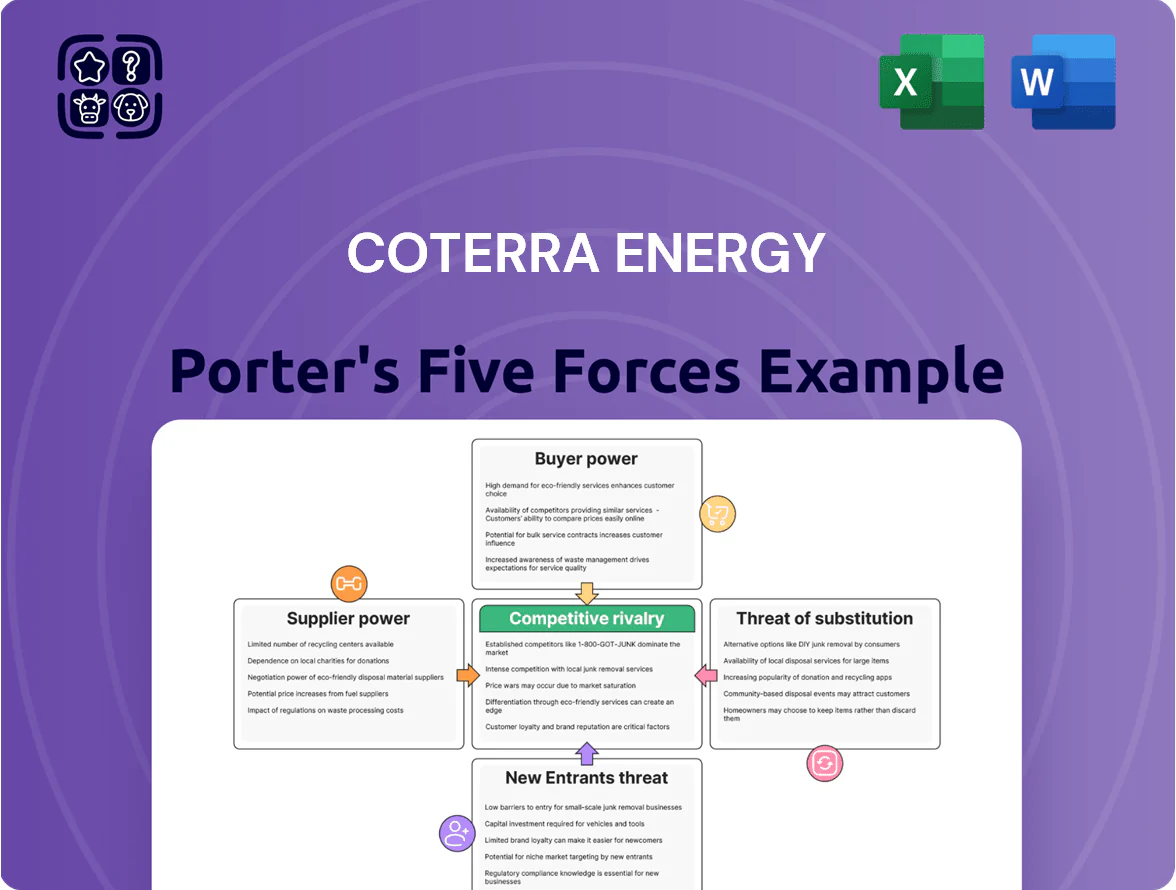

Coterra Energy Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Coterra Energy operates in a capital-intensive, commodity-driven sector where supplier bargaining, regulatory shifts, and volatile commodity prices shape margins; competitive rivalry is high among integrated E&P players while barriers to entry remain significant due to scale and capital needs. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Coterra Energy’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Specialized Oilfield Services

The market for high-spec drilling rigs and frack fleets is concentrated among a few firms (Schlumberger, Halliburton, Patterson-UTI), giving suppliers strong leverage over Coterra Energy in the Permian and Marcellus.

Coterra depends on these contractors for uptime and lateral lengths; in 2025 Coterra spent ~24% of capex on contract completion and service fees, heightening supplier influence.

