Cosco Shipping Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

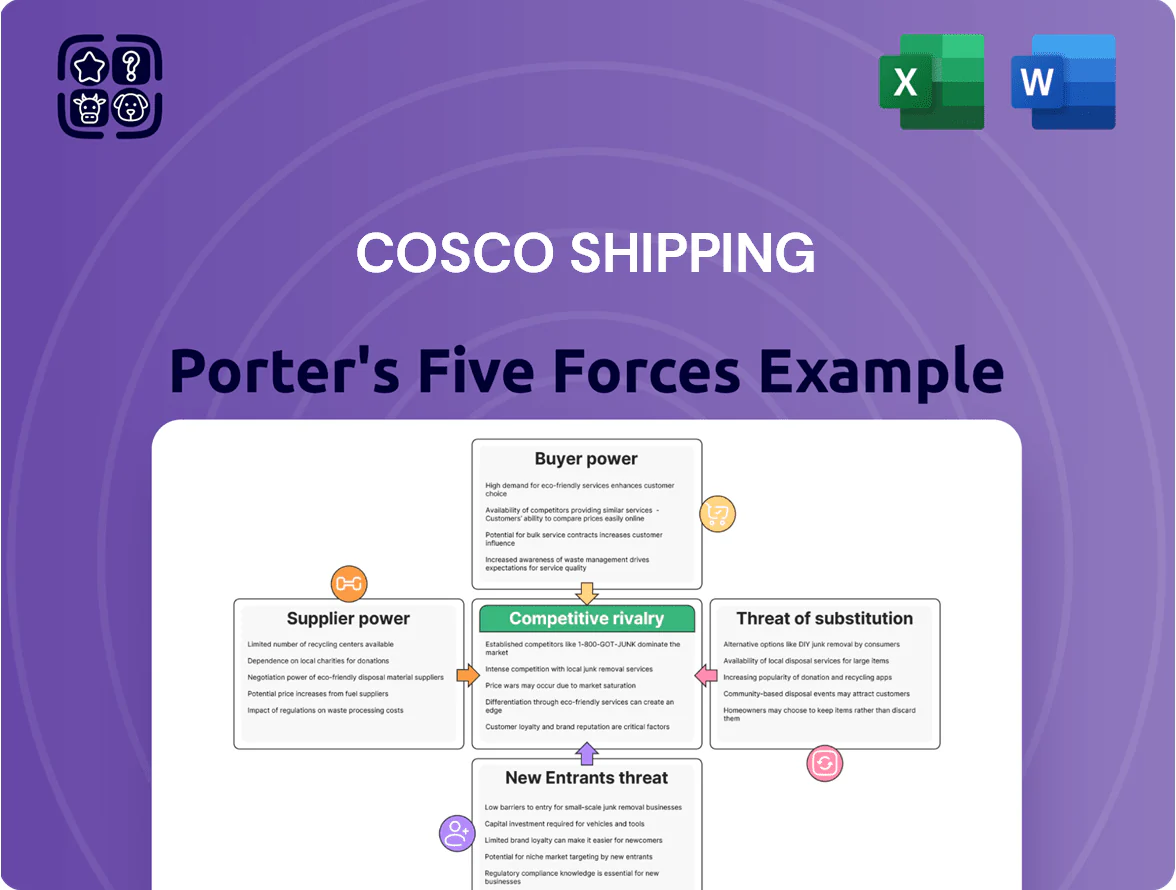

Cosco Shipping navigates intense competitive pressures—high supplier and buyer power, moderate threat from substitutes, and barriers to entry shaped by scale and regulation; strategic assets like global terminals and state backing offer resilience. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Cosco Shipping’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Shipbuilding Capacity

The global shipbuilding market is concentrated: China, South Korea, and Japan built ~90% of newbuilds in 2024, limiting COSCO’s price and delivery leverage versus a few dominant yards.

As the sector shifts to methanol/ammonia-ready ships by late 2025, yards with retrofit expertise command premiums—reported price premia of 10–20% and longer lead times of 12–30 months.

COSCO’s state-owned status gives preferential access to Chinese yards (China’s share ~40% of capacity), but modern high-tech berths for green vessels remain scarce, constraining fleet renewal speed.

