CompX PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political, economic, and technological forces are shaping CompX’s trajectory with our concise PESTLE snapshot—perfect for investors and strategists who need fast, actionable context; buy the full analysis to access in-depth insights, editable charts, and strategic recommendations you can use immediately.

Political factors

Trade Policy and Tariff Impacts

Government Infrastructure and Security Spending

CompX benefits from federal and state initiatives to upgrade government facilities, postal services, and transportation hubs that need high-security locking systems; the FY2025 U.S. homeland security and infrastructure budgets rose to roughly $120 billion combined, supporting higher procurement activity. Increased physical security spending historically tracks with a 10–15% uptick in institutional orders for CompX’s specialized products. Analysts monitor 2025 legislative priorities and earmarks to forecast potential growth in institutional contracts, noting several states increased capital outlays for transit and postal facility upgrades in 2024–25.

Maritime Regulatory Environment

Political decisions on maritime safety and recreational boating regulations directly affect design and sales of CompX marine components; for example, stricter safety mandates could raise compliance costs across the US/EU market—estimated $0.5–1.2bn industry compliance outlays in 2024—impacting throttle and steering margins.

Changes to boating access laws or waterway environmental mandates can reduce pleasure-boat registrations (US registrations fell 3.1% in 2023), shrinking demand in CompX’s primary market and pressuring revenue.

Active engagement with industry advocacy groups is essential: trade lobbying influenced a 2024 US Coast Guard rule delay, underscoring how advocacy can protect CompX’s sales of throttle and steering systems.

Geopolitical Supply Chain Security

Ongoing geopolitical tensions push CompX toward near-shoring/friend-shoring; 2024 supply-chain reshoring investments rose 18% globally, reducing reliance on high-risk suppliers for critical inputs.

Political instability in shipping lanes/manufacturing hubs can extend lead times by 20–35% and raise transportation costs for Marine Components, impacting margins.

CompX must keep flexible sourcing, multi-sourcing and buffer inventories to hedge sudden shifts in international relations or regional conflicts.

- Reshoring investments +18% (2024)

- Potential lead-time increase 20–35%

- Actions: near-shore, friend-shore, multi-source, inventory buffers

Corporate Taxation and Incentives

The US federal corporate tax rate remains 21% after 2017 reform; enhanced R&D tax credits (up to 20% effective relief for qualifying spend) materially influence CompX capital allocation—R&D capex represented 8% of revenues for peers in 2024, a benchmark for reinvestment.

Recent state-level manufacturing incentives (e.g., $1.2B in 2024 grants across Midwestern states) and IRA-linked credits for domestic production can shift CompX toward onshore facilities and automation to capture up to 10–15% effective tax savings.

Conversely, any hypothetical federal corporate rate increase to 25–28% would cut net income margins by ~4–7 percentage points on EBITDA margins of 18% (2024 peer median), reducing funds for dividends and buybacks and pressuring valuation multiples.

- 21% federal rate; R&D credits ≈ up to 20% relief

- State manufacturing incentives totaled ≈ $1.2B (2024)

- Potential rate hike to 25–28% could reduce net margins by ~4–7 pts

- R&D capex benchmark ≈ 8% of revenue (2024 peers)

Policy shocks could reshape CompX costs, capex, lead times and institutional demand

Political actions—trade tariffs, protectionism, tax policy, infrastructure spending, and maritime/regulatory changes—can shift CompX’s input costs (raw materials ≈42% of COGS), capex (+8–12% if reshoring), lead times (+15–35%), and addressable institutional demand (+10–15%).

