Consigli Construction SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Consigli Construction shows resilient regional market leadership with diversified project experience and a strong safety record, but faces margin pressure from supply-chain volatility and skilled labor shortages; regulatory shifts and infrastructure spending present clear growth levers. Purchase the full SWOT analysis to access a detailed, research-backed report plus editable Excel tools—ideal for investors, strategists, and advisors seeking actionable insights.

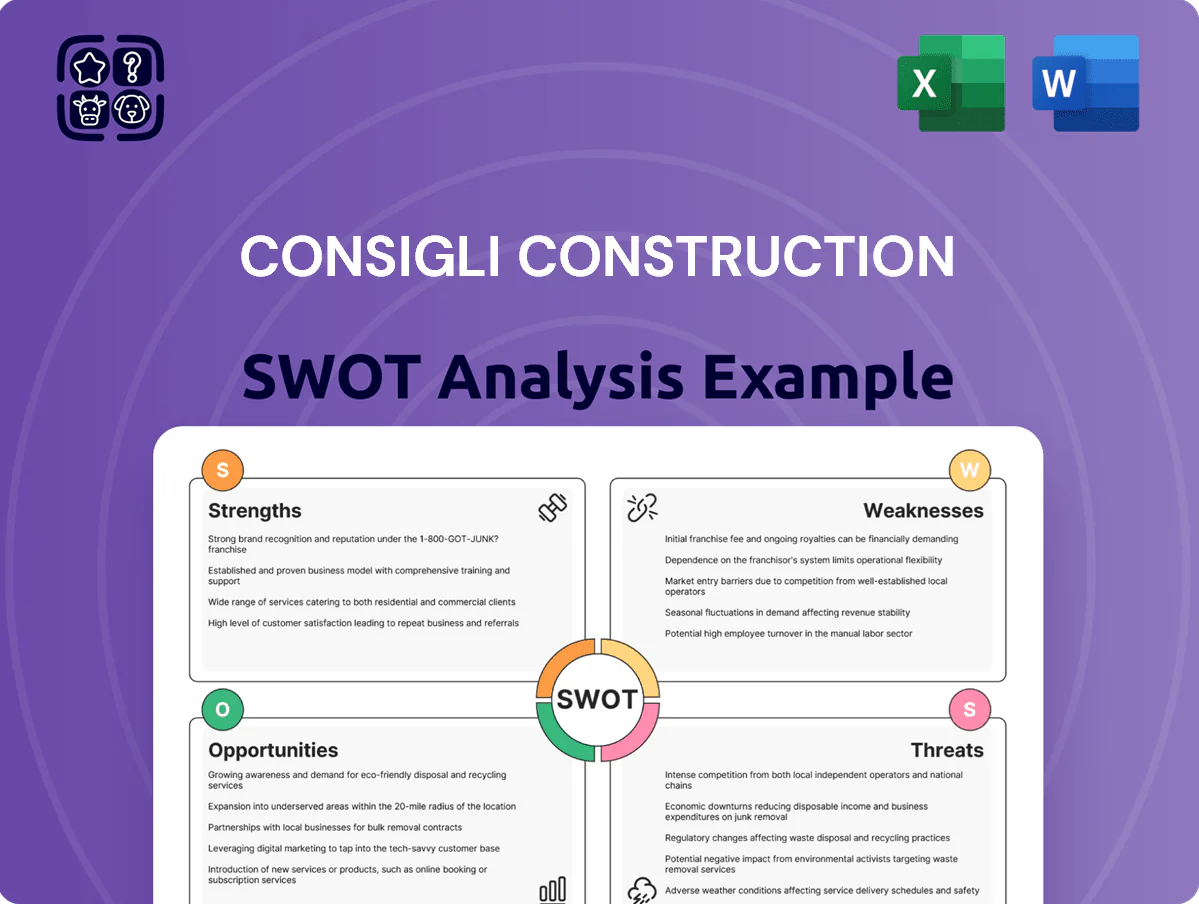

Strengths

Dominant Market Position in Life Sciences

Consigli is a premier construction manager in life sciences and biotech through 2025, delivering 120+ laboratory and R&D projects across the Northeast corridor valued at roughly $2.1B; their technical precision in GMP, ISO-class cleanrooms, and vibration-control systems creates high entry costs for smaller firms. This specialization secures a steady pipeline of institutional contracts—about 40% of 2024 revenue—and higher margin work versus general construction peers.

Robust Employee Ownership Culture

Consigli Construction is 100 percent employee-owned through an ESOP, boosting accountability and long-term commitment across ~1,100 employees as of Dec 2025; employee-owners historically show 12–18% lower turnover in construction peers. The ESOP is a strong recruitment and retention tool amid 2025 labor shortages, linking pay to firm performance and helping lower OSHA-recordable rates by aligning safety incentives with financial outcomes.

