OTE S.A. SWOT Analysis

Make Insightful Decisions Backed by Expert Research

OTE S.A. shows resilient market standing with strong telecom infrastructure and diversified services, yet faces regulatory pressure and intensifying competition; our full SWOT unpacks operational strengths, strategic threats, and growth levers to inform investment or strategic moves—purchase the complete report for a professionally formatted, editable Word and Excel package that accelerates research, planning, and presentations.

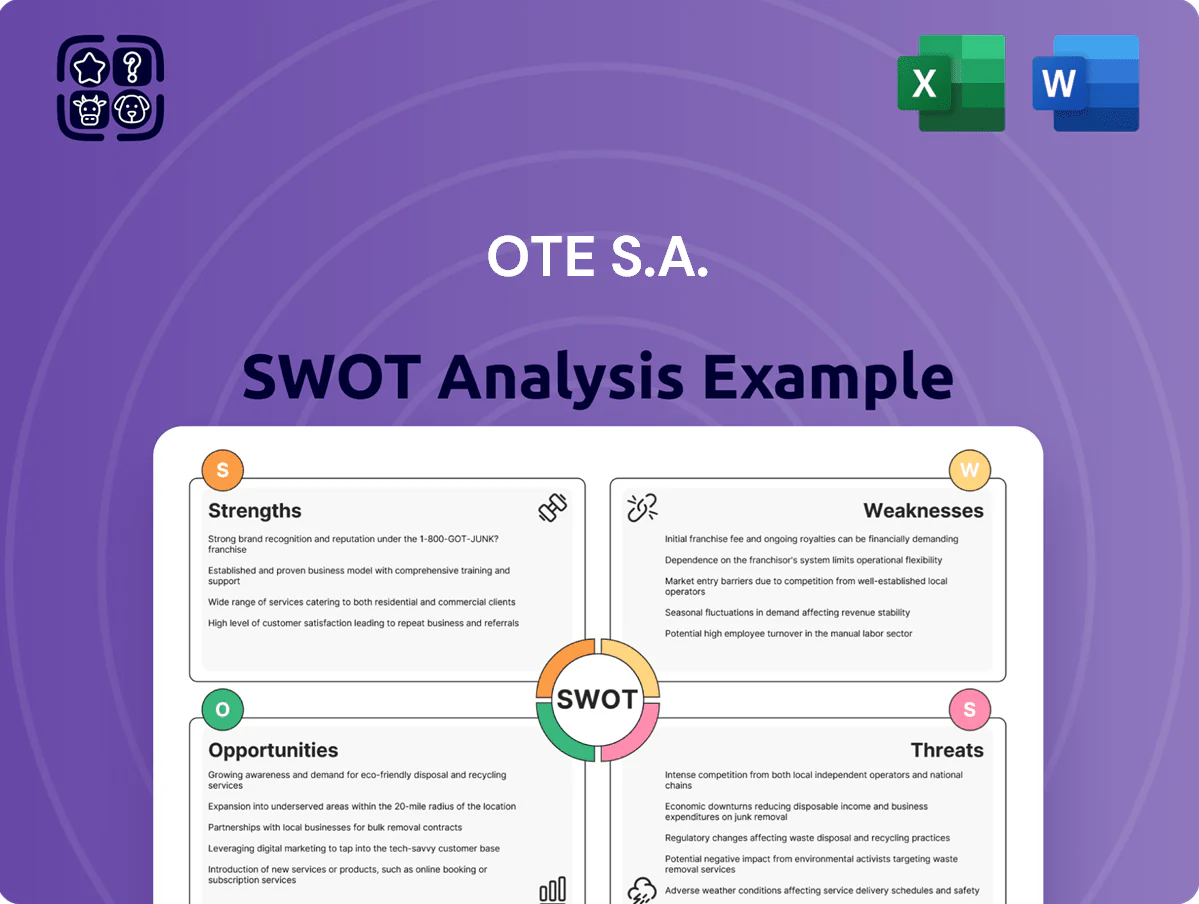

Strengths

Dominant Market Leadership in Greece

OTE, via Cosmote, holds leading shares in Greece: ~40% mobile, ~55% fixed broadband, and ~48% fixed voice market share as of 2025, giving strong customer loyalty and cross-sell reach.

