Consigli Construction Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

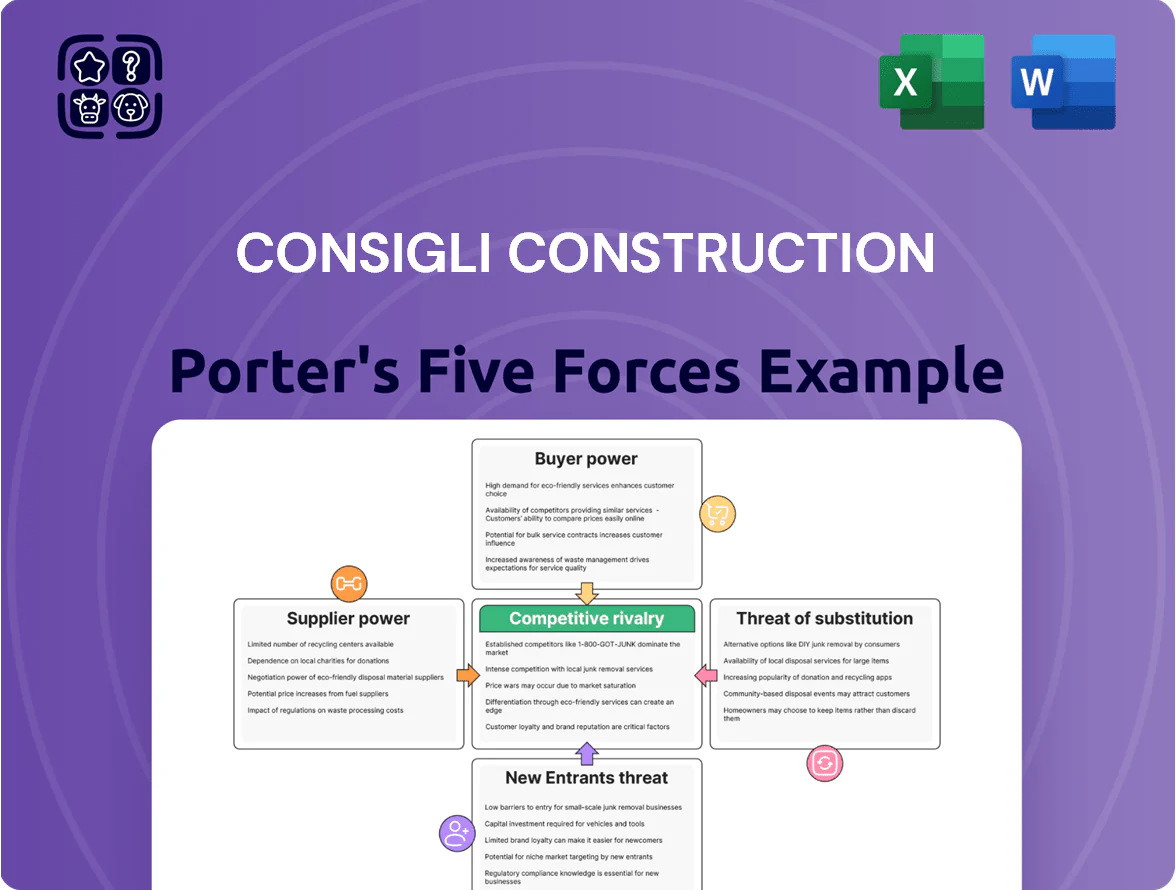

Consigli Construction faces moderate buyer power, intense rivalry in regional markets, and supplier influence driven by subcontractor availability and material costs; regulatory and project-scale barriers keep new entrants manageable but technology and substitutes (modular construction) pose rising threats. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Consigli’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Labor Shortages

The late-2025 shortage of skilled trades—MEP (mechanical, electrical, plumbing) workers—remains acute, with US Bureau of Labor Statistics data showing 11% fewer qualified journeymen in construction specialties versus 2019 and sector wage premiums up 9% year-over-year; that scarcity gives unions and niche subcontractors strong bargaining power over Consigli on pay and sequencing, so Consigli must nurture preferred-partner agreements and pay premiums to avoid schedule slippage and cost overruns.

Volatility in Raw Material Costs

Global supply chain disruptions and geopolitical shifts pushed structural steel prices up ~22% and softwood timber up ~18% between 2020–2025, keeping costs volatile into 2025.

