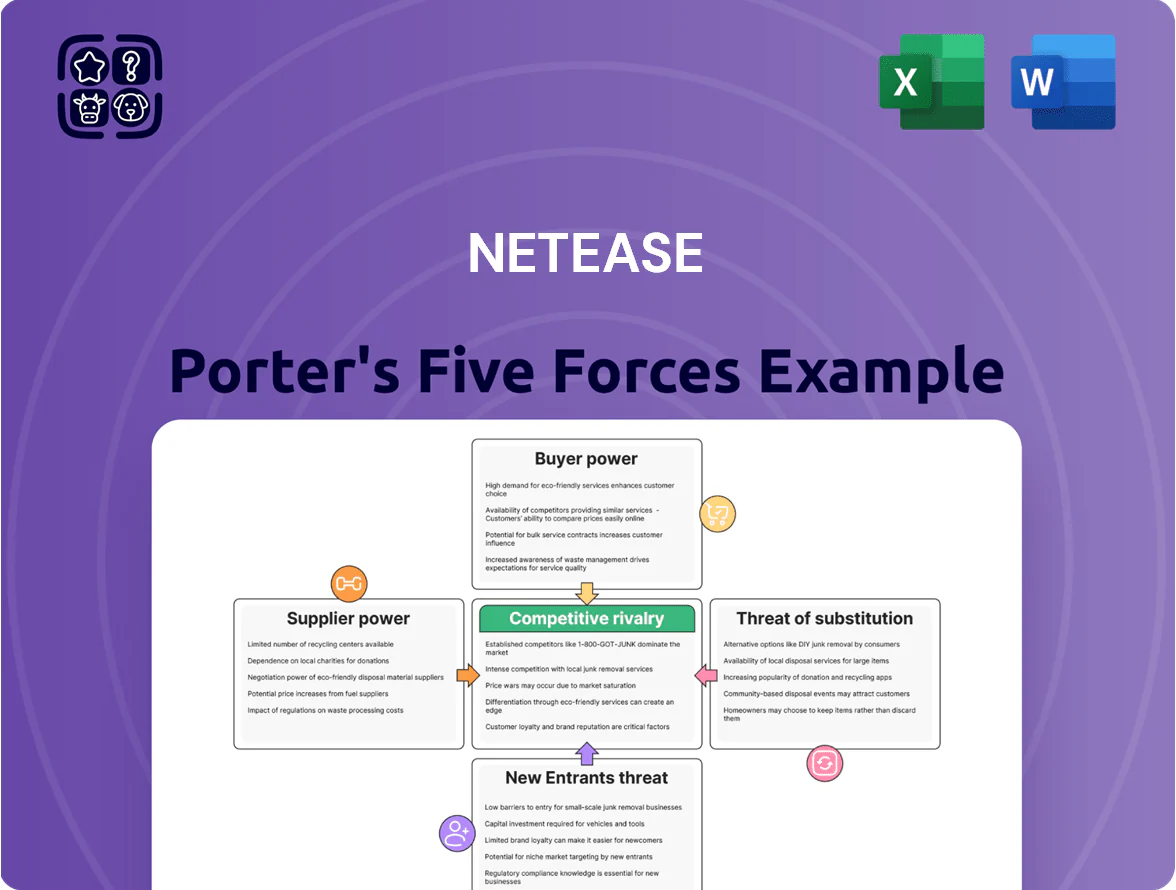

NetEase Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

NetEase operates in a fiercely competitive digital-entertainment and online services market where supplier leverage, buyer expectations, and substitute offerings constantly reshape margins and growth prospects.

This snapshot highlights key pressure points—strong buyer power in gaming platforms, moderate supplier influence, high threat from substitutes and new entrants—but the full Porter's Five Forces Analysis quantifies each force, provides visuals, and outlines strategic implications.

Unlock the complete report to get force-by-force ratings, actionable recommendations, and Excel/Word-ready deliverables to inform investment or strategy decisions.

