Contec PESTLE Analysis

Your Shortcut to Market Insight Starts Here

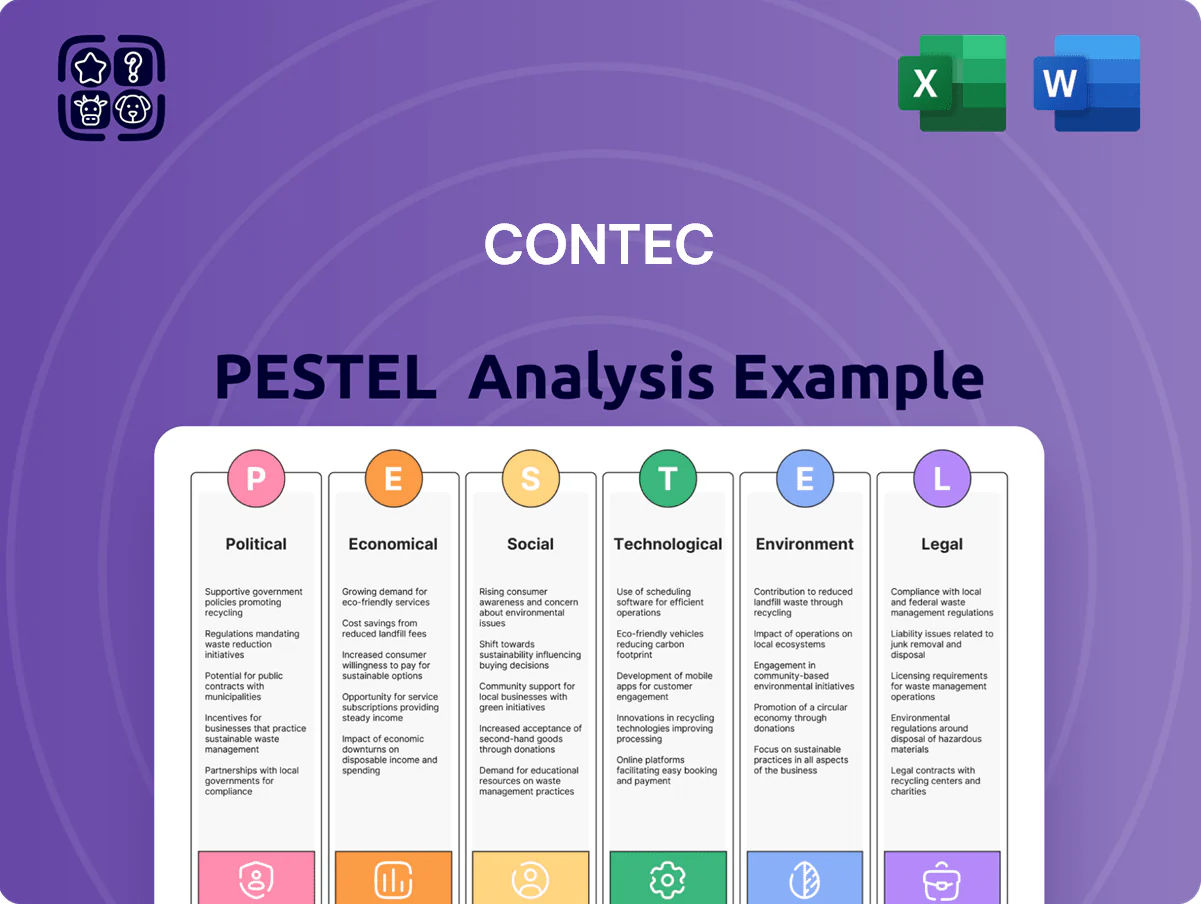

Gain a competitive edge with our focused PESTLE Analysis of Contec—identify the political, economic, social, technological, legal, and environmental forces shaping its future and use these insights to refine your strategy; buy the full report to access detailed, actionable intelligence ready for presentations and decision-making.

Political factors

Global Trade Policy and Export Controls

Contec must navigate escalating export controls: US-China restrictions on advanced semiconductors tightened through 2024, with US Entity List additions up 35% year-over-year and Japan implementing similar curbs, risking supply disruptions for components that account for ~28% of Contec’s BOM in 2024.

