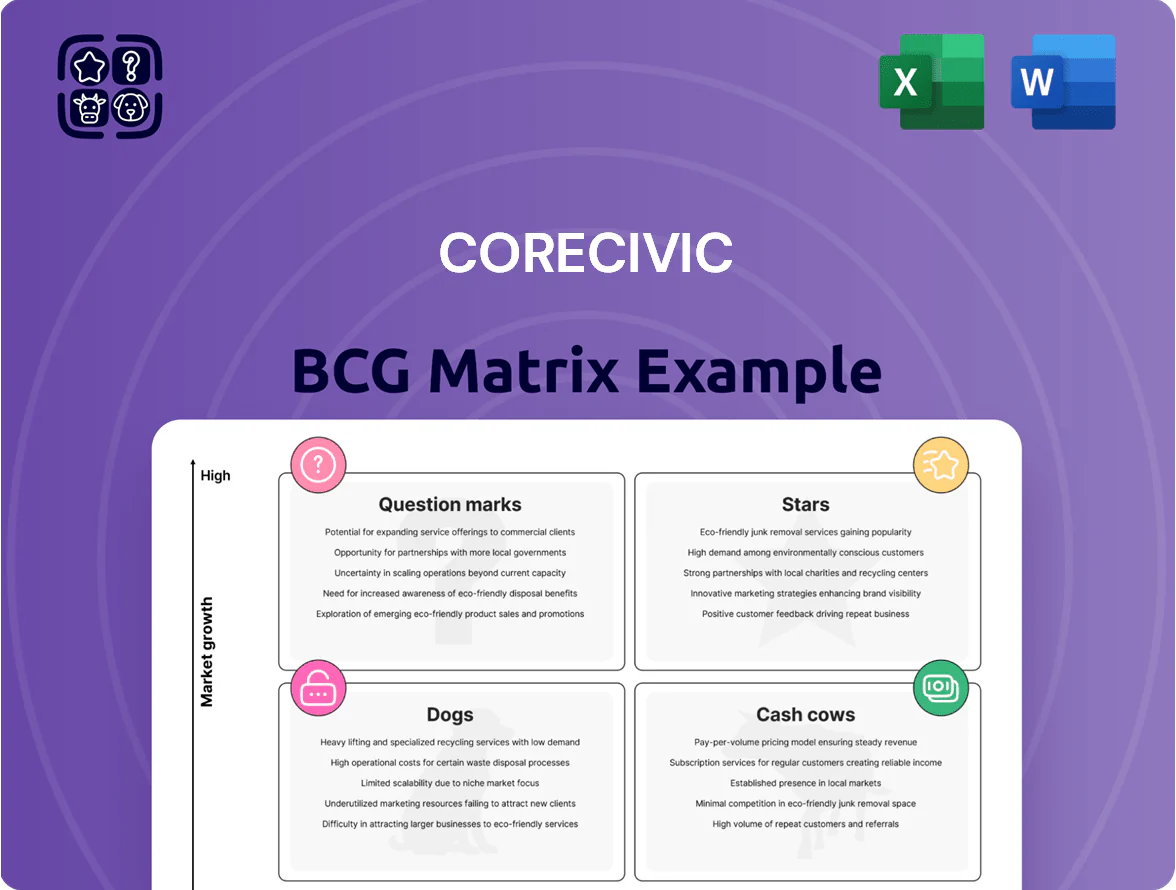

CoreCivic Boston Consulting Group Matrix

Unlock Strategic Clarity

CoreCivic’s BCG Matrix snapshot highlights how its business lines balance market share and growth amid shifting corrections and demand for private corrections services; some units show Cash Cow characteristics while others sit as Question Marks facing regulatory and market volatility. Purchase the full BCG Matrix for a quadrant-by-quadrant breakdown, data-backed recommendations, and a strategic roadmap to optimize capital allocation and operational focus.

Stars

ICE Detention Services

As of late 2025, heightened federal focus on border security drove detention demand up ~18% year-over-year, positioning ICE Detention Services as CoreCivic’s primary cash cow in a high-growth quadrant of the BCG matrix.