Volatility in Marine Fuel and Energy Markets

Bunker fuel is ~20–30% of COSCO Shipping’s vessel opex, so price moves by oil majors and national oil companies bite profitability; Brent 2025 forward at ~$85/bbl raises bunker-linked costs materially.

New 2025 IMO low-sulfur rules concentrate supply: fewer than 15 certified low-sulfur and biofuel producers control major volumes, giving suppliers leverage.

Suppliers now pass carbon levies and production premiums—recent premium for VLSFO averaged $40/ton over HSFO—directly to liners, squeezing margins unless COSCO hedges or secures long-term contracts.

Specialized Green Technology Providers

The global market for maritime decarbonization tech reached $12.8bn in 2024, and patented carbon capture, dual‑fuel engines, and energy‑saving systems are concentrated among few suppliers, limiting COSCO Shipping’s alternative sources for retrofit components.

With IMO 2030/2050 targets and EU ETS costs rising (EU ETS shipping price ~€90/ton in 2025), suppliers command pricing power and long lead times, raising CAPEX per retrofitted vessel by an estimated $8–15m.

This dependency shifts bargaining power to specialized tech firms, forcing COSCO to secure long‑term contracts or equity partnerships to stabilize supply, costs, and compliance timelines.

Port Infrastructure and Terminal Labor

COSCO Shipping controls many terminals but remains exposed to third-party port authorities and unionized labor in Western markets; 2024 IHS Markit data show port labor disputes delayed ~8% of global vessel calls, raising costs by an average $3,200 per TEU during strikes.

Specialized terminal processes and slot constraints limit COSCO’s ability to reroute containers, so sudden tariff hikes or stoppages sharply squeeze margins.

- High dependency on third-party ports

- Union strikes delay ~8% vessel calls (2024)

- Average strike cost ~$3,200/TEU

- Low substitutability of terminals

Access to Specialized Maritime Talent

Global shortage of qualified seafarers—ILO estimated a 4% shortfall in 2024—gives labor agencies and maritime academies more bargaining power over COSCO, especially for crew skilled in alternative fuels and automated bridges.

Higher wages and benefits are required: median specialized seafarer pay rose ~18% in 2023–24, squeezing COSCO’s operating costs and margins across its 1,300+ vessels.

Reduced crew availability limits scheduling flexibility and increases reroute and delay risk, raising voyage costs and capex on training and retention programs.

- ILO 2024: global seafarer shortfall ~4%

- Specialized pay +18% (2023–24)

- COSCO fleet >1,300 vessels—higher crew costs impact margins

Supplier squeeze: shipyards, green-tech & fuel costs force COSCO into long-term ties

Suppliers hold medium–high power: concentrated shipyards (China/Korea/Japan ~90% newbuilds 2024), scarce green-tech vendors (maritime decarb market $12.8bn 2024), bunker/vLSFO price exposure (Brent ~ $85/bbl 2025; VLSFO premium ~$40/ton), and crew shortages (ILO 4% gap 2024) push costs and lead times, forcing COSCO into long-term contracts or equity ties to stabilize supply and CAPEX.

| Metric | Value |

|---|---|

| Newbuild share (2024) | China/Korea/Japan ~90% |

| Decarb market | $12.8bn (2024) |

| Brent (2025F) | $85/bbl |

| VLSFO premium | $40/ton |

| Seafarer gap (2024) | ~4% |

What is included in the product

Tailored Porter’s Five Forces for Cosco Shipping that pinpoints competitive intensity, buyer/supplier leverage, substitution risks, and entry barriers, highlighting strategic threats and opportunities to protect market share.

A concise Porter's Five Forces snapshot for COSCO Shipping—quickly identify competitive threats, supplier/customer leverage, and regulatory pressure to speed strategic decisions.

Customers Bargaining Power

Concentration of Large Scale Retailers

Major retailers and e-commerce giants like Walmart and Amazon move volumes that let them push COSCO on contract terms and freight rates; in 2024 Walmart handled ~$740B in US sales and Amazon ~$560B worldwide, so their bargaining heft is huge.

By end-2025 these Big Box shippers further consolidated logistics, centralizing 30–40% more ocean freight via preferred carriers, and often threaten to switch if COSCO misses price or sustainability targets.

