ConocoPhillips Business Model Canvas

ConocoPhillips Business Model Canvas: Strategic Blueprint for Investors & Strategists

Unlock the full strategic blueprint behind ConocoPhillips’s business model—this concise Business Model Canvas exposes how the company creates value, optimizes upstream operations, and monetizes hydrocarbons while managing geopolitical and ESG risks; perfect for investors, consultants, and strategists seeking actionable, ready-to-use insights.

Partnerships

Joint Venture Partners

Joint ventures with QatarEnergy and national oil companies share the multi-billion-dollar capex and geological risk of giant upstream and LNG projects; for example, ConocoPhillips’ 2024-25 portfolio included stakes in LNG developments adding roughly $6–8 billion in pro rata project commitments.

Host Governments and Regulators

Maintaining diplomatic and contractual ties with host governments in Norway, Australia, and Libya secures concessions and licenses that underpin ConocoPhillips’ reserves—Norway accounted for ~8% of 2024 production and Australia projects $1.2B capex through 2026.

These partnerships require navigating fiscal regimes, emissions rules, and local content mandates; aligning with national energy security goals helps stabilize operations and safeguard long-term cash flow.

Oilfield Service Providers

Strategic alliances with SLB (Schlumberger), Halliburton, and Baker Hughes supply advanced drilling and completion tech—ConocoPhillips used these partners to cut Permian well costs ~15% and lift Bakken first‑year recovery by ~8% in 2024, per company disclosures. These firms provide specialized rigs, frac fleets, and reservoir services that lower capital intensity and boost EURs across North America.

Midstream and Logistics Providers

Partnerships with pipeline operators and marine transport firms move ConocoPhillips hydrocarbons from wellheads to Gulf Coast refineries and export terminals, helping avoid takeaway bottlenecks and capture regional price spreads; in 2024 ConocoPhillips sold ~1.45 million barrels of oil equivalent per day (mmboed), so midstream access materially affects realized prices.

- Reduces takeaway constraints

- Enables access to Gulf Coast export markets

- Improves capture of regional price differentials

- Supports ~1.45 mmboed 2024 production

Technology and Research Institutions

ConocoPhillips partners with universities and startups to accelerate carbon capture, sequestration, and subsurface imaging; in 2024 it funded or co-funded R&D projects totaling about $120 million to scale methane-detection tech and emissions-reduction pilots.

These collaborations aim to cut fugitive methane and CO2 intensity—targeting ~30% methane-detection coverage growth by 2026—and sustain operational efficiency and competitive advantage.

- 2024 R&D spend ~ $120 million

- Target: ~30% increase in methane-detection coverage by 2026

- Focus: carbon capture, sequestration, subsurface imaging

- Outcome: scalable emissions-reduction pilots, improved ops efficiency

Large JV LNG Capex, Norway 8% of Output, $120M R&D, Permian costs -15%, +30% methane

JV stakes (QatarEnergy, NOCs) share $6–8B pro rata LNG capex; Norway ~8% of 2024 production; 2024 sales ~1.45 mmboed; 2024 R&D ~$120M; tech partners cut Permian well costs ~15% and raised Bakken first‑year recovery ~8%; targets: ~30% methane-detection coverage growth by 2026.

