Consigli Construction PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Explore how political shifts, economic cycles, and evolving tech trends are reshaping Consigli Construction’s competitive landscape—our PESTLE distills these forces into actionable insight. Ideal for investors, strategists, and consultants, the full report delivers a detailed risk-opportunity map and ready-to-use recommendations. Purchase the complete analysis to unlock the data-driven guidance you need now.

Political factors

Federal infrastructure funding

The continued rollout of the Infrastructure Investment and Jobs Act (IIJA) ensures an estimated $550 billion in new infrastructure spending through 2025, creating a stable pipeline of public works; Consigli captures portions via state-level institutional and academic projects, with higher-education capital outlays up 12% in 2024-25 in key Northeast markets. This federal commitment bolsters long-term contract stability even as private-sector construction activity fluctuates.

State budget allocations

State budget allocations in Massachusetts and New York directly affect Consigli’s pipeline: Massachusetts capital spending hit $9.8bn in FY2024 while New York committed $12.5bn to capital projects, with higher education and healthcare making up ~28% of those totals; cuts or reallocations to public university and state-run hospital funding would reduce preconstruction opportunities, so aligning bids with each state’s 5-year capital improvement plans is critical to sustain regional market share.

Trade and tariff policies

Ongoing US-China trade tensions and 2024 tariff adjustments on steel/aluminum have driven import price swings up to 18%, increasing material cost risk on Consigli’s large projects; flexible procurement and secondary sourcing cut exposure, with contingency line items of 3–5% commonly applied. Political shifts in trade agreements demand real-time supplier re-evaluation to protect margins and ensure accurate budgeting for institutional clients.

Public-private partnerships expansion

Public-private partnerships (PPPs) are rising as governments redirect constrained capital: U.S. federal and municipal PPPs grew to $18.6B in 2024 for infrastructure projects, with life-science campus deals up 22% year-over-year.

Consigli’s political navigation and prior PPP track record position it to win high-profile urban and life-science hub contracts that require multi-year municipal commitments and stakeholder alignment.

PPPs demand rigorous regulatory compliance—procurement, bond financing, and long-term performance guarantees—adding execution risk but higher-margin, stable revenue streams.

- 2024 U.S. PPP market: $18.6B

- Life-science PPP deals +22% YoY

- Advantages: political navigation, track record

- Risks: regulatory oversight, long-term municipal commitment

Geopolitical supply chain stability

- Lead time up 18% (2024)

- Cost increase ~12% (2024)

- Schedule buffers 6–10 weeks

- Single-source exposure cut 34% → 22% (by 2025)

Consigli Poised for Public & Higher‑Ed Build Surge Amid IIJA, PPP Growth and Material Pressure

Federal IIJA funds (~$550B through 2025) and state capital (MA $9.8B FY2024, NY $12.5B) sustain Consigli’s public pipeline; higher-education spend +12% in 2024-25 in Northeast boosts bid opportunities. Trade tariffs pushed steel/aluminum import costs +~18% and material costs ~+12% in 2024, prompting 3–5% contingency lines. U.S. PPPs $18.6B (2024) and life-science PPPs +22% YoY favor Consigli’s track record but add regulatory/long-term risk.