| Metric | 2024–25 |

|---|---|

| Raw materials of COGS | ≈42% |

| Reshoring spend change | +18% |

| Lead-time risk | +15–35% |

| Institutional order lift | +10–15% |

What is included in the product

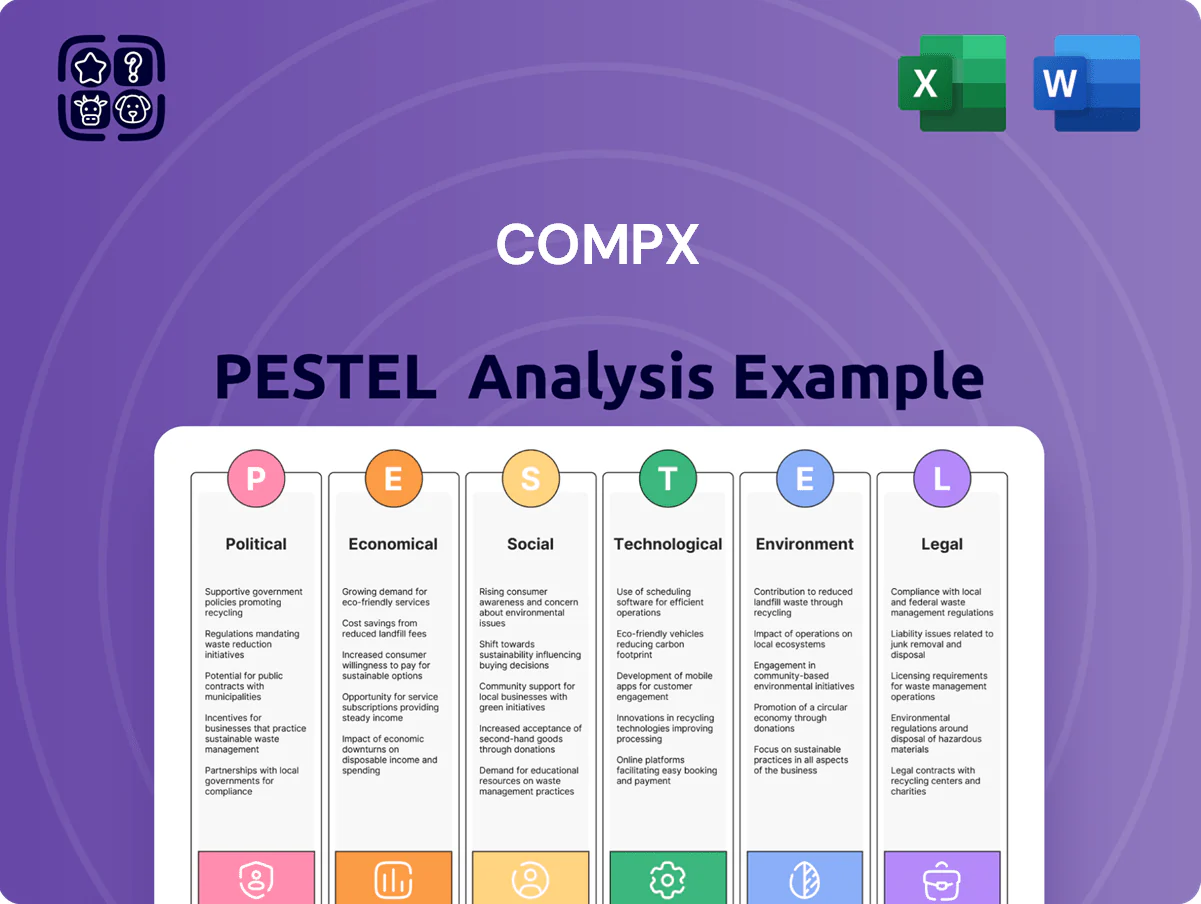

Explores how external macro-environmental factors uniquely affect CompX across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section supported by current data and trend analysis to identify risks and opportunities.

Condenses CompX's full PESTLE into a clear, shareable summary segmented by category for quick reference in meetings, presentations, or client reports—editable for local context and deliverable in presentation-ready format.

Economic factors

Interest Rate Environment and Consumer Financing

High interest rates reduce consumer borrowing for discretionary items like pleasure boats, pressuring CompX's Marine Components sales; US 30-year fixed mortgage averaged ~7.2% in Q4 2025 and US consumer auto/boat loan rates rose above 8%, dampening big-ticket purchases.

