CoreCivic Porter's Five Forces Analysis

From Overview to Strategy Blueprint

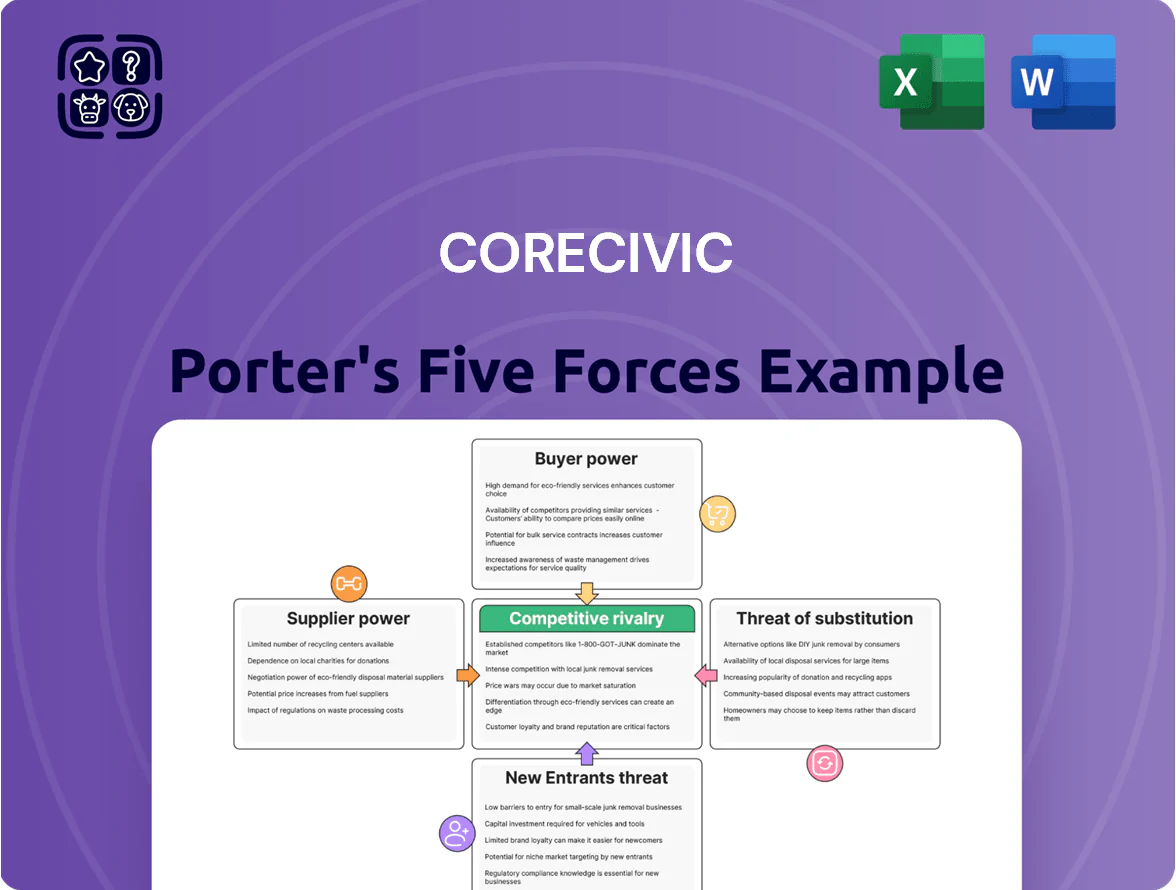

CoreCivic faces concentrated buyer and regulatory power, moderate supplier leverage, high barriers limiting new entrants, and evolving substitute threats from reform and alternatives to incarceration; these dynamics shape margins and strategic flexibility.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore CoreCivic’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Labor and Workforce Retention

CoreCivic’s primary input is a specialized workforce—correctional officers and healthcare staff—whose national turnover hit ~30% in 2024 and remained elevated into late 2025, boosting staff bargaining power.

Tight labor markets raised average starting wages by ~12% year-over-year in 2025 for similar roles, forcing CoreCivic to increase pay and benefits, squeezing operating margins by an estimated 150–250 basis points.

In jurisdictions with unions, ongoing collective bargaining drives higher fixed labor costs and staffing guarantees, adding contract risk and reducing flexibility.

Access to Capital and Financial Services

Financial institutions are key capital suppliers, but ESG-driven divestments since 2019 shrank willing lenders; CoreCivic reported net debt of $1.1 billion as of 2024, and financing options tightened, raising borrowing spreads by an estimated 150–300 basis points versus broader corporate averages.

