Coterra Energy Marketing Mix

Built for Strategy. Ready in Minutes.

Coterra Energy’s marketing mix aligns product offerings, competitive pricing, efficient distribution, and targeted promotions to strengthen its upstream energy position; our preview highlights key moves but only scratches the surface.

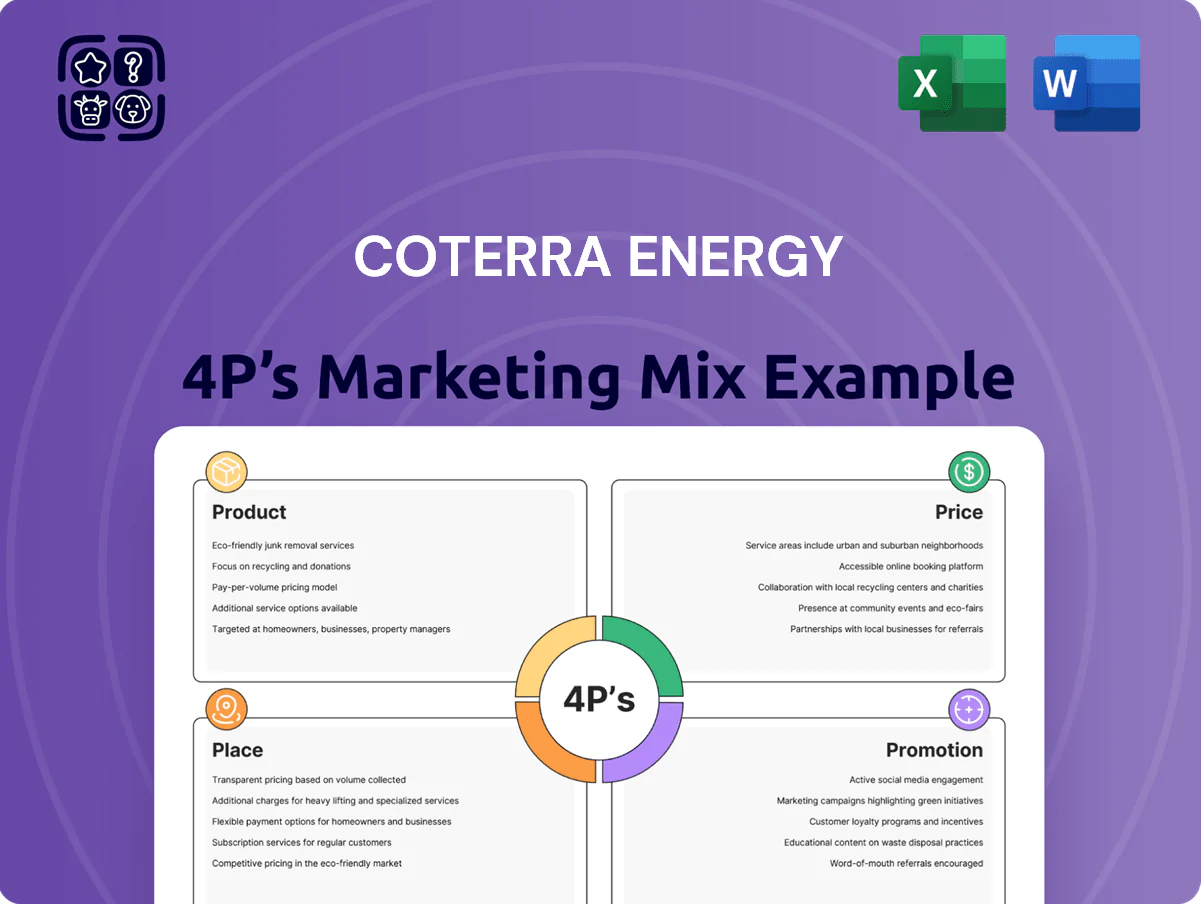

Product

Natural Gas Production

Coterra Energy produces premium natural gas from Marcellus Shale and Permian Basin acreage, delivering 6.2 billion cubic feet per day (bcfd) in 2024 and targeting 6.5 bcfd by late 2025.

The gas fuels US power generation and industrial users and reaches global markets via LNG exports, contributing to $5.1 billion of 2024 revenue from natural gas sales.

By late 2025 Coterra has cut methane intensity to 0.08% and reduced combustion CO2-equivalent per MMBtu by 12% through optimized drilling and emissions controls, supporting low-emission delivery.

