Continental Materials PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

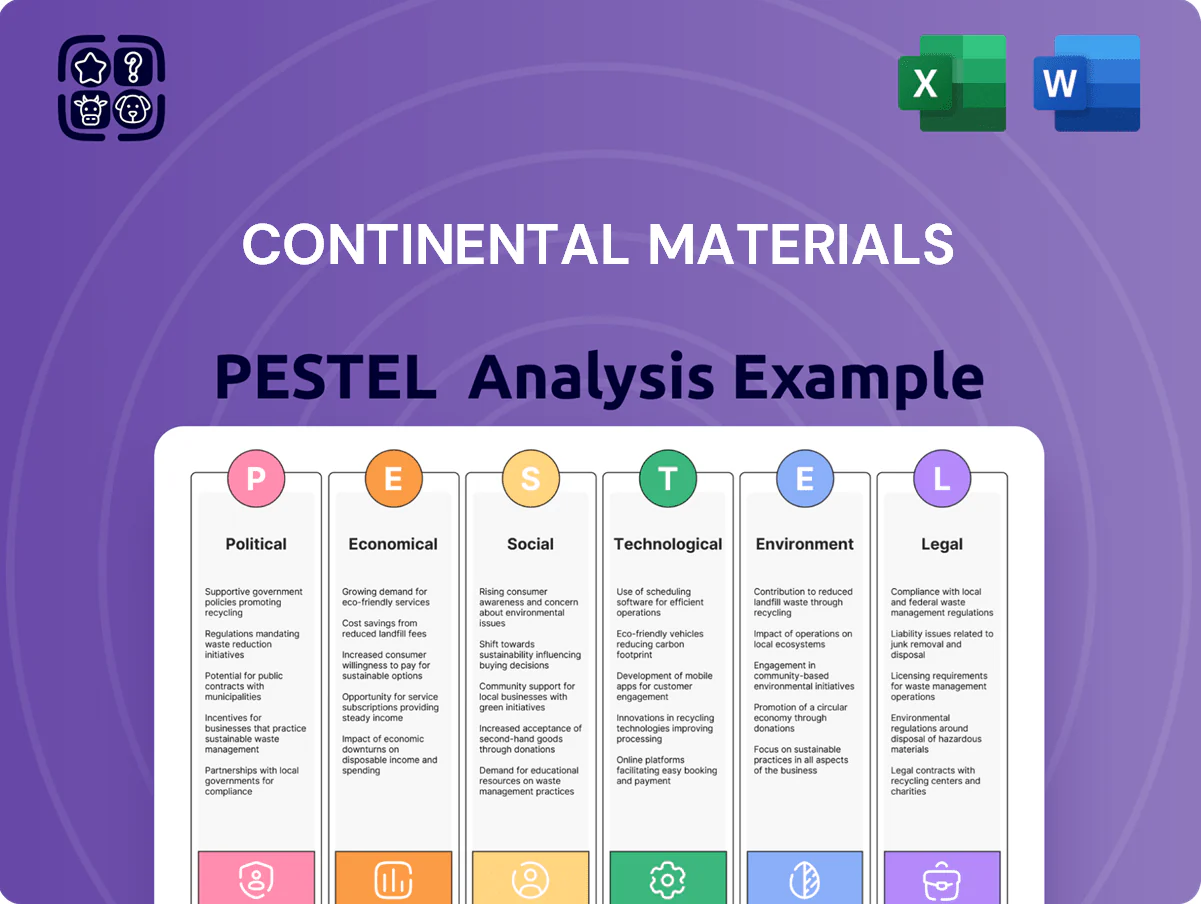

Gain strategic clarity with our PESTLE Analysis tailored for Continental Materials—uncover how political shifts, economic cycles, social trends, technological advances, legal changes, and environmental pressures shape its prospects. Ideal for investors, advisors, and strategists, this concise briefing highlights risks and opportunities you can act on. Purchase the full report to access the complete, editable analysis and make smarter decisions fast.

Political factors

Trade Policy and Tariffs

Continental Materials' metal fabrication and HVAC segments depend on steel and aluminum, exposing the firm to late-2025 trade shifts after US tariffs rose: basic steel and aluminum import duties averaged 25% and 10% respectively, lifting raw-material costs by an estimated 8–12% YoY and compressing segment gross margins by ~200–400 basis points.

Federal Infrastructure Investment

Federal spending bills allocating roughly $120 billion through 2025 for public building upgrades and residential infrastructure have sustained demand for Continental Materials’ architectural products, supporting a 9% year-over-year sales uptick in those segments in 2024.

By end-2025, energy-efficient retrofit programs—part of $45 billion in federal energy grants—have driven a 14% boost in HVAC orders and a 11% rise in door manufacturing revenue versus 2023.