CoreCivic held roughly 45%–50% market share of ICE-contracted beds (≈45,000 beds) and recorded detention-related revenue growth near 22% in FY2025, making it the company’s most aggressive revenue engine.

These contracts need heavy operating spend—staffing, healthcare, and security—consuming ~60% of segment margins, but still deliver outsized top-line expansion and strong contract renewal visibility through 2027.

Electronic Monitoring Technology

The shift to community-based supervision has created a $1.8B global market for electronic monitoring (2024 estimate), and CoreCivic has invested ~ $120M since 2021 in ankle-monitor hardware and mobile tracking software to capture share as alternatives to incarceration gain bipartisan support. This unit needs ongoing R&D—CoreCivic allocated 6–8% of the division’s revenue to tech development in 2024—to stay ahead of competitors like BI, Track Group, and GeoCom. Given rising use by 28 US states and projected CAGR ~9% to 2030, the segment shows high potential for long-term dominance but requires steady capex and product updates.

TransCor Logistics Operations

TransCor Logistics Operations is a Star in CoreCivic’s BCG Matrix, owning an estimated 60–70% share of outsourced inmate transport contracts and growing revenue CAGR ~8% from 2019–2025 as interstate detention transfers rose post-2020 policy shifts.

Specialized Behavioral Healthcare

CoreCivic has targeted specialized behavioral healthcare (intensive mental-health and substance-abuse treatment) as a Star: state funding for correctional behavioral programs rose ~18% from 2021–2024, and CoreCivic reports higher-margin contracts, boosting EBITDA margins on specialized units by an estimated 6–10 percentage points versus standard facilities.

The segment differentiates CoreCivic versus public jails through clinical capacity and outcomes, but requires upfront capital and licensed staff—initial staffing and licensure can add 20–30% to per-bed capex and delay ramp by 6–12 months.

- State funding up ~18% (2021–2024)

- EBITDA margin premium ~6–10 pp

- Capex/staffing +20–30% per bed

- Ramp delay 6–12 months

Modernized Flex-Capacity Facilities

Modernized Flex-Capacity Facilities are a high-growth asset class for CoreCivic, driving most new federal wins in 2025 because they offer rapid reconfiguration across security levels and agency needs.

These sites win contracts at higher rates than aging public infrastructure; CoreCivic reported a 28% increase in federal contract awards for modern facilities in 2024–2025, underpinning a competitive edge.

Continued capex is required—CoreCivic planned roughly $150m in 2025 maintenance and upgrade spend—to sustain conversion speed and tech edge, and these assets are the primary drivers of revenue growth in the segment.

- High-growth asset class: modern, reconfigurable sites

- 2024–2025: +28% federal contract awards for modern facilities

- 2025 capex plan: ≈$150m for upgrades

- Primary driver of new contract wins and segment revenue

CoreCivic's Growth Surge: ICE Beds, E‑Monitoring & TransCor Fuel Strong 2025 Momentum

Stars: ICE detention, electronic monitoring, TransCor logistics, specialized behavioral healthcare, and modern flex facilities drive high growth and share; ICE beds ~45k (45–50% share), detention rev +22% FY2025, e-monitoring market $1.8B (2024) with CoreCivic ~$120M investment, TransCor 60–70% share, behavioral care margin +6–10pp, 2025 capex ~$150M.

| Unit | Key metric | 2024–2025 |

|---|---|---|

| ICE detention | Beds ~45,000; share 45–50% | Rev +22% FY2025 |

| Electronic monitoring | Market $1.8B; CoreCivic invest $120M | CAGR ~9% to 2030 |

| TransCor | Contract share 60–70% | Revenue CAGR ~8% (2019–2025) |

| Behavioral healthcare | EBITDA +6–10 pp; state funding +18% | Capex/staff +20–30% per bed |

| Flex facilities | 2024–25 federal wins +28% | 2025 capex ~$150M |

What is included in the product

BCG Matrix analysis of CoreCivic's units: identifies Stars, Cash Cows, Question Marks, Dogs with investment, hold, or divest guidance.

One-page BCG matrix placing CoreCivic units in quadrants for quick C-suite decisions, export-ready for PowerPoint and printable A4/PDF.

