NetEase PESTLE Analysis

Your Competitive Advantage Starts with This Report

Explore how political oversight, economic shifts, and rapid tech innovation are reshaping NetEase’s growth prospects in our concise PESTLE snapshot—designed for investors and strategists who need fast, actionable context. Purchase the full PESTLE analysis to access detailed risks, market drivers, and strategic recommendations you can apply immediately.

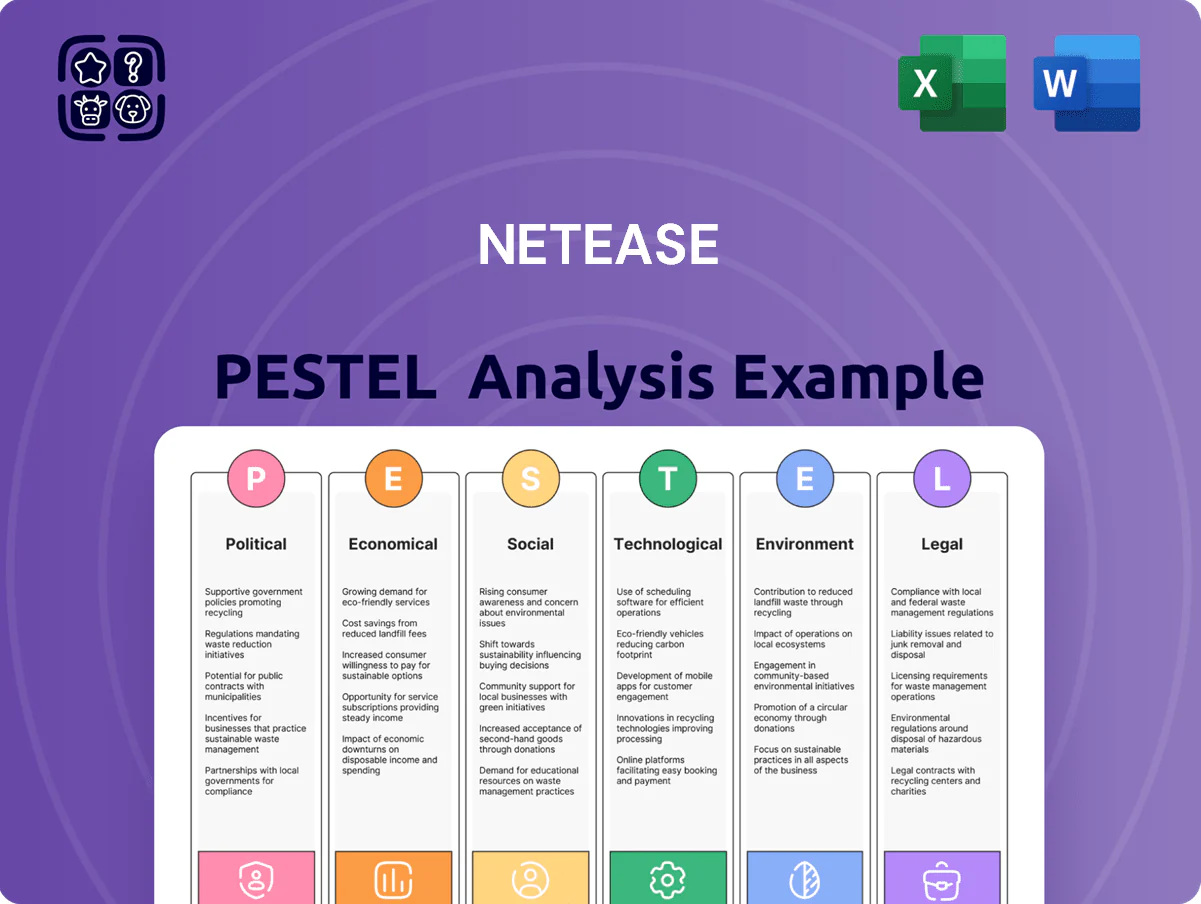

Political factors

Regulatory Oversight of Domestic Gaming

The National Press and Publication Administration exerts strict control over China’s gaming sector, with 2024 approvals dropping to about 3,000 games nationwide and annual licensing quotas tightly managed, directly constraining NetEase’s new title pipeline and monetization timing.

