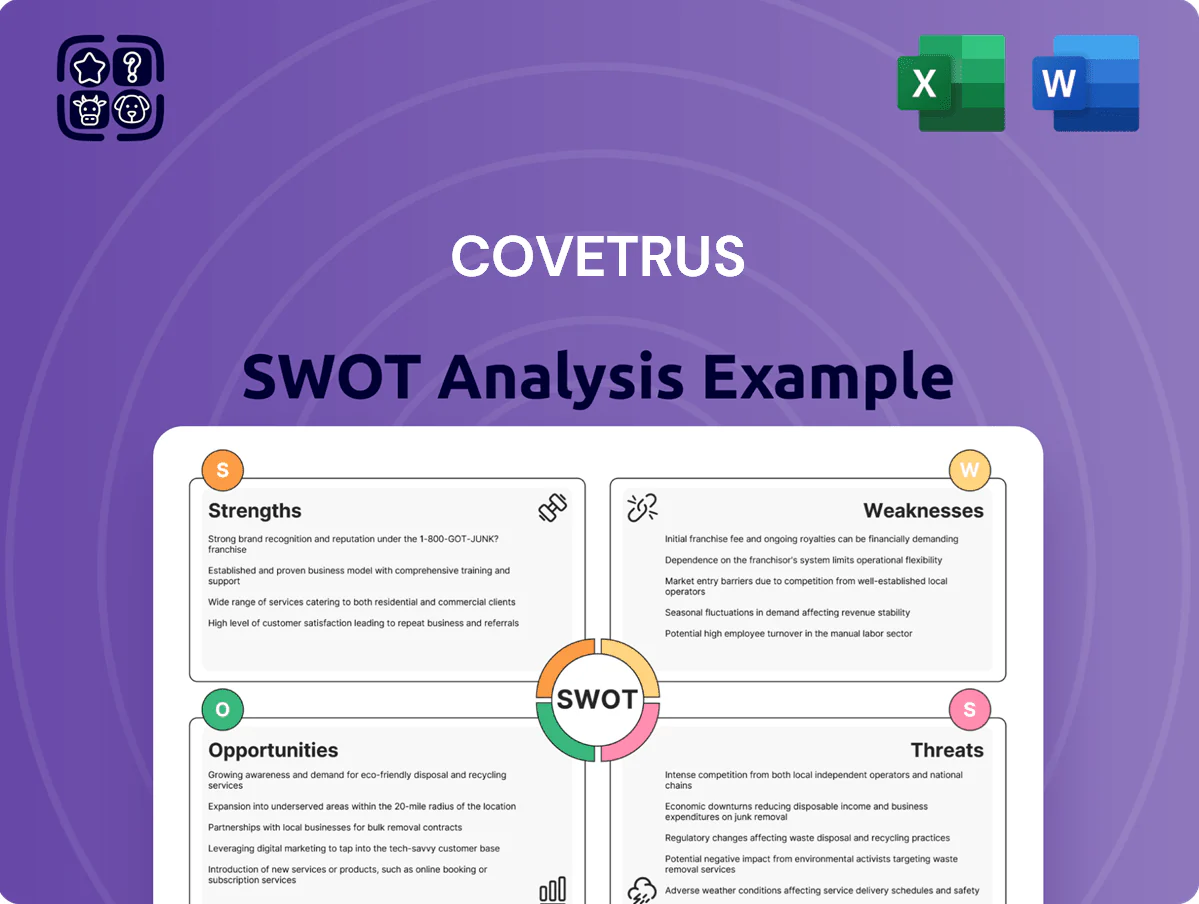

Covetrus SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Covetrus combines a strong recurring-revenue model and integrated supply-chain capabilities with growing digital tools for veterinary practices, but it faces margin pressure, competition, and regulatory risks that could affect scalability.

Strengths

Integrated Veterinary Ecosystem

Covetrus offers an end-to-end veterinary platform combining practice management software, supply chain distribution, and prescription fulfillment, enabling clinics to run clinical, inventory, and billing workflows with one vendor.

This vertical integration raised recurring revenue: in 2024 Covetrus reported $1.7B in product and services revenue, which tightens clinic dependence and raises switching costs through synced records and automated reorders.

Market-Leading Software Suite

Covetrus holds a dominant position via Pulse and eVetPractice, two cloud-based practice management systems used by over 15,000 clinics worldwide as of Q4 2025, handling clinical records, billing, inventory, and scheduling.

These platforms drive recurring SaaS revenue—about $420 million in 2024 services revenue—and anchor digital transformation for independent and corporate groups, reducing admin time by ~30% per clinic in vendor studies.

