Online pricing users (Q4 2025) | 78% |

| Seller-paid commission (2025) | ~5.1% |

| Compass tech spend (2024) | $160M |

| Institutional US RE holdings (2024) | >$10T |

| Compass FY2025 take-rate change | -~12% YoY |

What You See Is What You Get

Compass Porter's Five Forces Analysis

This preview displays the exact Compass Porter's Five Forces analysis document you'll receive upon purchase—no placeholders, no mockups. The file shown is the fully formatted, professionally written deliverable, ready for immediate download and use the moment you complete your payment. What you see here is precisely what you'll get: a complete, final analysis tailored for strategic insight and decision-making.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

Compass faces moderate buyer power, rising competitive rivalry from tech-enabled brokerages, and increasing regulatory scrutiny that together shape pricing and expansion strategies; suppliers and substitutes exert mixed pressure depending on market segment. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Compass’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

High-Performing Real Estate Agents

Compass depends on high-performing agents as primary suppliers of listings and client relationships, which drive ~85% of closed transactions at US brokerages; top agents’ books are highly portable, giving them strong leverage to join rivals or go independent.

By late 2025 Compass must keep investing in its tech platform (agent productivity tools, CRM, AI pricing) and pay competitive splits/incentives—agent retention costs rose ~10–15% industrywide in 2024–25—else key agents may defect.

Cloud Infrastructure and SaaS Providers

Compass’s end-to-end platform depends on major cloud hosts (AWS, Google Cloud, Azure) and analytics SaaS; global cloud infrastructure spend hit $200B in 2024, so suppliers hold moderate leverage because migrating multi-petabyte, microservice-based systems is costly and slow.

Supplier disruptions or price increases feed directly into Compass’s margins—cloud costs represented ~12–18% of property-tech peers’ OPEX in 2023—so a 15% price hike could cut gross margin by several percentage points and harm platform SLAs.

Multiple Listing Service Data Access

Access to localized Multiple Listing Service (MLS) data is non-negotiable for brokerages; in the US over 600 MLSs collectively cover ~90% of listings, making them crucial suppliers for Compass’s platform.

MLSs wield power via rule-based data feeds and governance—Compass must comply with hundreds of differing policies, licensing fees (often $10s–$100s per agent annually), and IDX/VTB restrictions to keep listings authoritative.

While many MLSs cooperate, enforcement actions and feed throttling pose real risks to Compass’s inventory reliability and go-to-market speed.

Marketing and Lead Generation Vendors

Compass relies on external vendors for high-end photography, digital marketing, and lead generation to sustain its luxury brand appeal; these suppliers directly affect listing speed and price realization, with premium shoots raising average listing price by ~3–5% per industry studies (NAR, 2024).

Many vendors exist, but firms that can scale nationally and deliver consistent luxury-grade work command pricing power; top-tier marketing agencies report gross margins of 20–35% and often charge retainers or performance fees, giving them leverage over large brokerages like Compass.

Switching costs are moderate—Compass can change vendors—but brand risk and integration effort make procurement selective, so supplier bargaining power is elevated for specialized, scalable partners.

- Premium vendor impact: +3–5% on listing price (NAR 2024)

- Top agency margins: 20–35% (industry 2024)

- Many vendors, few scalable luxury specialists

- Moderate switching cost but high brand-risk

Specialized Tech Talent Recruitment

- Essential human capital: proprietary platform depends on specialists

- High leverage: median AI/ML pay ~$180k (2025)

- Competitive rivals: Big Tech + well-funded startups

- Impact: higher costs, slower innovation if hires slip

Suppliers Hold the Cards: Top Agents, MLSs & Cloud/AI Costs Threaten Margins

Suppliers wield moderate-to-strong power: top agents supply ~85% of transactions and can defect; cloud/analytics vendors (cloud spend $200B in 2024) and MLSs (600+ covering ~90% listings) add lock-in; specialized luxury vendors and AI/ML hires (median pay ~$180k in 2025) increase costs—a 15% cloud price rise could cut gross margin several points.