Geopolitical tensions could curb sales in China and other Asian markets that represented ~42% of revenues in FY2023–24, forcing management to preserve market access while facing potential licensing delays and denied transfers.

By end-2025, dual-use regulations and sanctions volatility require agile compliance; estimated global licensing approval times rose 22% in 2024, increasing operational and working-capital risks for Contec’s export-dependent production and $45m–$60m annual procurement spend.

Government Subsidies for Digital Transformation

The Japanese government allocated about ¥1.6 trillion (2024 budget) for DX and Society 5.0 programs, boosting subsidies for IoT and factory automation adoption. Contec’s core IoT and FA product lines align with these mandates, positioning the firm to capture public-sector and industrial contracts funded by these grants. Strategic participation in government-funded projects offers Contec a more predictable revenue stream and potential multi-year partnerships with large manufacturers.

Geopolitical Supply Chain Resilience

Political instability has driven a 2024 trend toward friend-shoring and reshoring—global FDI into nearshore manufacturing rose 8% YOY—prompting Contec to reassess supplier locations for critical components to avoid disruption. Contec should map political risk across its suppliers; countries in high-risk categories accounted for 22% of global electronics output in 2023. Diversifying production and partnering with stable jurisdictions can reduce supply interruption probability and protect ~$120m in annual procurement spend.

National Security and Infrastructure Regulations

Governments are tightening hardware security for critical infrastructure; the US Executive Order on Improving the Nation’s Cybersecurity and EU NIS2 push firms to certify devices for energy, transport, and healthcare markets.

Contec must meet evolving certifications—failure risks exclusion from government contracts worth billions (US federal IT procurement exceeded $100bn in 2023) and regulated industrial tenders.

- Stricter standards driven by NIS2 and US directives

- Noncompliance risks loss of share in >$100bn public procurement

- Certifications required for energy, transport, medical sectors

Regional Stability in Manufacturing Hubs

The political climate in Southeast Asia and other manufacturing hubs directly affects Contec’s production costs and logistics; for example, 2024 port slowdowns in Vietnam and Thailand raised lead times by up to 18% and increased regional freight rates ~12% YoY.

Political unrest or sudden labor-law changes can disrupt assembly of industrial PC components and measurement equipment, risking capacity cuts given Contec’s ~40% APAC manufacturing exposure.

Contec must continuously monitor local political developments to anticipate regulatory changes or physical disruptions that could hinder meeting global demand, as 2023–24 supply shocks showed revenue-at-risk scenarios of 5–9%.

- 18% longer lead times (2024 Vietnam/Thailand port issues)

- ~12% rise in regional freight rates YoY

- ~40% of manufacturing in APAC

- 5–9% revenue-at-risk from 2023–24 supply shocks

Export controls threaten 28% BOM and 42% China revenue; APAC shocks risk 5–9%

Escalating export controls and sanctions (US Entity List +35% YoY to 2024) threaten 28% of Contec’s BOM and 42% revenue exposure in China; global licensing delays up 22% in 2024 raise working-capital risk on $45–60m procurement; friend-shoring lifted nearshore FDI +8% YoY, with 22% of electronics output in high-risk countries; APAC manufacturing ~40% of capacity, 5–9% revenue-at-risk from 2023–24 shocks.

| Metric | Value |

|---|---|

| BOM at risk | ~28% |

| Revenue China/APAC | ~42% |

| Entity List growth (to 2024) | +35% YoY |

| Licensing delays | +22% (2024) |

| Procurement spend | $45–60m |

| APAC manufacturing | ~40% |

| Revenue-at-risk | 5–9% |

| Nearshore FDI change | +8% YoY |

What is included in the product

Explores how external macro-environmental factors uniquely affect Contec across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

Provides a clean, summarized PESTLE overview tailored to Contec that’s visually segmented for quick reference in meetings and easily droppable into presentations or planning packs.

