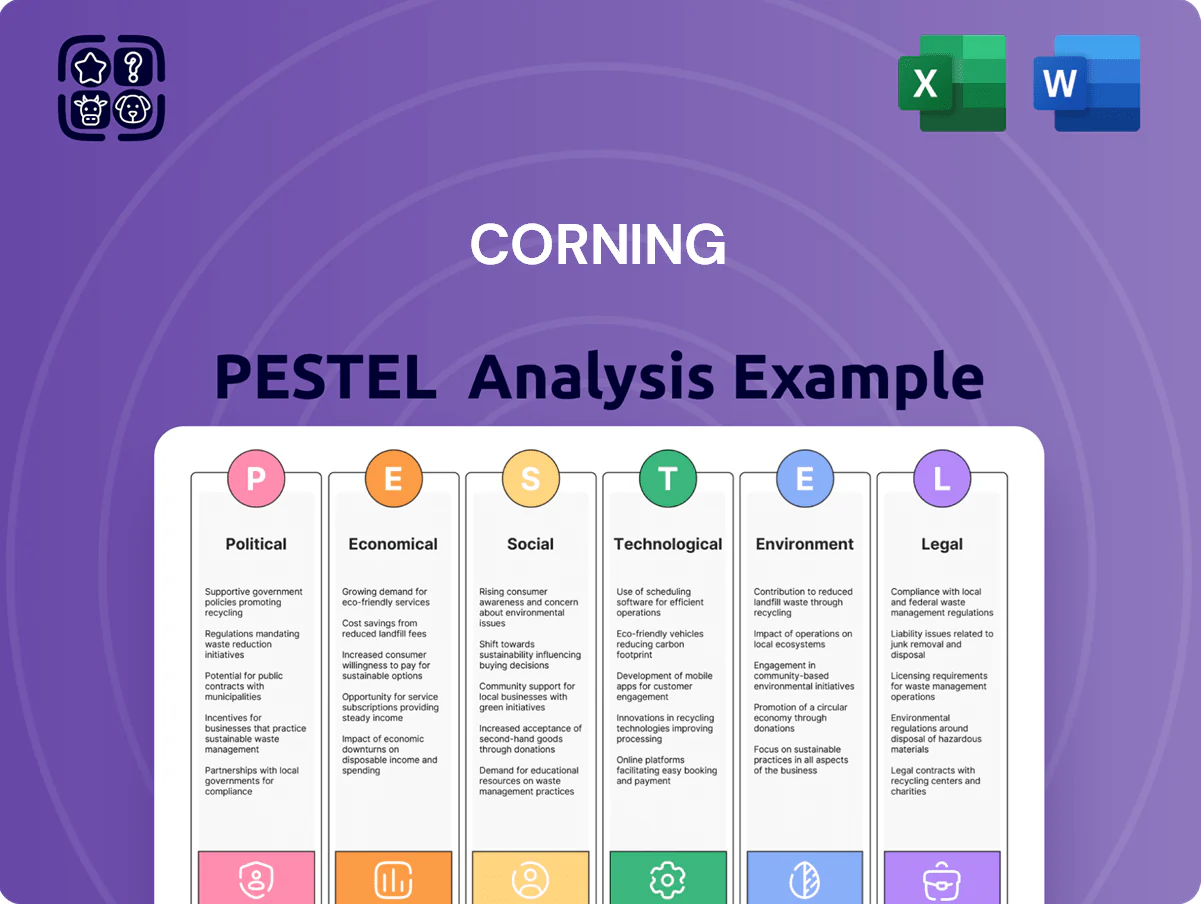

Corning PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic cycles, social trends, technological leadership, regulatory pressures, and environmental priorities converge to shape Corning’s strategic outlook—our concise PESTLE highlights key external risks and opportunities you need to know. Purchase the full PESTLE for a detailed, ready-to-use report with actionable insights to inform investment decisions, strategy sessions, and competitive analysis—download instantly.