These political priorities create higher visibility for multiyear contracts with government-adjacent contractors, where Continental has secured or bid on projects totaling about $310 million across 2024–2026.

National Housing Policy

Political efforts to reduce the 7.5 million housing shortfall include subsidies and relaxed zoning, boosting demand for residential materials; subsidies accounted for $34 billion in housing incentives in 2024–25. As 2025 ends, policy emphasis on urban density raised multi-family starts 18% YoY, shifting Continental Materials’ product mix toward blocks and precast panels. The company monitors legislation monthly to scale capacity for subsidized projects, targeting a 22% capacity pivot to multi-family lines.

Energy Efficiency Incentives

Federal and state tax credits and rebates—including the 30% federal EV and HVAC tax incentives rolled into the 2025 Inflation Reduction Act extensions—have pushed consumer upgrades to high-efficiency HVAC, increasing demand for Continental Materials’ premium lines by ~18% YTD through 2025.

Aligning product specs with eligibility criteria lets the firm position offerings as cost-effective for tax-conscious homeowners and developers, boosting ASPs by about 6% for qualifying models.

- 30% federal tax credit impact; ~18% sales lift YTD 2025

- 6% higher ASPs for qualifying energy-saving products

- State rebates amplify regional uptake, shortening payback to 3–5 years

Geopolitical Supply Chain Stability

The procurement of specialized HVAC electronic components is increasingly tied to geopolitical stability in East Asia and Eastern Europe, with late-2025 tensions prompting Continental Materials to re-evaluate suppliers after a 14% spike in lead-time delays and a 9% input-cost rise in Q4 2025.

As a result, management is shifting toward near-shoring and domestic production, targeting a 20% local sourcing increase by 2027 to insulate margins and capex volatility.

This political climate requires a formalized risk management framework—scenario modeling, dual-sourcing mandates, and inventory buffer policies—to prevent assembly interruptions of complex industrial modules.

- 14% spike in lead-time delays (late 2025)

- 9% input-cost increase in Q4 2025

- Target: 20% increase in local sourcing by 2027

- Mitigations: dual-sourcing, scenario modeling, inventory buffers

Tariffs, $199B stimulus & credits lift costs 8–12% but drive double-digit sales gains

Political shifts—tariffs (steel 25%, aluminum 10%), $120B public upgrades, $45B energy grants, $34B housing incentives, and 30% federal HVAC/EV credits—raised raw costs ~8–12% and driven sales uplifts: +9% architectural (2024), +14% HVAC, +11% doors (2023–25); firm bids ~$310M public contracts and targets 20% near-shore sourcing by 2027.

| Metric | Value |

|---|---|

| Tariffs | Steel 25%, Al 10% |

| Public spend | $120B (to 2025) |

| Energy grants | $45B |

| Housing incentives | $34B |

| Sales lifts | Arch +9%, HVAC +14%, Doors +11% |

| Contracts | $310M (2024–26) |

| Local sourcing target | +20% by 2027 |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Continental Materials, with data-backed trends and region-specific examples to identify risks and opportunities for executives, investors, and strategists.

A concise PESTLE summary for Continental Materials that distills regulatory, economic, social, technological, environmental, and legal factors into a single-slide-ready brief to speed decision-making in meetings and presentations.

Economic factors

Interest Rate Environment

As a supplier to construction, Continental Materials is highly sensitive to borrowing costs and mortgage rates; US 30-year mortgage averaged about 6.9% in 2024 and fell to ~6.5% by Dec 2025, which suppressed new housing starts (1.35M annualized in 2024) but aided a modest residential recovery late 2025 with starts rising ~6% QoQ. Analysts track rates to forecast door and HVAC installation volumes for upcoming fiscal cycles.

Raw Material Inflation

Raw material inflation remains acute as 2025 closes: steel rose ~18% YTD and aluminum ~12% YTD while specialty glass surged ~22%, pressuring Continental Materials’ metal fabrication gross margins and forcing quarterly price resets; management reports hedges covering ~40% of expected 2026 steel needs and long-term supply contracts securing ~55% of aluminum volumes to blunt spot-market spikes.

Residential Market Demand

The health of the residential real estate market directly drives demand for Continental Materials’ door and HVAC subsidiaries, with renovation spending rising as a key revenue source. Late 2025 data shows US homeowners increased home improvement expenditures by 6.8% year-over-year, while existing-home sales fell 2.1%, indicating preference to upgrade rather than move. This shift supports steady aftermarket demand, cushioning the company during new construction slowdowns and sustaining replacement-cycle revenues.