This concentration means losing one large account can cut regional throughput by 5–15% and shave operating profit margins materially, raising COSCO’s customer-concentration risk.

Growth of Digital Freight Platforms

The rise of digital freight platforms has boosted price transparency for SMEs, with platforms like Freightos reporting a 40% increase in instant rate comparisons 2021–2024, letting shippers compare spot rates in real time.

This commoditization lowers customer loyalty, pushing COSCO Shipping (COSCO Shipping Lines) to compete more on price than on service history, seen in a 2023 spot-rate volatility that cut average yields by ~8% on standard Asia-Europe lanes.

As information symmetry improves, maintaining premium margins on standard routes becomes harder; industry data show freight-forwarder market share gains of ~12% among digital adopters, pressuring COSCOs route-level EBIT margins.

Low Switching Costs for Standardized Cargo

For standard containerized cargo, switching from COSCO to Maersk or MSC costs little—spot rates and admin fees are under 2% of freight value for many shippers; 2024 Drewry data showed global 20ft container utilization and port overlap keep service substitutable.

Impact of Global Shipping Alliances

Alliances let carriers manage fleet capacity, but large freight forwarders leverage member overlap to bargain rates down—Drewry reported in 2024 that top 10 forwarders controlled ~45% of boxed export volumes, raising their leverage over carriers like COSCO.

Customers can access COSCO capacity via slot-charter and slot-exchange deals, so shippers often book through intermediaries, not COSCO directly; slot-charter volumes represented about 30% of deployed slots in 2023 on major trade lanes.

This indirect access erodes COSCO’s standalone bargaining power and boosts intermediary margins and negotiating clout, pressuring carrier freight rates and service differentiation.

- Forwarder share: ~45% of export volumes (2024 Drewry)

- Slot-charter share: ~30% of slots (2023 majors)

- Effect: weakens COSCO pricing power, raises intermediary leverage

Demands for Green Supply Chain Transparency

By 2025, corporate buyers facing Scope 3 reporting rules (eg, SEC climate rule draft, EU CSRD) pressure COSCO to offer low-carbon shipping, shifting selection toward carriers with verified emissions data.

Large shippers can blacklist carriers, so COSCO must invest in green tech—LNG, biofuels, shore power—raising capex and OPEX to meet customer standards.

This customer-driven demand centralizes environmental criteria across the logistics chain, effectively transferring bargaining power to buyers who set carrier ESG thresholds.

- Scope 3 reporting drives demand; 90% of emissions often in Scope 3

- Preferred-carrier status tied to verified ETS/IMO DCS data

- Capex hit: fleet decarbonization can cost carriers 10–30% of vessel value

Forwarders, retailers and digital platforms squeeze COSCO—slot loss and spot volatility dent margins

Large retailers and freight forwarders wield strong bargaining power vs COSCO: top 10 forwarders control ~45% of export volumes (Drewry 2024), slot-charters ~30% of slots (2023), and losing a big account can cut regional throughput 5–15%, trimming margins; digital platforms raised instant rate comparisons 40% (2021–24), and spot-rate volatility cut yields ~8% (2023).

| Metric | Value |

|---|---|

| Top-10 forwarder share (2024) | ~45% |

| Slot-charter share (2023) | ~30% |

| Throughput loss if major account exits | 5–15% |

| Instant rate comparisons rise (2021–24) | +40% |

| Spot-rate yield hit (2023) | ~-8% |

What You See Is What You Get

Cosco Shipping Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Cosco Shipping you’ll receive immediately after purchase—no placeholders, no mockups, fully formatted and ready to use.

It’s the complete document: in-depth assessment of competitive rivalry, supplier and buyer power, threat of entrants and substitutes, and strategic implications—available for instant download upon payment.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Cosco Shipping navigates intense competitive pressures—high supplier and buyer power, moderate threat from substitutes, and barriers to entry shaped by scale and regulation; strategic assets like global terminals and state backing offer resilience. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Cosco Shipping’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Shipbuilding Capacity

The global shipbuilding market is concentrated: China, South Korea, and Japan built ~90% of newbuilds in 2024, limiting COSCO’s price and delivery leverage versus a few dominant yards.