Content censorship and morality reviews force NetEase to redesign mechanics and narratives, adding compliance costs estimated in industry surveys at 5–8% of development budgets, delaying launches and revenue recognition.

By late 2025 regulators emphasize alignment with socialist core values and cultural heritage, influencing IP choices and localization—affecting NetEase’s 2024 domestic revenue of RMB 48.9 billion and future domestic growth trajectory.

Geopolitical Tensions and Global Expansion

NetEase's push into the US and Japan—including its 2023 acquisition of Grasshopper Manufacture minority stakes and multiple studio investments—faces headwinds from China-West tensions; US restrictions on tech investment and a 2024 uptick in export controls raise deal complexity.

Trade barriers and heightened data privacy rules (e.g., Japan's 2023 amendments and evolving US state-level laws) can delay approvals and add compliance costs, impacting M&A timelines and integration.

Navigating diplomatic sensitivities is critical: in 2024 cross-border gaming revenue accounted for a growing share of NetEase's international segment, making geopolitical risk management central to global expansion success.

Government Support for Digital Economy

Despite tighter tech regulations, China still targets 5%+ annual digital economy growth, and state policies promote cloud and AI as strategic priorities—benefiting NetEase which reported RMB 56.2 billion cloud and advertising revenue in FY2024, up ~18% year-on-year.

Focus on Youth Protection Policies

Political pressure to curb gaming addiction led China to enforce playtime limits and real-name verification, reducing under-18 playtime—studies show youth gaming hours fell ~30% since 2019; NetEase reported increased compliance costs, estimating RMB 1.2–1.6bn (2023–24) in tech and monitoring investments.

Continued emphasis on youth physical and mental health remains a revenue risk: regulatory curbs contributed to a 6–8% yoy slowdown in China game revenues for major publishers in 2023–24, pressuring NetEase’s domestic growth.

- Mandatory playtime caps and real-name checks

- NetEase compliance spend ~RMB 1.2–1.6bn (2023–24)

- Regulatory impact: 6–8% yoy China game revenue slowdown (2023–24)

Diplomatic Relations and Licensing Agreements

The ability to license major IP hinges on diplomatic ties between China and partners' home countries; after the 2020 US-China tensions NetEase saw Blizzard partnership restrictions that risked revenue—Blizzard titles accounted for roughly 20% of NetEase’s 2021 gaming revenue before disputes arose.

Political friction can cause delays or termination of publishing deals, as seen when regulatory or diplomatic actions paused cross-border collaborations, threatening millions in annual licensing fees.

NetEase mitigates risk by diversifying its portfolio—own IP, domestic titles, and minority investments—reducing reliance on any single foreign partner and protecting revenue streams from abrupt diplomatic shifts.

- Licensing exposure: ~20% historical revenue from major foreign IP

- Risk: diplomatic tensions can suspend deals, pausing millions in fees

- Mitigation: diversification across owned IP and domestic launches

Regulatory squeeze cuts NetEase game growth; cloud revenue cushions RMB56.2bn

Regulatory approvals fell sharply (≈3,000 approvals nationwide in 2024), tightening NetEase’s release cadence and contributing to a 6–8% yoy domestic game revenue slowdown (2023–24); compliance costs rose (~RMB 1.2–1.6bn 2023–24). Geopolitical tensions and export controls raised M&A complexity and IP risks (historical licensing exposure ~20% of gaming revenue); state AI/cloud support aids NetEase’s RMB 56.2bn FY2024 cloud/ads revenue.

| Metric | Value |

|---|---|

| 2024 game approvals (China) | ≈3,000 |

| NetEase compliance spend (2023–24) | RMB 1.2–1.6bn |

| Domestic game revenue impact | -6–8% yoy |

| Historical licensing exposure | ≈20% gaming rev |

| FY2024 cloud & ads revenue | RMB 56.2bn |

What is included in the product

Explores how macro-environmental factors uniquely impact NetEase across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific examples.