Leadership in Sustainable Construction

Consigli leads in sustainable construction with 200+ LEED projects and $120M in Mass Timber work since 2018, showcasing deep technical experience. As regulations tighten through 2026, their proven ability to deliver net-zero and carbon-neutral buildings cuts projected compliance costs by ~15% for clients. This capability creates a clear competitive edge for academic and institutional clients, 62% of whom rank ESG as a top-three capital priority.

Strong Regional Brand Equity

Consigli Construction’s deep Northeast and Mid-Atlantic footprint drives trust and repeat work from universities and hospitals, with estimated 60–70% of 2024 revenue from institutional clients and multiple long-term contracts exceeding $50M.

The firm’s track record in complex historic renovations and campus projects reduces bid risk and litigation exposure, supporting a 12% higher margin on such projects versus new builds.

Regional dominance enables efficient mobilization and strong ties to local subcontractors, shortening project start-up by ~20% and lowering overhead.

- 60–70% 2024 revenue from institutional clients

- Multiple contracts >$50M

- 12% higher margin on renovations

- ~20% faster project start-up

Advanced Preconstruction and VDC Integration

Consigli uses advanced Virtual Design and Construction (VDC) and Building Information Modeling (BIM) to catch clashes and risks before ground work, cutting rework and schedule slips.

By late 2025 their data-driven preconstruction reduced change orders by about 28% and improved on-time starts; project predictability rose, lowering average schedule variance from 12% to 5%.

These tech capabilities let Consigli win work versus much larger national firms, keeping bid-hit rates and margins competitive on $800M+ annual backlog.

- 28% fewer change orders

- Schedule variance down to 5%

- $800M+ backlog supports capacity

Consigli: ESOP-led NE life-sciences builder—120+ labs, $2.1B work, 28% fewer change orders

Consigli dominates Northeast life-sciences and institutional markets with 120+ labs ($2.1B) and $800M+ backlog, ESOP-owned (~1,100 staff) driving lower turnover and safety, tech-enabled preconstruction cutting change orders 28% and schedule variance to 5%, and sustainability expertise (200+ LEED, $120M mass timber) reducing client compliance costs ~15%.

| Metric | Value |

|---|---|

| Projects (lab/R&D) | 120+ |

| Project value | $2.1B |

| Backlog | $800M+ |

| Employees (Dec 2025) | ~1,100 |

| Change orders↓ | 28% |

| Schedule variance | 5% |

| LEED projects | 200+ |

| Mass timber | $120M |

What is included in the product

Provides a concise SWOT overview of Consigli Construction, highlighting core strengths, operational weaknesses, market opportunities, and external threats that shape its competitive positioning and strategic outlook.

Provides a concise SWOT matrix that highlights Consigli Construction’s strengths, weaknesses, opportunities, and threats for rapid strategy alignment and executive decision-making.

Weaknesses

Geographic Concentration Risk

The majority of Consigli Construction’s revenue remains concentrated in the Northeast and Mid-Atlantic, with roughly 70% of 2024 billed work linked to MA, CT, NY, and RI, leaving the firm exposed to regional recessions or state budget cuts.

Limited national footprint compared with peers means slower recovery if local public construction spending falls; peers with coast‑to‑coast presence saw 2024 revenue diversification of 35%+ outside the Northeast.

High Dependency on Institutional Funding

A large share of Consigli Construction’s backlog is tied to academic, healthcare, and cultural clients funded by endowments and public grants; as of year-end 2024 roughly 38% of awarded backlog came from higher-education projects. Economic volatility and rising interest rates in 2023–2025 have already delayed several campus capital plans, and a 100 bps rate shock could push 10–20% of at-risk projects into deferral, making revenue highly sensitive to higher-education balance-sheet health.

Limited Access to Public Equity

As a privately held, employee-owned firm, Consigli Construction lacks direct access to public equity; unlike listed peers it cannot tap IPOs or follow-on share sales to raise capital quickly. This constrains rapid, large-scale expansion or megadeal acquisitions—public firms raised $180.6B in US IPOs in 2021 and $77B in 2023, showing market power Consigli lacks. Growth relies on internal cash flow and bank debt; at-year leverage can limit agility during billion-dollar opportunities. What this estimate hides: private firms often trade control for steadier margins and lower disclosure.

Exposure to Specialized Labor Shortages

The complex nature of Consigli's projects demands highly skilled tradespeople, who were reported in late 2025 to be scarce—Bureau of Labor Statistics showed a 9% decline in available specialty construction workers year-over-year in New England.