Robust Distribution Network

Covetrus runs a global logistics network serving 100+ countries and over 150,000 veterinary customers, enabling on-time delivery of pharmaceuticals and clinical supplies; this scale supported $3.2B revenue in 2024 and boosts negotiating leverage with manufacturers for better purchase terms.

The company manages cold-chain logistics and regulatory complexity across markets, reducing spoilage and compliance fines—Covetrus reported a 98% on-time fill rate in 2024—creating a barrier versus smaller regional distributors.

Data-Driven Prescription Management

Covetrus’s data-driven prescription management lets clinics recapture revenue via home delivery; in 2024 the pharmacy segment grew revenue ~12%, showing demand for remote fulfillment.

Using analytics to track compliance and automate refills, Covetrus reports improved adherence and fewer missed doses, boosting patient outcomes and lowering follow-up visits.

This proactive pharmacy model increases clinic prescription revenue and recurring margin, supporting practice cash flow and profitability.

- Home delivery drives ~12% pharmacy revenue growth (2024)

- Automated refills raise adherence and cut missed-dose visits

- Improves clinic recurring revenue and cash flow

Strategic Private Equity Backing

Strategic private equity backing from Clayton, Dubilier & Rice and TPG Capital gives Covetrus deep capital and operational expertise, enabling multi-year tech investments and bold M&A without public-market quarterly pressure.

The partners’ financial flexibility funded Covetrus’s 2024 acquisition spree and supports digital initiatives and global expansion; combined PE dry powder exceeded $150 billion in 2024, easing large-scale financing.

- Long-term capital for tech and M&A

- No quarterly public reporting pressure

- Supports large digital projects and global growth

- Backed by PE firms with >$150B dry powder (2024)

Covetrus: $3.2B vet platform—15k+ clinics, 150k customers, recurring SaaS & 98% fill rate

Covetrus’s integrated vet platform (Pulse, eVetPractice) drives recurring SaaS + services: $1.7B product/services and $420M services in 2024, >15,000 clinics (Q4 2025), 150,000 customers across 100+ countries, $3.2B total revenue (2024), 98% on-time fill rate, pharmacy +12% growth (2024); PE backing (CD&R, TPG) with >$150B dry powder enables M&A and tech investment.

| Metric | Value |

|---|---|

| 2024 revenue (total) | $3.2B |

| Product & services (2024) | $1.7B |

| Services/SaaS (2024) | $420M |

| Clinics (Q4 2025) | >15,000 |

| Customers / Countries | 150,000 / 100+ |

| On-time fill rate (2024) | 98% |

| Pharmacy growth (2024) | +12% |

| PE dry powder (2024) | >$150B |

What is included in the product

Delivers a strategic overview of Covetrus’s internal strengths and weaknesses and the external opportunities and threats shaping its competitive position in the animal-health and veterinary supply market.

Delivers a concise Covetrus SWOT matrix for rapid strategic alignment across veterinary channels, easing stakeholder briefings and decision-making.

Weaknesses

Substantial Debt Obligations

Following its 2022 take‑private, Covetrus carries roughly $1.8 billion of long‑term debt on the balance sheet; servicing costs rose as U.S. benchmark rates climbed, pushing interest expense above $160 million in FY2024. Higher rates through 2024–2025 have squeezed free cash flow, likely constraining R and D and product investment. This leverage raises bankruptcy and liquidity risk in a downturn and reduces flexibility versus lower‑debt peers.

Legacy System Integration Hurdles

Covetrus was formed by the 2022 merger of Henry Schein Animal Health and Vets First Choice, leaving a tangle of legacy IT stacks; as of Q4 2024 IT consolidation lagged, with management reporting a 15–20% CRM integration gap across markets.

Partial harmonization improved order routing and inventory accuracy, cutting fulfillment errors by 9% in 2024, but full platform sync across 25+ countries remains incomplete.

Inconsistent UX on older modules correlated with a 4% net revenue retention drag in 2024 and higher churn among small clinics, per company disclosures.

Low-Margin Distribution Dependence

A large share of Covetrus revenue—about 60% in FY2024 revenue of $3.6B—comes from third‑party product distribution, which yields materially lower gross margins (~18%) versus its SaaS/technology segment (~65%). This high-volume, low-margin mix makes earnings sensitive to fuel and logistics swings: U.S. diesel rose ~25% year‑over‑year in 2022–23, squeezing distribution margins. Moving mix to higher‑margin SaaS is gradual and needs continual product innovation and sales ramp time.

High Operational Complexity

Managing Covetrus’s global supply chain plus a software development arm creates organizational friction; in 2024 Covetrus reported $3.1B revenue split across distribution and tech services, forcing trade-offs in capital and talent.

