Cosan Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

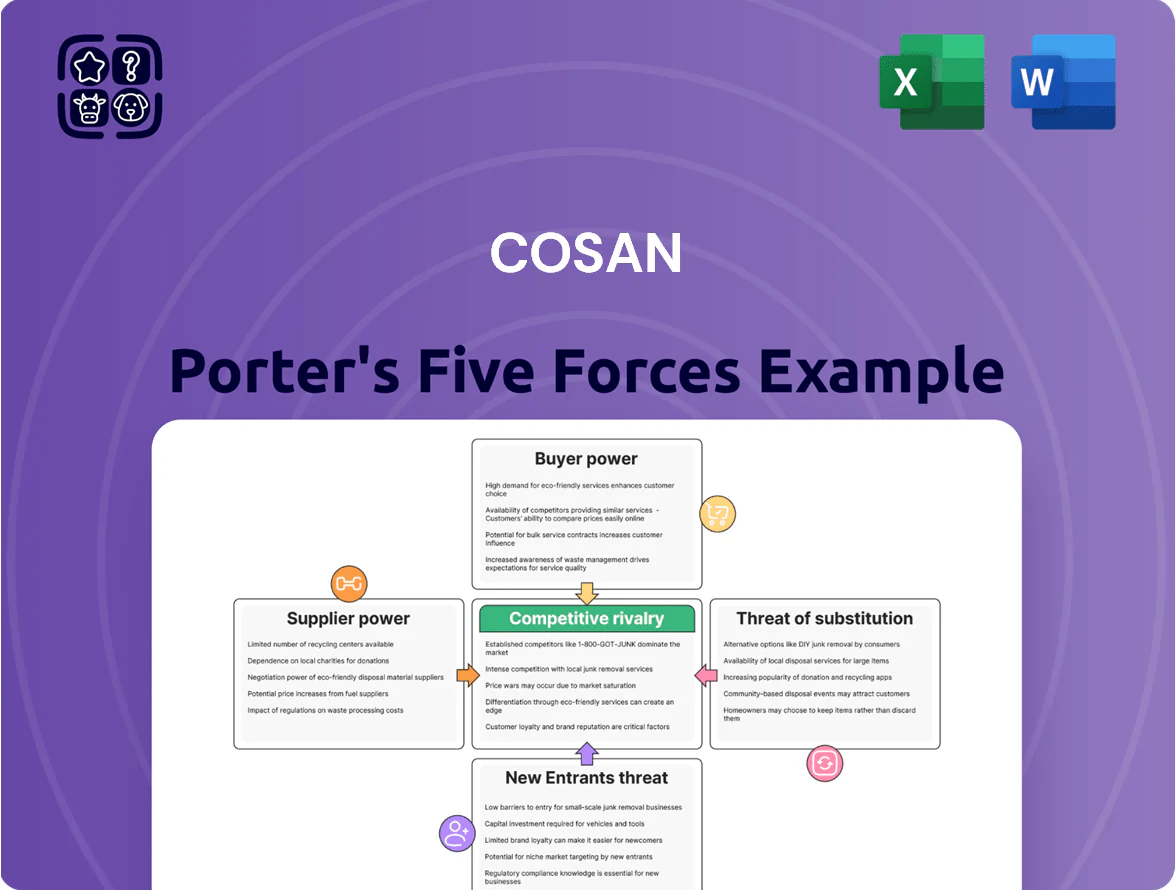

Cosan faces moderate supplier power, intense rivalry across energy and logistics segments, and shifting buyer expectations as ethanol and fuels markets evolve, while substitutes and entry barriers vary by region—this snapshot highlights core pressures shaping strategy and margins. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Cosan’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Sugarcane Producers

Global Commodity Price Volatility

Suppliers of fertilizers, pesticides and machinery—global firms like Bayer and John Deere—wield strong bargaining power because prices track international commodity markets and FX; fertilizer costs rose ~35% YoY in 2023 and remained elevated into 2024, raising input spend for sugarcane growers.

Cosan (ticker CZZ23/COSAN on B3) must absorb or pass on higher input costs to protect margins; a 10% rise in fertilizer prices can cut ethanol gross margin by ~3–5 percentage points given 2024 input-to-revenue ratios.