Industry consolidation by late 2025 raised dayrates: average Permian frack dayrates rose ~18% YoY, letting suppliers hold prices even during oil/gas price swings.

Scarcity of Skilled Technical Labor

The oil and gas sector faces a persistent shortfall of experienced petroleum engineers, geologists, and field techs; US Bureau of Labor Statistics projected ~6% faster than average growth for petroleum engineers through 2024, keeping competition high. Skilled workers command leverage in wage talks—median petroleum engineer pay hit $154,840 in May 2024—so Coterra must offer market-leading pay, retention bonuses, and training to secure expertise for unconventional extraction.

Supply Chain Sensitivity for Tubular Goods and Proppant

Procurement of steel casing, piping and frac sand (proppant) faces global supply disruptions; 2024 US steel billet prices rose ~18% YoY and frac sand spot pricing jumped ~25% in H1 2024, increasing input cost volatility for Coterra Energy (NYSE: CTRA).

Suppliers can favor major integrated oil majors by volume, pressuring independents; Coterra mitigates via multi-year sourcing contracts covering ~60–70% of volumes but still faces spot-market exposure.

Long-term agreements reduce short-term shocks, yet persistent industrial inflation—PPI for mining and quarrying up ~12% in 2024—keeps margin risk elevated for Coterra.

Midstream Infrastructure and Pipeline Access

Third-party midstream providers control gathering, processing, and transport for Coterra, creating supplier leverage over tariff rates and contract terms.

In the Marcellus, takeaway constraints pushed basis differentials to as much as 2.50 USD/MMBtu in 2023–2024, raising Coterra’s midstream costs and routing risks.

Access to Gulf Coast and export markets often depends on firm pipeline capacity and PO/FT agreements with midstream partners, affecting realized prices and export volumes.

- Third-party control = pricing leverage

- Marcellus basis spikes ~2.50 USD/MMBtu (2023–24)

- Gulf Coast access tied to firm capacity, contracts

- Midstream outages can hit realized revenue

Technological Proprietary Software and Hardware

Modern shale ops use advanced seismic imaging, automated drilling software, and real-time analytics from tech vendors that hold proprietary IP, raising supplier bargaining power and switching costs for Coterra Energy.

In 2024, top providers drove 10–20% lift in well EUR (estimated ultimate recovery) and up to 15% lower drilling time, so Coterra must balance vendor lock risk against these productivity gains.

- Proprietary tech = high switching costs

- 2024: 10–20% EUR gains from vendors

- Up to 15% faster drill times

- Need vendor mix + in‑house analytics

Supplier squeeze lifts Coterra costs—rising dayrates, materials, labor; 60–70% contract cushion

Suppliers wield strong leverage over Coterra via concentrated rig/frack contractors (Schlumberger, Halliburton, Patterson‑UTI), rising dayrates (~+18% Permian YoY 2025), costly inputs (steel +18% 2024, frac sand +25% H1 2024), skilled labor scarcity (median petroleum engineer pay $154,840 May 2024), and midstream control (Marcellus basis spikes ~$2.50/MMBtu 2023–24), partially mitigated by 60–70% multi‑year contracts.

| Metric | Value |

|---|---|

| Permian frack dayrates change | +18% YoY (2025) |

| Capex on contractors | ~24% (2025) |

| Steel billet price change | +18% (2024) |

| Frac sand spot change | +25% H1 2024 |

| Petroleum engineer median pay | $154,840 (May 2024) |

| Marcellus basis spike | ~$2.50/MMBtu (2023–24) |

| Volumes on contracts | 60–70% multi‑year coverage |

What is included in the product

Tailored Porter's Five Forces analysis for Coterra Energy uncovering competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats to its market share and profitability.

Clear, one-sheet Porter's Five Forces for Coterra Energy—quickly gauge competitive threats and regulatory risk to inform M&A and capital allocation decisions.

Customers Bargaining Power

Commodity Market Price Taking

As an independent producer, Coterra Energy sells standardized crude oil and natural gas into global and regional commodity markets where prices are set by supply and demand, not individual deals; in 2024 U.S. benchmark WTI averaged about 80 USD/bbl and Henry Hub gas averaged ~3.50 USD/MMBtu, constraining Coterra’s pricing power.