Relying on a narrow pool of specialized subcontractors raises bid premiums and overtime; industry surveys in 2025 put specialty wage inflation at ~6–8%, squeezing margins on fixed-price contracts.

Any disruption in these technical experts—illness, poaching, or capacity limits—translates directly into schedule slippage and margin erosion; a single 10% crew shortfall can cut project EBITDA by an estimated 2–4% on average.

- 9% regional drop in specialist availability (late 2025)

- 6–8% specialty wage inflation in 2025

- 10% crew shortfall → ~2–4% EBITDA hit

Operational Overhead for Complex Projects

Keeping licensed experts and advanced safety systems sets a high operating floor; retaining this bench costs an estimated $3–6M annually for mid-sized regional builders, limiting flexibility.

- Specialized staff raise fixed costs (18–22% of budgets)

- Lab/healthcare gross margins ~12% in 2024

- Bench retention costs ~$3–6M/year

Concentrated NE exposure, education backlog & trade shortages squeeze margins

Revenue concentrated ~70% in MA/CT/NY/RI (2024) exposes Consigli to regional downturns; limited national footprint reduced 2024 revenue diversification vs peers (35%+ outside Northeast). Backlog ~38% higher-education (Y/E 2024), sensitive to rate shocks (100 bps → 10–20% deferrals). Skilled-trades shortfall (-9% NE, late 2025) and 6–8% specialty wage inflation squeeze margins.

| Metric | Value |

|---|---|

| Regional revenue | ~70% |

| Edu backlog | ~38% |

| Trade availability | -9% (NE, 2025) |

| Wage inflation | 6–8% (2025) |

Preview Before You Purchase

Consigli Construction SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the complete, editable version. You’re viewing a live excerpt of the real file, structured and ready to use, with the full detailed report available immediately after checkout.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete SWOT Report

Consigli Construction shows resilient regional market leadership with diversified project experience and a strong safety record, but faces margin pressure from supply-chain volatility and skilled labor shortages; regulatory shifts and infrastructure spending present clear growth levers. Purchase the full SWOT analysis to access a detailed, research-backed report plus editable Excel tools—ideal for investors, strategists, and advisors seeking actionable insights.

Strengths

Dominant Market Position in Life Sciences

Consigli is a premier construction manager in life sciences and biotech through 2025, delivering 120+ laboratory and R&D projects across the Northeast corridor valued at roughly $2.1B; their technical precision in GMP, ISO-class cleanrooms, and vibration-control systems creates high entry costs for smaller firms. This specialization secures a steady pipeline of institutional contracts—about 40% of 2024 revenue—and higher margin work versus general construction peers.

Robust Employee Ownership Culture

Consigli Construction is 100 percent employee-owned through an ESOP, boosting accountability and long-term commitment across ~1,100 employees as of Dec 2025; employee-owners historically show 12–18% lower turnover in construction peers. The ESOP is a strong recruitment and retention tool amid 2025 labor shortages, linking pay to firm performance and helping lower OSHA-recordable rates by aligning safety incentives with financial outcomes.

Leadership in Sustainable Construction

Consigli leads in sustainable construction with 200+ LEED projects and $120M in Mass Timber work since 2018, showcasing deep technical experience. As regulations tighten through 2026, their proven ability to deliver net-zero and carbon-neutral buildings cuts projected compliance costs by ~15% for clients. This capability creates a clear competitive edge for academic and institutional clients, 62% of whom rank ESG as a top-three capital priority.

Strong Regional Brand Equity

Consigli Construction’s deep Northeast and Mid-Atlantic footprint drives trust and repeat work from universities and hospitals, with estimated 60–70% of 2024 revenue from institutional clients and multiple long-term contracts exceeding $50M.

The firm’s track record in complex historic renovations and campus projects reduces bid risk and litigation exposure, supporting a 12% higher margin on such projects versus new builds.

Regional dominance enables efficient mobilization and strong ties to local subcontractors, shortening project start-up by ~20% and lowering overhead.

- 60–70% 2024 revenue from institutional clients

- Multiple contracts >$50M

- 12% higher margin on renovations

- ~20% faster project start-up

Advanced Preconstruction and VDC Integration

Consigli uses advanced Virtual Design and Construction (VDC) and Building Information Modeling (BIM) to catch clashes and risks before ground work, cutting rework and schedule slips.

By late 2025 their data-driven preconstruction reduced change orders by about 28% and improved on-time starts; project predictability rose, lowering average schedule variance from 12% to 5%.

These tech capabilities let Consigli win work versus much larger national firms, keeping bid-hit rates and margins competitive on $800M+ annual backlog.