Energy and Infrastructure Equipment Costs

For Compass and Rumo, a small pool of suppliers for specialized industrial equipment and railway components raises supplier leverage; global rail suppliers account for roughly 60–70% of key parts supply chains. The high technical specs for gas distribution and logistics infrastructure tie Cosan to a few global engineering firms, which charge premium margins—often 10–25% above commodity equivalents. This concentration gives technology and hardware suppliers moderate to high bargaining power, raising CapEx risk for 2024–25 projects.

Labor Market Dynamics and Unionization

Skilled labor in logistics and energy is scarce and highly unionized in Brazil; Cosan faces collective bargaining that in 2024 pushed wage costs up ~8% in transport segments, raising operating expenses and EBITDA pressure.

Strong unions can halt rail or fuel distribution briefly, so stable labor relations are vital to avoid supply-chain outages that would cut revenue across Raízen and Rumo assets.

- High union density in transport: ~30–40% (sector 2024)

- Wage rises ~8% in 2024 collective deals

- Strike risk = direct service disruption, revenue loss

Land Lease and Ownership Regulations

- Key regions: Mato Grosso, São Paulo — 40% sugarcane

- Lease terms: typically 10–30 years

- Land value rise: ~18% (2021–2024)

- Risk: environmental rules force renegotiation

Raízen: 40.8m t cane, dispersed growers blunt supplier power as input costs bite

Suppliers: dispersed 200,000 growers provide ~60% of 2024 cane to Raízen, limiting single-supplier power but allowing large farms to secure premiums during price spikes; Raízen processed 40.8m tonnes in 2024. Input suppliers (fertilizer, machinery) exert high power—fertilizer +35% YoY in 2023 and remained high into 2024—hitting margins ~3–5ppt per 10% fertilizer rise. Rail/equipment vendors and unions (wages +8% in 2024) add moderate–high leverage.

| Metric | 2024 |

|---|---|

| Cane processed (Raízen) | 40.8m t |

| Growers supplying % | ~60% |

| Fertilizer price change | +35% (2023) |

| Wage rises (transport) | +8% |

What is included in the product

Concise Porter's Five Forces review of Cosan, assessing competitive rivalry, supplier and buyer power, threat of substitutes and entry barriers, and identifying strategic pressures and opportunities shaping its profitability.

Concise Porter's Five Forces snapshot for Cosan—clarifies competitive pressures instantly for faster strategic decisions.

Customers Bargaining Power

Wholesale Fuel Market Sensitivity

Through Raízen, Cosan supplies over 7,800 Shell-branded stations and large industrial clients who react strongly to price swings; Brazilian pump-price volatility hit ±8% in 2024, raising sensitivity. The Shell brand gives some loyalty, but fuel is commoditized, so buyers can shift to rivals like Vibra Energia (market share ~18% nationwide in 2024) if price gaps exceed a few cents per liter. That keeps wholesale buyer bargaining power relatively high.

Industrial Gas Contract Structures

Compass Gás e Energia supplies large industrial clients under long-term contracts; in 2024 about 62% of industrial gas volumes were under multi-year agreements, giving customers leverage to demand volume discounts of 5–12% and bespoke delivery SLAs.

Those high-value accounts (top 20 clients ~48% of industrial margin in 2024) make renewals critical; customers often push price reductions or penalty repricing at renewal, increasing Cosan’s revenue volatility if industrial demand drops.

Logistics Dependency and Rumo Services

Customers relying on Rumo’s rail network, notably Brazil’s grain exporters shipping ~90m tonnes in 2024, face scarce long-haul bulk alternatives, which lowers their bargaining power versus Cosan’s fuel segment.

Still, if Rumo’s service declines—delays, higher tariffs—shippers can shift to trucking (road share rose 18% 2019–24) or reroute to competing ports, keeping pressure on pricing and contracts.

Retail Consumer Price Elasticity

Individual motorists can easily switch brands at the pump, giving high bargaining power for brand choice, but they lack leverage to negotiate individual prices.

Collectively, consumers shift to unbranded or discount stations in downturns—Brazil saw fuel-volume share of discount stations rise ~4.5% in 2023 vs 2021.