High scale cuts unit costs—2025 EBITDA margin for Hellenic Telecoms segment was ~36.5%, supporting reinvestment and competitive pricing versus smaller rivals.

Incumbency kept ARPU resilient: mobile ARPU ~12.8 EUR/month and broadband churn under 9% in 2025, retaining high-value subscribers despite aggressive competition.

Strategic Partnership with Deutsche Telekom

Deutsche Telekom, as OTE S.A.’s majority shareholder since 2008, brings financial backing—helping OTE report net debt/EBITDA of 1.2x in FY2024—and supplies technical know-how and global procurement scale that cut capex unit costs by an estimated 8–12% versus peers.

That tie speeds OTE’s rollout of FTTH and 5G, reflected in 2024 capex of €477m and a 48% fiber household coverage, and boosts credit metrics—OTE held a BBB+ equivalent rating in 2025—improving access to international capital.

Extensive Fiber and 5G Infrastructure

OTE S.A. has invested over €3.2 billion since 2020 in Fiber to the Home (FTTH) and 5G, giving it ~65% national FTTH household coverage and 80% 5G population coverage by late 2025—highest in Greece.

This infrastructure delivers peak consumer speeds >1 Gbps and enterprise SLAs with 99.99% uptime, supporting cloud, IoT, and fixed-mobile convergence services.

Integrated ICT Service Portfolio

OTE S.A. has shifted from voice to full ICT, offering cloud, cybersecurity, and national-scale digital projects, reporting 2024 ICT revenues of ~€1.1bn—around 28% of group service sales—cutting dependence on shrinking voice margins.

This diversification positions OTE as a pillar of Greece’s digital economy, winning public-sector contracts (multi-year deals >€200m) and growing enterprise cloud customers by 18% YoY in 2024.

- 2024 ICT revenue ~€1.1bn

- ICT = 28% of service sales

- Enterprise cloud customers +18% YoY (2024)

- Public deals >€200m

Resilient Financial Profile and Cash Flow

- EBITDA margin 33.8% (FY2024)

- Free cash flow €420m (FY2024)

- Dividend €0.30/share; reinvestment €250m

- Net debt/EBITDA ~1.8x; adjusted EBITDA +5.6% YoY

Greek telecom leader: strong margins, €420m FCF, 65% FTTH & 80% 5G

Market leader in Greece (mobile ~40%, fixed broadband ~55%), high 2024 EBITDA margin 33.8%, strong cash flow (€420m FCF) and low leverage (net debt/EBITDA ~1.8x); Deutsche Telekom backing enabled €3.2bn capex since 2020, 65% FTTH and 80% 5G coverage (late 2025), and ICT revenue ~€1.1bn (28% service sales).

| Metric | Value |

|---|---|

| Mobile share | ~40% |

| Fixed broadband | ~55% |

| EBITDA margin (2024) | 33.8% |

| FCF (2024) | €420m |

| Net debt/EBITDA | ~1.8x |

| FTTH coverage | ~65% |

| 5G coverage | ~80% |

| ICT revenue (2024) | €1.1bn (28%) |

What is included in the product

Provides a concise SWOT overview of OTE S.A., highlighting its core strengths, operational weaknesses, market opportunities, and external threats shaping strategic decisions.

Provides a concise SWOT matrix for OTE S.A. to quickly align telecom strategy and regulatory responses.