Central bank policy trajectory remains pivotal: as of late 2025 the Fed signaled rates likely to stay restrictive, keeping financing costs high and constraining demand for high-end recreational hardware.

Conversely, a lower rate environment historically boosts housing and office activity—US housing starts rose ~12% year-over-year in 2024 when rates eased—supporting higher demand for cabinet and furniture locks.

Commodity Price Volatility

CompX faces material-price risk from zinc, brass and stainless steel; LME zinc rose ~18% in 2024 and U.S. stainless scrap prices surged ~22% year-on-year, elevating input costs and pressuring margins if price pass-through is limited.

Consumer Discretionary Spending Trends

The recreational marine segment is highly tied to disposable income among affluent households; U.S. boat retail sales rose 12% to $7.6 billion in 2023 but fell 4% in H1 2025 amid rising rates and softening confidence. Economic downturns historically cut boat orders — new boat wholesale units fell 9% in 2024 vs 2022 — directly affecting CompX’s boat-building customers. CompX revenue trends thus act as a bellwether for luxury and recreational spending cycles.

Commercial Real Estate and Office Cycles

Demand for CompX's security products tracks commercial office turnover and renovation; U.S. office vacancy rose to ~16.6% in Q4 2024 but healthcare and education capital spending increased, supporting durable lock demand.

Remote work trimmed new office builds, yet 2024 institutional construction spending grew ~4.2% YoY, sustaining mechanical/electrical lock sales during upgrade cycles.

- Office vacancy 16.6% (Q4 2024)

- Institutional construction +4.2% YoY (2024)

- Healthcare/education remain high-value, repeat lock markets

Labor Market Costs and Availability

Inflation-driven wage growth (US average hourly earnings rose 4.2% YoY in 2025 Q4) and a 2025 shortage of skilled manufacturing workers—vacancy rate 5.4% in North American manufacturing—raise CompX’s labor costs and pressure margins.

To remain profitable CompX must offer market-competitive pay while preserving lean operations; wages now account for ~28% of COGS in comparable firms.

Persistent labor shortfalls push accelerated automation spend—capital expenditures on robotics rose 12% YoY in 2025—to offset rising human capital expenses.

- Wage inflation: +4.2% YoY (2025 Q4)

- Manufacturing vacancy: 5.4% (2025)

- Labor ≈28% of COGS (peers)

- Robotics CAPEX +12% YoY (2025)

High rates squeeze marine demand; input, wage inflation boost automation push

High rates (30-yr mortgage ~7.2% Q4 2025; auto/boat loans >8%) curb marine discretionary demand while Fed keeps policy restrictive; housing/office easing historically lifts cabinet/lock sales (housing starts +12% YoY in 2024). Input-cost risk: LME zinc +18% (2024), U.S. stainless scrap +22% YoY, squeezing margins if pass-through limited. Labor pressure: wages +4.2% YoY (2025 Q4), manufacturing vacancy 5.4%, robotics CAPEX +12% YoY.

| Metric | Value |

|---|---|

| 30-yr mortgage | ~7.2% (Q4 2025) |

| Auto/boat loan rates | >8% (2025) |

| LME zinc | +18% (2024) |

| Stainless scrap US | +22% YoY (2024) |

| Wage growth | +4.2% YoY (2025 Q4) |

| Manufacturing vacancy | 5.4% (2025) |

| Robotics CAPEX | +12% YoY (2025) |

Preview the Actual Deliverable

CompX PESTLE Analysis

The preview shown here is the exact CompX PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning.

No placeholders or teasers: the content, layout, and insights visible in the preview are the final file you’ll be able to download immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political, economic, and technological forces are shaping CompX’s trajectory with our concise PESTLE snapshot—perfect for investors and strategists who need fast, actionable context; buy the full analysis to access in-depth insights, editable charts, and strategic recommendations you can use immediately.