Cosan counters with loyalty programs (Raízen Posto rewards) and premium fuels; loyalty members delivered ~12% higher ticket in 2024, lowering price elasticity.

- High brand-switching power

- Low individual price negotiation

- 4.5% rise in discount-station share (2021–2023)

- 12% higher spend from loyalty members (2024)

Governmental and Regulatory Oversight

- ANP oversight limits retail markup

- 2024 diesel subsidy talks shifted consumer leverage

- R$120bn fuel-tax revenue underscores state influence

- Alignment with Petrobras pricing reduces intervention risk

High fuel churn risk: commoditized prices, Vibra threat, discounts & tax constraints

Customers exert high bargaining power: fuel is commoditized, pump-price volatility ±8% (2024) and discount stations +4.5% (2021–23) boost switching; Vibra Energia ~18% market share (2024) threatens churn. Industrial buyers (62% under multi-year gas contracts, 2024) extract 5–12% discounts; top 20 clients ~48% industrial margin. ANP oversight and R$120bn fuel-tax revenue (2024) constrain pricing.

| Metric | Value (year) |

|---|---|

| Pump volatility | ±8% (2024) |

| Vibra market share | ~18% (2024) |

| Gas contracts | 62% multi-year (2024) |

| Top20 margin | ~48% (2024) |

| Discount share change | +4.5% (2021–23) |

| Loyalty uplift | +12% ticket (2024) |

| Fuel-tax rev | R$120bn (2024) |

Preview the Actual Deliverable

Cosan Porter's Five Forces Analysis

This preview shows the exact Cosan Porter’s Five Forces analysis you’ll receive after purchase—no placeholders or samples—fully formatted and ready for immediate download and use.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Cosan faces moderate supplier power, intense rivalry across energy and logistics segments, and shifting buyer expectations as ethanol and fuels markets evolve, while substitutes and entry barriers vary by region—this snapshot highlights core pressures shaping strategy and margins. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Cosan’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Sugarcane Producers

Global Commodity Price Volatility

Suppliers of fertilizers, pesticides and machinery—global firms like Bayer and John Deere—wield strong bargaining power because prices track international commodity markets and FX; fertilizer costs rose ~35% YoY in 2023 and remained elevated into 2024, raising input spend for sugarcane growers.

Cosan (ticker CZZ23/COSAN on B3) must absorb or pass on higher input costs to protect margins; a 10% rise in fertilizer prices can cut ethanol gross margin by ~3–5 percentage points given 2024 input-to-revenue ratios.

Energy and Infrastructure Equipment Costs

For Compass and Rumo, a small pool of suppliers for specialized industrial equipment and railway components raises supplier leverage; global rail suppliers account for roughly 60–70% of key parts supply chains. The high technical specs for gas distribution and logistics infrastructure tie Cosan to a few global engineering firms, which charge premium margins—often 10–25% above commodity equivalents. This concentration gives technology and hardware suppliers moderate to high bargaining power, raising CapEx risk for 2024–25 projects.

Labor Market Dynamics and Unionization

Skilled labor in logistics and energy is scarce and highly unionized in Brazil; Cosan faces collective bargaining that in 2024 pushed wage costs up ~8% in transport segments, raising operating expenses and EBITDA pressure.

Strong unions can halt rail or fuel distribution briefly, so stable labor relations are vital to avoid supply-chain outages that would cut revenue across Raízen and Rumo assets.

- High union density in transport: ~30–40% (sector 2024)

- Wage rises ~8% in 2024 collective deals

- Strike risk = direct service disruption, revenue loss

Land Lease and Ownership Regulations

- Key regions: Mato Grosso, São Paulo — 40% sugarcane

- Lease terms: typically 10–30 years

- Land value rise: ~18% (2021–2024)

- Risk: environmental rules force renegotiation

Raízen: 40.8m t cane, dispersed growers blunt supplier power as input costs bite

Suppliers: dispersed 200,000 growers provide ~60% of 2024 cane to Raízen, limiting single-supplier power but allowing large farms to secure premiums during price spikes; Raízen processed 40.8m tonnes in 2024. Input suppliers (fertilizer, machinery) exert high power—fertilizer +35% YoY in 2023 and remained high into 2024—hitting margins ~3–5ppt per 10% fertilizer rise. Rail/equipment vendors and unions (wages +8% in 2024) add moderate–high leverage.