Economic factors

Currency Exchange Rate Volatility

Fluctuations in the Japanese Yen—which depreciated about 8% vs the USD in 2024—directly affect Contec’s export competitiveness and import costs for semiconductors and electronic parts. A weaker Yen boosted overseas sales margins in FY2024 but raised import costs by an estimated 5–12% for specialized components. Contec employs FX hedging (covering roughly 60% of exposure) and localized pricing to preserve margins amid currency swings.

Global Capital Expenditure Trends

Contec's revenue correlates with global capex: semiconductor and automotive capex fell ~8% YoY in 2023 but rebounded with a projected 6% growth in 2024–25, impacting demand for industrial PCs and controllers.

High global policy rates—US Fed peak 5.25–5.50% in 2024—constrained 2023 factory automation spending, lowering Contec order volumes by company-reported mid-single digits.

During expansions, industrial upgrade cycles drive strong demand: the global factory automation market, $234.7B in 2023, is forecast to reach $285B by 2026, supporting Contec’s measurement and communication sales growth.

Inflation and Component Pricing

Persistent inflationary pressures into late 2025 have raised energy, labor and specialized electronic component costs by roughly 6–8% year-over-year, squeezing gross margins for industrial computing firms like Contec.

Contec must weigh passing some costs to customers—recent industry average price increases near 4%—against losing share to lower-priced global rivals.

Strengthening supply-chain resilience, securing long-term procurement contracts (locking component prices for 12–24 months) and hedging energy exposure are critical to stabilizing input costs and protecting EBITDA.

Interest Rate Environments

Central bank rate hikes raise borrowing costs for Contec clients, discouraging financing of large automation projects; global policy tightening in 2022–2024 pushed corporate borrowing spreads up—e.g., average OECD policy rates moved from ~0.5% in 2021 to ~3.5% by end-2024, slowing capex on industrial upgrades.

Higher rates typically lengthen Contec’s sales cycles for high-end solutions as clients defer CAPEX; monitoring Fed, ECB and PBOC moves lets Contec adjust sales forecasts and offer financing terms or phased contracts to preserve deal flow.

- OECD policy rates ~3.5% end-2024

- Longer sales cycles for capex-intensive equipment in 2023–24

- Action: align forecasts, offer financing/phased pricing

Emerging Market Growth Opportunities

Economic growth in Southeast Asia and India, with IMF 2025 GDP forecasts of ~5-6% annually and manufacturing growth at 4-7% CAGR, presents a major expansion opportunity for Contec beyond Japan.

Industrialization and smart manufacturing adoption are driving a projected increase in demand for measurement and control equipment—Asia factory automation spending rose ~9% in 2024 to $55–60bn.

Contec's cost-effective, durable solutions tailored to these markets can be a key revenue driver; targeting a 10–15% share in select segments could add tens of millions USD to international sales by 2028.

- IMF 2025 GDP growth: SE Asia/India ~5–6%

- Asia factory automation spend 2024: ~$55–60bn (+9%)

- Target international revenue upside: +$10–50M by 2028 with 10–15% segment share

Yen -8% lifts import costs, boosts export margins; capex rebound and Asia growth support

Yen -8% vs USD (2024) raised import costs 5–12% but improved export margins; FX hedging covers ~60%. Global capex rebounded +6% (2024–25) after -8% (2023), aiding demand. OECD policy rates ~3.5% end-2024 lengthened sales cycles; energy/labor/component inflation +6–8% squeezed margins. SE Asia/India GDP ~5–6% (IMF 2025) supports regional expansion.

| Metric | Value |

|---|---|

| Yen vs USD (2024) | -8% |

| Import cost rise | 5–12% |

| OECD policy rate (end-2024) | ~3.5% |

| Inflation impact | +6–8% |

| SE Asia/India GDP (2025) | ~5–6% |

Preview Before You Purchase

Contec PESTLE Analysis

The preview shown here is the exact Contec PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Shortcut to Market Insight Starts Here

Gain a competitive edge with our focused PESTLE Analysis of Contec—identify the political, economic, social, technological, legal, and environmental forces shaping its future and use these insights to refine your strategy; buy the full report to access detailed, actionable intelligence ready for presentations and decision-making.

