Corning Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

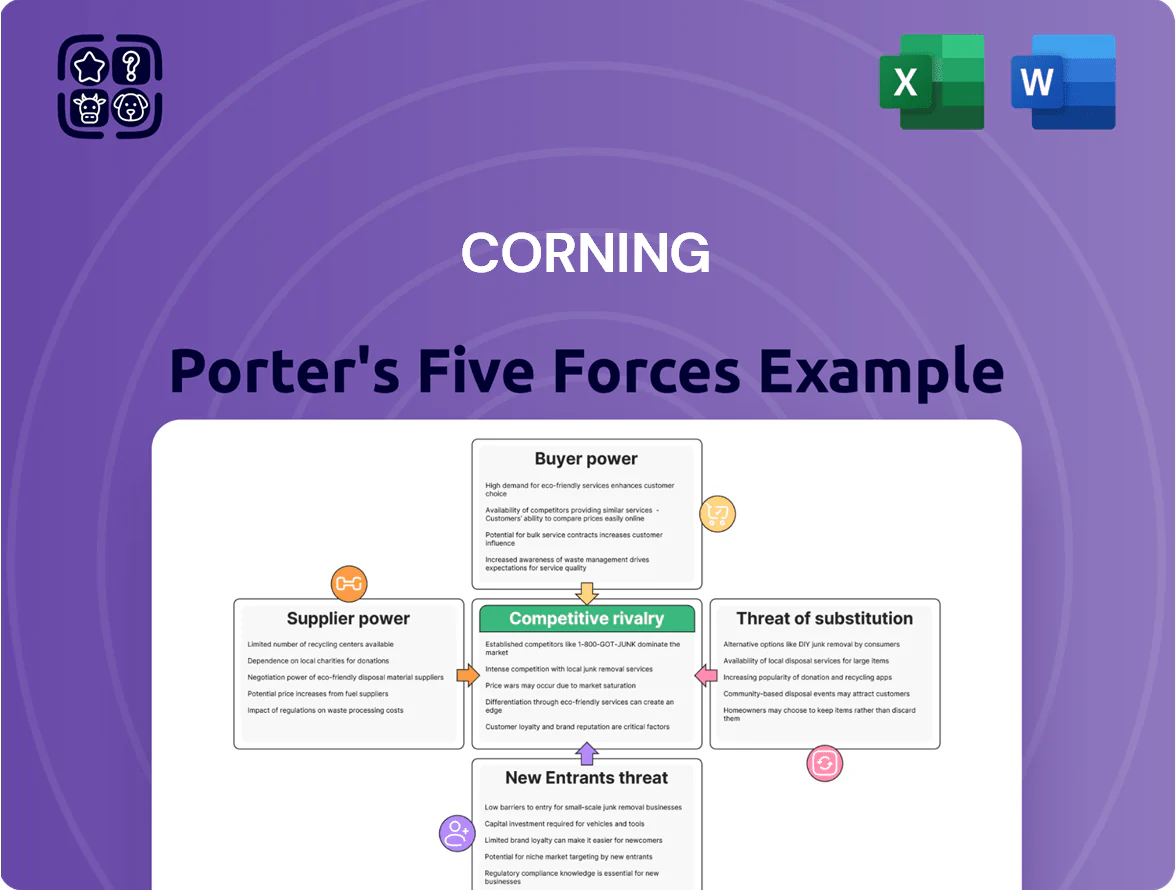

Corning faces a mix of intense supplier and buyer pressures, moderate threat from substitutes, and barriers to new entrants driven by scale and IP, shaping a competitive yet opportunity-rich landscape; strategic positioning hinges on innovation and vertical integration. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Corning’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Raw Material Constraints

Corning depends on high-purity silica, specialty chemicals, and platinum-group metals for its glass-melting furnaces; platinum prices averaged about $1,060/oz in 2025 YTD, raising input cost risk. Only a few global suppliers meet Corning’s <5 ppm impurity specs, so supplier concentration creates moderate dependency and potential single-source disruptions affecting ~10–15% of production capacity.