| Metric | 2024/Target |

|---|---|

| Pro rata LNG capex | $6–8B |

| Production (Norway) | ~8% |

| Sales | 1.45 mmboed |

| R&D | $120M |

| Permian cost cut | ~15% |

| Methane coverage target | +30% by 2026 |

What is included in the product

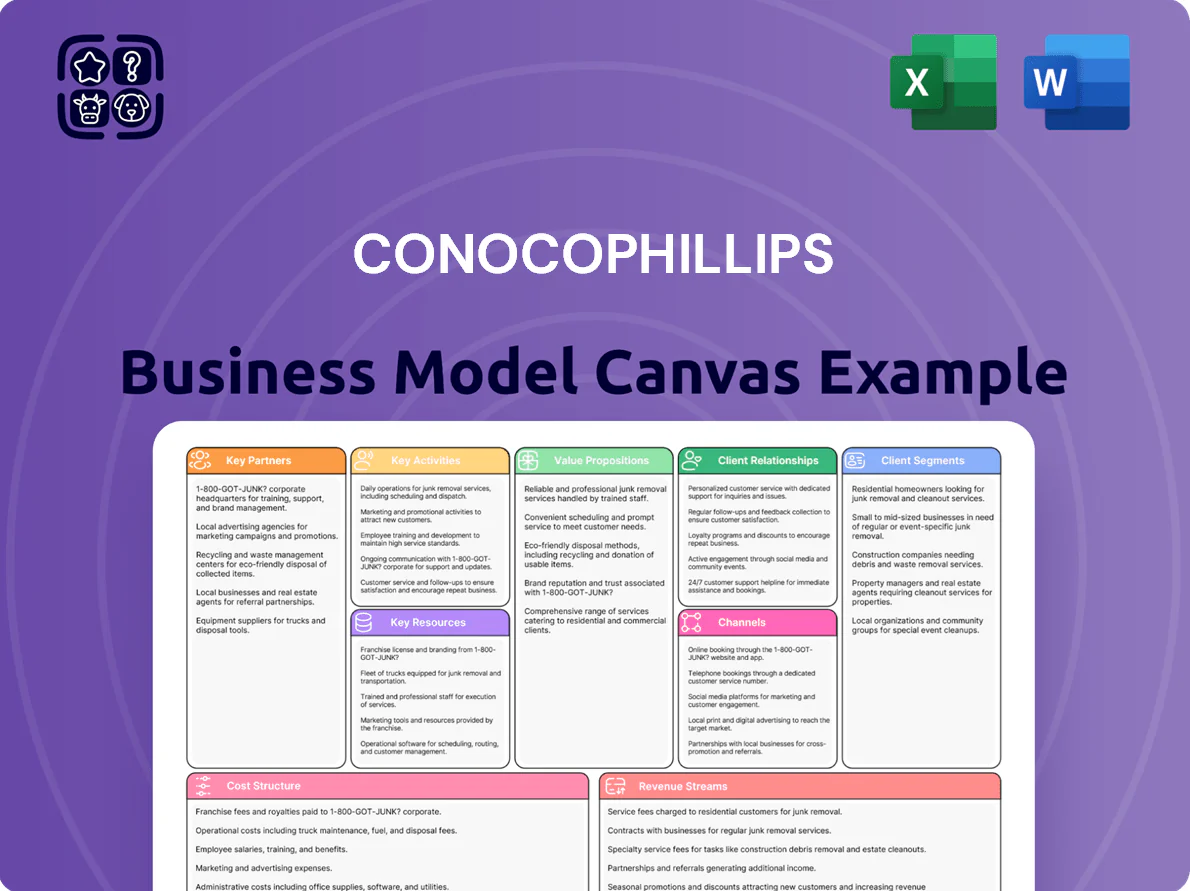

A comprehensive Business Model Canvas for ConocoPhillips detailing customer segments, channels, value propositions, key activities, resources, partners, cost structure and revenue streams aligned with its upstream-focused E&P strategy and integrated risk/ESG considerations.

High-level view of ConocoPhillips’ business model with editable cells to quickly pinpoint upstream strengths, cost drivers, and cashflow levers for boardrooms or team strategy sessions.

Activities

Exploration and Appraisal

ConocoPhillips uses advanced seismic imaging and geological modeling to pinpoint and appraise reserves across ~9.3 million net acres, prioritizing low-cost-of-supply plays that survive price swings; 2024 average upstream cash operating costs were about $8–10/boe. By late 2025 the company is maximizing value from core positions and selectively pursuing high‑impact international prospects, cutting lower-ranked acreage to boost returns.

Field Development and Production

Field development and production covers drilling, completion, and well management to produce crude oil, natural gas, and NGLs; ConocoPhillips reported average production of 1.401 million boe/d in 2024 and invested $6.9 billion in upstream capex that year.

The company uses reservoir management (e.g., 4D seismic, infill drilling) to optimize rates and extend asset life, while targeting safety and emissions cuts—contributing to a 12% reduction in operated methane intensity from 2019–2024.

Marketing and Trading

ConocoPhillips sells and ships ~1.4 million barrels of oil equivalent per day (2024 average) to global buyers, with marketing teams using market and logistics analysis to maximize netback and manage complex supply chains.

They employ physical trading, long‑term contracts, and financial hedges—ConocoPhillips reported $3.2 billion in realized gains on commodity risk management in 2024—to smooth cash flow and optimize revenue.

Portfolio Optimization

Continuous assessment of ConocoPhillips’ global asset base drives divestment of non-core assets and targeted acquisitions, directing capital to highest risk-adjusted returns; in 2025 the company completed full integration of Marathon Oil assets to capture estimated annual cost synergies of roughly $300–400 million and expand U.S. onshore production by ~10%.