Political factors

Global Trade Policy and Export Controls

Contec must navigate escalating export controls: US-China restrictions on advanced semiconductors tightened through 2024, with US Entity List additions up 35% year-over-year and Japan implementing similar curbs, risking supply disruptions for components that account for ~28% of Contec’s BOM in 2024.

Geopolitical tensions could curb sales in China and other Asian markets that represented ~42% of revenues in FY2023–24, forcing management to preserve market access while facing potential licensing delays and denied transfers.

By end-2025, dual-use regulations and sanctions volatility require agile compliance; estimated global licensing approval times rose 22% in 2024, increasing operational and working-capital risks for Contec’s export-dependent production and $45m–$60m annual procurement spend.

Government Subsidies for Digital Transformation

The Japanese government allocated about ¥1.6 trillion (2024 budget) for DX and Society 5.0 programs, boosting subsidies for IoT and factory automation adoption. Contec’s core IoT and FA product lines align with these mandates, positioning the firm to capture public-sector and industrial contracts funded by these grants. Strategic participation in government-funded projects offers Contec a more predictable revenue stream and potential multi-year partnerships with large manufacturers.

Geopolitical Supply Chain Resilience

Political instability has driven a 2024 trend toward friend-shoring and reshoring—global FDI into nearshore manufacturing rose 8% YOY—prompting Contec to reassess supplier locations for critical components to avoid disruption. Contec should map political risk across its suppliers; countries in high-risk categories accounted for 22% of global electronics output in 2023. Diversifying production and partnering with stable jurisdictions can reduce supply interruption probability and protect ~$120m in annual procurement spend.

National Security and Infrastructure Regulations

Governments are tightening hardware security for critical infrastructure; the US Executive Order on Improving the Nation’s Cybersecurity and EU NIS2 push firms to certify devices for energy, transport, and healthcare markets.

Contec must meet evolving certifications—failure risks exclusion from government contracts worth billions (US federal IT procurement exceeded $100bn in 2023) and regulated industrial tenders.

- Stricter standards driven by NIS2 and US directives

- Noncompliance risks loss of share in >$100bn public procurement

- Certifications required for energy, transport, medical sectors

Regional Stability in Manufacturing Hubs

The political climate in Southeast Asia and other manufacturing hubs directly affects Contec’s production costs and logistics; for example, 2024 port slowdowns in Vietnam and Thailand raised lead times by up to 18% and increased regional freight rates ~12% YoY.

Political unrest or sudden labor-law changes can disrupt assembly of industrial PC components and measurement equipment, risking capacity cuts given Contec’s ~40% APAC manufacturing exposure.

Contec must continuously monitor local political developments to anticipate regulatory changes or physical disruptions that could hinder meeting global demand, as 2023–24 supply shocks showed revenue-at-risk scenarios of 5–9%.

- 18% longer lead times (2024 Vietnam/Thailand port issues)

- ~12% rise in regional freight rates YoY

- ~40% of manufacturing in APAC

- 5–9% revenue-at-risk from 2023–24 supply shocks

Export controls threaten 28% BOM and 42% China revenue; APAC shocks risk 5–9%

Escalating export controls and sanctions (US Entity List +35% YoY to 2024) threaten 28% of Contec’s BOM and 42% revenue exposure in China; global licensing delays up 22% in 2024 raise working-capital risk on $45–60m procurement; friend-shoring lifted nearshore FDI +8% YoY, with 22% of electronics output in high-risk countries; APAC manufacturing ~40% of capacity, 5–9% revenue-at-risk from 2023–24 shocks.

| Metric | Value |

|---|---|

| BOM at risk | ~28% |

| Revenue China/APAC | ~42% |

| Entity List growth (to 2024) | +35% YoY |

| Licensing delays | +22% (2024) |

| Procurement spend | $45–60m |

| APAC manufacturing | ~40% |

| Revenue-at-risk | 5–9% |

| Nearshore FDI change | +8% YoY |

What is included in the product

Explores how external macro-environmental factors uniquely affect Contec across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—backed by current data and trends to identify threats and opportunities for executives, consultants, and entrepreneurs.