Concentration of Utility and Industrial Buyers

A significant share of Coterra Energy’s gas goes to large electric utilities and industrial firms, and these buyers' scale lets them demand discounts or switch suppliers; in 2024 utilities accounted for roughly 30–40% of U.S. natural gas offtake by volume, giving them leverage. As of 2025, rising use of 5–15 year supply contracts for power plants locks in prices but preserves buyer bargaining power versus independent producers like Coterra.

Influence of LNG Export Terminals

The rapid rise in US LNG export capacity—reaching about 13.8 billion cubic feet per day (Bcf/d) of send-out capacity by end-2025—creates powerful buyers with strict volume and quality specs, raising customer bargaining power over upstream producers.

Terminals act as gatekeepers to 2025 international demand, enforcing tight delivery windows and penalties; this pressures Coterra Energy to meet schedules or lose cargo slots.

Coterra’s Marcellus and Permian output makes it a strategically important supplier, but it must competitively bid for limited export capacity and spot cargoes amid higher-priced international markets.

Switching Costs for Refineries

Refineries are often tuned to specific crude grades, so switching suppliers can require processing changes and raise costs, but in 2024 Permian light sweet crude accounted for about 5.5 million b/d of US production, giving refineries many alternatives beyond Coterra and reducing its leverage.

The broad Permian supply—dozens of producers and Coterra’s ~500,000 boe/d 2024 production—means comparable feedstock is widely available, so refineries retain strong bargaining power and can play suppliers off each other on price and delivery terms.

- 2024 Permian production ~5.5 million b/d

- Coterra production ~500,000 boe/d (2024)

- Many refineries configured for light sweet crude

- Switching costs exist but alternatives limit supplier leverage

Role of Financial Traders and Marketers

A portion of Coterra’s production is sold to marketing firms and financial intermediaries that aggregate supply for utilities, refiners, and traders; these counterparties accounted for roughly 20–30% of U.S. gas and NGL off-take in 2024, per industry trade reports.

These intermediaries have deep basin-level price intelligence and can shift volumes across Appalachia, Permian, and Haynesville based on marginal price spreads; in 2024 average monthly basis spreads exceeded $0.50/MMBtu between basins, enabling frequent arbitrage.

Their arbitrage power pressures Coterra to keep unit cash costs and downtime low—Coterra reported $1.30/BOE operating cash cost in 2024—so it stays the preferred supplier for high-volume traders.

- Counterparty concentration: ~20–30% of off-take

- Basis spread lever: >$0.50/MMBtu avg 2024

- Coterra 2024 cash op cost: $1.30/BOE

- Response: focus on efficiency, uptime, transport access

Buyers Hold the Leverage: Commodities Cap Prices as Alternatives Abound

Customers hold strong bargaining power: commodity pricing (WTI ~$80/bbl, Henry Hub ~$3.50/MMBtu in 2024) limits Coterra’s price control; large utilities, LNG buyers and intermediaries (20–30% off-take) can demand discounts or shift volumes; Permian supply (~5.5m b/d) and Coterra’s ~500,000 boe/d (2024) mean many alternatives.

| Metric | Value |

|---|---|

| Coterra prod (2024) | ~500,000 boe/d |

| Permian prod (2024) | ~5.5M b/d |

| Intermediary off-take (2024) | 20–30% |

| WTI (2024 avg) | ~$80/bbl |

Preview the Actual Deliverable

Coterra Energy Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Coterra Energy you'll receive immediately after purchase—no surprises, no placeholders. The document outlines competitive rivalry, supplier and buyer power, threat of new entrants, and substitute pressures with data-driven insights and sector context. It's fully formatted and ready to download the moment you buy. What you see here is precisely the deliverable you will get.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Coterra Energy operates in a capital-intensive, commodity-driven sector where supplier bargaining, regulatory shifts, and volatile commodity prices shape margins; competitive rivalry is high among integrated E&P players while barriers to entry remain significant due to scale and capital needs. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Coterra Energy’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentration of Specialized Oilfield Services

The market for high-spec drilling rigs and frack fleets is concentrated among a few firms (Schlumberger, Halliburton, Patterson-UTI), giving suppliers strong leverage over Coterra Energy in the Permian and Marcellus.