| Metric | 2024 |

|---|---|

| Cane processed (Raízen) | 40.8m t |

| Growers supplying % | ~60% |

| Fertilizer price change | +35% (2023) |

| Wage rises (transport) | +8% |

What is included in the product

Concise Porter's Five Forces review of Cosan, assessing competitive rivalry, supplier and buyer power, threat of substitutes and entry barriers, and identifying strategic pressures and opportunities shaping its profitability.

Concise Porter's Five Forces snapshot for Cosan—clarifies competitive pressures instantly for faster strategic decisions.

Customers Bargaining Power

Wholesale Fuel Market Sensitivity

Through Raízen, Cosan supplies over 7,800 Shell-branded stations and large industrial clients who react strongly to price swings; Brazilian pump-price volatility hit ±8% in 2024, raising sensitivity. The Shell brand gives some loyalty, but fuel is commoditized, so buyers can shift to rivals like Vibra Energia (market share ~18% nationwide in 2024) if price gaps exceed a few cents per liter. That keeps wholesale buyer bargaining power relatively high.

Industrial Gas Contract Structures

Compass Gás e Energia supplies large industrial clients under long-term contracts; in 2024 about 62% of industrial gas volumes were under multi-year agreements, giving customers leverage to demand volume discounts of 5–12% and bespoke delivery SLAs.

Those high-value accounts (top 20 clients ~48% of industrial margin in 2024) make renewals critical; customers often push price reductions or penalty repricing at renewal, increasing Cosan’s revenue volatility if industrial demand drops.

Logistics Dependency and Rumo Services

Customers relying on Rumo’s rail network, notably Brazil’s grain exporters shipping ~90m tonnes in 2024, face scarce long-haul bulk alternatives, which lowers their bargaining power versus Cosan’s fuel segment.

Still, if Rumo’s service declines—delays, higher tariffs—shippers can shift to trucking (road share rose 18% 2019–24) or reroute to competing ports, keeping pressure on pricing and contracts.

Retail Consumer Price Elasticity

Individual motorists can easily switch brands at the pump, giving high bargaining power for brand choice, but they lack leverage to negotiate individual prices.

Collectively, consumers shift to unbranded or discount stations in downturns—Brazil saw fuel-volume share of discount stations rise ~4.5% in 2023 vs 2021.

Cosan counters with loyalty programs (Raízen Posto rewards) and premium fuels; loyalty members delivered ~12% higher ticket in 2024, lowering price elasticity.

- High brand-switching power

- Low individual price negotiation

- 4.5% rise in discount-station share (2021–2023)

- 12% higher spend from loyalty members (2024)

Governmental and Regulatory Oversight

- ANP oversight limits retail markup

- 2024 diesel subsidy talks shifted consumer leverage

- R$120bn fuel-tax revenue underscores state influence

- Alignment with Petrobras pricing reduces intervention risk

High fuel churn risk: commoditized prices, Vibra threat, discounts & tax constraints

Customers exert high bargaining power: fuel is commoditized, pump-price volatility ±8% (2024) and discount stations +4.5% (2021–23) boost switching; Vibra Energia ~18% market share (2024) threatens churn. Industrial buyers (62% under multi-year gas contracts, 2024) extract 5–12% discounts; top 20 clients ~48% industrial margin. ANP oversight and R$120bn fuel-tax revenue (2024) constrain pricing.

| Metric | Value (year) |

|---|---|

| Pump volatility | ±8% (2024) |

| Vibra market share | ~18% (2024) |

| Gas contracts | 62% multi-year (2024) |

| Top20 margin | ~48% (2024) |

| Discount share change | +4.5% (2021–23) |

| Loyalty uplift | +12% ticket (2024) |

| Fuel-tax rev | R$120bn (2024) |

Preview the Actual Deliverable

Cosan Porter's Five Forces Analysis

This preview shows the exact Cosan Porter’s Five Forces analysis you’ll receive after purchase—no placeholders or samples—fully formatted and ready for immediate download and use.