Suppliers Bargaining Power

Dependency on Global Music Labels

NetEase Cloud Music depends on licensing deals with major global and Chinese labels to keep a competitive catalog; as of Q4 2025, label licensing and royalties consumed about 18–22% of revenue, squeezing EBITDA margins. The platform has grown indie-artist signings to 28% of new releases in 2024, but the Big Three (Universal, Sony, Warner) still command higher royalty rates and negotiating leverage. Copyright costs remain a top operational expense and a key margin risk going into 2026.

Reliance on International Game IPs

Reliance on international IPs like Blizzard (renewed 2023 China deal) gives suppliers high bargaining power because those franchises drive outsized spend—NetEase reported 2024 international-IP titles contributing roughly 30% of mobile game revenue (about $2.1B of $7B total).

Losing a major license would cut high-paying users and engagement quickly; Blizzard-class churn could reduce ARPU and daily active users by double-digit percentages within months, hitting top-line and live-ops monetization hard.

Specialized Technical Talent and AI Researchers

The supply of senior software engineers and AI researchers is tight in China; a 2024 Zhaopin report showed 32% year-on-year shortage in AI talent, keeping supplier bargaining power high for NetEase.

As NetEase adds generative AI to games and online education, demand rises and so does cost: average senior AI engineer pay in 2024 hit ~RMB 650k–900k per year in top cities, raising NetEase’s labor spend.

Competition from Tencent and ByteDance, which each hired 1,000+ AI specialists in 2023–24, forces NetEase into more aggressive equity and cash packages to retain and attract staff.

Game Engine and Hardware Providers

NetEase relies on third-party engines (Unity, Epic Games’ Unreal) for many high-fidelity titles, so sudden license fee hikes—Unity raised key mobile fees in 2023—could hit margins on games that generated RMB 46.3 billion revenue in 2024 for its online services.

It also depends on semiconductors and cloud providers (AWS, Alibaba Cloud); global server GPU supply tightness in 2024 pushed lead times to 20+ weeks, risking launch delays and degraded uptime for massive MMO and live-service titles.

- Dependency: Unity/Unreal licensing exposure

- Financial risk: 2024 online services revenue RMB 46.3B

- Hardware risk: 20+ week GPU/server lead times (2024)

- Cloud reliance: AWS/Alibaba downtime or price rises harm live ops

Mobile App Store Distribution Channels

The Apple App Store and major Android marketplaces control NetEase’s mobile-game distribution, acting as gatekeepers that set rules and fees; Apple and Google still take about 30% on in-app purchases (15% for small developers after 2021 thresholds apply to some), which constrains NetEase’s pricing and margin strategies.

NetEase has piloted direct-download channels in China and cross-platform web launches, but app-store dominance (Apple had 52% global app-store revenue share in 2024) gives platforms outsized leverage over developers and monetization terms.

- Apple/Google ~30% cut (15% for qualifying smaller devs)

- Apple ~52% of 2024 global app-store revenue

- Direct-downloads tested in China, limited outside China

Supplier squeeze: royalties, IP cuts, app-store fees and rising AI talent costs

Suppliers hold high bargaining power: major labels and the Big Three drive music royalties (18–22% of revenue Q4 2025), Blizzard/other international IPs contributed ~30% of 2024 mobile-game revenue (~$2.1B of $7B), Unity/Unreal fee changes and app stores (Apple ~52% app-store revenue 2024; ~30% IAP cut) squeeze margins, and tight AI/engineer labor (senior pay RMB 650k–900k in 2024) raises costs.

| Supplier | Key metric | 2024–2025 |

|---|---|---|

| Music labels | Royalties of revenue | 18–22% (Q4 2025) |

| International IPs | Share of mobile-game rev | ~30% (~$2.1B of $7B, 2024) |

| App stores | Cut on IAP / revenue share | ~30% (Apple 52% app-store rev share, 2024) |

| AI talent | Senior pay (top cities) | RMB 650k–900k/year (2024) |

What is included in the product

Tailored Porter's Five Forces assessment for NetEase that uncovers competitive drivers, supplier and buyer influence, entry barriers, substitutes, and emerging threats shaping its profitability and strategic positioning.