Crude Oil Extraction

Coterra Energy produces high-grade crude oil mainly from the Permian and Anadarko Basins, averaging about 280 MBbls/d oil-equivalent in 2025, with oil representing roughly 45% of total production.

This crude feeds global energy markets and petrochemical supply chains, with Coterra selling into midstream and refinery contracts that value its consistent API and low-sulfur specs.

The firm manages a balanced production profile, shifting gas/oil mix and hedging to capture oil price swings—realized oil price was $72.40/Bbl in 2025 YTD.

Quality and steady volumes make Coterra a preferred supplier, supporting stable offtake terms and lower transport basis differentials versus peers.

Natural Gas Liquids

Coterra Energy also produces sizable volumes of natural gas liquids (ethane, propane, butane), which feed plastics and heating markets and add revenue beyond dry gas and oil.

By year-end 2025 Coterra boosted processing capacity—raising NGL capture rates to about 18–22% of gas production and adding roughly $200–350 million of annualized EBITDA potential.

This NGL mix diversifies cash flow and reduces exposure to single-commodity swings; when gas prices fell 2022–24, NGL sales softened the impact on total revenue.

Midstream Infrastructure Services

Coterra Energy operates and invests in midstream assets—gathering systems and processing facilities—that move gas and NGLs from wellhead to major pipelines, supporting ~1.9 Bcfe/d total production (2025 guidance).

Controlling parts of the midstream chain cuts third-party fees, raised uptime, and lowers per-unit transport cost; shared infrastructure reduced gather/processing expense by an estimated 8–12% vs full third-party reliance in 2024.

This integration strengthens reliability and pricing leverage for buyers, improving realized prices and preserving margin across commodity cycles.

- Assets: gathering + processing

- Supports ~1.9 Bcfe/d (2025)

- Reduces fees ~8–12% (2024 est)

- Improves uptime, margins, buyer pricing

Sustainable Energy Initiatives

As of late 2025, Coterra Energy offers responsibly sourced gas certifications and tracks methane intensity, meeting utility and industrial demand for lower-emission fuels; the company reported a 22% reduction in methane intensity from 2022 levels and 2025 Scope 1+2+3 reporting to investors.

Investments in continuous emissions monitoring and leak detection technology reduce operational emissions and differentiate Coterra’s physical product in a crowded market, helping secure offtake deals with ESG-focused buyers.

This sustainability focus adds investor appeal—ESG-aligned funds owned roughly 12% of Coterra by Q4 2025—and supports premium pricing for certified low-methane gas.

- 22% methane intensity cut since 2022

- 2025 Scope 1+2+3 disclosures published

- ~12% ownership by ESG funds (Q4 2025)

- Continuous emissions monitoring investments

Coterra: Scaling to 6.5 bcfd with $5.1B gas revenue, strong oil mix & low methane (0.08%)

Coterra supplies 6.2 bcfd (2024), targeting 6.5 bcfd by late 2025, plus ~280 MBbls/d oil-equivalent (2025 YTD), with oil ~45% of mix and NGLs ~18–22% of gas output.

2024 gas revenue $5.1B; realized oil price $72.40/Bbl (2025 YTD); NGLs add $200–350M EBITDA potential (annualized).

Methane intensity cut 22% since 2022 to 0.08% (late 2025); Scope 1–3 reporting and low-methane certification support premium offtake.

| Metric | Value |

|---|---|

| Gas prod (2024) | 6.2 bcfd |

| Target (late 2025) | 6.5 bcfd |

| Oil (2025 YTD) | 280 MBbls/d |

| Realized oil price | $72.40/Bbl |

| Gas revenue (2024) | $5.1B |

| NGL capture | 18–22% |

| NGL EBITDA upside | $200–350M |

| Methane intensity | 0.08% (–22% vs 2022) |

What is included in the product

Delivers a concise, company-specific deep dive into Coterra Energy’s Product, Price, Place, and Promotion strategies, grounded in real operations and competitive context.

Condenses Coterra Energy’s 4P marketing insights into a concise, leadership-ready snapshot that eases strategic decision-making and cross-functional alignment.

Place

Permian Basin Strategic Hub

The Permian Basin, spanning West Texas and Southeast New Mexico, is Coterra Energy’s primary geographic pillar, supplying roughly 40% of the company’s 2025 production after consolidation of assets to 600+ operated wells.