Energy Intensity and Utility Costs

Energy intensity in glass and ceramics means Corning consumes vast continuous natural gas and electricity; in 2024 Corning reported energy costs rising ~6% year-over-year, and utilities account for an estimated 8–12% of manufacturing COGS, so suppliers wield indirect pricing power.

Technological Co-dependence

Certain suppliers provide proprietary fusion-draw furnace components and precision tooling critical to Corning’s specialty glass lines, creating technical lock-in; switching costs can exceed $50m per production line given integration and requalification timelines. This dependence gave high-tech equipment makers leverage in 2024–25, influencing maintenance pricing and extension cycles that Corning disclosed as driving ~3–5% incremental OPEX on select segments.

Geopolitical Supply Chain Risks

- Key sources: China, Australia, Chile, Africa

- 2025 spot-price rise: 12–18% for critical minerals

- Export restrictions and tariffs increased supplier leverage

- Stable-region suppliers command premiums

Limited Forward Integration

Most suppliers of sand, minerals, and specialty chemicals lack the capital and proprietary materials-science needed to move into glass production, limiting forward integration and weakening supplier bargaining power.

Corning’s scale—$14.1 billion revenue in 2024 and multi-year high-volume contracts for display and optical fiber segments—gives it leverage over fragmented vendors, reducing input-price pressure and switching costs.

- Low supplier integration capability

- Corning revenue: $14.1B (2024)

- High purchasing scale → stronger negotiation

Suppliers pressure Corning: 2025 input shocks vs $14.1B scale buffer

Suppliers have moderate bargaining power: critical inputs (platinum, lithium, boron) and specialty tooling concentrate supply, causing 10–18% spot-price shocks in 2025 and ~3–5% higher OPEX on niche lines, but Corning’s $14.1B 2024 scale and long-term contracts limit price pass-through and switching cost exposure.

| Metric | Value |

|---|---|

| 2024 Revenue | $14.1B |

| 2025 spot-price rise | 12–18% |

| Production at risk (single-source) | 10–15% |

| Incremental OPEX from tooling | 3–5% |

| Estimated energy share of COGS | 8–12% |

What is included in the product

Tailored Porter’s Five Forces analysis for Corning that evaluates competitive rivalry, supplier and buyer power, threats from new entrants and substitutes, and highlights disruptive technologies and market dynamics affecting Corning’s pricing power and profitability.

A concise Porter’s Five Forces snapshot for Corning—quickly assess supplier, buyer, rivalry, entrant, and substitute pressures to streamline strategic choices.

Customers Bargaining Power

Concentration of Major Tech OEMs

A significant share of Corning’s Mobile Consumer Electronics and Display revenue—about 35% of consolidated net sales in 2024—comes from a few large OEMs such as Apple and Samsung, giving these buyers strong bargaining power.

These customers push for lower prices and rapid product cycles; Corning reported 6–12 month innovation timelines with them in 2024, raising margin pressure.

Loss of a single major contract or a sourcing shift by Apple or Samsung could reduce annual revenue by several percentage points and materially hit operating income; Corning’s 2024 operating margin was 19.2%.

Standardization in Optical Communications

Large carriers and hyperscale data center operators insist on standards for interoperability, making 40%–60% of fiber purchases price-sensitive; in 2024 Corning reported optical sales growth of 6% but faced margin pressure as standardized single-mode fiber prices fell ~8% YOY.

High Switching Costs for Integrated Systems

Once Corning’s glass or fiber is specified into a system, switching costs are high—retooling, retesting and supplier validation can exceed millions; a 2024 survey found 62% of OEMs cite supplier change costs >$1m.

In Life Sciences and Automotive, regulatory approvals and ISO/TS certifications are material-specific, so design-in creates technical stickiness that lowers customer leverage.

Price Sensitivity in Display Markets

The TV and monitor sectors run on razor-thin OEM margins—global LCD TV ASPs fell ~6% in 2024 and panel makers saw operating margins near 3–5%, so buyers push hard on glass substrate pricing.

Corning faces frequent price-pressure from large OEMs and fabs; it counters by driving down unit costs via scale and a lowest-cost-producer focus, keeping capex and yield improvements central to protect EBITDA.