| Metric | 2024/25 |

|---|---|

| IIJA funding | $550B (through 2025) |

| MA capital | $9.8B FY2024 |

| NY capital | $12.5B |

| Higher-ed spend change | +12% (2024-25) |

| PPP market | $18.6B (2024) |

| Life-science PPPs | +22% YoY |

| Import cost swings | Steel/Al ±18%; materials +12% (2024) |

| Contingency | 3–5% |

What is included in the product

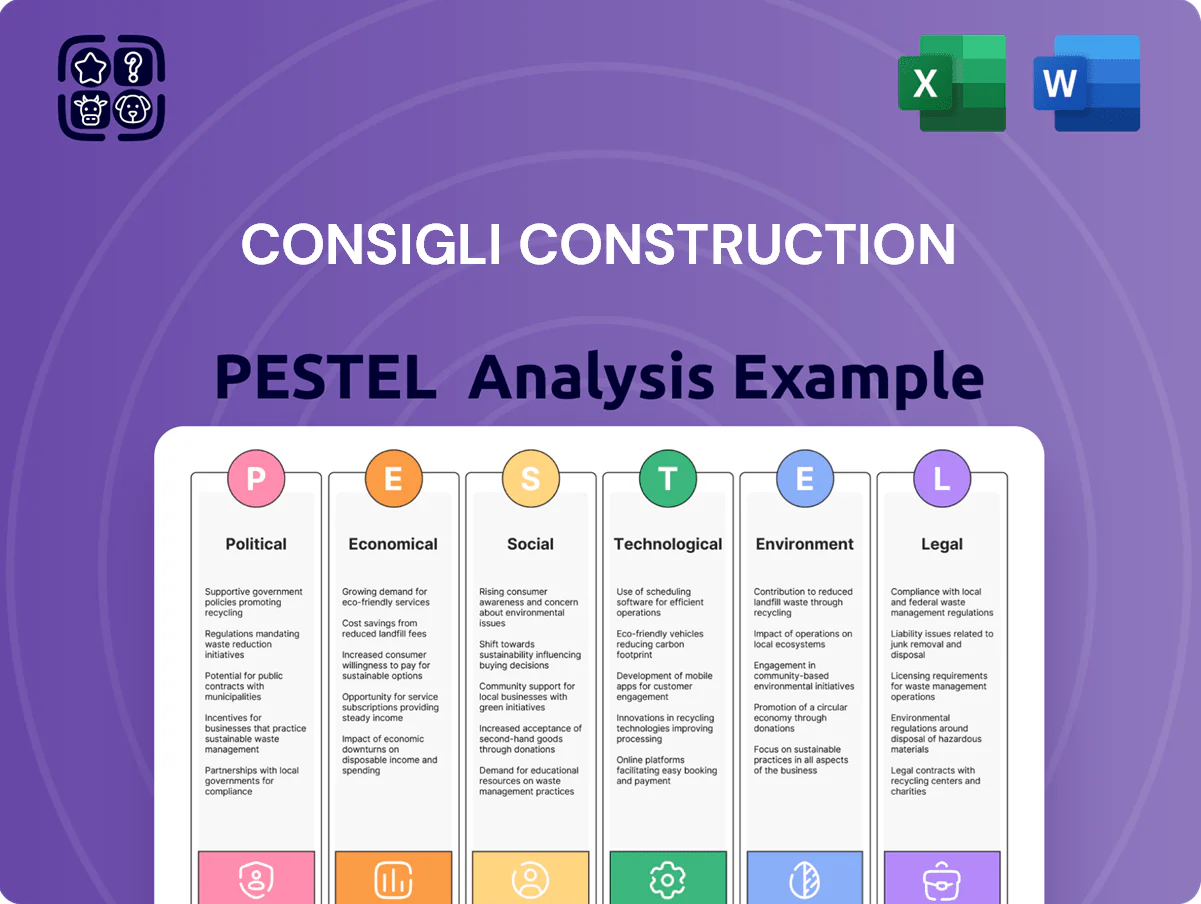

Explores how macro-environmental forces uniquely impact Consigli Construction across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to identify risks and opportunities for executives, consultants, and investors.

A concise, visually segmented PESTLE summary tailored for Consigli Construction that streamlines meeting prep, supports quick risk discussions, and can be dropped into presentations or shared across teams for fast alignment.

Economic factors

Interest rate environment

The cost of capital at end-2025 remains a primary driver for private institutional and life-science developments; average 10-year Treasury yields near 4.3% and BBB corporate spreads ~150bps have pushed effective borrowing costs higher. High interest rates have prompted some private developers to pause or scale back projects—commercial construction starts fell 12% YoY in 2024. Publicly funded work is less rate-sensitive, but Consigli’s backlog depends on the Federal Reserve successfully lowering inflation from 3.4% (2024) without triggering a severe slowdown in construction activity.

Labor market constraints

A persistent shortage of skilled tradespeople has pushed US construction wages up 5.8% year-over-year in 2024, raising project labor costs and delaying schedules; Consigli counters by investing in apprenticeship programs and training to expand its bench.

Strong subcontractor partnerships and preferred-vendor agreements give Consigli more reliable labor access amid 8%-plus industry-wide labor demand growth, helping stabilize staffing for critical projects.

With labor costs compressing margins, Consigli prioritizes efficiency, retention and productivity initiatives—reducing turnover and protecting project EBITDA in a tight market.

Material price volatility

While extreme spikes have eased since 2021–2022, specialized material costs remain ~18–25% above pre‑pandemic averages; Consigli uses preconstruction estimating and hedging tools to lock prices on ~60–70% of major line items, reducing exposure to monthly steel and timber swings of 5–8%. Accurate forecasting—driven by SKU‑level cost models and supplier index tracking—is essential to protect margins on fixed‑price contracts.

Life sciences sector growth

The life sciences and biotech sectors in hubs like Boston and New York remain strong revenue drivers, with Greater Boston attracting over 10 billion USD in annual biotech venture funding in 2024 and NYC seeing a 15% lab space absorption growth year-over-year through 2024.

Demand for specialized lab and research facilities shows resilience versus broader commercial real estate headwinds, supporting higher-margin, long-term projects for builders like Consigli.

Consigli’s specialized expertise positions it to secure high-value contracts in this niche that are less sensitive to general economic downturns, capturing premium rates and multi-year engagements.