A concise NetEase PESTLE summary that’s visually segmented by category for quick interpretation in meetings, easily dropped into presentations or shared across teams to support external risk discussions and strategic planning.

Economic factors

Consumption Trends in the Chinese Market

NetEase revenue is highly sensitive to Chinese disposable income; mainland household disposable income rose 5.0% in 2024 as per NBS, but consumer confidence remains uneven, pressuring discretionary spends such as in-game purchases that accounted for ~62% of NetEase Interactive Entertainment revenue in FY2023. Post-COVID recovery and structural shifts have moderated spending growth, with music subscription ARPU up modestly while total paid music users reached 80 million in 2024, and economic stability in tier-1/2 cities—where higher penetration of premium tiers exists—remains a key revenue driver.

Impact of Global Inflationary Pressures

Global inflation drove China CPI to 0.3% in 2024 while US core PCE remained ~3.7% YoY, pushing NetEase recruitment and cloud costs up; the company reported R&D and IP-related expenses rising ~14% YoY in FY2024, squeezing gross margins from 39.2% to 37.6%.

Currency Exchange Rate Volatility

As NetEase scales internationally, RMB weaknesses against USD and JPY pose material FX risk: a 5% RMB depreciation versus USD in 2024 would cut reported overseas revenue by roughly 3–4% after translation, given ~30% of 2024 revenue tied to international studios (~RMB 20–25bn). NetEase uses forwards, non-deliverable forwards and FX reserves; hedging reduced FX volatility in 2024, lowering translation loss by ~60% vs unhedged exposure.

Investment Climate in the Tech Sector

The availability of capital and valuations on HK and US markets shape NetEase’s M&A and R&D pace; HK tech index fell ~18% in 2024 while NASDAQ-100 rose ~12%, impacting cross-listing and funding options.

Interest rate shifts—US Fed funds at ~5.25% (2024) —raise NetEase’s cost of debt and can reduce institutional appetite for growth stocks, pressuring buybacks/dividends.

In a cautious climate NetEase may cut discretionary spend; management reduced non-core investments by ~10% in 2024.

- HK tech slump vs US outperformance alters capital access

- Fed rate ~5.25% increases borrowing costs

- Institutional flows favor value, pressuring growth valuations

- Non-core spending trimmed ~10% in 2024

Labor Market Dynamics for Specialized Talent

The economic cost of hiring and retaining top-tier AI researchers and game designers has risen; average tech AI researcher total compensation in China reached about CNY 700k–1.2m in 2024, pressuring NetEase’s payroll.

Competition from Tencent, ByteDance and startups drives wage growth—industry headcount spending on R&D rose ~12% YoY in 2024—creating high-pressure labor markets.

NetEase must balance market-competitive packages with efficiency: optimizing hiring, equity incentives, and productivity to contain personnel cost growth.

- Average AI researcher pay CNY 700k–1.2m (2024)

- Tech R&D payroll +12% YoY (2024)

- Strategies: equity incentives, targeted hiring, productivity metrics

NetEase faces rising R&D pay, RMB drag as disposable income fuels in-game spend

NetEase revenue tied to Chinese disposable income; household disposable income +5.0% (2024) while in-game purchases ~62% of Interactive Entertainment FY2023; CPI 0.3% (2024) pushed R&D/IP costs +14% YoY; RMB weakness (5% vs USD) would cut overseas revenue ~3–4%; Fed funds ~5.25% raised borrowing costs; AI researcher pay CNY 700k–1.2m (2024), R&D payroll +12% YoY.

| Metric | 2024 |

|---|---|

| Disposable income growth | +5.0% |

| CPI | 0.3% |

| R&D/IP cost change | +14% YoY |

| AI researcher pay | CNY 700k–1.2m |

Full Version Awaits

NetEase PESTLE Analysis

The preview shown here is the exact NetEase PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategy or investment work.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Explore how political oversight, economic shifts, and rapid tech innovation are reshaping NetEase’s growth prospects in our concise PESTLE snapshot—designed for investors and strategists who need fast, actionable context. Purchase the full PESTLE analysis to access detailed risks, market drivers, and strategic recommendations you can apply immediately.