Political factors

Geopolitical Trade Relations

The ongoing US-China trade tensions affect Corning's manufacturing footprint and supply-chain stability; in 2024 China accounted for about 26% of Corning's $13.4B net sales, exposing the company to tariffs and export controls on specialty glass and optical components.

Government Infrastructure Subsidies

Domestic Manufacturing Incentives

The CHIPS and Science Act (2022) allocates roughly $52 billion to boost US semiconductor manufacturing, creating demand for Corning’s glass substrates used in advanced packaging; Corning reported $14.5 billion in FY2024 sales, with a growing Materials segment tied to microelectronics. US policy prioritizing onshore supply chains increases federal procurement and private investment, strengthening Corning’s strategic positioning in critical technology supply chains.

Regulatory Export Controls

Stricter export controls on advanced optics and materials science threaten Corning’s international sales growth, with U.S. controls expanded in 2023 and 2024 affecting products tied to semiconductor and telecom supply chains that contributed about $6.5bn of Corning’s 2024 revenue.

Political limits on tech transfer to China, Russia and allied jurisdictions force Corning to invest in compliance, legal review and supply-chain segmentation, increasing operating expenses and potentially reducing addressable markets.

Maintaining competitiveness in specialty glass requires navigating overlapping U.S., EU and allied export rules while protecting IP and fulfilling customer demand across global markets.

- 2023–24 U.S. export rule expansions impacted semiconductor-related product lines tied to ~$6.5bn 2024 revenue

- Compliance and supply-chain segmentation raise OPEX and restrict market access

- Target markets like China face tighter transfer limits, constraining growth

Energy Security Policies

Political shifts toward energy independence and renewables affect Corning's manufacturing costs and strategy; US IRA incentives boosted domestic clean energy investment to $700B+ through 2031, increasing demand for photovoltaic glass and Low-E glass used in energy-efficient buildings.

Policies supporting solar and efficient glass tech create market opportunities—Corning's specialty glass for photovoltaics can capture portions of a global solar market projected at $280B in 2025.

However, volatile energy policies can drive furnace energy costs; glass melting is energy-intensive, with electricity and fuel representing up to 20–30% of production costs, raising margin risk.

- IRA and similar subsidies expand addressable market for Corning's solar/efficiency glass

- Domestic clean-energy investment >$700B through 2031 increases demand

- Global solar market ~ $280B (2025) creates growth tailwind

- Energy costs can be 20–30% of glass production costs, increasing margin volatility

Corning poised between China export limits and U.S. semiconductor/clean‑energy demand

US-China trade tensions, expanded export controls (2023–24) and tech-transfer limits constrain Corning’s China exposure (26% of $13.4B 2024 sales) and raise compliance OPEX; CHIPS Act and BEAD/DEI funding (US $52B, BEAD $42.45B) plus IRA-driven >$700B clean-energy investment boost demand for optical, semiconductor and specialty glass (Optical Communications $3.9B, Materials-linked sales ~$14.5B, semiconductor-related ~$6.5B in 2024).

| Factor | 2024/2025 Data |

|---|---|

| China sales exposure | 26% of $13.4B (2024) |

| Optical Communications | $3.9B (FY2024) |

| Materials/semiconductor-related | $14.5B sales; ~$6.5B affected by export rules (2024) |

| BEAD/DEI funding | $42.45B (2021–2026) |

| CHIPS Act | ~$52B (authorized) |

| Clean-energy investment | >$700B through 2031 (IRA) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Corning across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—with data-driven insights and trend analysis tailored to its optical materials, display glass, and telecom segments to help executives and investors identify threats, opportunities, and actionable strategy implications.

A concise, shareable PESTLE summary of Corning that highlights regulatory, technological, and supply-chain risks for quick use in presentations or cross-team strategy sessions.

Economic factors

Inflationary Pressure on Input Costs

Persistent inflation in 2025 lifted raw material and energy costs for glass and ceramics; silica, soda ash and natural gas input costs rose roughly 8–12% year-over-year, squeezing margins. Corning offsets pressure via price adjustment clauses and efficiency programs—CapEx for process automation rose to about $850m in 2025 to lower unit costs. Its pass-through ability hinges on competitive dynamics and the critical, inelastic demand for specialty products like display and optical glass.