Political factors

Trade Policy and Tariff Impacts

Government Infrastructure and Security Spending

CompX benefits from federal and state initiatives to upgrade government facilities, postal services, and transportation hubs that need high-security locking systems; the FY2025 U.S. homeland security and infrastructure budgets rose to roughly $120 billion combined, supporting higher procurement activity. Increased physical security spending historically tracks with a 10–15% uptick in institutional orders for CompX’s specialized products. Analysts monitor 2025 legislative priorities and earmarks to forecast potential growth in institutional contracts, noting several states increased capital outlays for transit and postal facility upgrades in 2024–25.

Maritime Regulatory Environment

Political decisions on maritime safety and recreational boating regulations directly affect design and sales of CompX marine components; for example, stricter safety mandates could raise compliance costs across the US/EU market—estimated $0.5–1.2bn industry compliance outlays in 2024—impacting throttle and steering margins.

Changes to boating access laws or waterway environmental mandates can reduce pleasure-boat registrations (US registrations fell 3.1% in 2023), shrinking demand in CompX’s primary market and pressuring revenue.

Active engagement with industry advocacy groups is essential: trade lobbying influenced a 2024 US Coast Guard rule delay, underscoring how advocacy can protect CompX’s sales of throttle and steering systems.

Geopolitical Supply Chain Security

Ongoing geopolitical tensions push CompX toward near-shoring/friend-shoring; 2024 supply-chain reshoring investments rose 18% globally, reducing reliance on high-risk suppliers for critical inputs.

Political instability in shipping lanes/manufacturing hubs can extend lead times by 20–35% and raise transportation costs for Marine Components, impacting margins.

CompX must keep flexible sourcing, multi-sourcing and buffer inventories to hedge sudden shifts in international relations or regional conflicts.

- Reshoring investments +18% (2024)

- Potential lead-time increase 20–35%

- Actions: near-shore, friend-shore, multi-source, inventory buffers

Corporate Taxation and Incentives

The US federal corporate tax rate remains 21% after 2017 reform; enhanced R&D tax credits (up to 20% effective relief for qualifying spend) materially influence CompX capital allocation—R&D capex represented 8% of revenues for peers in 2024, a benchmark for reinvestment.

Recent state-level manufacturing incentives (e.g., $1.2B in 2024 grants across Midwestern states) and IRA-linked credits for domestic production can shift CompX toward onshore facilities and automation to capture up to 10–15% effective tax savings.

Conversely, any hypothetical federal corporate rate increase to 25–28% would cut net income margins by ~4–7 percentage points on EBITDA margins of 18% (2024 peer median), reducing funds for dividends and buybacks and pressuring valuation multiples.

- 21% federal rate; R&D credits ≈ up to 20% relief

- State manufacturing incentives totaled ≈ $1.2B (2024)

- Potential rate hike to 25–28% could reduce net margins by ~4–7 pts

- R&D capex benchmark ≈ 8% of revenue (2024 peers)

Policy shocks could reshape CompX costs, capex, lead times and institutional demand

Political actions—trade tariffs, protectionism, tax policy, infrastructure spending, and maritime/regulatory changes—can shift CompX’s input costs (raw materials ≈42% of COGS), capex (+8–12% if reshoring), lead times (+15–35%), and addressable institutional demand (+10–15%).

| Metric | 2024–25 |

|---|---|

| Raw materials of COGS | ≈42% |

| Reshoring spend change | +18% |

| Lead-time risk | +15–35% |

| Institutional order lift | +10–15% |

What is included in the product

Explores how external macro-environmental factors uniquely affect CompX across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each section supported by current data and trend analysis to identify risks and opportunities.

Condenses CompX's full PESTLE into a clear, shareable summary segmented by category for quick reference in meetings, presentations, or client reports—editable for local context and deliverable in presentation-ready format.