Provides a clean, summarized PESTLE overview tailored to Contec that’s visually segmented for quick reference in meetings and easily droppable into presentations or planning packs.

Economic factors

Currency Exchange Rate Volatility

Fluctuations in the Japanese Yen—which depreciated about 8% vs the USD in 2024—directly affect Contec’s export competitiveness and import costs for semiconductors and electronic parts. A weaker Yen boosted overseas sales margins in FY2024 but raised import costs by an estimated 5–12% for specialized components. Contec employs FX hedging (covering roughly 60% of exposure) and localized pricing to preserve margins amid currency swings.

Global Capital Expenditure Trends

Contec's revenue correlates with global capex: semiconductor and automotive capex fell ~8% YoY in 2023 but rebounded with a projected 6% growth in 2024–25, impacting demand for industrial PCs and controllers.

High global policy rates—US Fed peak 5.25–5.50% in 2024—constrained 2023 factory automation spending, lowering Contec order volumes by company-reported mid-single digits.

During expansions, industrial upgrade cycles drive strong demand: the global factory automation market, $234.7B in 2023, is forecast to reach $285B by 2026, supporting Contec’s measurement and communication sales growth.

Inflation and Component Pricing

Persistent inflationary pressures into late 2025 have raised energy, labor and specialized electronic component costs by roughly 6–8% year-over-year, squeezing gross margins for industrial computing firms like Contec.

Contec must weigh passing some costs to customers—recent industry average price increases near 4%—against losing share to lower-priced global rivals.

Strengthening supply-chain resilience, securing long-term procurement contracts (locking component prices for 12–24 months) and hedging energy exposure are critical to stabilizing input costs and protecting EBITDA.

Interest Rate Environments

Central bank rate hikes raise borrowing costs for Contec clients, discouraging financing of large automation projects; global policy tightening in 2022–2024 pushed corporate borrowing spreads up—e.g., average OECD policy rates moved from ~0.5% in 2021 to ~3.5% by end-2024, slowing capex on industrial upgrades.

Higher rates typically lengthen Contec’s sales cycles for high-end solutions as clients defer CAPEX; monitoring Fed, ECB and PBOC moves lets Contec adjust sales forecasts and offer financing terms or phased contracts to preserve deal flow.

- OECD policy rates ~3.5% end-2024

- Longer sales cycles for capex-intensive equipment in 2023–24

- Action: align forecasts, offer financing/phased pricing

Emerging Market Growth Opportunities

Economic growth in Southeast Asia and India, with IMF 2025 GDP forecasts of ~5-6% annually and manufacturing growth at 4-7% CAGR, presents a major expansion opportunity for Contec beyond Japan.

Industrialization and smart manufacturing adoption are driving a projected increase in demand for measurement and control equipment—Asia factory automation spending rose ~9% in 2024 to $55–60bn.

Contec's cost-effective, durable solutions tailored to these markets can be a key revenue driver; targeting a 10–15% share in select segments could add tens of millions USD to international sales by 2028.

- IMF 2025 GDP growth: SE Asia/India ~5–6%

- Asia factory automation spend 2024: ~$55–60bn (+9%)

- Target international revenue upside: +$10–50M by 2028 with 10–15% segment share

Yen -8% lifts import costs, boosts export margins; capex rebound and Asia growth support

Yen -8% vs USD (2024) raised import costs 5–12% but improved export margins; FX hedging covers ~60%. Global capex rebounded +6% (2024–25) after -8% (2023), aiding demand. OECD policy rates ~3.5% end-2024 lengthened sales cycles; energy/labor/component inflation +6–8% squeezed margins. SE Asia/India GDP ~5–6% (IMF 2025) supports regional expansion.

| Metric | Value |

|---|---|

| Yen vs USD (2024) | -8% |

| Import cost rise | 5–12% |

| OECD policy rate (end-2024) | ~3.5% |

| Inflation impact | +6–8% |

| SE Asia/India GDP (2025) | ~5–6% |

Preview Before You Purchase

Contec PESTLE Analysis

The preview shown here is the exact Contec PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use.