Low substitute availability for high-spec institutional projects gives suppliers pricing power, especially for certified steel and CLT (cross-laminated timber).

Consigli reduces exposure via early procurement and bulk buys—over 40% of 2024 large-project tonnage was pre-contracted—but supplier leverage still compresses margins by an estimated 1–2 percentage points.

Technological Integration Requirements

Suppliers of Building Information Modeling software and green-tech hold strong leverage over Consigli because their products are specialized and few vendors meet industry BIM certification and LEED/ILFI sustainable-material standards; global BIM market grew 12.6% in 2024 to $9.9B, concentrating vendor power.

Consigli’s 2025 sustainability targets raise reliance on certified low-carbon materials—only ~15% of US suppliers meet stringent carbon-reporting standards—so supplier options shrink and negotiation power rises.

High switching costs for integrated tech and supply chains—often >$1M per large project in rework and retraining—lock Consigli to vendors, further empowering suppliers.

Subcontractor Concentration in Niche Markets

In academic and cultural projects, roughly 10–15 specialist subcontractors dominate complex historical renovations and high-tech lab fit-outs, allowing them to command premiums of 12–20% above standard rates and to pick projects selectively.

Consigli’s dependence on this elite tier for core segments raises supplier power significantly, increasing schedule risk and input cost variability; in 2024 Consigli reported ~28% of revenue tied to projects needing such specialists.

- 10–15 specialist firms dominate niche work

- Price premium 12–20% vs. standard subs

- Consigli ~28% 2024 revenue exposure

- Higher schedule and cost volatility

Energy and Logistics Costs

Suppliers of transport and heavy machinery face rising energy prices—US industrial diesel rose 14% in 2025 YTD—and new carbon taxes (eg, $35/ton in several states) that they pass to construction managers like Consigli, shrinking margins.

Consigli has limited pushback: specialized urban logistics and last-mile crane moves increase per-job premiums by ~8–12%, so suppliers hold clear pricing power.

- Diesel +14% 2025 YTD

- Carbon tax ≈ $35/ton in some states

- Urban logistics premium 8–12%

- Costs largely passed to Consigli

Supplier leverage squeezes margins: labor, materials and specialist premiums bite

Suppliers hold strong leverage: skilled-trades shortage (11% below 2019) and wage premiums +9% force pay increases; certified materials (steel +22%, timber +18% 2020–25) and BIM vendors (global BIM $9.9B in 2024) narrow options; Consigli precontracts 40% tonnage but supplier-driven margin squeeze ~1–2ppt; specialist subs (10–15 firms) charge +12–20% and cover ~28% revenue.

| Metric | Value |

|---|---|

| Skilled-trades gap | -11% vs 2019 |

| Wage premium | +9% YoY |

| Steel price rise | +22% (2020–25) |

| Precontracting | 40% tonnage 2024 |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, and entry/exit barriers specific to Consigli Construction, highlighting disruptive threats, substitutes, and strategic levers that affect its pricing, profitability, and market positioning.

Concise five-forces snapshot tailored to Consigli Construction—instantly highlights competitive pressures and buyer/supplier risks to speed strategic decisions and bid planning.

Customers Bargaining Power

High Concentration of Institutional Clients

Consigli’s primary clients are large universities, healthcare systems, and government agencies that manage multi-billion-dollar capital budgets; for example, US public university construction spending topped $38B in 2024, concentrating demand. These sophisticated buyers have procurement teams that push down management fees—industry reports show margin pressure of 150–300 basis points on construction management contracts. Because contracts are high-value and multi-year, clients extract strict performance guarantees and favorable terms, raising switching costs and bargaining leverage.

Rigorous Competitive Bidding Processes

Public and institutional tendering forces Consigli into transparent, regulated bids where clients compare cost breakdowns and technical offers; in 2024 U.S. public construction procurements totaled about $420B, raising price sensitivity.

Low Switching Costs at Project Initiation

Before contract signing institutional clients face low switching costs between major construction managers, and with ~70% of US public projects solicited competitively in 2024, clients can pick firms that match budget or net-zero targets; because many firms offer similar preconstruction and management services, Consigli must lean on reputation, technical niches, and specialty credentials—like its LEED/SBE track record—to defend margins and win roughly 15–25% higher-fee projects.

Demand for Sustainable and Net-Zero Building

Information Symmetry and Consultant Usage

Clients commonly hire independent owner representatives and project consultants with sector benchmarks; a 2024 FMI survey found 62% of owners use third-party project controls, cutting builders’ informational edge.

