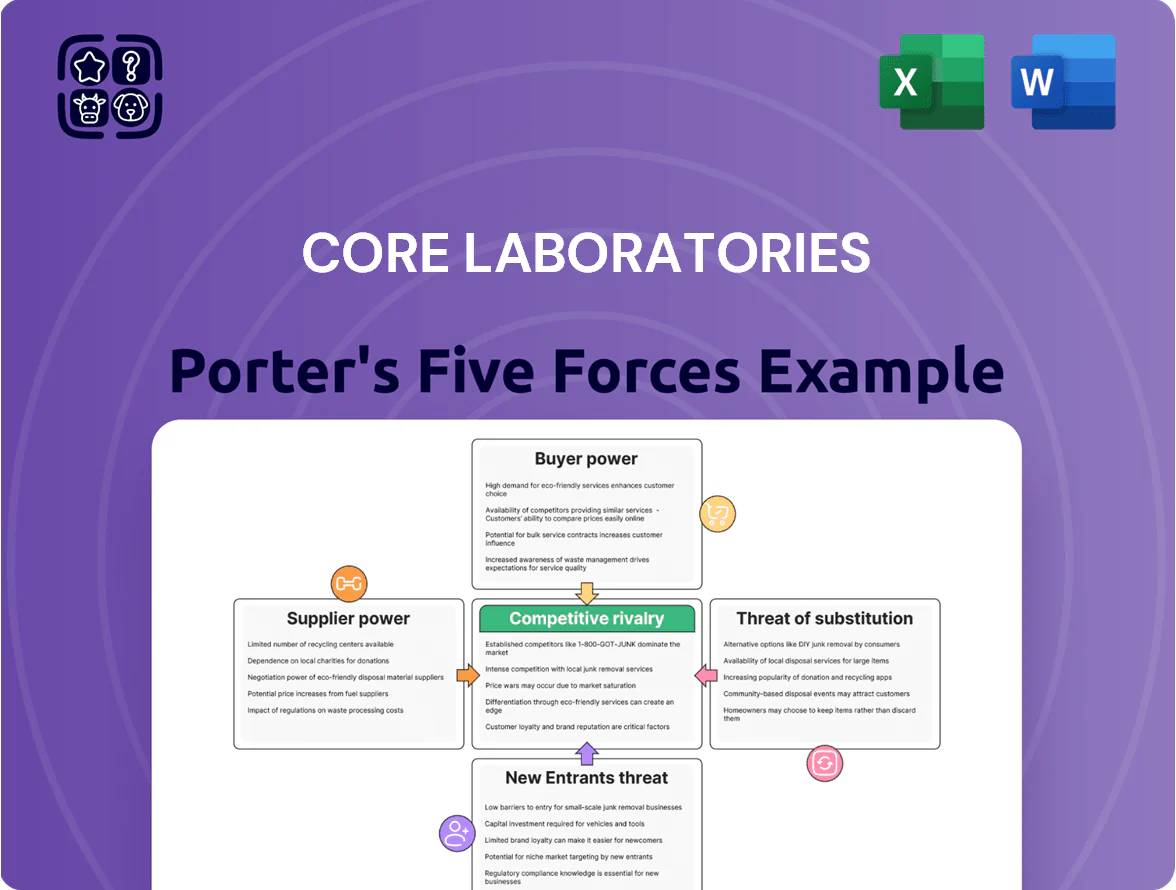

Core Laboratories Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Core Laboratories faces moderate supplier power due to specialized tech and high switching costs, while buyer pressure is tempered by its niche services and long-term contracts; rivalry is driven by a few focused competitors and cyclical oilfield demand.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Core Laboratories’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Laboratory Equipment Providers

Core Laboratories depends on proprietary lab instruments for reservoir description and production enhancement; roughly 60–70% of its lab capex in 2024 went to specialized equipment and maintenance, giving a narrow pool of high-tech suppliers moderate pricing power.

Because a few firms make precision sensors and high-pressure analysis tools, supplier leverage affects service contracts and can raise costs by 5–10% if parts or calibration services tighten.