- 2024 Greater Boston biotech funding: >10B USD

- NYC lab space absorption growth 2024: +15% YoY

- Specialized lab projects: higher margins, longer timelines

Inflationary impact on overhead

General inflation in 2024—CPI up about 3.4% year-over-year through Q3—pushes Consigli’s material and internal operating costs higher, with insurance premiums rising ~12% and fuel up ~15% in 2023–24, increasing project overhead.

Higher tech and subcontractor costs force tighter margins; optimizing workflows and procurement is critical to sustain competitive bids amid input-cost inflation.

Managing these overhead pressures is essential to preserve EBITDA margins and support long-term growth and balance-sheet resilience.

- 2024 CPI +3.4% YoY

- Insurance +~12% (2023–24)

- Fuel +~15% (2023–24)

- Focus: process optimization, procurement leverage

Rising costs, tighter demand: Consigli hedges soften labor and materials squeeze

Higher borrowing costs (10y Treasury ~4.3%, BBB spreads ~150bps) and 2024 CPI +3.4% raised effective project costs; construction starts fell 12% YoY in 2024. Labor shortages lifted wages +5.8% YoY and industry demand +8%, while specialty material prices remain ~18–25% above pre‑pandemic levels. Consigli mitigates via apprenticeships, preconstruction price locks (60–70% coverage) and supplier hedges.

| Metric | 2024/2025 |

|---|---|

| 10y Treasury | ~4.3% |

| Construction starts | -12% YoY (2024) |

| Wage growth | +5.8% YoY |

| Material premium | +18–25% vs pre‑pandemic |

| Price lock coverage | 60–70% |

Full Version Awaits

Consigli Construction PESTLE Analysis

The preview shown here is the exact Consigli Construction PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investor review.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Explore how political shifts, economic cycles, and evolving tech trends are reshaping Consigli Construction’s competitive landscape—our PESTLE distills these forces into actionable insight. Ideal for investors, strategists, and consultants, the full report delivers a detailed risk-opportunity map and ready-to-use recommendations. Purchase the complete analysis to unlock the data-driven guidance you need now.

Political factors

Federal infrastructure funding

The continued rollout of the Infrastructure Investment and Jobs Act (IIJA) ensures an estimated $550 billion in new infrastructure spending through 2025, creating a stable pipeline of public works; Consigli captures portions via state-level institutional and academic projects, with higher-education capital outlays up 12% in 2024-25 in key Northeast markets. This federal commitment bolsters long-term contract stability even as private-sector construction activity fluctuates.

State budget allocations

State budget allocations in Massachusetts and New York directly affect Consigli’s pipeline: Massachusetts capital spending hit $9.8bn in FY2024 while New York committed $12.5bn to capital projects, with higher education and healthcare making up ~28% of those totals; cuts or reallocations to public university and state-run hospital funding would reduce preconstruction opportunities, so aligning bids with each state’s 5-year capital improvement plans is critical to sustain regional market share.

Trade and tariff policies

Ongoing US-China trade tensions and 2024 tariff adjustments on steel/aluminum have driven import price swings up to 18%, increasing material cost risk on Consigli’s large projects; flexible procurement and secondary sourcing cut exposure, with contingency line items of 3–5% commonly applied. Political shifts in trade agreements demand real-time supplier re-evaluation to protect margins and ensure accurate budgeting for institutional clients.

Public-private partnerships expansion

Public-private partnerships (PPPs) are rising as governments redirect constrained capital: U.S. federal and municipal PPPs grew to $18.6B in 2024 for infrastructure projects, with life-science campus deals up 22% year-over-year.

Consigli’s political navigation and prior PPP track record position it to win high-profile urban and life-science hub contracts that require multi-year municipal commitments and stakeholder alignment.

PPPs demand rigorous regulatory compliance—procurement, bond financing, and long-term performance guarantees—adding execution risk but higher-margin, stable revenue streams.

- 2024 U.S. PPP market: $18.6B

- Life-science PPP deals +22% YoY

- Advantages: political navigation, track record

- Risks: regulatory oversight, long-term municipal commitment

Geopolitical supply chain stability

- Lead time up 18% (2024)

- Cost increase ~12% (2024)

- Schedule buffers 6–10 weeks

- Single-source exposure cut 34% → 22% (by 2025)

Consigli Poised for Public & Higher‑Ed Build Surge Amid IIJA, PPP Growth and Material Pressure

Federal IIJA funds (~$550B through 2025) and state capital (MA $9.8B FY2024, NY $12.5B) sustain Consigli’s public pipeline; higher-education spend +12% in 2024-25 in Northeast boosts bid opportunities. Trade tariffs pushed steel/aluminum import costs +~18% and material costs ~+12% in 2024, prompting 3–5% contingency lines. U.S. PPPs $18.6B (2024) and life-science PPPs +22% YoY favor Consigli’s track record but add regulatory/long-term risk.