This region offers access to some of North America’s lowest full-cycle costs—around $15–20/boe for Coterra in 2025—boosting margins and cash flow.

By 2025 Coterra has consolidated its footprint to maximize operational efficiency and logistics, cutting unit opex by ~12% versus 2022.

Close proximity to Gulf Coast refineries and export terminals enables quick access to high-value markets, keeping takeaway bottlenecks under 5% of capacity in 2025.

Marcellus Shale Dominance

Coterra Energy holds a leading position in the Marcellus Shale in Northeast Pennsylvania, part of one of the world’s largest gas basins with ~141 Tcf estimated recoverable gas (2024 US EIA); the area feeds high-demand Northeastern US and Eastern Canada markets, supporting stronger regional prices (Henry Hub basis to TET-NY spreads). Coterra moves production via extensive gathering networks into major interstate pipelines, leveraging low transport costs and existing infrastructure to protect margins and realized gas prices.

Anadarko Basin Operations

The Anadarko Basin in Oklahoma gives Coterra Energy a diversified geographic base alongside its Permian and Marcellus assets, contributing roughly 12% of company production in 2025 (about 85 mboe/d). The basin’s mixed oil and gas profile lets Coterra shift capital — CAPEX allocated here fell to $180M in 2025 as focus moved to higher-return zones. By late 2025 Coterra refined its drilling inventory to ~1,100 high‑graded locations targeting top-tier economics. Strong pipeline connectivity in Oklahoma supports efficient flows to Mid‑Continent and Gulf Coast hubs, lowering takeaway costs by an estimated $0.50–$1.00/boe.

Interstate Pipeline Connectivity

Coterra relies on a complex interstate pipeline network to move gas from wellhead to market, backed by firm transport contracts that guarantee capacity during peak demand and reduce price risk.

Long-term agreements secured by 2025 link production to liquid hubs such as Henry Hub and Permian-Texas hubs, helping avoid regional bottlenecks that can cut local prices by up to 10% in stress periods.

Here’s the quick math: firm capacity covers a majority of volumes—roughly 60–75% of pipelineable output—lowering basis exposure and supporting stable netbacks.

- Firm transport ensures delivery in peak demand

- Long-term contracts through 2025 to major hubs

- Reduces regional price weakness (est. up to 10%)

- Firm capacity ~60–75% of pipelineable volumes

Global Export Market Access

Through Gulf Coast pipeline and port links, Coterra Energy (Coterra Energy Inc., NYSE: CTRA) ships LNG and crude to international buyers, tapping higher global price points when U.S. supply is heavy.

By end-2025 Coterra shifted ~18% of production cycles to match global demand peaks, improving realized prices and cutting domestic price exposure.

This export focus lowers geographic risk and speeds inventory clearance for large volumes during seasonal surpluses.

- Gulf Coast terminal access: LNG and crude exports

- End-2025: ~18% production re-timing to global cycles

- Captures international price premiums vs domestic

- Reduces geographic concentration; clears large volumes

Coterra 2025: Permian 40% & low $15–20/boe costs, Marcellus gas leader, Anadarko 12%

Coterra’s Place: 2025 core footprint—Permian ~40% production (600+ wells), Marcellus leading gas position, Anadarko ~12% (~85 mboe/d); low full-cycle costs $15–20/boe; firm pipeline capacity 60–75% of volumes; Gulf Coast export links shift ~18% of flows to global markets, cutting regional price risk up to 10% and lowering unit opex ~12% vs 2022.

| Region | 2025 % Prod | Key stats |

|---|---|---|

| Permian | ~40% | 600+ wells; $15–20/boe |

| Marcellus | — | feeds NE/Canada; 141 Tcf basin |

| Anadarko | ~12% | ~85 mboe/d; 1,100 locations |

Same Document Delivered

Coterra Energy 4P's Marketing Mix Analysis

The preview shown here is the actual Coterra Energy 4P's Marketing Mix analysis you’ll receive instantly after purchase—fully complete, editable, and ready to use with no surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Built for Strategy. Ready in Minutes.

Coterra Energy’s marketing mix aligns product offerings, competitive pricing, efficient distribution, and targeted promotions to strengthen its upstream energy position; our preview highlights key moves but only scratches the surface.

Product

Natural Gas Production

Coterra Energy produces premium natural gas from Marcellus Shale and Permian Basin acreage, delivering 6.2 billion cubic feet per day (bcfd) in 2024 and targeting 6.5 bcfd by late 2025.