Supply-chain disruptions—notably semiconductor and precision-machining delays seen in 2023–24—could cut lab throughput and squeeze margins, with an estimated 2–4 percentage-point EBITDA hit per quarter of prolonged outages.

Highly Skilled Technical Labor

Core Lab depends on specialized petrophysicists, geologists, and petroleum engineers to interpret complex data and run lab workflows, giving these suppliers high leverage.

Competition from tech and renewables for STEM talent keeps bargaining power elevated; US STEM wage growth hit 4.5% in 2024, above overall inflation.

With a shrinking pool of experienced oilfield experts — industry reports show a 12% decline in veteran field engineers since 2018 — Core Lab must offer premium pay and benefits to retain proprietary human capital.

Specialized Chemical and Proppant Producers

For Core Laboratories’ production enhancement segment, high-performance additives for deepwater and unconventional reservoirs are concentrated among a few large chemical conglomerates, giving suppliers notable bargaining power.

These specialized inputs, unlike commodity chemicals, saw raw-material price rises of about 12–18% in 2021–2022 and spiked again during 2024 supply-chain stress, letting suppliers pass costs through to service providers.

If global rig counts or demand rebound, suppliers can tighten terms; Core Labs’ 2024 gross margin of ~31% reflects some pass-through but also margin pressure from input inflation.

Energy and Utility Providers

Operating global labs and plants forces Core Laboratories to consume large energy volumes for HVAC, presses, and test rigs; in 2024 industrial energy use rose 3.1% globally, pushing utility bills up.

Core faces regional utility monopolies and volatile oil/gas prices—Brent averaged $86/bbl in 2024—limiting its pricing control.

Sustained high energy costs cut margins, notably where carbon pricing exists (EU average carbon price €84/t in 2024), increasing operating expense risk.

- High energy intensity in labs and plants

- Brent ~$86/bbl (2024) drives input costs

- EU carbon €84/ton (2024) raises regional costs

- Regional utility monopolies limit bargaining

Data and Software Infrastructure Vendors

As Core Laboratories adds digital twins and cloud analytics to reservoir services, dependence on AWS, Microsoft Azure, and Google Cloud grows, raising supplier power due to costly data migration and revalidating models.

High switching costs plus proprietary software and multiyear licences (typical cloud commitments >$1M for enterprise oilfield accounts) lock in vendors and strengthen their bargaining position.

- Dependence: major cloud vendors (AWS, Azure, Google)

- Switching cost: migrating petabytes and retraining models

- Contracts: multiyear licences and integration

- Financial: enterprise cloud spends often exceed $1M annually

Suppliers Squeeze Core Labs: 5–18% Price Power Cuts Margins, 2024 Gross at ~31%

Suppliers—specialized lab-equipment makers, chemical additive firms, cloud providers, energy utilities, and experienced STEM staff—hold moderate-to-high bargaining power for Core Laboratories, able to push prices 5–18% and tighten terms; supply shocks in 2023–24 cost ~2–4 pp EBITDA per quarter and 2024 gross margin was ~31% showing pass-through stress.

| Supplier | Power | Key metric |

|---|---|---|

| Lab equipment | Moderate | 60–70% lab capex (2024) |

| Chemical additives | High | Price rise 12–18% (2021–22) |

| Cloud | High | Enterprise spend >$1M/yr |

| Energy/utilities | Moderate | Brent $86/bbl; EU carbon €84/t (2024) |

| STEM talent | High | US STEM wage +4.5% (2024); veteran engineers −12% since 2018 |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Core Laboratories, revealing competitive intensity, supplier and buyer power, barriers to entry, threat of substitutes, and industry rivalry with strategic implications and editable findings for reports and decks.

Concise Porter's Five Forces snapshot tailored for Core Laboratories—clarify competitive pressures fast and slot directly into investor decks or strategy memos.

Customers Bargaining Power

Consolidation of Supermajor Oil Companies

The customer base for Core Laboratories is dominated by a few supermajors and national oil companies holding over 60% of upstream spend; these buyers command immense purchasing power and can push for lower prices and longer payment terms.