That expertise narrows the information gap, limiting Consigli Construction’s ability to extract margin via unseen cost lines and scope changes.

Consultants equip clients to negotiate from data—cost models, RFP comparatives, and earned value metrics—throughout delivery, raising price pressure and contract scrutiny.

- 62% of owners use third-party project controls (FMI 2024)

- Consultants provide cost benchmarks and earned-value metrics

- Reduced information asymmetry compresses builder margins

Public RFPs, ESG Mandates & 3rd‑Party Controls Squeeze CM Fees and Raise Capex

Large, sophisticated institutional clients (universities, healthcare, government) exert strong bargaining power via regulated competitive RFPs (≈70% of public projects, 2024) and require ESG/net-zero (60%+ RFPs by 2025), compressing CM fees by 150–300 bps and forcing 3–7% design premiums and $2–5M capex per large project; third‑party controls (62% owners, FMI 2024) further cut information asymmetry.

| Metric | Value |

|---|---|

| Public competitive projects (2024) | ≈70% |

| Public procurement total (2024) | $420B |

| Fee margin pressure | 150–300 bps |

| Net‑zero RFPs (by 2025) | 60%+ |

| Design/premium cost | 3–7% |

| Capex per large project | $2–5M |

| Owners using 3rd‑party controls (FMI 2024) | 62% |

What You See Is What You Get

Consigli Construction Porter's Five Forces Analysis

This preview shows the exact Consigli Construction Porter’s Five Forces Analysis you’ll receive immediately after purchase—no placeholders, no drafts; the document is fully formatted, professionally written, and ready for download and use the moment you buy.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Consigli Construction faces moderate buyer power, intense rivalry in regional markets, and supplier influence driven by subcontractor availability and material costs; regulatory and project-scale barriers keep new entrants manageable but technology and substitutes (modular construction) pose rising threats. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Consigli’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Labor Shortages

The late-2025 shortage of skilled trades—MEP (mechanical, electrical, plumbing) workers—remains acute, with US Bureau of Labor Statistics data showing 11% fewer qualified journeymen in construction specialties versus 2019 and sector wage premiums up 9% year-over-year; that scarcity gives unions and niche subcontractors strong bargaining power over Consigli on pay and sequencing, so Consigli must nurture preferred-partner agreements and pay premiums to avoid schedule slippage and cost overruns.

Volatility in Raw Material Costs

Global supply chain disruptions and geopolitical shifts pushed structural steel prices up ~22% and softwood timber up ~18% between 2020–2025, keeping costs volatile into 2025.

Low substitute availability for high-spec institutional projects gives suppliers pricing power, especially for certified steel and CLT (cross-laminated timber).

Consigli reduces exposure via early procurement and bulk buys—over 40% of 2024 large-project tonnage was pre-contracted—but supplier leverage still compresses margins by an estimated 1–2 percentage points.

Technological Integration Requirements

Suppliers of Building Information Modeling software and green-tech hold strong leverage over Consigli because their products are specialized and few vendors meet industry BIM certification and LEED/ILFI sustainable-material standards; global BIM market grew 12.6% in 2024 to $9.9B, concentrating vendor power.

Consigli’s 2025 sustainability targets raise reliance on certified low-carbon materials—only ~15% of US suppliers meet stringent carbon-reporting standards—so supplier options shrink and negotiation power rises.

High switching costs for integrated tech and supply chains—often >$1M per large project in rework and retraining—lock Consigli to vendors, further empowering suppliers.

Subcontractor Concentration in Niche Markets

In academic and cultural projects, roughly 10–15 specialist subcontractors dominate complex historical renovations and high-tech lab fit-outs, allowing them to command premiums of 12–20% above standard rates and to pick projects selectively.

Consigli’s dependence on this elite tier for core segments raises supplier power significantly, increasing schedule risk and input cost variability; in 2024 Consigli reported ~28% of revenue tied to projects needing such specialists.

- 10–15 specialist firms dominate niche work

- Price premium 12–20% vs. standard subs

- Consigli ~28% 2024 revenue exposure

- Higher schedule and cost volatility

Energy and Logistics Costs

Suppliers of transport and heavy machinery face rising energy prices—US industrial diesel rose 14% in 2025 YTD—and new carbon taxes (eg, $35/ton in several states) that they pass to construction managers like Consigli, shrinking margins.