- 2025 synergy target: $300–400M/yr

- U.S. onshore prod +~10% post-integration

- Capital allocation focused on top-tier acreage

Sustainability and Emissions Reduction

- Electrification of remote sites: ongoing pilots, lowers Scope 1 emissions

- Advanced methane monitoring: 12% methane intensity cut since 2016

- Carbon capture investment: $2.5 billion committed to 2030

Integrated energy growth: 1.4M boe/d, $6.9B capex, $3.2B hedges, $2.5B CCUS

Core activities: explore/appraise ~9.3M net acres using advanced seismic and geology, develop/produce 1.401M boe/d (2024) with $6.9B upstream capex (2024), run reservoir optimization and emissions cuts (12% methane intensity reduction vs 2019), market ~1.4M boe/d, use trading/hedges (US$3.2B realized gains 2024), pursue divestments/acquisitions (Marathon integration: $300–400M synergies; US onshore +~10%), and invest $2.5B in CCUS to 2030.

| Metric | Value |

|---|---|

| Net acres | ~9.3M |

| Prod (2024) | 1.401M boe/d |

| Upstream capex (2024) | $6.9B |

| Realized hedge gains (2024) | $3.2B |

| Methane intensity cut | 12% (2019–2024) |

| Marathon synergies (2025) | $300–400M/yr |

| CCUS commit to 2030 | $2.5B |

Full Version Awaits

Business Model Canvas

The ConocoPhillips Business Model Canvas preview shown here is the actual deliverable—not a mockup or sample—and represents the same content and layout you will receive after purchase.

When you complete your order, you’ll instantly get the full, editable document in Word and Excel formats, structured exactly as seen in this preview with no hidden pages or filler content.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

ConocoPhillips Business Model Canvas: Strategic Blueprint for Investors & Strategists

Unlock the full strategic blueprint behind ConocoPhillips’s business model—this concise Business Model Canvas exposes how the company creates value, optimizes upstream operations, and monetizes hydrocarbons while managing geopolitical and ESG risks; perfect for investors, consultants, and strategists seeking actionable, ready-to-use insights.

Partnerships

Joint Venture Partners

Joint ventures with QatarEnergy and national oil companies share the multi-billion-dollar capex and geological risk of giant upstream and LNG projects; for example, ConocoPhillips’ 2024-25 portfolio included stakes in LNG developments adding roughly $6–8 billion in pro rata project commitments.

Host Governments and Regulators

Maintaining diplomatic and contractual ties with host governments in Norway, Australia, and Libya secures concessions and licenses that underpin ConocoPhillips’ reserves—Norway accounted for ~8% of 2024 production and Australia projects $1.2B capex through 2026.

These partnerships require navigating fiscal regimes, emissions rules, and local content mandates; aligning with national energy security goals helps stabilize operations and safeguard long-term cash flow.

Oilfield Service Providers

Strategic alliances with SLB (Schlumberger), Halliburton, and Baker Hughes supply advanced drilling and completion tech—ConocoPhillips used these partners to cut Permian well costs ~15% and lift Bakken first‑year recovery by ~8% in 2024, per company disclosures. These firms provide specialized rigs, frac fleets, and reservoir services that lower capital intensity and boost EURs across North America.

Midstream and Logistics Providers

Partnerships with pipeline operators and marine transport firms move ConocoPhillips hydrocarbons from wellheads to Gulf Coast refineries and export terminals, helping avoid takeaway bottlenecks and capture regional price spreads; in 2024 ConocoPhillips sold ~1.45 million barrels of oil equivalent per day (mmboed), so midstream access materially affects realized prices.

- Reduces takeaway constraints

- Enables access to Gulf Coast export markets

- Improves capture of regional price differentials

- Supports ~1.45 mmboed 2024 production

Technology and Research Institutions

ConocoPhillips partners with universities and startups to accelerate carbon capture, sequestration, and subsurface imaging; in 2024 it funded or co-funded R&D projects totaling about $120 million to scale methane-detection tech and emissions-reduction pilots.

These collaborations aim to cut fugitive methane and CO2 intensity—targeting ~30% methane-detection coverage growth by 2026—and sustain operational efficiency and competitive advantage.