Political factors

Regulatory Oversight of Domestic Gaming

The National Press and Publication Administration exerts strict control over China’s gaming sector, with 2024 approvals dropping to about 3,000 games nationwide and annual licensing quotas tightly managed, directly constraining NetEase’s new title pipeline and monetization timing.

Content censorship and morality reviews force NetEase to redesign mechanics and narratives, adding compliance costs estimated in industry surveys at 5–8% of development budgets, delaying launches and revenue recognition.

By late 2025 regulators emphasize alignment with socialist core values and cultural heritage, influencing IP choices and localization—affecting NetEase’s 2024 domestic revenue of RMB 48.9 billion and future domestic growth trajectory.

Geopolitical Tensions and Global Expansion

NetEase's push into the US and Japan—including its 2023 acquisition of Grasshopper Manufacture minority stakes and multiple studio investments—faces headwinds from China-West tensions; US restrictions on tech investment and a 2024 uptick in export controls raise deal complexity.

Trade barriers and heightened data privacy rules (e.g., Japan's 2023 amendments and evolving US state-level laws) can delay approvals and add compliance costs, impacting M&A timelines and integration.

Navigating diplomatic sensitivities is critical: in 2024 cross-border gaming revenue accounted for a growing share of NetEase's international segment, making geopolitical risk management central to global expansion success.

Government Support for Digital Economy

Despite tighter tech regulations, China still targets 5%+ annual digital economy growth, and state policies promote cloud and AI as strategic priorities—benefiting NetEase which reported RMB 56.2 billion cloud and advertising revenue in FY2024, up ~18% year-on-year.

Focus on Youth Protection Policies

Political pressure to curb gaming addiction led China to enforce playtime limits and real-name verification, reducing under-18 playtime—studies show youth gaming hours fell ~30% since 2019; NetEase reported increased compliance costs, estimating RMB 1.2–1.6bn (2023–24) in tech and monitoring investments.

Continued emphasis on youth physical and mental health remains a revenue risk: regulatory curbs contributed to a 6–8% yoy slowdown in China game revenues for major publishers in 2023–24, pressuring NetEase’s domestic growth.

- Mandatory playtime caps and real-name checks

- NetEase compliance spend ~RMB 1.2–1.6bn (2023–24)

- Regulatory impact: 6–8% yoy China game revenue slowdown (2023–24)

Diplomatic Relations and Licensing Agreements

The ability to license major IP hinges on diplomatic ties between China and partners' home countries; after the 2020 US-China tensions NetEase saw Blizzard partnership restrictions that risked revenue—Blizzard titles accounted for roughly 20% of NetEase’s 2021 gaming revenue before disputes arose.

Political friction can cause delays or termination of publishing deals, as seen when regulatory or diplomatic actions paused cross-border collaborations, threatening millions in annual licensing fees.

NetEase mitigates risk by diversifying its portfolio—own IP, domestic titles, and minority investments—reducing reliance on any single foreign partner and protecting revenue streams from abrupt diplomatic shifts.

- Licensing exposure: ~20% historical revenue from major foreign IP

- Risk: diplomatic tensions can suspend deals, pausing millions in fees

- Mitigation: diversification across owned IP and domestic launches

Regulatory squeeze cuts NetEase game growth; cloud revenue cushions RMB56.2bn

Regulatory approvals fell sharply (≈3,000 approvals nationwide in 2024), tightening NetEase’s release cadence and contributing to a 6–8% yoy domestic game revenue slowdown (2023–24); compliance costs rose (~RMB 1.2–1.6bn 2023–24). Geopolitical tensions and export controls raised M&A complexity and IP risks (historical licensing exposure ~20% of gaming revenue); state AI/cloud support aids NetEase’s RMB 56.2bn FY2024 cloud/ads revenue.

| Metric | Value |

|---|---|

| 2024 game approvals (China) | ≈3,000 |

| NetEase compliance spend (2023–24) | RMB 1.2–1.6bn |

| Domestic game revenue impact | -6–8% yoy |

| Historical licensing exposure | ≈20% gaming rev |

| FY2024 cloud & ads revenue | RMB 56.2bn |

What is included in the product

Explores how macro-environmental factors uniquely impact NetEase across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with data-driven trends and region-specific examples.