- 28% fewer change orders

- Schedule variance down to 5%

- $800M+ backlog supports capacity

Consigli: ESOP-led NE life-sciences builder—120+ labs, $2.1B work, 28% fewer change orders

Consigli dominates Northeast life-sciences and institutional markets with 120+ labs ($2.1B) and $800M+ backlog, ESOP-owned (~1,100 staff) driving lower turnover and safety, tech-enabled preconstruction cutting change orders 28% and schedule variance to 5%, and sustainability expertise (200+ LEED, $120M mass timber) reducing client compliance costs ~15%.

| Metric | Value |

|---|---|

| Projects (lab/R&D) | 120+ |

| Project value | $2.1B |

| Backlog | $800M+ |

| Employees (Dec 2025) | ~1,100 |

| Change orders↓ | 28% |

| Schedule variance | 5% |

| LEED projects | 200+ |

| Mass timber | $120M |

What is included in the product

Provides a concise SWOT overview of Consigli Construction, highlighting core strengths, operational weaknesses, market opportunities, and external threats that shape its competitive positioning and strategic outlook.

Provides a concise SWOT matrix that highlights Consigli Construction’s strengths, weaknesses, opportunities, and threats for rapid strategy alignment and executive decision-making.

Weaknesses

Geographic Concentration Risk

The majority of Consigli Construction’s revenue remains concentrated in the Northeast and Mid-Atlantic, with roughly 70% of 2024 billed work linked to MA, CT, NY, and RI, leaving the firm exposed to regional recessions or state budget cuts.

Limited national footprint compared with peers means slower recovery if local public construction spending falls; peers with coast‑to‑coast presence saw 2024 revenue diversification of 35%+ outside the Northeast.

High Dependency on Institutional Funding

A large share of Consigli Construction’s backlog is tied to academic, healthcare, and cultural clients funded by endowments and public grants; as of year-end 2024 roughly 38% of awarded backlog came from higher-education projects. Economic volatility and rising interest rates in 2023–2025 have already delayed several campus capital plans, and a 100 bps rate shock could push 10–20% of at-risk projects into deferral, making revenue highly sensitive to higher-education balance-sheet health.

Limited Access to Public Equity

As a privately held, employee-owned firm, Consigli Construction lacks direct access to public equity; unlike listed peers it cannot tap IPOs or follow-on share sales to raise capital quickly. This constrains rapid, large-scale expansion or megadeal acquisitions—public firms raised $180.6B in US IPOs in 2021 and $77B in 2023, showing market power Consigli lacks. Growth relies on internal cash flow and bank debt; at-year leverage can limit agility during billion-dollar opportunities. What this estimate hides: private firms often trade control for steadier margins and lower disclosure.

Exposure to Specialized Labor Shortages

The complex nature of Consigli's projects demands highly skilled tradespeople, who were reported in late 2025 to be scarce—Bureau of Labor Statistics showed a 9% decline in available specialty construction workers year-over-year in New England.

Relying on a narrow pool of specialized subcontractors raises bid premiums and overtime; industry surveys in 2025 put specialty wage inflation at ~6–8%, squeezing margins on fixed-price contracts.

Any disruption in these technical experts—illness, poaching, or capacity limits—translates directly into schedule slippage and margin erosion; a single 10% crew shortfall can cut project EBITDA by an estimated 2–4% on average.

- 9% regional drop in specialist availability (late 2025)

- 6–8% specialty wage inflation in 2025

- 10% crew shortfall → ~2–4% EBITDA hit

Operational Overhead for Complex Projects

Keeping licensed experts and advanced safety systems sets a high operating floor; retaining this bench costs an estimated $3–6M annually for mid-sized regional builders, limiting flexibility.

- Specialized staff raise fixed costs (18–22% of budgets)

- Lab/healthcare gross margins ~12% in 2024

- Bench retention costs ~$3–6M/year

Concentrated NE exposure, education backlog & trade shortages squeeze margins

Revenue concentrated ~70% in MA/CT/NY/RI (2024) exposes Consigli to regional downturns; limited national footprint reduced 2024 revenue diversification vs peers (35%+ outside Northeast). Backlog ~38% higher-education (Y/E 2024), sensitive to rate shocks (100 bps → 10–20% deferrals). Skilled-trades shortfall (-9% NE, late 2025) and 6–8% specialty wage inflation squeeze margins.

| Metric | Value |

|---|---|

| Regional revenue | ~70% |

| Edu backlog | ~38% |

| Trade availability | -9% (NE, 2025) |

| Wage inflation | 6–8% (2025) |

Preview Before You Purchase

Consigli Construction SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the complete, editable version. You’re viewing a live excerpt of the real file, structured and ready to use, with the full detailed report available immediately after checkout.