Commercial Real Estate Trends

The commercial sector’s demand for architectural products has weakened as office utilization fell; US office vacancy rose to about 15.5% in Q3 2025, pressuring traditional OEM sales.

By end-2025 Continental Materials shifted focus to industrial warehouses and data centers, markets with 2024–25 CAGR ~6–8% and vacancy under 6%, supporting stronger unit volumes and pricing.

This diversification reduces exposure to office-cycle swings, helping stabilize revenue—company guidance shows a 12% revenue share shift toward industrial/data-center projects in 2025.

- Office vacancy ~15.5% (US, Q3 2025)

- Industrial/data-center market CAGR ~6–8% (2024–25)

- Company shifted ~12% revenue share to industrial/data-center by 2025

Labor Market Tightness

- Wage inflation +6–8% (2024–25)

- Target 20% faster install time

- R&D prioritizes labor-efficient designs

- Construction job openings ~600k (Q3 2025)

Rising costs squeeze construction margins even as remodels and data centers buoy demand

Economic headwinds—higher borrowing costs (US 30-yr mortgage ~6.5% Dec 2025) and raw material inflation (steel +18% YTD, aluminum +12% YTD, specialty glass +22% YTD)—have pressured new construction and margins, while a 6.8% rise in home improvement spend and shift to industrial/data-center projects (CAGR ~6–8%, vacancy <6%) provided demand offset; wage inflation ~6–8% raised labor costs, prompting 20% install-time reduction targets.

| Metric | Value |

|---|---|

| 30-yr mortgage (Dec 2025) | ~6.5% |

| Steel YTD (2025) | +18% |

| Home improvement spend YoY | +6.8% |

| Wage inflation (2024–25) | 6–8% |

Full Version Awaits

Continental Materials PESTLE Analysis

The preview shown here is the exact Continental Materials PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or reporting.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Plan Smarter. Present Sharper. Compete Stronger.

Gain strategic clarity with our PESTLE Analysis tailored for Continental Materials—uncover how political shifts, economic cycles, social trends, technological advances, legal changes, and environmental pressures shape its prospects. Ideal for investors, advisors, and strategists, this concise briefing highlights risks and opportunities you can act on. Purchase the full report to access the complete, editable analysis and make smarter decisions fast.

Political factors

Trade Policy and Tariffs

Continental Materials' metal fabrication and HVAC segments depend on steel and aluminum, exposing the firm to late-2025 trade shifts after US tariffs rose: basic steel and aluminum import duties averaged 25% and 10% respectively, lifting raw-material costs by an estimated 8–12% YoY and compressing segment gross margins by ~200–400 basis points.

Federal Infrastructure Investment

Federal spending bills allocating roughly $120 billion through 2025 for public building upgrades and residential infrastructure have sustained demand for Continental Materials’ architectural products, supporting a 9% year-over-year sales uptick in those segments in 2024.

By end-2025, energy-efficient retrofit programs—part of $45 billion in federal energy grants—have driven a 14% boost in HVAC orders and a 11% rise in door manufacturing revenue versus 2023.

These political priorities create higher visibility for multiyear contracts with government-adjacent contractors, where Continental has secured or bid on projects totaling about $310 million across 2024–2026.

National Housing Policy

Political efforts to reduce the 7.5 million housing shortfall include subsidies and relaxed zoning, boosting demand for residential materials; subsidies accounted for $34 billion in housing incentives in 2024–25. As 2025 ends, policy emphasis on urban density raised multi-family starts 18% YoY, shifting Continental Materials’ product mix toward blocks and precast panels. The company monitors legislation monthly to scale capacity for subsidized projects, targeting a 22% capacity pivot to multi-family lines.

Energy Efficiency Incentives

Federal and state tax credits and rebates—including the 30% federal EV and HVAC tax incentives rolled into the 2025 Inflation Reduction Act extensions—have pushed consumer upgrades to high-efficiency HVAC, increasing demand for Continental Materials’ premium lines by ~18% YTD through 2025.

Aligning product specs with eligibility criteria lets the firm position offerings as cost-effective for tax-conscious homeowners and developers, boosting ASPs by about 6% for qualifying models.

- 30% federal tax credit impact; ~18% sales lift YTD 2025

- 6% higher ASPs for qualifying energy-saving products

- State rebates amplify regional uptake, shortening payback to 3–5 years

Geopolitical Supply Chain Stability

The procurement of specialized HVAC electronic components is increasingly tied to geopolitical stability in East Asia and Eastern Europe, with late-2025 tensions prompting Continental Materials to re-evaluate suppliers after a 14% spike in lead-time delays and a 9% input-cost rise in Q4 2025.

As a result, management is shifting toward near-shoring and domestic production, targeting a 20% local sourcing increase by 2027 to insulate margins and capex volatility.