- Panel maker margins ~3–5% (2024)

- Global LCD TV ASPs −6% in 2024

- Corning targets yield/cost cuts to defend pricing

Demand for Co-Innovation

Customers now demand co-innovation, pushing Corning into joint R&D for foldable displays and autonomous-vehicle sensors; in 2024 Corning reported R&D spending of $1.1 billion, reflecting this shift.

This gives customers influence over roadmaps but creates dependence on Corning’s specialized glass and materials science, balancing bargaining power.

- 2024 R&D $1.1B

- JV product timelines shorten, shared IP stakes rise

- Customers gain roadmap input but rely on Corning’s tech

OEM concentration squeezes Corning margins as fiber prices drop and switching costs remain high

Major OEMs (Apple, Samsung) drive ~35% of Corning’s 2024 sales, forcing price cuts and 6–12 month product cycles that squeezed margins (2024 operating margin 19.2%). Large optical buyers made 40–60% of fiber demand price-sensitive; single-mode fiber prices fell ~8% YOY in 2024. High switching costs (survey: 62% OEMs >$1m) and design-in in Life Sciences/Automotive reduce buyer leverage.

| Metric | 2024 |

|---|---|

| Share from big OEMs | ~35% |

| Operating margin | 19.2% |

| R&D | $1.1B |

| Fiber price change | −8% YOY |

| OEMs citing >$1m switch cost | 62% |

Full Version Awaits

Corning Porter's Five Forces Analysis

This preview shows the exact Corning Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready to use with no placeholders or samples. It includes evaluation of competitive rivalry, supplier and buyer power, threats of new entrants and substitutes, and concise implications for strategy and valuation. Purchase grants instant access to this same complete document.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

Corning faces a mix of intense supplier and buyer pressures, moderate threat from substitutes, and barriers to new entrants driven by scale and IP, shaping a competitive yet opportunity-rich landscape; strategic positioning hinges on innovation and vertical integration. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Corning’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Raw Material Constraints

Corning depends on high-purity silica, specialty chemicals, and platinum-group metals for its glass-melting furnaces; platinum prices averaged about $1,060/oz in 2025 YTD, raising input cost risk. Only a few global suppliers meet Corning’s <5 ppm impurity specs, so supplier concentration creates moderate dependency and potential single-source disruptions affecting ~10–15% of production capacity.

Energy Intensity and Utility Costs

Energy intensity in glass and ceramics means Corning consumes vast continuous natural gas and electricity; in 2024 Corning reported energy costs rising ~6% year-over-year, and utilities account for an estimated 8–12% of manufacturing COGS, so suppliers wield indirect pricing power.

Technological Co-dependence

Certain suppliers provide proprietary fusion-draw furnace components and precision tooling critical to Corning’s specialty glass lines, creating technical lock-in; switching costs can exceed $50m per production line given integration and requalification timelines. This dependence gave high-tech equipment makers leverage in 2024–25, influencing maintenance pricing and extension cycles that Corning disclosed as driving ~3–5% incremental OPEX on select segments.

Geopolitical Supply Chain Risks

- Key sources: China, Australia, Chile, Africa

- 2025 spot-price rise: 12–18% for critical minerals

- Export restrictions and tariffs increased supplier leverage

- Stable-region suppliers command premiums

Limited Forward Integration

Most suppliers of sand, minerals, and specialty chemicals lack the capital and proprietary materials-science needed to move into glass production, limiting forward integration and weakening supplier bargaining power.

Corning’s scale—$14.1 billion revenue in 2024 and multi-year high-volume contracts for display and optical fiber segments—gives it leverage over fragmented vendors, reducing input-price pressure and switching costs.