A concise NetEase PESTLE summary that’s visually segmented by category for quick interpretation in meetings, easily dropped into presentations or shared across teams to support external risk discussions and strategic planning.

Economic factors

Consumption Trends in the Chinese Market

NetEase revenue is highly sensitive to Chinese disposable income; mainland household disposable income rose 5.0% in 2024 as per NBS, but consumer confidence remains uneven, pressuring discretionary spends such as in-game purchases that accounted for ~62% of NetEase Interactive Entertainment revenue in FY2023. Post-COVID recovery and structural shifts have moderated spending growth, with music subscription ARPU up modestly while total paid music users reached 80 million in 2024, and economic stability in tier-1/2 cities—where higher penetration of premium tiers exists—remains a key revenue driver.

Impact of Global Inflationary Pressures

Global inflation drove China CPI to 0.3% in 2024 while US core PCE remained ~3.7% YoY, pushing NetEase recruitment and cloud costs up; the company reported R&D and IP-related expenses rising ~14% YoY in FY2024, squeezing gross margins from 39.2% to 37.6%.

Currency Exchange Rate Volatility

As NetEase scales internationally, RMB weaknesses against USD and JPY pose material FX risk: a 5% RMB depreciation versus USD in 2024 would cut reported overseas revenue by roughly 3–4% after translation, given ~30% of 2024 revenue tied to international studios (~RMB 20–25bn). NetEase uses forwards, non-deliverable forwards and FX reserves; hedging reduced FX volatility in 2024, lowering translation loss by ~60% vs unhedged exposure.

Investment Climate in the Tech Sector

The availability of capital and valuations on HK and US markets shape NetEase’s M&A and R&D pace; HK tech index fell ~18% in 2024 while NASDAQ-100 rose ~12%, impacting cross-listing and funding options.

Interest rate shifts—US Fed funds at ~5.25% (2024) —raise NetEase’s cost of debt and can reduce institutional appetite for growth stocks, pressuring buybacks/dividends.

In a cautious climate NetEase may cut discretionary spend; management reduced non-core investments by ~10% in 2024.

- HK tech slump vs US outperformance alters capital access

- Fed rate ~5.25% increases borrowing costs

- Institutional flows favor value, pressuring growth valuations

- Non-core spending trimmed ~10% in 2024

Labor Market Dynamics for Specialized Talent

The economic cost of hiring and retaining top-tier AI researchers and game designers has risen; average tech AI researcher total compensation in China reached about CNY 700k–1.2m in 2024, pressuring NetEase’s payroll.

Competition from Tencent, ByteDance and startups drives wage growth—industry headcount spending on R&D rose ~12% YoY in 2024—creating high-pressure labor markets.

NetEase must balance market-competitive packages with efficiency: optimizing hiring, equity incentives, and productivity to contain personnel cost growth.

- Average AI researcher pay CNY 700k–1.2m (2024)

- Tech R&D payroll +12% YoY (2024)

- Strategies: equity incentives, targeted hiring, productivity metrics

NetEase faces rising R&D pay, RMB drag as disposable income fuels in-game spend

NetEase revenue tied to Chinese disposable income; household disposable income +5.0% (2024) while in-game purchases ~62% of Interactive Entertainment FY2023; CPI 0.3% (2024) pushed R&D/IP costs +14% YoY; RMB weakness (5% vs USD) would cut overseas revenue ~3–4%; Fed funds ~5.25% raised borrowing costs; AI researcher pay CNY 700k–1.2m (2024), R&D payroll +12% YoY.

| Metric | 2024 |

|---|---|

| Disposable income growth | +5.0% |

| CPI | 0.3% |

| R&D/IP cost change | +14% YoY |

| AI researcher pay | CNY 700k–1.2m |

Full Version Awaits

NetEase PESTLE Analysis

The preview shown here is the exact NetEase PESTLE document you’ll receive after purchase—fully formatted, professionally structured, and ready to use for strategy or investment work.