Weaknesses

High Capital Expenditure Requirements

Maintaining a tech lead forces OTE S.A. to commit heavy CAPEX—EUR 1.1bn spent on fixed network and spectrum in 2024 and planned EUR 1.0–1.2bn annually through 2026 for FTTH and 6G trials—reducing free cash flow and room for M&A or faster debt paydown; net debt/EBITDA was ~2.6x at FY2024, so management must weigh network superiority against dividend and deleverage expectations.

Dependency on the Greek Economy

OTE S.A. derives around 65% of 2024 revenue from Greece, so domestic shocks hit top-line hard; a 1% Greek GDP drop (GDP -4.5% in 2020, recovered to +2.0% in 2023) tends to slow subscription additions and cut ARPU.

Household consumption swings and high Greek unemployment (12.4% in 2024) depress pay-TV and broadband uptake, directly lowering OTE’s service margins and cash flow.

Lack of geographic diversification vs multinationals means country-specific fiscal, regulatory, or currency risks are concentrated; international peers dilute such shocks across markets.

Legacy Infrastructure Maintenance Costs

OTE S.A. still operates extensive legacy copper networks that raised maintenance costs to about €120–150 million in 2024, versus lower unit costs for fiber, and these aging lines deliver lower bandwidth and higher fault rates. Transitioning customers to fiber involves OPEX and CAPEX spikes—estimated €200–300 per household migrated—and risks service interruptions that can increase churn. Running dual copper and fiber networks complicates technical support, stretches workforce allocation, and raised maintenance headcount by ~12% in 2024. This mix limits operational efficiency and delays full upgrade ROI.

Rigid Regulatory Environment

- Regulatory caps slowed tariff moves vs rivals

- ~15% of broadband pricing subject to NRA actions (2024)

- €72m regulatory compliance cost (OTE, 2024)

- GDPR and EU telecom rules increase legal/admin burden

Exposure to Intense Pricing Competition

OTE faces intense price competition in Greece, where the top three operators ran aggressive promotions in 2024–2025, driving mobile ARPU down ~6% YoY to about €9.5 in Q4 2024 for prepaid users according to Hellenic Telecommunications Organization data.

Pressure is strongest in mobile and prepaid segments, forcing OTE to invest in product differentiation, bundled services, and network upgrades to justify premium pricing and curb churn to lower-cost rivals.

Failure to innovate quickly could erode EBITDA margins (OTE Group reported 2024 EBITDA margin ~30%), so retention and value-added upsells are critical.

- Top-3 price wars cut mobile ARPU ~6% YoY

- Prepaid ARPU ~€9.5 (Q4 2024)

- OTE 2024 EBITDA margin ~30%

Heavy CAPEX, high Greek exposure & falling ARPU squeeze cash flow and M&A firepower

Heavy CAPEX (EUR 1.1bn in 2024; EUR 1.0–1.2bn p.a. planned) squeezes free cash flow and M&A room; net debt/EBITDA ~2.6x (FY2024). Revenue concentration: ~65% from Greece, high unemployment 12.4% (2024) and GDP volatility hurt ARPU and additions. Legacy copper raised maintenance ~€120–150m (2024) and migration costs €200–300/household. Regulatory costs €72m (2024); mobile ARPU fell ~6% YoY to €9.5 (Q4 2024).

| Metric | 2024 value |

|---|---|

| CAPEX | €1.1bn |

| Planned CAPEX (2025–26) | €1.0–1.2bn p.a. |

| Net debt/EBITDA | ~2.6x |

| Greece revenue share | ~65% |

| Unemployment (Greece) | 12.4% |

| Copper maintenance | €120–150m |

| Migration cost/household | €200–300 |

| Regulatory compliance | €72m |

| Prepaid ARPU (Q4) | €9.5 (-6% YoY) |

Full Version Awaits

OTE S.A. SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth version. You’re viewing a live preview of the actual SWOT analysis file, and the complete, editable document becomes available after checkout.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Make Insightful Decisions Backed by Expert Research

OTE S.A. shows resilient market standing with strong telecom infrastructure and diversified services, yet faces regulatory pressure and intensifying competition; our full SWOT unpacks operational strengths, strategic threats, and growth levers to inform investment or strategic moves—purchase the complete report for a professionally formatted, editable Word and Excel package that accelerates research, planning, and presentations.