- Low supplier integration capability

- Corning revenue: $14.1B (2024)

- High purchasing scale → stronger negotiation

Suppliers pressure Corning: 2025 input shocks vs $14.1B scale buffer

Suppliers have moderate bargaining power: critical inputs (platinum, lithium, boron) and specialty tooling concentrate supply, causing 10–18% spot-price shocks in 2025 and ~3–5% higher OPEX on niche lines, but Corning’s $14.1B 2024 scale and long-term contracts limit price pass-through and switching cost exposure.

| Metric | Value |

|---|---|

| 2024 Revenue | $14.1B |

| 2025 spot-price rise | 12–18% |

| Production at risk (single-source) | 10–15% |

| Incremental OPEX from tooling | 3–5% |

| Estimated energy share of COGS | 8–12% |

What is included in the product

Tailored Porter’s Five Forces analysis for Corning that evaluates competitive rivalry, supplier and buyer power, threats from new entrants and substitutes, and highlights disruptive technologies and market dynamics affecting Corning’s pricing power and profitability.

A concise Porter’s Five Forces snapshot for Corning—quickly assess supplier, buyer, rivalry, entrant, and substitute pressures to streamline strategic choices.

Customers Bargaining Power

Concentration of Major Tech OEMs

A significant share of Corning’s Mobile Consumer Electronics and Display revenue—about 35% of consolidated net sales in 2024—comes from a few large OEMs such as Apple and Samsung, giving these buyers strong bargaining power.

These customers push for lower prices and rapid product cycles; Corning reported 6–12 month innovation timelines with them in 2024, raising margin pressure.

Loss of a single major contract or a sourcing shift by Apple or Samsung could reduce annual revenue by several percentage points and materially hit operating income; Corning’s 2024 operating margin was 19.2%.

Standardization in Optical Communications

Large carriers and hyperscale data center operators insist on standards for interoperability, making 40%–60% of fiber purchases price-sensitive; in 2024 Corning reported optical sales growth of 6% but faced margin pressure as standardized single-mode fiber prices fell ~8% YOY.

High Switching Costs for Integrated Systems

Once Corning’s glass or fiber is specified into a system, switching costs are high—retooling, retesting and supplier validation can exceed millions; a 2024 survey found 62% of OEMs cite supplier change costs >$1m.

In Life Sciences and Automotive, regulatory approvals and ISO/TS certifications are material-specific, so design-in creates technical stickiness that lowers customer leverage.

Price Sensitivity in Display Markets

The TV and monitor sectors run on razor-thin OEM margins—global LCD TV ASPs fell ~6% in 2024 and panel makers saw operating margins near 3–5%, so buyers push hard on glass substrate pricing.

Corning faces frequent price-pressure from large OEMs and fabs; it counters by driving down unit costs via scale and a lowest-cost-producer focus, keeping capex and yield improvements central to protect EBITDA.

- Panel maker margins ~3–5% (2024)

- Global LCD TV ASPs −6% in 2024

- Corning targets yield/cost cuts to defend pricing

Demand for Co-Innovation

Customers now demand co-innovation, pushing Corning into joint R&D for foldable displays and autonomous-vehicle sensors; in 2024 Corning reported R&D spending of $1.1 billion, reflecting this shift.

This gives customers influence over roadmaps but creates dependence on Corning’s specialized glass and materials science, balancing bargaining power.

- 2024 R&D $1.1B

- JV product timelines shorten, shared IP stakes rise

- Customers gain roadmap input but rely on Corning’s tech

OEM concentration squeezes Corning margins as fiber prices drop and switching costs remain high

Major OEMs (Apple, Samsung) drive ~35% of Corning’s 2024 sales, forcing price cuts and 6–12 month product cycles that squeezed margins (2024 operating margin 19.2%). Large optical buyers made 40–60% of fiber demand price-sensitive; single-mode fiber prices fell ~8% YOY in 2024. High switching costs (survey: 62% OEMs >$1m) and design-in in Life Sciences/Automotive reduce buyer leverage.

| Metric | 2024 |

|---|---|

| Share from big OEMs | ~35% |

| Operating margin | 19.2% |

| R&D | $1.1B |

| Fiber price change | −8% YOY |

| OEMs citing >$1m switch cost | 62% |

Full Version Awaits

Corning Porter's Five Forces Analysis

This preview shows the exact Corning Porter's Five Forces analysis you'll receive immediately after purchase—fully formatted, professionally written, and ready to use with no placeholders or samples. It includes evaluation of competitive rivalry, supplier and buyer power, threats of new entrants and substitutes, and concise implications for strategy and valuation. Purchase grants instant access to this same complete document.