Since 2019 M&A (eg. Chevron- Anadarko 2020, Shell-BG earlier) and 2024–25 deals concentrated production, centralizing procurement and enabling larger volume discounts that squeeze Core Labs’ margins.

Because top 10 customers can represent ~40% of Core Labs’ revenue, losing one major contract would cut annual revenue materially and raise churn and pricing pressure across the book.

Cyclical Capital Expenditure Budgets

Customer spending on reservoir description and production enhancement for Core Laboratories (CLB) is tightly linked to oil and gas prices; after the 2020 price crash CAPEX fell ~30–40% globally and E&P budgets only recovered by about 20% in 2021–2022, showing sensitivity to commodity cycles.

When prices are volatile or low, operators defer discretionary advanced analysis or switch to basic services, reducing CLB’s mix of high-margin work and pressuring revenue.

This cyclicality gives customers leverage to demand price cuts, extended payment terms, or project deferrals during downturns—CLB reported working-capital extensions and contract repricing in multiple 2020–2023 client negotiations.

Internal Technical Capabilities of Large E&P Firms

Many large E&P firms like ExxonMobil, Shell and Saudi Aramco maintain R&D labs; ExxonMobil spent about $1.5bn on R&D in 2024, showing real in-house capacity.

Core Laboratories’ proprietary tech gives higher accuracy, but these in-house labs pose a credible threat if external lab fees rise above customer budgets.

As a result, CoreLabs faces a pricing ceiling for routine analyses—industry sources estimate in-house substitution could cap price premiums at roughly 10–20% for standard tests.

Shift Toward Short-Cycle Projects

Shift toward short-cycle shale projects has raised customer price sensitivity as operators prioritize speed and cost-efficiency over long-term deepwater work; US shale capex rose to about $120 billion in 2024, concentrating demand for fast, standardized services.

Core Laboratories must prove ROI: its premium production-enhancement services need to show incremental recovery or NPV gains exceeding pricing gaps versus commoditized providers to avoid churn.

- Short-cycle focus: US shale capex ~$120B (2024)

- Higher price sensitivity; demand for standardized packages

- CoreLab must demonstrate clear incremental ROI vs cheaper rivals

Rigid Procurement and Tendering Processes

The procurement teams at major oil and gas firms run formal, competitive tenders to pick service providers, pushing Core Laboratories to bid directly against global rivals; in 2024, 70% of large E&P spending used centralized tendering, per IEA procurement surveys.

These standardized bids limit charging power tied to legacy ties or brand: projects often score only on price and technical compliance, squeezing premiums—CoreLabs reported 6–8% margin pressure in 2023 tender-heavy contracts.

Oil buyers centralize power: majors/NOCs squeeze suppliers, capping premiums ~10–20%

Major oil majors and NOCs (>60% upstream spend) concentrate purchasing, centralize tenders (70% in 2024) and can cut prices or extend terms; top 10 clients ≈40% revenue so contract loss is material. Cyclic CAPEX sensitivity (‑30–40% in 2020; US shale capex ~$120B in 2024) and in‑house labs (Exxon R&D $1.5B in 2024) cap pricing power to ~10–20% premiums.

| Metric | Value |

|---|---|

| Share by majors/NOCs | >60% |

| Top10 revenue | ~40% |

| Centralized tenders (2024) | 70% |

| US shale capex (2024) | $120B |

| Exxon R&D (2024) | $1.5B |

| Price premium cap | 10–20% |

Preview Before You Purchase

Core Laboratories Porter's Five Forces Analysis

This preview shows the exact Core Laboratories Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups.

The document displayed here is the same professionally written file you'll be able to download and use the moment you buy, fully formatted and ready for your needs.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Core Laboratories faces moderate supplier power due to specialized tech and high switching costs, while buyer pressure is tempered by its niche services and long-term contracts; rivalry is driven by a few focused competitors and cyclical oilfield demand.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Core Laboratories’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Laboratory Equipment Providers

Core Laboratories depends on proprietary lab instruments for reservoir description and production enhancement; roughly 60–70% of its lab capex in 2024 went to specialized equipment and maintenance, giving a narrow pool of high-tech suppliers moderate pricing power.