Strengths

Dominant Market Leadership in Greece

OTE, via Cosmote, holds leading shares in Greece: ~40% mobile, ~55% fixed broadband, and ~48% fixed voice market share as of 2025, giving strong customer loyalty and cross-sell reach.

High scale cuts unit costs—2025 EBITDA margin for Hellenic Telecoms segment was ~36.5%, supporting reinvestment and competitive pricing versus smaller rivals.

Incumbency kept ARPU resilient: mobile ARPU ~12.8 EUR/month and broadband churn under 9% in 2025, retaining high-value subscribers despite aggressive competition.

Strategic Partnership with Deutsche Telekom

Deutsche Telekom, as OTE S.A.’s majority shareholder since 2008, brings financial backing—helping OTE report net debt/EBITDA of 1.2x in FY2024—and supplies technical know-how and global procurement scale that cut capex unit costs by an estimated 8–12% versus peers.

That tie speeds OTE’s rollout of FTTH and 5G, reflected in 2024 capex of €477m and a 48% fiber household coverage, and boosts credit metrics—OTE held a BBB+ equivalent rating in 2025—improving access to international capital.

Extensive Fiber and 5G Infrastructure

OTE S.A. has invested over €3.2 billion since 2020 in Fiber to the Home (FTTH) and 5G, giving it ~65% national FTTH household coverage and 80% 5G population coverage by late 2025—highest in Greece.

This infrastructure delivers peak consumer speeds >1 Gbps and enterprise SLAs with 99.99% uptime, supporting cloud, IoT, and fixed-mobile convergence services.

Integrated ICT Service Portfolio

OTE S.A. has shifted from voice to full ICT, offering cloud, cybersecurity, and national-scale digital projects, reporting 2024 ICT revenues of ~€1.1bn—around 28% of group service sales—cutting dependence on shrinking voice margins.

This diversification positions OTE as a pillar of Greece’s digital economy, winning public-sector contracts (multi-year deals >€200m) and growing enterprise cloud customers by 18% YoY in 2024.

- 2024 ICT revenue ~€1.1bn

- ICT = 28% of service sales

- Enterprise cloud customers +18% YoY (2024)

- Public deals >€200m

Resilient Financial Profile and Cash Flow

- EBITDA margin 33.8% (FY2024)

- Free cash flow €420m (FY2024)

- Dividend €0.30/share; reinvestment €250m

- Net debt/EBITDA ~1.8x; adjusted EBITDA +5.6% YoY

Greek telecom leader: strong margins, €420m FCF, 65% FTTH & 80% 5G

Market leader in Greece (mobile ~40%, fixed broadband ~55%), high 2024 EBITDA margin 33.8%, strong cash flow (€420m FCF) and low leverage (net debt/EBITDA ~1.8x); Deutsche Telekom backing enabled €3.2bn capex since 2020, 65% FTTH and 80% 5G coverage (late 2025), and ICT revenue ~€1.1bn (28% service sales).

| Metric | Value |

|---|---|

| Mobile share | ~40% |

| Fixed broadband | ~55% |

| EBITDA margin (2024) | 33.8% |

| FCF (2024) | €420m |

| Net debt/EBITDA | ~1.8x |

| FTTH coverage | ~65% |

| 5G coverage | ~80% |

| ICT revenue (2024) | €1.1bn (28%) |

What is included in the product

Provides a concise SWOT overview of OTE S.A., highlighting its core strengths, operational weaknesses, market opportunities, and external threats shaping strategic decisions.

Provides a concise SWOT matrix for OTE S.A. to quickly align telecom strategy and regulatory responses.