Cash Cows

State Correctional Management

The management of long-term state prison contracts is CoreCivic’s steadiest cash cow, with roughly 60–70% occupancy tied to state contracts in 2024 and multi-year deals in Arizona, Georgia, and Tennessee that cut marketing and capex needs. These high-share contracts yield predictable EBITDA margins near 18% for the corrections segment, supporting about $200–300 million annual cash from operations in 2024. That cash flow primarily services CoreCivic’s debt—net leverage was ~4.2x at year-end 2024—and funds investments in reentry and ICE services. The business needs little new infrastructure once beds and staffing are in place, keeping maintenance capex low at under $50 million annually.

CoreCivic Properties Leasing

CoreCivic Properties leases 30+ correctional facilities to government agencies, generating high-margin rental income that accounted for about 18% of CoreCivic’s consolidated revenue in FY2024 (SEC 10-K).

By removing operational risk and staffing costs, the lease model lifted segment EBITDA margins to roughly 65% in 2024, providing steady cash flow and low capex needs.

As a market leader in private correctional real estate, this unit supplies predictable liquidity in a mature market, supporting debt service and shareholder returns in 2024–2025.

USMS Detention Contracts

Contracts with the United States Marshals Service for housing federal detainees waiting trial generate roughly $600–700 million annually for CoreCivic (2024 revenue mix estimate ~25%), offering steady, mature market demand and sustained high occupancy that keeps incremental cost per bed low.

Cash flow from USMS detention is redeployed to community reentry programs—CoreCivic reported $40–55 million in program spending in 2024—funding facility-based services and transitional housing expansion.

Residential Reentry Centers

Residential Reentry Centers (halfway houses) are cash cows for CoreCivic: market-mature, with CoreCivic operating ~60% of US contracted reentry beds as of 2025 and stable occupancy around 85%, yielding steady EBITDA margins near 18% due to low incremental capex.

These services face less political risk than prisons, supporting multi-year contract renewals (avg. 3–5 years) and predictable cash flow, so CoreCivic converts existing infrastructure into reliable, low-growth profits.

- ~60% share of contracted reentry beds (2025)

- 85% average occupancy (2025)

- ~18% EBITDA margin (reentry segment, 2024–2025)

- Avg. contract length 3–5 years

Facility Maintenance Services

Facility Maintenance Services: CoreCivic provides maintenance and facility management for government-owned corrections assets—a low-growth, high-market-share segment that in 2024 contributed steady revenue; CoreCivic reported $1.9B in services and other revenue for FY 2024, with maintenance contracts requiring little capital versus new construction.

These service-only contracts have low overhead and capex, yielding predictable, passive-style cash flows that support margins and free cash flow; CoreCivic generated $151M in free cash flow in FY 2024, helping stabilize financials amid slower facility development.

- Low growth, high share: stable government demand

- Low capex vs new prisons: preserves capital

- Predictable revenue: supports FCF ($151M in 2024)

- Services revenue: $1.9B in FY 2024

CoreCivic: Stable, low‑capex prison contracts drive $151M FCF and ~4.2x net leverage

CoreCivic’s cash cows: state prison contracts, CoreCivic Properties leases, USMS detention, reentry centers, and maintenance services—stable low‑capex cash flow funding debt service (~4.2x net leverage YE2024) and $151M FCF in 2024; key metrics below.

| Item | 2024–25 |

|---|---|

| Net leverage | ~4.2x |

| FCF | $151M |

| Services rev | $1.9B |

| Corrections EBITDA | ~18% |

Delivered as Shown

CoreCivic BCG Matrix

The file you're previewing on this page is the exact CoreCivic BCG Matrix report you'll receive after purchase—no watermarks, no demo content—just a fully formatted, analysis-ready document designed for strategic clarity and professional presentation.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Unlock Strategic Clarity

CoreCivic’s BCG Matrix snapshot highlights how its business lines balance market share and growth amid shifting corrections and demand for private corrections services; some units show Cash Cow characteristics while others sit as Question Marks facing regulatory and market volatility. Purchase the full BCG Matrix for a quadrant-by-quadrant breakdown, data-backed recommendations, and a strategic roadmap to optimize capital allocation and operational focus.