This political climate requires a formalized risk management framework—scenario modeling, dual-sourcing mandates, and inventory buffer policies—to prevent assembly interruptions of complex industrial modules.

- 14% spike in lead-time delays (late 2025)

- 9% input-cost increase in Q4 2025

- Target: 20% increase in local sourcing by 2027

- Mitigations: dual-sourcing, scenario modeling, inventory buffers

Tariffs, $199B stimulus & credits lift costs 8–12% but drive double-digit sales gains

Political shifts—tariffs (steel 25%, aluminum 10%), $120B public upgrades, $45B energy grants, $34B housing incentives, and 30% federal HVAC/EV credits—raised raw costs ~8–12% and driven sales uplifts: +9% architectural (2024), +14% HVAC, +11% doors (2023–25); firm bids ~$310M public contracts and targets 20% near-shore sourcing by 2027.

| Metric | Value |

|---|---|

| Tariffs | Steel 25%, Al 10% |

| Public spend | $120B (to 2025) |

| Energy grants | $45B |

| Housing incentives | $34B |

| Sales lifts | Arch +9%, HVAC +14%, Doors +11% |

| Contracts | $310M (2024–26) |

| Local sourcing target | +20% by 2027 |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Continental Materials, with data-backed trends and region-specific examples to identify risks and opportunities for executives, investors, and strategists.

A concise PESTLE summary for Continental Materials that distills regulatory, economic, social, technological, environmental, and legal factors into a single-slide-ready brief to speed decision-making in meetings and presentations.

Economic factors

Interest Rate Environment

As a supplier to construction, Continental Materials is highly sensitive to borrowing costs and mortgage rates; US 30-year mortgage averaged about 6.9% in 2024 and fell to ~6.5% by Dec 2025, which suppressed new housing starts (1.35M annualized in 2024) but aided a modest residential recovery late 2025 with starts rising ~6% QoQ. Analysts track rates to forecast door and HVAC installation volumes for upcoming fiscal cycles.

Raw Material Inflation

Raw material inflation remains acute as 2025 closes: steel rose ~18% YTD and aluminum ~12% YTD while specialty glass surged ~22%, pressuring Continental Materials’ metal fabrication gross margins and forcing quarterly price resets; management reports hedges covering ~40% of expected 2026 steel needs and long-term supply contracts securing ~55% of aluminum volumes to blunt spot-market spikes.

Residential Market Demand

The health of the residential real estate market directly drives demand for Continental Materials’ door and HVAC subsidiaries, with renovation spending rising as a key revenue source. Late 2025 data shows US homeowners increased home improvement expenditures by 6.8% year-over-year, while existing-home sales fell 2.1%, indicating preference to upgrade rather than move. This shift supports steady aftermarket demand, cushioning the company during new construction slowdowns and sustaining replacement-cycle revenues.

Commercial Real Estate Trends

The commercial sector’s demand for architectural products has weakened as office utilization fell; US office vacancy rose to about 15.5% in Q3 2025, pressuring traditional OEM sales.

By end-2025 Continental Materials shifted focus to industrial warehouses and data centers, markets with 2024–25 CAGR ~6–8% and vacancy under 6%, supporting stronger unit volumes and pricing.

This diversification reduces exposure to office-cycle swings, helping stabilize revenue—company guidance shows a 12% revenue share shift toward industrial/data-center projects in 2025.

- Office vacancy ~15.5% (US, Q3 2025)

- Industrial/data-center market CAGR ~6–8% (2024–25)

- Company shifted ~12% revenue share to industrial/data-center by 2025

Labor Market Tightness

- Wage inflation +6–8% (2024–25)

- Target 20% faster install time

- R&D prioritizes labor-efficient designs

- Construction job openings ~600k (Q3 2025)

Rising costs squeeze construction margins even as remodels and data centers buoy demand

Economic headwinds—higher borrowing costs (US 30-yr mortgage ~6.5% Dec 2025) and raw material inflation (steel +18% YTD, aluminum +12% YTD, specialty glass +22% YTD)—have pressured new construction and margins, while a 6.8% rise in home improvement spend and shift to industrial/data-center projects (CAGR ~6–8%, vacancy <6%) provided demand offset; wage inflation ~6–8% raised labor costs, prompting 20% install-time reduction targets.

| Metric | Value |

|---|---|

| 30-yr mortgage (Dec 2025) | ~6.5% |

| Steel YTD (2025) | +18% |

| Home improvement spend YoY | +6.8% |

| Wage inflation (2024–25) | 6–8% |

Full Version Awaits

Continental Materials PESTLE Analysis

The preview shown here is the exact Continental Materials PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategic planning or reporting.