Consigli has limited pushback: specialized urban logistics and last-mile crane moves increase per-job premiums by ~8–12%, so suppliers hold clear pricing power.

- Diesel +14% 2025 YTD

- Carbon tax ≈ $35/ton in some states

- Urban logistics premium 8–12%

- Costs largely passed to Consigli

Supplier leverage squeezes margins: labor, materials and specialist premiums bite

Suppliers hold strong leverage: skilled-trades shortage (11% below 2019) and wage premiums +9% force pay increases; certified materials (steel +22%, timber +18% 2020–25) and BIM vendors (global BIM $9.9B in 2024) narrow options; Consigli precontracts 40% tonnage but supplier-driven margin squeeze ~1–2ppt; specialist subs (10–15 firms) charge +12–20% and cover ~28% revenue.

| Metric | Value |

|---|---|

| Skilled-trades gap | -11% vs 2019 |

| Wage premium | +9% YoY |

| Steel price rise | +22% (2020–25) |

| Precontracting | 40% tonnage 2024 |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, and entry/exit barriers specific to Consigli Construction, highlighting disruptive threats, substitutes, and strategic levers that affect its pricing, profitability, and market positioning.

Concise five-forces snapshot tailored to Consigli Construction—instantly highlights competitive pressures and buyer/supplier risks to speed strategic decisions and bid planning.

Customers Bargaining Power

High Concentration of Institutional Clients

Consigli’s primary clients are large universities, healthcare systems, and government agencies that manage multi-billion-dollar capital budgets; for example, US public university construction spending topped $38B in 2024, concentrating demand. These sophisticated buyers have procurement teams that push down management fees—industry reports show margin pressure of 150–300 basis points on construction management contracts. Because contracts are high-value and multi-year, clients extract strict performance guarantees and favorable terms, raising switching costs and bargaining leverage.

Rigorous Competitive Bidding Processes

Public and institutional tendering forces Consigli into transparent, regulated bids where clients compare cost breakdowns and technical offers; in 2024 U.S. public construction procurements totaled about $420B, raising price sensitivity.

Low Switching Costs at Project Initiation

Before contract signing institutional clients face low switching costs between major construction managers, and with ~70% of US public projects solicited competitively in 2024, clients can pick firms that match budget or net-zero targets; because many firms offer similar preconstruction and management services, Consigli must lean on reputation, technical niches, and specialty credentials—like its LEED/SBE track record—to defend margins and win roughly 15–25% higher-fee projects.

Demand for Sustainable and Net-Zero Building

Information Symmetry and Consultant Usage

Clients commonly hire independent owner representatives and project consultants with sector benchmarks; a 2024 FMI survey found 62% of owners use third-party project controls, cutting builders’ informational edge.

That expertise narrows the information gap, limiting Consigli Construction’s ability to extract margin via unseen cost lines and scope changes.

Consultants equip clients to negotiate from data—cost models, RFP comparatives, and earned value metrics—throughout delivery, raising price pressure and contract scrutiny.

- 62% of owners use third-party project controls (FMI 2024)

- Consultants provide cost benchmarks and earned-value metrics

- Reduced information asymmetry compresses builder margins

Public RFPs, ESG Mandates & 3rd‑Party Controls Squeeze CM Fees and Raise Capex

Large, sophisticated institutional clients (universities, healthcare, government) exert strong bargaining power via regulated competitive RFPs (≈70% of public projects, 2024) and require ESG/net-zero (60%+ RFPs by 2025), compressing CM fees by 150–300 bps and forcing 3–7% design premiums and $2–5M capex per large project; third‑party controls (62% owners, FMI 2024) further cut information asymmetry.

| Metric | Value |

|---|---|

| Public competitive projects (2024) | ≈70% |

| Public procurement total (2024) | $420B |

| Fee margin pressure | 150–300 bps |

| Net‑zero RFPs (by 2025) | 60%+ |

| Design/premium cost | 3–7% |

| Capex per large project | $2–5M |

| Owners using 3rd‑party controls (FMI 2024) | 62% |

What You See Is What You Get

Consigli Construction Porter's Five Forces Analysis

This preview shows the exact Consigli Construction Porter’s Five Forces Analysis you’ll receive immediately after purchase—no placeholders, no drafts; the document is fully formatted, professionally written, and ready for download and use the moment you buy.