Stars

ICE Detention Services

As of late 2025, heightened federal focus on border security drove detention demand up ~18% year-over-year, positioning ICE Detention Services as CoreCivic’s primary cash cow in a high-growth quadrant of the BCG matrix.

CoreCivic held roughly 45%–50% market share of ICE-contracted beds (≈45,000 beds) and recorded detention-related revenue growth near 22% in FY2025, making it the company’s most aggressive revenue engine.

These contracts need heavy operating spend—staffing, healthcare, and security—consuming ~60% of segment margins, but still deliver outsized top-line expansion and strong contract renewal visibility through 2027.

Electronic Monitoring Technology

The shift to community-based supervision has created a $1.8B global market for electronic monitoring (2024 estimate), and CoreCivic has invested ~ $120M since 2021 in ankle-monitor hardware and mobile tracking software to capture share as alternatives to incarceration gain bipartisan support. This unit needs ongoing R&D—CoreCivic allocated 6–8% of the division’s revenue to tech development in 2024—to stay ahead of competitors like BI, Track Group, and GeoCom. Given rising use by 28 US states and projected CAGR ~9% to 2030, the segment shows high potential for long-term dominance but requires steady capex and product updates.

TransCor Logistics Operations

TransCor Logistics Operations is a Star in CoreCivic’s BCG Matrix, owning an estimated 60–70% share of outsourced inmate transport contracts and growing revenue CAGR ~8% from 2019–2025 as interstate detention transfers rose post-2020 policy shifts.

Specialized Behavioral Healthcare

CoreCivic has targeted specialized behavioral healthcare (intensive mental-health and substance-abuse treatment) as a Star: state funding for correctional behavioral programs rose ~18% from 2021–2024, and CoreCivic reports higher-margin contracts, boosting EBITDA margins on specialized units by an estimated 6–10 percentage points versus standard facilities.

The segment differentiates CoreCivic versus public jails through clinical capacity and outcomes, but requires upfront capital and licensed staff—initial staffing and licensure can add 20–30% to per-bed capex and delay ramp by 6–12 months.

- State funding up ~18% (2021–2024)

- EBITDA margin premium ~6–10 pp

- Capex/staffing +20–30% per bed

- Ramp delay 6–12 months

Modernized Flex-Capacity Facilities

Modernized Flex-Capacity Facilities are a high-growth asset class for CoreCivic, driving most new federal wins in 2025 because they offer rapid reconfiguration across security levels and agency needs.

These sites win contracts at higher rates than aging public infrastructure; CoreCivic reported a 28% increase in federal contract awards for modern facilities in 2024–2025, underpinning a competitive edge.

Continued capex is required—CoreCivic planned roughly $150m in 2025 maintenance and upgrade spend—to sustain conversion speed and tech edge, and these assets are the primary drivers of revenue growth in the segment.

- High-growth asset class: modern, reconfigurable sites

- 2024–2025: +28% federal contract awards for modern facilities

- 2025 capex plan: ≈$150m for upgrades

- Primary driver of new contract wins and segment revenue

CoreCivic's Growth Surge: ICE Beds, E‑Monitoring & TransCor Fuel Strong 2025 Momentum

Stars: ICE detention, electronic monitoring, TransCor logistics, specialized behavioral healthcare, and modern flex facilities drive high growth and share; ICE beds ~45k (45–50% share), detention rev +22% FY2025, e-monitoring market $1.8B (2024) with CoreCivic ~$120M investment, TransCor 60–70% share, behavioral care margin +6–10pp, 2025 capex ~$150M.

| Unit | Key metric | 2024–2025 |

|---|---|---|

| ICE detention | Beds ~45,000; share 45–50% | Rev +22% FY2025 |

| Electronic monitoring | Market $1.8B; CoreCivic invest $120M | CAGR ~9% to 2030 |

| TransCor | Contract share 60–70% | Revenue CAGR ~8% (2019–2025) |

| Behavioral healthcare | EBITDA +6–10 pp; state funding +18% | Capex/staff +20–30% per bed |

| Flex facilities | 2024–25 federal wins +28% | 2025 capex ~$150M |

What is included in the product

BCG Matrix analysis of CoreCivic's units: identifies Stars, Cash Cows, Question Marks, Dogs with investment, hold, or divest guidance.