Consumer Spending on Electronics

Demand for Corning's Gorilla Glass tracks global smartphone/tablet sales—IDC reported 2024 global smartphone shipments at ~1.21 billion, down 2.4% YoY, pressuring cover-glass volumes. Economic slowdowns that cut discretionary income extend device replacement cycles; US consumer savings rate fell to 3.8% in 2024, indicating tighter spend. Analysts watch global policy rates (Fed funds ~5.25–5.50% in 2024) and unemployment (US 2024 avg ~4.0%) as leading indicators for premium device demand.

Capital Expenditure Trends in Telecom

Corning's revenue is highly tied to capex at major carriers and data-center operators; global telecom capex fell 2% in 2024 while hyperscaler network spend rose ~5%, per industry reports, directly affecting fiber and optical demand.

High borrowing costs in 2024–2025 prompted some carriers to delay 5G and FTTH rollouts, with U.S. telecom capex guidance cut by several operators by mid-single digits.

Nonetheless, secular data growth—global IP traffic projected to grow ~20% year-over-year in 2024—helps mitigate short-term pauses, sustaining long-term demand for Corning's fiber and optical products.

Cyclicality of the Display Market

The display glass market is highly cyclical, with global LCD/OLED panel capacity swings causing periodic supply-demand imbalances that pressured large-size glass pricing and utilization; Corning noted LCD panel area shipments fell ~8% year-over-year in 2023, contributing to lower substrate orders.

During economic slowdowns inventory buildups at panel makers reduced Corning’s large-substrate demand, but flexible manufacturing and cost controls helped sustain margins—Corning reported a 2024 operating margin resilience with adjusted gross margin near 30%.

- Panel shipment volatility: ~-8% YoY in 2023

- Impact: reduced large-substrate orders, inventory gluts

- Corning response: flexible manufacturing platforms, cost controls

- Outcome: maintained adjusted gross margin ~30% in 2024

Automotive Industry Growth

Economic recovery and global vehicle production rebound to ~85 million units in 2024 supports demand for Corning’s automotive glass and ceramic substrates used in catalytic converters and particulate filters, with automotive revenue ~10% of Corning’s 2024 sales. The EV transition—EV sales ~14% of global light-vehicle sales in 2024—boosts demand for specialty glass for touch displays and ceramic substrates for power electronics. Rising consumer demand for premium in-car experiences increases average selling prices for curved displays and laminated glass, strengthening Corning’s higher-margin specialty glass segment.

- 2024 global vehicle production ~85M units

- EV share ~14% of light-vehicle sales (2024)

- Automotive ≈10% of Corning 2024 revenue

Inflation, automation CapEx squeeze margins as demand shifts to fiber/specialty glass

Inflation raised silica, soda ash and gas costs ~8–12% in 2025, squeezing margins despite $850m 2025 CapEx for automation; Corning passed some costs via price clauses. 2024 smartphone shipments ~1.21B (-2.4% YoY) and panel area shipments -8% (2023) pressured display volumes; data-center/hyperscaler capex +5% (2024) vs telco capex -2% shifted optical demand toward fiber and specialty glass.

| Metric | Value |

|---|---|

| Raw material cost rise (2025) | 8–12% |

| CapEx for automation (2025) | $850m |

| Smartphone shipments (2024) | 1.21B (-2.4%) |

| Panel area shipments (2023) | -8% |

| Hyperscaler spend (2024) | +5% |

| Telco capex (2024) | -2% |

Same Document Delivered

Corning PESTLE Analysis

The preview shown here is the exact Corning PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the layout, content, and structure visible in this preview are exactly what you’ll be able to download immediately after buying.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic cycles, social trends, technological leadership, regulatory pressures, and environmental priorities converge to shape Corning’s strategic outlook—our concise PESTLE highlights key external risks and opportunities you need to know. Purchase the full PESTLE for a detailed, ready-to-use report with actionable insights to inform investment decisions, strategy sessions, and competitive analysis—download instantly.