- 2024 R&D spend ~ $120 million

- Target: ~30% increase in methane-detection coverage by 2026

- Focus: carbon capture, sequestration, subsurface imaging

- Outcome: scalable emissions-reduction pilots, improved ops efficiency

Large JV LNG Capex, Norway 8% of Output, $120M R&D, Permian costs -15%, +30% methane

JV stakes (QatarEnergy, NOCs) share $6–8B pro rata LNG capex; Norway ~8% of 2024 production; 2024 sales ~1.45 mmboed; 2024 R&D ~$120M; tech partners cut Permian well costs ~15% and raised Bakken first‑year recovery ~8%; targets: ~30% methane-detection coverage growth by 2026.

| Metric | 2024/Target |

|---|---|

| Pro rata LNG capex | $6–8B |

| Production (Norway) | ~8% |

| Sales | 1.45 mmboed |

| R&D | $120M |

| Permian cost cut | ~15% |

| Methane coverage target | +30% by 2026 |

What is included in the product

A comprehensive Business Model Canvas for ConocoPhillips detailing customer segments, channels, value propositions, key activities, resources, partners, cost structure and revenue streams aligned with its upstream-focused E&P strategy and integrated risk/ESG considerations.

High-level view of ConocoPhillips’ business model with editable cells to quickly pinpoint upstream strengths, cost drivers, and cashflow levers for boardrooms or team strategy sessions.

Activities

Exploration and Appraisal

ConocoPhillips uses advanced seismic imaging and geological modeling to pinpoint and appraise reserves across ~9.3 million net acres, prioritizing low-cost-of-supply plays that survive price swings; 2024 average upstream cash operating costs were about $8–10/boe. By late 2025 the company is maximizing value from core positions and selectively pursuing high‑impact international prospects, cutting lower-ranked acreage to boost returns.

Field Development and Production

Field development and production covers drilling, completion, and well management to produce crude oil, natural gas, and NGLs; ConocoPhillips reported average production of 1.401 million boe/d in 2024 and invested $6.9 billion in upstream capex that year.

The company uses reservoir management (e.g., 4D seismic, infill drilling) to optimize rates and extend asset life, while targeting safety and emissions cuts—contributing to a 12% reduction in operated methane intensity from 2019–2024.

Marketing and Trading

ConocoPhillips sells and ships ~1.4 million barrels of oil equivalent per day (2024 average) to global buyers, with marketing teams using market and logistics analysis to maximize netback and manage complex supply chains.

They employ physical trading, long‑term contracts, and financial hedges—ConocoPhillips reported $3.2 billion in realized gains on commodity risk management in 2024—to smooth cash flow and optimize revenue.

Portfolio Optimization

Continuous assessment of ConocoPhillips’ global asset base drives divestment of non-core assets and targeted acquisitions, directing capital to highest risk-adjusted returns; in 2025 the company completed full integration of Marathon Oil assets to capture estimated annual cost synergies of roughly $300–400 million and expand U.S. onshore production by ~10%.

- 2025 synergy target: $300–400M/yr

- U.S. onshore prod +~10% post-integration

- Capital allocation focused on top-tier acreage

Sustainability and Emissions Reduction

- Electrification of remote sites: ongoing pilots, lowers Scope 1 emissions

- Advanced methane monitoring: 12% methane intensity cut since 2016

- Carbon capture investment: $2.5 billion committed to 2030

Integrated energy growth: 1.4M boe/d, $6.9B capex, $3.2B hedges, $2.5B CCUS

Core activities: explore/appraise ~9.3M net acres using advanced seismic and geology, develop/produce 1.401M boe/d (2024) with $6.9B upstream capex (2024), run reservoir optimization and emissions cuts (12% methane intensity reduction vs 2019), market ~1.4M boe/d, use trading/hedges (US$3.2B realized gains 2024), pursue divestments/acquisitions (Marathon integration: $300–400M synergies; US onshore +~10%), and invest $2.5B in CCUS to 2030.

| Metric | Value |

|---|---|

| Net acres | ~9.3M |

| Prod (2024) | 1.401M boe/d |

| Upstream capex (2024) | $6.9B |

| Realized hedge gains (2024) | $3.2B |

| Methane intensity cut | 12% (2019–2024) |

| Marathon synergies (2025) | $300–400M/yr |

| CCUS commit to 2030 | $2.5B |

Full Version Awaits

Business Model Canvas

The ConocoPhillips Business Model Canvas preview shown here is the actual deliverable—not a mockup or sample—and represents the same content and layout you will receive after purchase.

When you complete your order, you’ll instantly get the full, editable document in Word and Excel formats, structured exactly as seen in this preview with no hidden pages or filler content.