| Supplier | Key stat | Leverage |

|---|---|---|

| Top agents | ~85% transactions | High |

| Cloud providers | $200B global spend (2024) | Moderate |

| MLSs | 600+ MLS, ~90% listings | High |

| AI/ML hires | Median $180k (2025) | High |

What is included in the product

Tailored Porter’s Five Forces analysis for Compass, identifying competitive pressures, supplier and buyer influence, threat of substitutes and new entrants, and strategic levers to protect market share and profitability.

Interactive Porter's Five Forces in a single view—quickly pinpoint and relieve strategic pressure points for faster, confident decisions.

Customers Bargaining Power

End-User Home Buyers and Sellers

End-user buyers and sellers hold strong bargaining power as online listings and MLS transparency have raised market information; by Q4 2025, 78% of US homebuyers used online tools for pricing and comps per NAR surveys, enabling tougher commission negotiation.

With average seller-paid commission pressure down to ~5.1% in 2025 from 5.5% in 2019, Compass agents must prove value via platform tech — proprietary market-matching, real-time comps, and agent productivity tools — to justify fees.

Commission Rate Sensitivities

Following 2024–25 industry settlements that capped or reformed certain commission practices, sellers now push for listing fees down by 10–25% and buyers scrutinize reps’ pay; this raised customer bargaining power and forced Compass to adopt more flexible, transparent pricing—Compass reported in FY2025 gross commission income pressure with average take-rates falling ~12% year-over-year—so competitive survival needs clear, tiered fee options and published service breakouts.

Low Switching Costs for Clients

For most US buyers/sellers, switching from a Compass agent is low-cost before listing—real estate is infrequent, so 72% of consumers report choosing agents per transaction rather than brand loyalty (NAR 2024); Compass faces little sticky demand compared with subscription services.

This forces Compass to win each deal on service and tech: in 2024 Compass closed ~37,000 transactions, so marginal losses to aggressive local brokers can quickly erode share unless every agent delivers an exceptional experience.

Institutional Investor Influence

Demand for Integrated Digital Experiences

Modern buyers demand seamless, end-to-end digital journeys like in finance or retail; 70% of home hunters use mobile apps for searches and 52% expect instant messaging support, raising churn risk if Compass lags.

If Compass fails to match rivals—Redfin, Zillow—customers can switch to brokerages offering superior tech, pressuring Compass to invest in UX; Compass spent $160M on technology in 2024, showing this arms race.

- 70% use mobile apps

- 52% expect instant support

- $160M Compass tech spend 2024

- High churn vs Redfin/Zillow

Online pricing, shrinking commissions & Compass churn risk as institutions demand ROI

Buyers/sellers gained strong leverage from online transparency—78% used pricing tools by Q4 2025 (NAR); seller-paid commissions fell to ~5.1% in 2025, forcing Compass to justify fees with proprietary tech and tiers; institutional clients (>$10T holdings in 2024) demand bulk discounts and ROI analytics; Compass tech spend $160M in 2024 but FY2025 take-rates fell ~12%, so switching costs are low and churn risk high.

| Metric | Value |

|---|---|

| Online pricing users (Q4 2025) | 78% |

| Seller-paid commission (2025) | ~5.1% |

| Compass tech spend (2024) | $160M |

| Institutional US RE holdings (2024) | >$10T |

| Compass FY2025 take-rate change | -~12% YoY |

What You See Is What You Get

Compass Porter's Five Forces Analysis

This preview displays the exact Compass Porter's Five Forces analysis document you'll receive upon purchase—no placeholders, no mockups. The file shown is the fully formatted, professionally written deliverable, ready for immediate download and use the moment you complete your payment. What you see here is precisely what you'll get: a complete, final analysis tailored for strategic insight and decision-making.