Specialized Healthcare and Food Services

Third-party inmate healthcare and food services sit in a consolidated market with a few large vendors able to meet federal and state standards, giving suppliers moderate bargaining power over CoreCivic.

CoreCivic depends on specialist clinical staffing and accredited nutrition programs to meet contracts and avoid litigation, so switching costs are high and suppliers can press terms.

In 2025 rising medical supply and pharmaceutical prices—US drug CPI up 6.2% in 2025 year-over-year—further boosted suppliers’ pricing power, increasing CoreCivic’s operating expense risk.

Construction and Facility Maintenance Contractors

CoreCivic relies on a small set of specialized contractors with high-security clearances for expansions and renovations, giving suppliers strong leverage during growth phases.

In 2025, industry-wide material inflation averaged ~7–9%, letting contractors pass cost increases to CoreCivic and pressuring CAPEX; limited vendor competition raises switching costs and schedule risk.

Technology and Surveillance Systems

Suppliers of proprietary electronic security, biometrics, and data systems exert strong bargaining power over CoreCivic due to patent protections and high switching costs; replacing an integrated system can exceed $5m per facility in hardware, software, and downtime. By 2025 CoreCivic’s rollout of AI-driven surveillance raises vendor dependence—AI maintenance and licensing can add 8–12% to annual tech OPEX. This concentration risks price hikes and slower upgrades.

- Proprietary IP: high vendor leverage

- Switching cost: ~$5m per facility

- AI additions: +8–12% annual tech OPEX

- Vendor concentration increases pricing and upgrade risk

Suppliers wield rising pricing and financing power, squeezing margins amid high switching costs

Suppliers hold moderate-to-strong power: labor turnover ~30% in 2024 raised wages ~12% in 2025, squeezing margins 150–250 bps; net debt $1.1B (2024) and ESG-driven lender retreat widened borrowing spreads ~150–300 bps; medical/drug CPI +6.2% (2025) and material inflation 7–9% lifted OPEX/CAPEX; proprietary security systems and cleared contractors create high switching costs (~$5m/facility) and vendor leverage.

| Metric | Value |

|---|---|

| Labor turnover (2024) | ~30% |

| Wage rise (2025) | ~+12% |

| Net debt (2024) | $1.1B |

| Borrowing spread increase | +150–300 bps |

| Drug CPI (2025) | +6.2% |

| Material inflation (2025) | 7–9% |

| Switching cost per facility | ~$5M |

| AI tech OPEX rise | +8–12% |

What is included in the product

Uncovers competitive pressures facing CoreCivic—evaluating rivalry intensity, supplier and buyer power, entry barriers, and substitution risks—highlighting regulatory, contract-dependency, and reputational dynamics that shape pricing and profitability.

A concise Porter's Five Forces one-sheet for CoreCivic—quickly highlights competitive threats, prison service buyer power, regulatory risk, substitution risk, and barriers to entry to speed executive decisions.

Customers Bargaining Power

Concentration of Federal Government Agencies

CoreCivic derives about 70% of 2024 revenue from federal contracts, mainly ICE and U.S. Marshals Service, concentrating buying power in few agencies.

That concentration lets federal buyers set contract terms, cap pricing, and impose strict compliance standards that compress margins and raise operating costs.

If a major agency shifts procurement—e.g., reducing detainee beds or moving in-house—CoreCivic faces severe revenue loss and valuation downside.

Political and Policy Volatility

The bargaining power of customers for CoreCivic shifts with political winds; the 2025 federal emphasis on border security boosted detention demand, while prior administrations sought to phase out private prisons—policies that can cut or not renew contracts regardless of CoreCivic’s 2024 revenue of $1.9B and government-payments making up ~80% of total revenue. This creates high customer leverage tied to ideology, not performance.

State and Local Budgetary Constraints

State and local budget cuts boost customers’ bargaining power: during 2023–2024, 38% of US states reported fiscal stress, pushing many to press CoreCivic for lower per-diem rates or added services to meet tight budgets.

Procurement reviews often force CoreCivic to accept slimmer margins or lose bids to public facilities; a single 10% rate cut can erase typical operating margins of 6–8% on detention contracts.

Contractual Flexibility and Termination Clauses

Government contracts often include termination-for-convenience clauses allowing exits with 30–180 days notice, giving buyers strong leverage during annual reviews and renewals; in 2024 CoreCivic reported 73% of revenue from federal/state contracts, so this risk is material.

CoreCivic frequently funds capital upgrades or operational concessions—company disclosed $120m–$200m annual maintenance/capex range in 2023–24—to retain these long-term agreements.