The gas fuels US power generation and industrial users and reaches global markets via LNG exports, contributing to $5.1 billion of 2024 revenue from natural gas sales.

By late 2025 Coterra has cut methane intensity to 0.08% and reduced combustion CO2-equivalent per MMBtu by 12% through optimized drilling and emissions controls, supporting low-emission delivery.

Crude Oil Extraction

Coterra Energy produces high-grade crude oil mainly from the Permian and Anadarko Basins, averaging about 280 MBbls/d oil-equivalent in 2025, with oil representing roughly 45% of total production.

This crude feeds global energy markets and petrochemical supply chains, with Coterra selling into midstream and refinery contracts that value its consistent API and low-sulfur specs.

The firm manages a balanced production profile, shifting gas/oil mix and hedging to capture oil price swings—realized oil price was $72.40/Bbl in 2025 YTD.

Quality and steady volumes make Coterra a preferred supplier, supporting stable offtake terms and lower transport basis differentials versus peers.

Natural Gas Liquids

Coterra Energy also produces sizable volumes of natural gas liquids (ethane, propane, butane), which feed plastics and heating markets and add revenue beyond dry gas and oil.

By year-end 2025 Coterra boosted processing capacity—raising NGL capture rates to about 18–22% of gas production and adding roughly $200–350 million of annualized EBITDA potential.

This NGL mix diversifies cash flow and reduces exposure to single-commodity swings; when gas prices fell 2022–24, NGL sales softened the impact on total revenue.

Midstream Infrastructure Services

Coterra Energy operates and invests in midstream assets—gathering systems and processing facilities—that move gas and NGLs from wellhead to major pipelines, supporting ~1.9 Bcfe/d total production (2025 guidance).

Controlling parts of the midstream chain cuts third-party fees, raised uptime, and lowers per-unit transport cost; shared infrastructure reduced gather/processing expense by an estimated 8–12% vs full third-party reliance in 2024.

This integration strengthens reliability and pricing leverage for buyers, improving realized prices and preserving margin across commodity cycles.

- Assets: gathering + processing

- Supports ~1.9 Bcfe/d (2025)

- Reduces fees ~8–12% (2024 est)

- Improves uptime, margins, buyer pricing

Sustainable Energy Initiatives

As of late 2025, Coterra Energy offers responsibly sourced gas certifications and tracks methane intensity, meeting utility and industrial demand for lower-emission fuels; the company reported a 22% reduction in methane intensity from 2022 levels and 2025 Scope 1+2+3 reporting to investors.

Investments in continuous emissions monitoring and leak detection technology reduce operational emissions and differentiate Coterra’s physical product in a crowded market, helping secure offtake deals with ESG-focused buyers.

This sustainability focus adds investor appeal—ESG-aligned funds owned roughly 12% of Coterra by Q4 2025—and supports premium pricing for certified low-methane gas.

- 22% methane intensity cut since 2022

- 2025 Scope 1+2+3 disclosures published

- ~12% ownership by ESG funds (Q4 2025)

- Continuous emissions monitoring investments

Coterra: Scaling to 6.5 bcfd with $5.1B gas revenue, strong oil mix & low methane (0.08%)

Coterra supplies 6.2 bcfd (2024), targeting 6.5 bcfd by late 2025, plus ~280 MBbls/d oil-equivalent (2025 YTD), with oil ~45% of mix and NGLs ~18–22% of gas output.

2024 gas revenue $5.1B; realized oil price $72.40/Bbl (2025 YTD); NGLs add $200–350M EBITDA potential (annualized).

Methane intensity cut 22% since 2022 to 0.08% (late 2025); Scope 1–3 reporting and low-methane certification support premium offtake.

| Metric | Value |

|---|---|

| Gas prod (2024) | 6.2 bcfd |

| Target (late 2025) | 6.5 bcfd |

| Oil (2025 YTD) | 280 MBbls/d |

| Realized oil price | $72.40/Bbl |

| Gas revenue (2024) | $5.1B |

| NGL capture | 18–22% |

| NGL EBITDA upside | $200–350M |

| Methane intensity | 0.08% (–22% vs 2022) |

What is included in the product

Delivers a concise, company-specific deep dive into Coterra Energy’s Product, Price, Place, and Promotion strategies, grounded in real operations and competitive context.