Concise Porter's Five Forces summary for NetEase—spot competitive pressures fast and tailor force intensity to new market data for swift strategic decisions.

Customers Bargaining Power

Low Switching Costs for Casual Gamers

The mobile market’s flood of free-to-play titles means switching costs are near zero for casual gamers; 2024 data shows average monthly churn for casual mobile players exceeded 20%, so players hop to new trends with little financial pain.

Hardcore users stay due to account investment and ARPU (average revenue per user) skew—NetEase reported ARPU of about $18 in 2024—but casual churn forces frequent live-ops and content drops to sustain retention.

Price Sensitivity in E-commerce and Music

Users of NetEase Yanxuan (e-commerce) and Cloud Music are highly price-sensitive because dozens of rivals offer similar goods and freemium streams; Yanxuan faced 2024 gross merchandise value of ~RMB 45.2bn, so small price moves affect volume materially.

In music, Cloud Music’s 2024 paying users ~15.6m can easily switch to Tencent Music (2024 paying users ~88m) if perceived value or exclusives rise, capping NetEase’s pricing power and raising churn risk if subscriptions increase.

Influence of Community Feedback and Social Media

Demand for High Quality and Originality

As China’s gamer base matures, players demand high-production-value titles—complex narratives and advanced graphics—raising development costs and time for NetEase; in 2024 China’s game market reached $45.7 billion, with premium titles growing faster than casual games.

Higher quality expectations make consumers pickier and spend selectively, favoring unique, immersive experiences that boost retention but require bigger upfront investment and risk.

- 2024 China market: $45.7B

- Premium title share: rising YoY (industry reports 2023–24)

- Higher dev cost → longer cycles, bigger risk

- Selective spend boosts ARPU for hits

Sophistication of Institutional Advertisers

Institutional advertisers on NetEase have high bargaining power because they measure precise ROI and can reallocate budgets to rivals like ByteDance's TikTok (over 1.2 billion MAUs worldwide in 2024) or Tencent's WeChat (≈1.3 billion MAUs) when targeting or CPCs are better, pressuring NetEase to invest in analytics and ad tech; NetEase's online advertising revenue fell 2% YoY to RMB 20.4 billion in FY2023, highlighting sensitivity to ad shifts.

- Advertisers track ROI precisely, raising switching risk

- TikTok/WeChat scale (1.2B/1.3B MAUs) draws budgets

- NetEase ad revenue RMB 20.4B in FY2023, down 2% YoY

- Requires continual ad-tech and analytics upgrades

NetEase Faces Buyer Power: High Gamer Churn, Ad Pressure & Competitive Music/Commerce

Buyers hold moderate-to-high power: casual gamers churn >20% monthly (2024), NetEase ARPU ≈ $18 (2024) so live-ops must run; Cloud Music paying users ~15.6M vs Tencent Music ~88M limits pricing; Yanxuan GMV ~RMB45.2B (2024) makes price moves sensitive; NetEase ad revenue RMB20.4B (FY2023) fell 2% YoY as advertisers shift to TikTok/WeChat (1.2B/1.3B MAUs 2024).

| Metric | Value |

|---|---|

| Casual churn | >20% monthly (2024) |

| NetEase ARPU | ≈ $18 (2024) |

| Cloud Music paying | 15.6M (2024) |

| Tencent Music paying | ≈88M (2024) |

| Yanxuan GMV | RMB45.2B (2024) |

| Ad revenue | RMB20.4B FY2023, -2% YoY |

Preview the Actual Deliverable

NetEase Porter's Five Forces Analysis

This preview shows the exact NetEase Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or mockups; fully formatted and ready for download and use the moment you buy.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

A Must-Have Tool for Decision-Makers

NetEase operates in a fiercely competitive digital-entertainment and online services market where supplier leverage, buyer expectations, and substitute offerings constantly reshape margins and growth prospects.

This snapshot highlights key pressure points—strong buyer power in gaming platforms, moderate supplier influence, high threat from substitutes and new entrants—but the full Porter's Five Forces Analysis quantifies each force, provides visuals, and outlines strategic implications.