- Termination notice: 30–180 days

- Revenue tied to contracts: ~73% (2024)

- Annual capex/maintenance: $120m–$200m

Influence of Public Advocacy and Oversight

Government customers, sensitive to public opinion and civil-rights advocacy, can demand stricter oversight and transparency from CoreCivic after high-profile incidents; for example, 2023 DOJ inquiries and state contract reviews followed reports of facility abuses that drew national media attention.

That social pressure lets buyers impose tougher reporting and accountability without higher fees, squeezing margins—CoreCivic reported a 2024 revenue decline of 6% year-over-year, partly from contract renegotiations and loss.

- 2023 DOJ/state probes increased oversight

- 2024 revenue -6% YOY

- Customers can force reporting, audits

- Higher accountability often without higher pay

CoreCivic at Risk: 73% Govt Revenue, Rising Oversight Could Erase 6–8% Margins

CoreCivic faces very high customer bargaining power: ~73% revenue from government contracts (2024 $1.9B), termination-for-convenience 30–180 days, 2024 revenue -6% YOY, annual capex $120–$200m; political shifts and oversight (2023 DOJ probes) can cut contracts or force rate cuts that erase 6–8% operating margins.

| Metric | Value |

|---|---|

| 2024 revenue | $1.9B |

| Govt revenue | ~73% |

| YOY | -6% |

| Capex | $120–$200m |

What You See Is What You Get

CoreCivic Porter's Five Forces Analysis

This preview shows the exact CoreCivic Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders, fully formatted for use.

The document displayed here is the same professionally written file you’ll be able to download and apply the moment you buy, containing detailed force-by-force evaluation and practical implications.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

From Overview to Strategy Blueprint

CoreCivic faces concentrated buyer and regulatory power, moderate supplier leverage, high barriers limiting new entrants, and evolving substitute threats from reform and alternatives to incarceration; these dynamics shape margins and strategic flexibility.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore CoreCivic’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Labor and Workforce Retention

CoreCivic’s primary input is a specialized workforce—correctional officers and healthcare staff—whose national turnover hit ~30% in 2024 and remained elevated into late 2025, boosting staff bargaining power.

Tight labor markets raised average starting wages by ~12% year-over-year in 2025 for similar roles, forcing CoreCivic to increase pay and benefits, squeezing operating margins by an estimated 150–250 basis points.

In jurisdictions with unions, ongoing collective bargaining drives higher fixed labor costs and staffing guarantees, adding contract risk and reducing flexibility.

Access to Capital and Financial Services

Financial institutions are key capital suppliers, but ESG-driven divestments since 2019 shrank willing lenders; CoreCivic reported net debt of $1.1 billion as of 2024, and financing options tightened, raising borrowing spreads by an estimated 150–300 basis points versus broader corporate averages.

Specialized Healthcare and Food Services

Third-party inmate healthcare and food services sit in a consolidated market with a few large vendors able to meet federal and state standards, giving suppliers moderate bargaining power over CoreCivic.

CoreCivic depends on specialist clinical staffing and accredited nutrition programs to meet contracts and avoid litigation, so switching costs are high and suppliers can press terms.

In 2025 rising medical supply and pharmaceutical prices—US drug CPI up 6.2% in 2025 year-over-year—further boosted suppliers’ pricing power, increasing CoreCivic’s operating expense risk.

Construction and Facility Maintenance Contractors

CoreCivic relies on a small set of specialized contractors with high-security clearances for expansions and renovations, giving suppliers strong leverage during growth phases.

In 2025, industry-wide material inflation averaged ~7–9%, letting contractors pass cost increases to CoreCivic and pressuring CAPEX; limited vendor competition raises switching costs and schedule risk.

Technology and Surveillance Systems

Suppliers of proprietary electronic security, biometrics, and data systems exert strong bargaining power over CoreCivic due to patent protections and high switching costs; replacing an integrated system can exceed $5m per facility in hardware, software, and downtime. By 2025 CoreCivic’s rollout of AI-driven surveillance raises vendor dependence—AI maintenance and licensing can add 8–12% to annual tech OPEX. This concentration risks price hikes and slower upgrades.