| Metric | 2024/25 |

|---|---|

| IIJA funding | $550B (through 2025) |

| MA capital | $9.8B FY2024 |

| NY capital | $12.5B |

| Higher-ed spend change | +12% (2024-25) |

| PPP market | $18.6B (2024) |

| Life-science PPPs | +22% YoY |

| Import cost swings | Steel/Al ±18%; materials +12% (2024) |

| Contingency | 3–5% |

What is included in the product

Explores how macro-environmental forces uniquely impact Consigli Construction across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-backed trends and region-specific examples to identify risks and opportunities for executives, consultants, and investors.

A concise, visually segmented PESTLE summary tailored for Consigli Construction that streamlines meeting prep, supports quick risk discussions, and can be dropped into presentations or shared across teams for fast alignment.

Economic factors

Interest rate environment

The cost of capital at end-2025 remains a primary driver for private institutional and life-science developments; average 10-year Treasury yields near 4.3% and BBB corporate spreads ~150bps have pushed effective borrowing costs higher. High interest rates have prompted some private developers to pause or scale back projects—commercial construction starts fell 12% YoY in 2024. Publicly funded work is less rate-sensitive, but Consigli’s backlog depends on the Federal Reserve successfully lowering inflation from 3.4% (2024) without triggering a severe slowdown in construction activity.

Labor market constraints

A persistent shortage of skilled tradespeople has pushed US construction wages up 5.8% year-over-year in 2024, raising project labor costs and delaying schedules; Consigli counters by investing in apprenticeship programs and training to expand its bench.

Strong subcontractor partnerships and preferred-vendor agreements give Consigli more reliable labor access amid 8%-plus industry-wide labor demand growth, helping stabilize staffing for critical projects.

With labor costs compressing margins, Consigli prioritizes efficiency, retention and productivity initiatives—reducing turnover and protecting project EBITDA in a tight market.

Material price volatility

While extreme spikes have eased since 2021–2022, specialized material costs remain ~18–25% above pre‑pandemic averages; Consigli uses preconstruction estimating and hedging tools to lock prices on ~60–70% of major line items, reducing exposure to monthly steel and timber swings of 5–8%. Accurate forecasting—driven by SKU‑level cost models and supplier index tracking—is essential to protect margins on fixed‑price contracts.

Life sciences sector growth

The life sciences and biotech sectors in hubs like Boston and New York remain strong revenue drivers, with Greater Boston attracting over 10 billion USD in annual biotech venture funding in 2024 and NYC seeing a 15% lab space absorption growth year-over-year through 2024.

Demand for specialized lab and research facilities shows resilience versus broader commercial real estate headwinds, supporting higher-margin, long-term projects for builders like Consigli.

Consigli’s specialized expertise positions it to secure high-value contracts in this niche that are less sensitive to general economic downturns, capturing premium rates and multi-year engagements.

- 2024 Greater Boston biotech funding: >10B USD

- NYC lab space absorption growth 2024: +15% YoY

- Specialized lab projects: higher margins, longer timelines

Inflationary impact on overhead

General inflation in 2024—CPI up about 3.4% year-over-year through Q3—pushes Consigli’s material and internal operating costs higher, with insurance premiums rising ~12% and fuel up ~15% in 2023–24, increasing project overhead.

Higher tech and subcontractor costs force tighter margins; optimizing workflows and procurement is critical to sustain competitive bids amid input-cost inflation.

Managing these overhead pressures is essential to preserve EBITDA margins and support long-term growth and balance-sheet resilience.

- 2024 CPI +3.4% YoY

- Insurance +~12% (2023–24)

- Fuel +~15% (2023–24)

- Focus: process optimization, procurement leverage

Rising costs, tighter demand: Consigli hedges soften labor and materials squeeze

Higher borrowing costs (10y Treasury ~4.3%, BBB spreads ~150bps) and 2024 CPI +3.4% raised effective project costs; construction starts fell 12% YoY in 2024. Labor shortages lifted wages +5.8% YoY and industry demand +8%, while specialty material prices remain ~18–25% above pre‑pandemic levels. Consigli mitigates via apprenticeships, preconstruction price locks (60–70% coverage) and supplier hedges.

| Metric | 2024/2025 |

|---|---|

| 10y Treasury | ~4.3% |

| Construction starts | -12% YoY (2024) |

| Wage growth | +5.8% YoY |

| Material premium | +18–25% vs pre‑pandemic |

| Price lock coverage | 60–70% |

Full Version Awaits

Consigli Construction PESTLE Analysis

The preview shown here is the exact Consigli Construction PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or investor review.