Condenses Coterra Energy’s 4P marketing insights into a concise, leadership-ready snapshot that eases strategic decision-making and cross-functional alignment.

Place

Permian Basin Strategic Hub

The Permian Basin, spanning West Texas and Southeast New Mexico, is Coterra Energy’s primary geographic pillar, supplying roughly 40% of the company’s 2025 production after consolidation of assets to 600+ operated wells.

This region offers access to some of North America’s lowest full-cycle costs—around $15–20/boe for Coterra in 2025—boosting margins and cash flow.

By 2025 Coterra has consolidated its footprint to maximize operational efficiency and logistics, cutting unit opex by ~12% versus 2022.

Close proximity to Gulf Coast refineries and export terminals enables quick access to high-value markets, keeping takeaway bottlenecks under 5% of capacity in 2025.

Marcellus Shale Dominance

Coterra Energy holds a leading position in the Marcellus Shale in Northeast Pennsylvania, part of one of the world’s largest gas basins with ~141 Tcf estimated recoverable gas (2024 US EIA); the area feeds high-demand Northeastern US and Eastern Canada markets, supporting stronger regional prices (Henry Hub basis to TET-NY spreads). Coterra moves production via extensive gathering networks into major interstate pipelines, leveraging low transport costs and existing infrastructure to protect margins and realized gas prices.

Anadarko Basin Operations

The Anadarko Basin in Oklahoma gives Coterra Energy a diversified geographic base alongside its Permian and Marcellus assets, contributing roughly 12% of company production in 2025 (about 85 mboe/d). The basin’s mixed oil and gas profile lets Coterra shift capital — CAPEX allocated here fell to $180M in 2025 as focus moved to higher-return zones. By late 2025 Coterra refined its drilling inventory to ~1,100 high‑graded locations targeting top-tier economics. Strong pipeline connectivity in Oklahoma supports efficient flows to Mid‑Continent and Gulf Coast hubs, lowering takeaway costs by an estimated $0.50–$1.00/boe.

Interstate Pipeline Connectivity

Coterra relies on a complex interstate pipeline network to move gas from wellhead to market, backed by firm transport contracts that guarantee capacity during peak demand and reduce price risk.

Long-term agreements secured by 2025 link production to liquid hubs such as Henry Hub and Permian-Texas hubs, helping avoid regional bottlenecks that can cut local prices by up to 10% in stress periods.

Here’s the quick math: firm capacity covers a majority of volumes—roughly 60–75% of pipelineable output—lowering basis exposure and supporting stable netbacks.

- Firm transport ensures delivery in peak demand

- Long-term contracts through 2025 to major hubs

- Reduces regional price weakness (est. up to 10%)

- Firm capacity ~60–75% of pipelineable volumes

Global Export Market Access

Through Gulf Coast pipeline and port links, Coterra Energy (Coterra Energy Inc., NYSE: CTRA) ships LNG and crude to international buyers, tapping higher global price points when U.S. supply is heavy.

By end-2025 Coterra shifted ~18% of production cycles to match global demand peaks, improving realized prices and cutting domestic price exposure.

This export focus lowers geographic risk and speeds inventory clearance for large volumes during seasonal surpluses.

- Gulf Coast terminal access: LNG and crude exports

- End-2025: ~18% production re-timing to global cycles

- Captures international price premiums vs domestic

- Reduces geographic concentration; clears large volumes

Coterra 2025: Permian 40% & low $15–20/boe costs, Marcellus gas leader, Anadarko 12%

Coterra’s Place: 2025 core footprint—Permian ~40% production (600+ wells), Marcellus leading gas position, Anadarko ~12% (~85 mboe/d); low full-cycle costs $15–20/boe; firm pipeline capacity 60–75% of volumes; Gulf Coast export links shift ~18% of flows to global markets, cutting regional price risk up to 10% and lowering unit opex ~12% vs 2022.

| Region | 2025 % Prod | Key stats |

|---|---|---|

| Permian | ~40% | 600+ wells; $15–20/boe |

| Marcellus | — | feeds NE/Canada; 141 Tcf basin |

| Anadarko | ~12% | ~85 mboe/d; 1,100 locations |

Same Document Delivered

Coterra Energy 4P's Marketing Mix Analysis

The preview shown here is the actual Coterra Energy 4P's Marketing Mix analysis you’ll receive instantly after purchase—fully complete, editable, and ready to use with no surprises.