Unlock the complete report to get force-by-force ratings, actionable recommendations, and Excel/Word-ready deliverables to inform investment or strategy decisions.

Suppliers Bargaining Power

Dependency on Global Music Labels

NetEase Cloud Music depends on licensing deals with major global and Chinese labels to keep a competitive catalog; as of Q4 2025, label licensing and royalties consumed about 18–22% of revenue, squeezing EBITDA margins. The platform has grown indie-artist signings to 28% of new releases in 2024, but the Big Three (Universal, Sony, Warner) still command higher royalty rates and negotiating leverage. Copyright costs remain a top operational expense and a key margin risk going into 2026.

Reliance on International Game IPs

Reliance on international IPs like Blizzard (renewed 2023 China deal) gives suppliers high bargaining power because those franchises drive outsized spend—NetEase reported 2024 international-IP titles contributing roughly 30% of mobile game revenue (about $2.1B of $7B total).

Losing a major license would cut high-paying users and engagement quickly; Blizzard-class churn could reduce ARPU and daily active users by double-digit percentages within months, hitting top-line and live-ops monetization hard.

Specialized Technical Talent and AI Researchers

The supply of senior software engineers and AI researchers is tight in China; a 2024 Zhaopin report showed 32% year-on-year shortage in AI talent, keeping supplier bargaining power high for NetEase.

As NetEase adds generative AI to games and online education, demand rises and so does cost: average senior AI engineer pay in 2024 hit ~RMB 650k–900k per year in top cities, raising NetEase’s labor spend.

Competition from Tencent and ByteDance, which each hired 1,000+ AI specialists in 2023–24, forces NetEase into more aggressive equity and cash packages to retain and attract staff.

Game Engine and Hardware Providers

NetEase relies on third-party engines (Unity, Epic Games’ Unreal) for many high-fidelity titles, so sudden license fee hikes—Unity raised key mobile fees in 2023—could hit margins on games that generated RMB 46.3 billion revenue in 2024 for its online services.

It also depends on semiconductors and cloud providers (AWS, Alibaba Cloud); global server GPU supply tightness in 2024 pushed lead times to 20+ weeks, risking launch delays and degraded uptime for massive MMO and live-service titles.

- Dependency: Unity/Unreal licensing exposure

- Financial risk: 2024 online services revenue RMB 46.3B

- Hardware risk: 20+ week GPU/server lead times (2024)

- Cloud reliance: AWS/Alibaba downtime or price rises harm live ops

Mobile App Store Distribution Channels

The Apple App Store and major Android marketplaces control NetEase’s mobile-game distribution, acting as gatekeepers that set rules and fees; Apple and Google still take about 30% on in-app purchases (15% for small developers after 2021 thresholds apply to some), which constrains NetEase’s pricing and margin strategies.

NetEase has piloted direct-download channels in China and cross-platform web launches, but app-store dominance (Apple had 52% global app-store revenue share in 2024) gives platforms outsized leverage over developers and monetization terms.

- Apple/Google ~30% cut (15% for qualifying smaller devs)

- Apple ~52% of 2024 global app-store revenue

- Direct-downloads tested in China, limited outside China

Supplier squeeze: royalties, IP cuts, app-store fees and rising AI talent costs

Suppliers hold high bargaining power: major labels and the Big Three drive music royalties (18–22% of revenue Q4 2025), Blizzard/other international IPs contributed ~30% of 2024 mobile-game revenue (~$2.1B of $7B), Unity/Unreal fee changes and app stores (Apple ~52% app-store revenue 2024; ~30% IAP cut) squeeze margins, and tight AI/engineer labor (senior pay RMB 650k–900k in 2024) raises costs.

| Supplier | Key metric | 2024–2025 |

|---|---|---|

| Music labels | Royalties of revenue | 18–22% (Q4 2025) |

| International IPs | Share of mobile-game rev | ~30% (~$2.1B of $7B, 2024) |

| App stores | Cut on IAP / revenue share | ~30% (Apple 52% app-store rev share, 2024) |

| AI talent | Senior pay (top cities) | RMB 650k–900k/year (2024) |

What is included in the product

Tailored Porter's Five Forces assessment for NetEase that uncovers competitive drivers, supplier and buyer influence, entry barriers, substitutes, and emerging threats shaping its profitability and strategic positioning.