Because a few firms make precision sensors and high-pressure analysis tools, supplier leverage affects service contracts and can raise costs by 5–10% if parts or calibration services tighten.

Supply-chain disruptions—notably semiconductor and precision-machining delays seen in 2023–24—could cut lab throughput and squeeze margins, with an estimated 2–4 percentage-point EBITDA hit per quarter of prolonged outages.

Highly Skilled Technical Labor

Core Lab depends on specialized petrophysicists, geologists, and petroleum engineers to interpret complex data and run lab workflows, giving these suppliers high leverage.

Competition from tech and renewables for STEM talent keeps bargaining power elevated; US STEM wage growth hit 4.5% in 2024, above overall inflation.

With a shrinking pool of experienced oilfield experts — industry reports show a 12% decline in veteran field engineers since 2018 — Core Lab must offer premium pay and benefits to retain proprietary human capital.

Specialized Chemical and Proppant Producers

For Core Laboratories’ production enhancement segment, high-performance additives for deepwater and unconventional reservoirs are concentrated among a few large chemical conglomerates, giving suppliers notable bargaining power.

These specialized inputs, unlike commodity chemicals, saw raw-material price rises of about 12–18% in 2021–2022 and spiked again during 2024 supply-chain stress, letting suppliers pass costs through to service providers.

If global rig counts or demand rebound, suppliers can tighten terms; Core Labs’ 2024 gross margin of ~31% reflects some pass-through but also margin pressure from input inflation.

Energy and Utility Providers

Operating global labs and plants forces Core Laboratories to consume large energy volumes for HVAC, presses, and test rigs; in 2024 industrial energy use rose 3.1% globally, pushing utility bills up.

Core faces regional utility monopolies and volatile oil/gas prices—Brent averaged $86/bbl in 2024—limiting its pricing control.

Sustained high energy costs cut margins, notably where carbon pricing exists (EU average carbon price €84/t in 2024), increasing operating expense risk.

- High energy intensity in labs and plants

- Brent ~$86/bbl (2024) drives input costs

- EU carbon €84/ton (2024) raises regional costs

- Regional utility monopolies limit bargaining

Data and Software Infrastructure Vendors

As Core Laboratories adds digital twins and cloud analytics to reservoir services, dependence on AWS, Microsoft Azure, and Google Cloud grows, raising supplier power due to costly data migration and revalidating models.

High switching costs plus proprietary software and multiyear licences (typical cloud commitments >$1M for enterprise oilfield accounts) lock in vendors and strengthen their bargaining position.

- Dependence: major cloud vendors (AWS, Azure, Google)

- Switching cost: migrating petabytes and retraining models

- Contracts: multiyear licences and integration

- Financial: enterprise cloud spends often exceed $1M annually

Suppliers Squeeze Core Labs: 5–18% Price Power Cuts Margins, 2024 Gross at ~31%

Suppliers—specialized lab-equipment makers, chemical additive firms, cloud providers, energy utilities, and experienced STEM staff—hold moderate-to-high bargaining power for Core Laboratories, able to push prices 5–18% and tighten terms; supply shocks in 2023–24 cost ~2–4 pp EBITDA per quarter and 2024 gross margin was ~31% showing pass-through stress.

| Supplier | Power | Key metric |

|---|---|---|

| Lab equipment | Moderate | 60–70% lab capex (2024) |

| Chemical additives | High | Price rise 12–18% (2021–22) |

| Cloud | High | Enterprise spend >$1M/yr |

| Energy/utilities | Moderate | Brent $86/bbl; EU carbon €84/t (2024) |

| STEM talent | High | US STEM wage +4.5% (2024); veteran engineers −12% since 2018 |

What is included in the product

Comprehensive Porter's Five Forces analysis tailored to Core Laboratories, revealing competitive intensity, supplier and buyer power, barriers to entry, threat of substitutes, and industry rivalry with strategic implications and editable findings for reports and decks.