Political factors

Geopolitical Trade Relations

The ongoing US-China trade tensions affect Corning's manufacturing footprint and supply-chain stability; in 2024 China accounted for about 26% of Corning's $13.4B net sales, exposing the company to tariffs and export controls on specialty glass and optical components.

Government Infrastructure Subsidies

Domestic Manufacturing Incentives

The CHIPS and Science Act (2022) allocates roughly $52 billion to boost US semiconductor manufacturing, creating demand for Corning’s glass substrates used in advanced packaging; Corning reported $14.5 billion in FY2024 sales, with a growing Materials segment tied to microelectronics. US policy prioritizing onshore supply chains increases federal procurement and private investment, strengthening Corning’s strategic positioning in critical technology supply chains.

Regulatory Export Controls

Stricter export controls on advanced optics and materials science threaten Corning’s international sales growth, with U.S. controls expanded in 2023 and 2024 affecting products tied to semiconductor and telecom supply chains that contributed about $6.5bn of Corning’s 2024 revenue.

Political limits on tech transfer to China, Russia and allied jurisdictions force Corning to invest in compliance, legal review and supply-chain segmentation, increasing operating expenses and potentially reducing addressable markets.

Maintaining competitiveness in specialty glass requires navigating overlapping U.S., EU and allied export rules while protecting IP and fulfilling customer demand across global markets.

- 2023–24 U.S. export rule expansions impacted semiconductor-related product lines tied to ~$6.5bn 2024 revenue

- Compliance and supply-chain segmentation raise OPEX and restrict market access

- Target markets like China face tighter transfer limits, constraining growth

Energy Security Policies

Political shifts toward energy independence and renewables affect Corning's manufacturing costs and strategy; US IRA incentives boosted domestic clean energy investment to $700B+ through 2031, increasing demand for photovoltaic glass and Low-E glass used in energy-efficient buildings.

Policies supporting solar and efficient glass tech create market opportunities—Corning's specialty glass for photovoltaics can capture portions of a global solar market projected at $280B in 2025.

However, volatile energy policies can drive furnace energy costs; glass melting is energy-intensive, with electricity and fuel representing up to 20–30% of production costs, raising margin risk.

- IRA and similar subsidies expand addressable market for Corning's solar/efficiency glass

- Domestic clean-energy investment >$700B through 2031 increases demand

- Global solar market ~ $280B (2025) creates growth tailwind

- Energy costs can be 20–30% of glass production costs, increasing margin volatility

Corning poised between China export limits and U.S. semiconductor/clean‑energy demand

US-China trade tensions, expanded export controls (2023–24) and tech-transfer limits constrain Corning’s China exposure (26% of $13.4B 2024 sales) and raise compliance OPEX; CHIPS Act and BEAD/DEI funding (US $52B, BEAD $42.45B) plus IRA-driven >$700B clean-energy investment boost demand for optical, semiconductor and specialty glass (Optical Communications $3.9B, Materials-linked sales ~$14.5B, semiconductor-related ~$6.5B in 2024).

| Factor | 2024/2025 Data |

|---|---|

| China sales exposure | 26% of $13.4B (2024) |

| Optical Communications | $3.9B (FY2024) |

| Materials/semiconductor-related | $14.5B sales; ~$6.5B affected by export rules (2024) |

| BEAD/DEI funding | $42.45B (2021–2026) |

| CHIPS Act | ~$52B (authorized) |

| Clean-energy investment | >$700B through 2031 (IRA) |

What is included in the product

Explores how external macro-environmental factors uniquely affect Corning across six dimensions—Political, Economic, Social, Technological, Environmental, and Legal—with data-driven insights and trend analysis tailored to its optical materials, display glass, and telecom segments to help executives and investors identify threats, opportunities, and actionable strategy implications.

A concise, shareable PESTLE summary of Corning that highlights regulatory, technological, and supply-chain risks for quick use in presentations or cross-team strategy sessions.