As the sector shifts to methanol/ammonia-ready ships by late 2025, yards with retrofit expertise command premiums—reported price premia of 10–20% and longer lead times of 12–30 months.

COSCO’s state-owned status gives preferential access to Chinese yards (China’s share ~40% of capacity), but modern high-tech berths for green vessels remain scarce, constraining fleet renewal speed.

Volatility in Marine Fuel and Energy Markets

Bunker fuel is ~20–30% of COSCO Shipping’s vessel opex, so price moves by oil majors and national oil companies bite profitability; Brent 2025 forward at ~$85/bbl raises bunker-linked costs materially.

New 2025 IMO low-sulfur rules concentrate supply: fewer than 15 certified low-sulfur and biofuel producers control major volumes, giving suppliers leverage.

Suppliers now pass carbon levies and production premiums—recent premium for VLSFO averaged $40/ton over HSFO—directly to liners, squeezing margins unless COSCO hedges or secures long-term contracts.

Specialized Green Technology Providers

The global market for maritime decarbonization tech reached $12.8bn in 2024, and patented carbon capture, dual‑fuel engines, and energy‑saving systems are concentrated among few suppliers, limiting COSCO Shipping’s alternative sources for retrofit components.

With IMO 2030/2050 targets and EU ETS costs rising (EU ETS shipping price ~€90/ton in 2025), suppliers command pricing power and long lead times, raising CAPEX per retrofitted vessel by an estimated $8–15m.

This dependency shifts bargaining power to specialized tech firms, forcing COSCO to secure long‑term contracts or equity partnerships to stabilize supply, costs, and compliance timelines.

Port Infrastructure and Terminal Labor

COSCO Shipping controls many terminals but remains exposed to third-party port authorities and unionized labor in Western markets; 2024 IHS Markit data show port labor disputes delayed ~8% of global vessel calls, raising costs by an average $3,200 per TEU during strikes.

Specialized terminal processes and slot constraints limit COSCO’s ability to reroute containers, so sudden tariff hikes or stoppages sharply squeeze margins.

- High dependency on third-party ports

- Union strikes delay ~8% vessel calls (2024)

- Average strike cost ~$3,200/TEU

- Low substitutability of terminals

Access to Specialized Maritime Talent

Global shortage of qualified seafarers—ILO estimated a 4% shortfall in 2024—gives labor agencies and maritime academies more bargaining power over COSCO, especially for crew skilled in alternative fuels and automated bridges.

Higher wages and benefits are required: median specialized seafarer pay rose ~18% in 2023–24, squeezing COSCO’s operating costs and margins across its 1,300+ vessels.

Reduced crew availability limits scheduling flexibility and increases reroute and delay risk, raising voyage costs and capex on training and retention programs.

- ILO 2024: global seafarer shortfall ~4%

- Specialized pay +18% (2023–24)

- COSCO fleet >1,300 vessels—higher crew costs impact margins

Supplier squeeze: shipyards, green-tech & fuel costs force COSCO into long-term ties

Suppliers hold medium–high power: concentrated shipyards (China/Korea/Japan ~90% newbuilds 2024), scarce green-tech vendors (maritime decarb market $12.8bn 2024), bunker/vLSFO price exposure (Brent ~ $85/bbl 2025; VLSFO premium ~$40/ton), and crew shortages (ILO 4% gap 2024) push costs and lead times, forcing COSCO into long-term contracts or equity ties to stabilize supply and CAPEX.

| Metric | Value |

|---|---|

| Newbuild share (2024) | China/Korea/Japan ~90% |

| Decarb market | $12.8bn (2024) |

| Brent (2025F) | $85/bbl |

| VLSFO premium | $40/ton |

| Seafarer gap (2024) | ~4% |

What is included in the product

Tailored Porter’s Five Forces for Cosco Shipping that pinpoints competitive intensity, buyer/supplier leverage, substitution risks, and entry barriers, highlighting strategic threats and opportunities to protect market share.

A concise Porter's Five Forces snapshot for COSCO Shipping—quickly identify competitive threats, supplier/customer leverage, and regulatory pressure to speed strategic decisions.