Coterra depends on these contractors for uptime and lateral lengths; in 2025 Coterra spent ~24% of capex on contract completion and service fees, heightening supplier influence.

Industry consolidation by late 2025 raised dayrates: average Permian frack dayrates rose ~18% YoY, letting suppliers hold prices even during oil/gas price swings.

Scarcity of Skilled Technical Labor

The oil and gas sector faces a persistent shortfall of experienced petroleum engineers, geologists, and field techs; US Bureau of Labor Statistics projected ~6% faster than average growth for petroleum engineers through 2024, keeping competition high. Skilled workers command leverage in wage talks—median petroleum engineer pay hit $154,840 in May 2024—so Coterra must offer market-leading pay, retention bonuses, and training to secure expertise for unconventional extraction.

Supply Chain Sensitivity for Tubular Goods and Proppant

Procurement of steel casing, piping and frac sand (proppant) faces global supply disruptions; 2024 US steel billet prices rose ~18% YoY and frac sand spot pricing jumped ~25% in H1 2024, increasing input cost volatility for Coterra Energy (NYSE: CTRA).

Suppliers can favor major integrated oil majors by volume, pressuring independents; Coterra mitigates via multi-year sourcing contracts covering ~60–70% of volumes but still faces spot-market exposure.

Long-term agreements reduce short-term shocks, yet persistent industrial inflation—PPI for mining and quarrying up ~12% in 2024—keeps margin risk elevated for Coterra.

Midstream Infrastructure and Pipeline Access

Third-party midstream providers control gathering, processing, and transport for Coterra, creating supplier leverage over tariff rates and contract terms.

In the Marcellus, takeaway constraints pushed basis differentials to as much as 2.50 USD/MMBtu in 2023–2024, raising Coterra’s midstream costs and routing risks.

Access to Gulf Coast and export markets often depends on firm pipeline capacity and PO/FT agreements with midstream partners, affecting realized prices and export volumes.

- Third-party control = pricing leverage

- Marcellus basis spikes ~2.50 USD/MMBtu (2023–24)

- Gulf Coast access tied to firm capacity, contracts

- Midstream outages can hit realized revenue

Technological Proprietary Software and Hardware

Modern shale ops use advanced seismic imaging, automated drilling software, and real-time analytics from tech vendors that hold proprietary IP, raising supplier bargaining power and switching costs for Coterra Energy.

In 2024, top providers drove 10–20% lift in well EUR (estimated ultimate recovery) and up to 15% lower drilling time, so Coterra must balance vendor lock risk against these productivity gains.

- Proprietary tech = high switching costs

- 2024: 10–20% EUR gains from vendors

- Up to 15% faster drill times

- Need vendor mix + in‑house analytics

Supplier squeeze lifts Coterra costs—rising dayrates, materials, labor; 60–70% contract cushion

Suppliers wield strong leverage over Coterra via concentrated rig/frack contractors (Schlumberger, Halliburton, Patterson‑UTI), rising dayrates (~+18% Permian YoY 2025), costly inputs (steel +18% 2024, frac sand +25% H1 2024), skilled labor scarcity (median petroleum engineer pay $154,840 May 2024), and midstream control (Marcellus basis spikes ~$2.50/MMBtu 2023–24), partially mitigated by 60–70% multi‑year contracts.

| Metric | Value |

|---|---|

| Permian frack dayrates change | +18% YoY (2025) |

| Capex on contractors | ~24% (2025) |

| Steel billet price change | +18% (2024) |

| Frac sand spot change | +25% H1 2024 |

| Petroleum engineer median pay | $154,840 (May 2024) |

| Marcellus basis spike | ~$2.50/MMBtu (2023–24) |

| Volumes on contracts | 60–70% multi‑year coverage |

What is included in the product

Tailored Porter's Five Forces analysis for Coterra Energy uncovering competitive drivers, supplier and buyer power, entry barriers, substitutes, and disruptive threats to its market share and profitability.

Clear, one-sheet Porter's Five Forces for Coterra Energy—quickly gauge competitive threats and regulatory risk to inform M&A and capital allocation decisions.