Economic factors

Inflationary Pressure on Input Costs

Persistent inflation in 2025 lifted raw material and energy costs for glass and ceramics; silica, soda ash and natural gas input costs rose roughly 8–12% year-over-year, squeezing margins. Corning offsets pressure via price adjustment clauses and efficiency programs—CapEx for process automation rose to about $850m in 2025 to lower unit costs. Its pass-through ability hinges on competitive dynamics and the critical, inelastic demand for specialty products like display and optical glass.

Consumer Spending on Electronics

Demand for Corning's Gorilla Glass tracks global smartphone/tablet sales—IDC reported 2024 global smartphone shipments at ~1.21 billion, down 2.4% YoY, pressuring cover-glass volumes. Economic slowdowns that cut discretionary income extend device replacement cycles; US consumer savings rate fell to 3.8% in 2024, indicating tighter spend. Analysts watch global policy rates (Fed funds ~5.25–5.50% in 2024) and unemployment (US 2024 avg ~4.0%) as leading indicators for premium device demand.

Capital Expenditure Trends in Telecom

Corning's revenue is highly tied to capex at major carriers and data-center operators; global telecom capex fell 2% in 2024 while hyperscaler network spend rose ~5%, per industry reports, directly affecting fiber and optical demand.

High borrowing costs in 2024–2025 prompted some carriers to delay 5G and FTTH rollouts, with U.S. telecom capex guidance cut by several operators by mid-single digits.

Nonetheless, secular data growth—global IP traffic projected to grow ~20% year-over-year in 2024—helps mitigate short-term pauses, sustaining long-term demand for Corning's fiber and optical products.

Cyclicality of the Display Market

The display glass market is highly cyclical, with global LCD/OLED panel capacity swings causing periodic supply-demand imbalances that pressured large-size glass pricing and utilization; Corning noted LCD panel area shipments fell ~8% year-over-year in 2023, contributing to lower substrate orders.

During economic slowdowns inventory buildups at panel makers reduced Corning’s large-substrate demand, but flexible manufacturing and cost controls helped sustain margins—Corning reported a 2024 operating margin resilience with adjusted gross margin near 30%.

- Panel shipment volatility: ~-8% YoY in 2023

- Impact: reduced large-substrate orders, inventory gluts

- Corning response: flexible manufacturing platforms, cost controls

- Outcome: maintained adjusted gross margin ~30% in 2024

Automotive Industry Growth

Economic recovery and global vehicle production rebound to ~85 million units in 2024 supports demand for Corning’s automotive glass and ceramic substrates used in catalytic converters and particulate filters, with automotive revenue ~10% of Corning’s 2024 sales. The EV transition—EV sales ~14% of global light-vehicle sales in 2024—boosts demand for specialty glass for touch displays and ceramic substrates for power electronics. Rising consumer demand for premium in-car experiences increases average selling prices for curved displays and laminated glass, strengthening Corning’s higher-margin specialty glass segment.

- 2024 global vehicle production ~85M units

- EV share ~14% of light-vehicle sales (2024)

- Automotive ≈10% of Corning 2024 revenue

Inflation, automation CapEx squeeze margins as demand shifts to fiber/specialty glass

Inflation raised silica, soda ash and gas costs ~8–12% in 2025, squeezing margins despite $850m 2025 CapEx for automation; Corning passed some costs via price clauses. 2024 smartphone shipments ~1.21B (-2.4% YoY) and panel area shipments -8% (2023) pressured display volumes; data-center/hyperscaler capex +5% (2024) vs telco capex -2% shifted optical demand toward fiber and specialty glass.

| Metric | Value |

|---|---|

| Raw material cost rise (2025) | 8–12% |

| CapEx for automation (2025) | $850m |

| Smartphone shipments (2024) | 1.21B (-2.4%) |

| Panel area shipments (2023) | -8% |

| Hyperscaler spend (2024) | +5% |

| Telco capex (2024) | -2% |

Same Document Delivered

Corning PESTLE Analysis

The preview shown here is the exact Corning PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use.

No placeholders or teasers: the layout, content, and structure visible in this preview are exactly what you’ll be able to download immediately after buying.