- Proprietary IP: high vendor leverage

- Switching cost: ~$5m per facility

- AI additions: +8–12% annual tech OPEX

- Vendor concentration increases pricing and upgrade risk

Suppliers wield rising pricing and financing power, squeezing margins amid high switching costs

Suppliers hold moderate-to-strong power: labor turnover ~30% in 2024 raised wages ~12% in 2025, squeezing margins 150–250 bps; net debt $1.1B (2024) and ESG-driven lender retreat widened borrowing spreads ~150–300 bps; medical/drug CPI +6.2% (2025) and material inflation 7–9% lifted OPEX/CAPEX; proprietary security systems and cleared contractors create high switching costs (~$5m/facility) and vendor leverage.

| Metric | Value |

|---|---|

| Labor turnover (2024) | ~30% |

| Wage rise (2025) | ~+12% |

| Net debt (2024) | $1.1B |

| Borrowing spread increase | +150–300 bps |

| Drug CPI (2025) | +6.2% |

| Material inflation (2025) | 7–9% |

| Switching cost per facility | ~$5M |

| AI tech OPEX rise | +8–12% |

What is included in the product

Uncovers competitive pressures facing CoreCivic—evaluating rivalry intensity, supplier and buyer power, entry barriers, and substitution risks—highlighting regulatory, contract-dependency, and reputational dynamics that shape pricing and profitability.

A concise Porter's Five Forces one-sheet for CoreCivic—quickly highlights competitive threats, prison service buyer power, regulatory risk, substitution risk, and barriers to entry to speed executive decisions.

Customers Bargaining Power

Concentration of Federal Government Agencies

CoreCivic derives about 70% of 2024 revenue from federal contracts, mainly ICE and U.S. Marshals Service, concentrating buying power in few agencies.

That concentration lets federal buyers set contract terms, cap pricing, and impose strict compliance standards that compress margins and raise operating costs.

If a major agency shifts procurement—e.g., reducing detainee beds or moving in-house—CoreCivic faces severe revenue loss and valuation downside.

Political and Policy Volatility

The bargaining power of customers for CoreCivic shifts with political winds; the 2025 federal emphasis on border security boosted detention demand, while prior administrations sought to phase out private prisons—policies that can cut or not renew contracts regardless of CoreCivic’s 2024 revenue of $1.9B and government-payments making up ~80% of total revenue. This creates high customer leverage tied to ideology, not performance.

State and Local Budgetary Constraints

State and local budget cuts boost customers’ bargaining power: during 2023–2024, 38% of US states reported fiscal stress, pushing many to press CoreCivic for lower per-diem rates or added services to meet tight budgets.

Procurement reviews often force CoreCivic to accept slimmer margins or lose bids to public facilities; a single 10% rate cut can erase typical operating margins of 6–8% on detention contracts.

Contractual Flexibility and Termination Clauses

Government contracts often include termination-for-convenience clauses allowing exits with 30–180 days notice, giving buyers strong leverage during annual reviews and renewals; in 2024 CoreCivic reported 73% of revenue from federal/state contracts, so this risk is material.

CoreCivic frequently funds capital upgrades or operational concessions—company disclosed $120m–$200m annual maintenance/capex range in 2023–24—to retain these long-term agreements.

- Termination notice: 30–180 days

- Revenue tied to contracts: ~73% (2024)

- Annual capex/maintenance: $120m–$200m

Influence of Public Advocacy and Oversight

Government customers, sensitive to public opinion and civil-rights advocacy, can demand stricter oversight and transparency from CoreCivic after high-profile incidents; for example, 2023 DOJ inquiries and state contract reviews followed reports of facility abuses that drew national media attention.

That social pressure lets buyers impose tougher reporting and accountability without higher fees, squeezing margins—CoreCivic reported a 2024 revenue decline of 6% year-over-year, partly from contract renegotiations and loss.

- 2023 DOJ/state probes increased oversight

- 2024 revenue -6% YOY

- Customers can force reporting, audits

- Higher accountability often without higher pay

CoreCivic at Risk: 73% Govt Revenue, Rising Oversight Could Erase 6–8% Margins

CoreCivic faces very high customer bargaining power: ~73% revenue from government contracts (2024 $1.9B), termination-for-convenience 30–180 days, 2024 revenue -6% YOY, annual capex $120–$200m; political shifts and oversight (2023 DOJ probes) can cut contracts or force rate cuts that erase 6–8% operating margins.

| Metric | Value |

|---|---|

| 2024 revenue | $1.9B |

| Govt revenue | ~73% |

| YOY | -6% |

| Capex | $120–$200m |

What You See Is What You Get

CoreCivic Porter's Five Forces Analysis

This preview shows the exact CoreCivic Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders, fully formatted for use.

The document displayed here is the same professionally written file you’ll be able to download and apply the moment you buy, containing detailed force-by-force evaluation and practical implications.