One-page BCG matrix placing CoreCivic units in quadrants for quick C-suite decisions, export-ready for PowerPoint and printable A4/PDF.

Cash Cows

State Correctional Management

The management of long-term state prison contracts is CoreCivic’s steadiest cash cow, with roughly 60–70% occupancy tied to state contracts in 2024 and multi-year deals in Arizona, Georgia, and Tennessee that cut marketing and capex needs. These high-share contracts yield predictable EBITDA margins near 18% for the corrections segment, supporting about $200–300 million annual cash from operations in 2024. That cash flow primarily services CoreCivic’s debt—net leverage was ~4.2x at year-end 2024—and funds investments in reentry and ICE services. The business needs little new infrastructure once beds and staffing are in place, keeping maintenance capex low at under $50 million annually.

CoreCivic Properties Leasing

CoreCivic Properties leases 30+ correctional facilities to government agencies, generating high-margin rental income that accounted for about 18% of CoreCivic’s consolidated revenue in FY2024 (SEC 10-K).

By removing operational risk and staffing costs, the lease model lifted segment EBITDA margins to roughly 65% in 2024, providing steady cash flow and low capex needs.

As a market leader in private correctional real estate, this unit supplies predictable liquidity in a mature market, supporting debt service and shareholder returns in 2024–2025.

USMS Detention Contracts

Contracts with the United States Marshals Service for housing federal detainees waiting trial generate roughly $600–700 million annually for CoreCivic (2024 revenue mix estimate ~25%), offering steady, mature market demand and sustained high occupancy that keeps incremental cost per bed low.

Cash flow from USMS detention is redeployed to community reentry programs—CoreCivic reported $40–55 million in program spending in 2024—funding facility-based services and transitional housing expansion.

Residential Reentry Centers

Residential Reentry Centers (halfway houses) are cash cows for CoreCivic: market-mature, with CoreCivic operating ~60% of US contracted reentry beds as of 2025 and stable occupancy around 85%, yielding steady EBITDA margins near 18% due to low incremental capex.

These services face less political risk than prisons, supporting multi-year contract renewals (avg. 3–5 years) and predictable cash flow, so CoreCivic converts existing infrastructure into reliable, low-growth profits.

- ~60% share of contracted reentry beds (2025)

- 85% average occupancy (2025)

- ~18% EBITDA margin (reentry segment, 2024–2025)

- Avg. contract length 3–5 years

Facility Maintenance Services

Facility Maintenance Services: CoreCivic provides maintenance and facility management for government-owned corrections assets—a low-growth, high-market-share segment that in 2024 contributed steady revenue; CoreCivic reported $1.9B in services and other revenue for FY 2024, with maintenance contracts requiring little capital versus new construction.

These service-only contracts have low overhead and capex, yielding predictable, passive-style cash flows that support margins and free cash flow; CoreCivic generated $151M in free cash flow in FY 2024, helping stabilize financials amid slower facility development.

- Low growth, high share: stable government demand

- Low capex vs new prisons: preserves capital

- Predictable revenue: supports FCF ($151M in 2024)

- Services revenue: $1.9B in FY 2024

CoreCivic: Stable, low‑capex prison contracts drive $151M FCF and ~4.2x net leverage

CoreCivic’s cash cows: state prison contracts, CoreCivic Properties leases, USMS detention, reentry centers, and maintenance services—stable low‑capex cash flow funding debt service (~4.2x net leverage YE2024) and $151M FCF in 2024; key metrics below.

| Item | 2024–25 |

|---|---|

| Net leverage | ~4.2x |

| FCF | $151M |

| Services rev | $1.9B |

| Corrections EBITDA | ~18% |

Delivered as Shown

CoreCivic BCG Matrix

The file you're previewing on this page is the exact CoreCivic BCG Matrix report you'll receive after purchase—no watermarks, no demo content—just a fully formatted, analysis-ready document designed for strategic clarity and professional presentation.