Weaknesses

High Capital Expenditure Requirements

Maintaining a tech lead forces OTE S.A. to commit heavy CAPEX—EUR 1.1bn spent on fixed network and spectrum in 2024 and planned EUR 1.0–1.2bn annually through 2026 for FTTH and 6G trials—reducing free cash flow and room for M&A or faster debt paydown; net debt/EBITDA was ~2.6x at FY2024, so management must weigh network superiority against dividend and deleverage expectations.

Dependency on the Greek Economy

OTE S.A. derives around 65% of 2024 revenue from Greece, so domestic shocks hit top-line hard; a 1% Greek GDP drop (GDP -4.5% in 2020, recovered to +2.0% in 2023) tends to slow subscription additions and cut ARPU.

Household consumption swings and high Greek unemployment (12.4% in 2024) depress pay-TV and broadband uptake, directly lowering OTE’s service margins and cash flow.

Lack of geographic diversification vs multinationals means country-specific fiscal, regulatory, or currency risks are concentrated; international peers dilute such shocks across markets.

Legacy Infrastructure Maintenance Costs

OTE S.A. still operates extensive legacy copper networks that raised maintenance costs to about €120–150 million in 2024, versus lower unit costs for fiber, and these aging lines deliver lower bandwidth and higher fault rates. Transitioning customers to fiber involves OPEX and CAPEX spikes—estimated €200–300 per household migrated—and risks service interruptions that can increase churn. Running dual copper and fiber networks complicates technical support, stretches workforce allocation, and raised maintenance headcount by ~12% in 2024. This mix limits operational efficiency and delays full upgrade ROI.

Rigid Regulatory Environment

- Regulatory caps slowed tariff moves vs rivals

- ~15% of broadband pricing subject to NRA actions (2024)

- €72m regulatory compliance cost (OTE, 2024)

- GDPR and EU telecom rules increase legal/admin burden

Exposure to Intense Pricing Competition

OTE faces intense price competition in Greece, where the top three operators ran aggressive promotions in 2024–2025, driving mobile ARPU down ~6% YoY to about €9.5 in Q4 2024 for prepaid users according to Hellenic Telecommunications Organization data.

Pressure is strongest in mobile and prepaid segments, forcing OTE to invest in product differentiation, bundled services, and network upgrades to justify premium pricing and curb churn to lower-cost rivals.

Failure to innovate quickly could erode EBITDA margins (OTE Group reported 2024 EBITDA margin ~30%), so retention and value-added upsells are critical.

- Top-3 price wars cut mobile ARPU ~6% YoY

- Prepaid ARPU ~€9.5 (Q4 2024)

- OTE 2024 EBITDA margin ~30%

Heavy CAPEX, high Greek exposure & falling ARPU squeeze cash flow and M&A firepower

Heavy CAPEX (EUR 1.1bn in 2024; EUR 1.0–1.2bn p.a. planned) squeezes free cash flow and M&A room; net debt/EBITDA ~2.6x (FY2024). Revenue concentration: ~65% from Greece, high unemployment 12.4% (2024) and GDP volatility hurt ARPU and additions. Legacy copper raised maintenance ~€120–150m (2024) and migration costs €200–300/household. Regulatory costs €72m (2024); mobile ARPU fell ~6% YoY to €9.5 (Q4 2024).

| Metric | 2024 value |

|---|---|

| CAPEX | €1.1bn |

| Planned CAPEX (2025–26) | €1.0–1.2bn p.a. |

| Net debt/EBITDA | ~2.6x |

| Greece revenue share | ~65% |

| Unemployment (Greece) | 12.4% |

| Copper maintenance | €120–150m |

| Migration cost/household | €200–300 |

| Regulatory compliance | €72m |

| Prepaid ARPU (Q4) | €9.5 (-6% YoY) |

Full Version Awaits

OTE S.A. SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchase unlocks the entire in-depth version. You’re viewing a live preview of the actual SWOT analysis file, and the complete, editable document becomes available after checkout.