Economic factors

Interest Rate Environment and Consumer Financing

High interest rates reduce consumer borrowing for discretionary items like pleasure boats, pressuring CompX's Marine Components sales; US 30-year fixed mortgage averaged ~7.2% in Q4 2025 and US consumer auto/boat loan rates rose above 8%, dampening big-ticket purchases.

Central bank policy trajectory remains pivotal: as of late 2025 the Fed signaled rates likely to stay restrictive, keeping financing costs high and constraining demand for high-end recreational hardware.

Conversely, a lower rate environment historically boosts housing and office activity—US housing starts rose ~12% year-over-year in 2024 when rates eased—supporting higher demand for cabinet and furniture locks.

Commodity Price Volatility

CompX faces material-price risk from zinc, brass and stainless steel; LME zinc rose ~18% in 2024 and U.S. stainless scrap prices surged ~22% year-on-year, elevating input costs and pressuring margins if price pass-through is limited.

Consumer Discretionary Spending Trends

The recreational marine segment is highly tied to disposable income among affluent households; U.S. boat retail sales rose 12% to $7.6 billion in 2023 but fell 4% in H1 2025 amid rising rates and softening confidence. Economic downturns historically cut boat orders — new boat wholesale units fell 9% in 2024 vs 2022 — directly affecting CompX’s boat-building customers. CompX revenue trends thus act as a bellwether for luxury and recreational spending cycles.

Commercial Real Estate and Office Cycles

Demand for CompX's security products tracks commercial office turnover and renovation; U.S. office vacancy rose to ~16.6% in Q4 2024 but healthcare and education capital spending increased, supporting durable lock demand.

Remote work trimmed new office builds, yet 2024 institutional construction spending grew ~4.2% YoY, sustaining mechanical/electrical lock sales during upgrade cycles.

- Office vacancy 16.6% (Q4 2024)

- Institutional construction +4.2% YoY (2024)

- Healthcare/education remain high-value, repeat lock markets

Labor Market Costs and Availability

Inflation-driven wage growth (US average hourly earnings rose 4.2% YoY in 2025 Q4) and a 2025 shortage of skilled manufacturing workers—vacancy rate 5.4% in North American manufacturing—raise CompX’s labor costs and pressure margins.

To remain profitable CompX must offer market-competitive pay while preserving lean operations; wages now account for ~28% of COGS in comparable firms.

Persistent labor shortfalls push accelerated automation spend—capital expenditures on robotics rose 12% YoY in 2025—to offset rising human capital expenses.

- Wage inflation: +4.2% YoY (2025 Q4)

- Manufacturing vacancy: 5.4% (2025)

- Labor ≈28% of COGS (peers)

- Robotics CAPEX +12% YoY (2025)

High rates squeeze marine demand; input, wage inflation boost automation push

High rates (30-yr mortgage ~7.2% Q4 2025; auto/boat loans >8%) curb marine discretionary demand while Fed keeps policy restrictive; housing/office easing historically lifts cabinet/lock sales (housing starts +12% YoY in 2024). Input-cost risk: LME zinc +18% (2024), U.S. stainless scrap +22% YoY, squeezing margins if pass-through limited. Labor pressure: wages +4.2% YoY (2025 Q4), manufacturing vacancy 5.4%, robotics CAPEX +12% YoY.

| Metric | Value |

|---|---|

| 30-yr mortgage | ~7.2% (Q4 2025) |

| Auto/boat loan rates | >8% (2025) |

| LME zinc | +18% (2024) |

| Stainless scrap US | +22% YoY (2024) |

| Wage growth | +4.2% YoY (2025 Q4) |

| Manufacturing vacancy | 5.4% (2025) |

| Robotics CAPEX | +12% YoY (2025) |

Preview the Actual Deliverable

CompX PESTLE Analysis

The preview shown here is the exact CompX PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning.

No placeholders or teasers: the content, layout, and insights visible in the preview are the final file you’ll be able to download immediately after checkout.