Customers Bargaining Power

Commodity Market Price Taking

As an independent producer, Coterra Energy sells standardized crude oil and natural gas into global and regional commodity markets where prices are set by supply and demand, not individual deals; in 2024 U.S. benchmark WTI averaged about 80 USD/bbl and Henry Hub gas averaged ~3.50 USD/MMBtu, constraining Coterra’s pricing power.

Concentration of Utility and Industrial Buyers

A significant share of Coterra Energy’s gas goes to large electric utilities and industrial firms, and these buyers' scale lets them demand discounts or switch suppliers; in 2024 utilities accounted for roughly 30–40% of U.S. natural gas offtake by volume, giving them leverage. As of 2025, rising use of 5–15 year supply contracts for power plants locks in prices but preserves buyer bargaining power versus independent producers like Coterra.

Influence of LNG Export Terminals

The rapid rise in US LNG export capacity—reaching about 13.8 billion cubic feet per day (Bcf/d) of send-out capacity by end-2025—creates powerful buyers with strict volume and quality specs, raising customer bargaining power over upstream producers.

Terminals act as gatekeepers to 2025 international demand, enforcing tight delivery windows and penalties; this pressures Coterra Energy to meet schedules or lose cargo slots.

Coterra’s Marcellus and Permian output makes it a strategically important supplier, but it must competitively bid for limited export capacity and spot cargoes amid higher-priced international markets.

Switching Costs for Refineries

Refineries are often tuned to specific crude grades, so switching suppliers can require processing changes and raise costs, but in 2024 Permian light sweet crude accounted for about 5.5 million b/d of US production, giving refineries many alternatives beyond Coterra and reducing its leverage.

The broad Permian supply—dozens of producers and Coterra’s ~500,000 boe/d 2024 production—means comparable feedstock is widely available, so refineries retain strong bargaining power and can play suppliers off each other on price and delivery terms.

- 2024 Permian production ~5.5 million b/d

- Coterra production ~500,000 boe/d (2024)

- Many refineries configured for light sweet crude

- Switching costs exist but alternatives limit supplier leverage

Role of Financial Traders and Marketers

A portion of Coterra’s production is sold to marketing firms and financial intermediaries that aggregate supply for utilities, refiners, and traders; these counterparties accounted for roughly 20–30% of U.S. gas and NGL off-take in 2024, per industry trade reports.

These intermediaries have deep basin-level price intelligence and can shift volumes across Appalachia, Permian, and Haynesville based on marginal price spreads; in 2024 average monthly basis spreads exceeded $0.50/MMBtu between basins, enabling frequent arbitrage.

Their arbitrage power pressures Coterra to keep unit cash costs and downtime low—Coterra reported $1.30/BOE operating cash cost in 2024—so it stays the preferred supplier for high-volume traders.

- Counterparty concentration: ~20–30% of off-take

- Basis spread lever: >$0.50/MMBtu avg 2024

- Coterra 2024 cash op cost: $1.30/BOE

- Response: focus on efficiency, uptime, transport access

Buyers Hold the Leverage: Commodities Cap Prices as Alternatives Abound

Customers hold strong bargaining power: commodity pricing (WTI ~$80/bbl, Henry Hub ~$3.50/MMBtu in 2024) limits Coterra’s price control; large utilities, LNG buyers and intermediaries (20–30% off-take) can demand discounts or shift volumes; Permian supply (~5.5m b/d) and Coterra’s ~500,000 boe/d (2024) mean many alternatives.

| Metric | Value |

|---|---|

| Coterra prod (2024) | ~500,000 boe/d |

| Permian prod (2024) | ~5.5M b/d |

| Intermediary off-take (2024) | 20–30% |

| WTI (2024 avg) | ~$80/bbl |

Preview the Actual Deliverable

Coterra Energy Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Coterra Energy you'll receive immediately after purchase—no surprises, no placeholders. The document outlines competitive rivalry, supplier and buyer power, threat of new entrants, and substitute pressures with data-driven insights and sector context. It's fully formatted and ready to download the moment you buy. What you see here is precisely the deliverable you will get.