Customers Bargaining Power

Concentration of Large Scale Retailers

Major retailers and e-commerce giants like Walmart and Amazon move volumes that let them push COSCO on contract terms and freight rates; in 2024 Walmart handled ~$740B in US sales and Amazon ~$560B worldwide, so their bargaining heft is huge.

By end-2025 these Big Box shippers further consolidated logistics, centralizing 30–40% more ocean freight via preferred carriers, and often threaten to switch if COSCO misses price or sustainability targets.

This concentration means losing one large account can cut regional throughput by 5–15% and shave operating profit margins materially, raising COSCO’s customer-concentration risk.

Growth of Digital Freight Platforms

The rise of digital freight platforms has boosted price transparency for SMEs, with platforms like Freightos reporting a 40% increase in instant rate comparisons 2021–2024, letting shippers compare spot rates in real time.

This commoditization lowers customer loyalty, pushing COSCO Shipping (COSCO Shipping Lines) to compete more on price than on service history, seen in a 2023 spot-rate volatility that cut average yields by ~8% on standard Asia-Europe lanes.

As information symmetry improves, maintaining premium margins on standard routes becomes harder; industry data show freight-forwarder market share gains of ~12% among digital adopters, pressuring COSCOs route-level EBIT margins.

Low Switching Costs for Standardized Cargo

For standard containerized cargo, switching from COSCO to Maersk or MSC costs little—spot rates and admin fees are under 2% of freight value for many shippers; 2024 Drewry data showed global 20ft container utilization and port overlap keep service substitutable.

Impact of Global Shipping Alliances

Alliances let carriers manage fleet capacity, but large freight forwarders leverage member overlap to bargain rates down—Drewry reported in 2024 that top 10 forwarders controlled ~45% of boxed export volumes, raising their leverage over carriers like COSCO.

Customers can access COSCO capacity via slot-charter and slot-exchange deals, so shippers often book through intermediaries, not COSCO directly; slot-charter volumes represented about 30% of deployed slots in 2023 on major trade lanes.

This indirect access erodes COSCO’s standalone bargaining power and boosts intermediary margins and negotiating clout, pressuring carrier freight rates and service differentiation.

- Forwarder share: ~45% of export volumes (2024 Drewry)

- Slot-charter share: ~30% of slots (2023 majors)

- Effect: weakens COSCO pricing power, raises intermediary leverage

Demands for Green Supply Chain Transparency

By 2025, corporate buyers facing Scope 3 reporting rules (eg, SEC climate rule draft, EU CSRD) pressure COSCO to offer low-carbon shipping, shifting selection toward carriers with verified emissions data.

Large shippers can blacklist carriers, so COSCO must invest in green tech—LNG, biofuels, shore power—raising capex and OPEX to meet customer standards.

This customer-driven demand centralizes environmental criteria across the logistics chain, effectively transferring bargaining power to buyers who set carrier ESG thresholds.

- Scope 3 reporting drives demand; 90% of emissions often in Scope 3

- Preferred-carrier status tied to verified ETS/IMO DCS data

- Capex hit: fleet decarbonization can cost carriers 10–30% of vessel value

Forwarders, retailers and digital platforms squeeze COSCO—slot loss and spot volatility dent margins

Large retailers and freight forwarders wield strong bargaining power vs COSCO: top 10 forwarders control ~45% of export volumes (Drewry 2024), slot-charters ~30% of slots (2023), and losing a big account can cut regional throughput 5–15%, trimming margins; digital platforms raised instant rate comparisons 40% (2021–24), and spot-rate volatility cut yields ~8% (2023).

| Metric | Value |

|---|---|

| Top-10 forwarder share (2024) | ~45% |

| Slot-charter share (2023) | ~30% |

| Throughput loss if major account exits | 5–15% |

| Instant rate comparisons rise (2021–24) | +40% |

| Spot-rate yield hit (2023) | ~-8% |

What You See Is What You Get

Cosco Shipping Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis of Cosco Shipping you’ll receive immediately after purchase—no placeholders, no mockups, fully formatted and ready to use.

It’s the complete document: in-depth assessment of competitive rivalry, supplier and buyer power, threat of entrants and substitutes, and strategic implications—available for instant download upon payment.