Concise Porter's Five Forces snapshot tailored for Core Laboratories—clarify competitive pressures fast and slot directly into investor decks or strategy memos.

Customers Bargaining Power

Consolidation of Supermajor Oil Companies

The customer base for Core Laboratories is dominated by a few supermajors and national oil companies holding over 60% of upstream spend; these buyers command immense purchasing power and can push for lower prices and longer payment terms.

Since 2019 M&A (eg. Chevron- Anadarko 2020, Shell-BG earlier) and 2024–25 deals concentrated production, centralizing procurement and enabling larger volume discounts that squeeze Core Labs’ margins.

Because top 10 customers can represent ~40% of Core Labs’ revenue, losing one major contract would cut annual revenue materially and raise churn and pricing pressure across the book.

Cyclical Capital Expenditure Budgets

Customer spending on reservoir description and production enhancement for Core Laboratories (CLB) is tightly linked to oil and gas prices; after the 2020 price crash CAPEX fell ~30–40% globally and E&P budgets only recovered by about 20% in 2021–2022, showing sensitivity to commodity cycles.

When prices are volatile or low, operators defer discretionary advanced analysis or switch to basic services, reducing CLB’s mix of high-margin work and pressuring revenue.

This cyclicality gives customers leverage to demand price cuts, extended payment terms, or project deferrals during downturns—CLB reported working-capital extensions and contract repricing in multiple 2020–2023 client negotiations.

Internal Technical Capabilities of Large E&P Firms

Many large E&P firms like ExxonMobil, Shell and Saudi Aramco maintain R&D labs; ExxonMobil spent about $1.5bn on R&D in 2024, showing real in-house capacity.

Core Laboratories’ proprietary tech gives higher accuracy, but these in-house labs pose a credible threat if external lab fees rise above customer budgets.

As a result, CoreLabs faces a pricing ceiling for routine analyses—industry sources estimate in-house substitution could cap price premiums at roughly 10–20% for standard tests.

Shift Toward Short-Cycle Projects

Shift toward short-cycle shale projects has raised customer price sensitivity as operators prioritize speed and cost-efficiency over long-term deepwater work; US shale capex rose to about $120 billion in 2024, concentrating demand for fast, standardized services.

Core Laboratories must prove ROI: its premium production-enhancement services need to show incremental recovery or NPV gains exceeding pricing gaps versus commoditized providers to avoid churn.

- Short-cycle focus: US shale capex ~$120B (2024)

- Higher price sensitivity; demand for standardized packages

- CoreLab must demonstrate clear incremental ROI vs cheaper rivals

Rigid Procurement and Tendering Processes

The procurement teams at major oil and gas firms run formal, competitive tenders to pick service providers, pushing Core Laboratories to bid directly against global rivals; in 2024, 70% of large E&P spending used centralized tendering, per IEA procurement surveys.

These standardized bids limit charging power tied to legacy ties or brand: projects often score only on price and technical compliance, squeezing premiums—CoreLabs reported 6–8% margin pressure in 2023 tender-heavy contracts.

Oil buyers centralize power: majors/NOCs squeeze suppliers, capping premiums ~10–20%

Major oil majors and NOCs (>60% upstream spend) concentrate purchasing, centralize tenders (70% in 2024) and can cut prices or extend terms; top 10 clients ≈40% revenue so contract loss is material. Cyclic CAPEX sensitivity (‑30–40% in 2020; US shale capex ~$120B in 2024) and in‑house labs (Exxon R&D $1.5B in 2024) cap pricing power to ~10–20% premiums.

| Metric | Value |

|---|---|

| Share by majors/NOCs | >60% |

| Top10 revenue | ~40% |

| Centralized tenders (2024) | 70% |

| US shale capex (2024) | $120B |

| Exxon R&D (2024) | $1.5B |

| Price premium cap | 10–20% |

Preview Before You Purchase

Core Laboratories Porter's Five Forces Analysis

This preview shows the exact Core Laboratories Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups.

The document displayed here is the same professionally written file you'll be able to download and use the moment you buy, fully formatted and ready for your needs.