Concise Porter's Five Forces summary for NetEase—spot competitive pressures fast and tailor force intensity to new market data for swift strategic decisions.

Customers Bargaining Power

Low Switching Costs for Casual Gamers

The mobile market’s flood of free-to-play titles means switching costs are near zero for casual gamers; 2024 data shows average monthly churn for casual mobile players exceeded 20%, so players hop to new trends with little financial pain.

Hardcore users stay due to account investment and ARPU (average revenue per user) skew—NetEase reported ARPU of about $18 in 2024—but casual churn forces frequent live-ops and content drops to sustain retention.

Price Sensitivity in E-commerce and Music

Users of NetEase Yanxuan (e-commerce) and Cloud Music are highly price-sensitive because dozens of rivals offer similar goods and freemium streams; Yanxuan faced 2024 gross merchandise value of ~RMB 45.2bn, so small price moves affect volume materially.

In music, Cloud Music’s 2024 paying users ~15.6m can easily switch to Tencent Music (2024 paying users ~88m) if perceived value or exclusives rise, capping NetEase’s pricing power and raising churn risk if subscriptions increase.

Influence of Community Feedback and Social Media

Demand for High Quality and Originality

As China’s gamer base matures, players demand high-production-value titles—complex narratives and advanced graphics—raising development costs and time for NetEase; in 2024 China’s game market reached $45.7 billion, with premium titles growing faster than casual games.

Higher quality expectations make consumers pickier and spend selectively, favoring unique, immersive experiences that boost retention but require bigger upfront investment and risk.

- 2024 China market: $45.7B

- Premium title share: rising YoY (industry reports 2023–24)

- Higher dev cost → longer cycles, bigger risk

- Selective spend boosts ARPU for hits

Sophistication of Institutional Advertisers

Institutional advertisers on NetEase have high bargaining power because they measure precise ROI and can reallocate budgets to rivals like ByteDance's TikTok (over 1.2 billion MAUs worldwide in 2024) or Tencent's WeChat (≈1.3 billion MAUs) when targeting or CPCs are better, pressuring NetEase to invest in analytics and ad tech; NetEase's online advertising revenue fell 2% YoY to RMB 20.4 billion in FY2023, highlighting sensitivity to ad shifts.

- Advertisers track ROI precisely, raising switching risk

- TikTok/WeChat scale (1.2B/1.3B MAUs) draws budgets

- NetEase ad revenue RMB 20.4B in FY2023, down 2% YoY

- Requires continual ad-tech and analytics upgrades

NetEase Faces Buyer Power: High Gamer Churn, Ad Pressure & Competitive Music/Commerce

Buyers hold moderate-to-high power: casual gamers churn >20% monthly (2024), NetEase ARPU ≈ $18 (2024) so live-ops must run; Cloud Music paying users ~15.6M vs Tencent Music ~88M limits pricing; Yanxuan GMV ~RMB45.2B (2024) makes price moves sensitive; NetEase ad revenue RMB20.4B (FY2023) fell 2% YoY as advertisers shift to TikTok/WeChat (1.2B/1.3B MAUs 2024).

| Metric | Value |

|---|---|

| Casual churn | >20% monthly (2024) |

| NetEase ARPU | ≈ $18 (2024) |

| Cloud Music paying | 15.6M (2024) |

| Tencent Music paying | ≈88M (2024) |

| Yanxuan GMV | RMB45.2B (2024) |

| Ad revenue | RMB20.4B FY2023, -2% YoY |

Preview the Actual Deliverable

NetEase Porter's Five Forces Analysis

This preview shows the exact NetEase Porter’s Five Forces analysis you’ll receive immediately after purchase—no placeholders or mockups; fully formatted and ready for download and use the moment you buy.