The dual business model needs distinct expertise, causing misaligned priorities between logistics and product teams and slowing product-to-market timing in a fast-growing pet health market (global pet care market ~$325B in 2024).

Geographic Concentration in North America

- ~78% revenue from North America (2024)

- International revenue CAGR ~3% (2021–2024)

- Higher sensitivity to US regulation and macro shocks

- Slower-than-expected Asian/Latin American expansion

High Debt, Fragile Growth: 78% NA Revenue, Heavy Distribution, Margin & IT Strain

High leverage: $1.8B long‑term debt; interest expense >$160M FY2024, pressuring FCF. Legacy IT fragmentation: 15–20% CRM integration gap; 4% NRR drag in 2024. Revenue mix weak: 60% low‑margin distribution (≈18% gross); SaaS ~65% gross. Geographic concentration: ~78% revenue North America; intl CAGR ~3% (2021–2024).

| Metric | 2024 |

|---|---|

| Long‑term debt | $1.8B |

| Interest expense | $160M+ |

| Revenue | $3.6B |

| Distribution share | 60% |

| NA revenue share | 78% |

Preview the Actual Deliverable

Covetrus SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

This is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Dive Deeper Into the Company’s Strategic Blueprint

Covetrus combines a strong recurring-revenue model and integrated supply-chain capabilities with growing digital tools for veterinary practices, but it faces margin pressure, competition, and regulatory risks that could affect scalability.

Strengths

Integrated Veterinary Ecosystem

Covetrus offers an end-to-end veterinary platform combining practice management software, supply chain distribution, and prescription fulfillment, enabling clinics to run clinical, inventory, and billing workflows with one vendor.

This vertical integration raised recurring revenue: in 2024 Covetrus reported $1.7B in product and services revenue, which tightens clinic dependence and raises switching costs through synced records and automated reorders.

Market-Leading Software Suite

Covetrus holds a dominant position via Pulse and eVetPractice, two cloud-based practice management systems used by over 15,000 clinics worldwide as of Q4 2025, handling clinical records, billing, inventory, and scheduling.

These platforms drive recurring SaaS revenue—about $420 million in 2024 services revenue—and anchor digital transformation for independent and corporate groups, reducing admin time by ~30% per clinic in vendor studies.

Robust Distribution Network

Covetrus runs a global logistics network serving 100+ countries and over 150,000 veterinary customers, enabling on-time delivery of pharmaceuticals and clinical supplies; this scale supported $3.2B revenue in 2024 and boosts negotiating leverage with manufacturers for better purchase terms.

The company manages cold-chain logistics and regulatory complexity across markets, reducing spoilage and compliance fines—Covetrus reported a 98% on-time fill rate in 2024—creating a barrier versus smaller regional distributors.

Data-Driven Prescription Management

Covetrus’s data-driven prescription management lets clinics recapture revenue via home delivery; in 2024 the pharmacy segment grew revenue ~12%, showing demand for remote fulfillment.

Using analytics to track compliance and automate refills, Covetrus reports improved adherence and fewer missed doses, boosting patient outcomes and lowering follow-up visits.

This proactive pharmacy model increases clinic prescription revenue and recurring margin, supporting practice cash flow and profitability.

- Home delivery drives ~12% pharmacy revenue growth (2024)

- Automated refills raise adherence and cut missed-dose visits

- Improves clinic recurring revenue and cash flow

Strategic Private Equity Backing

Strategic private equity backing from Clayton, Dubilier & Rice and TPG Capital gives Covetrus deep capital and operational expertise, enabling multi-year tech investments and bold M&A without public-market quarterly pressure.

The partners’ financial flexibility funded Covetrus’s 2024 acquisition spree and supports digital initiatives and global expansion; combined PE dry powder exceeded $150 billion in 2024, easing large-scale financing.

- Long-term capital for tech and M&A

- No quarterly public reporting pressure

- Supports large digital projects and global growth

- Backed by PE firms with >$150B dry powder (2024)

Covetrus: $3.2B vet platform—15k+ clinics, 150k customers, recurring SaaS & 98% fill rate

Covetrus’s integrated vet platform (Pulse, eVetPractice) drives recurring SaaS + services: $1.7B product/services and $420M services in 2024, >15,000 clinics (Q4 2025), 150,000 customers across 100+ countries, $3.2B total revenue (2024), 98% on-time fill rate, pharmacy +12% growth (2024); PE backing (CD&R, TPG) with >$150B dry powder enables M&A and tech investment.

| Metric | Value |

|---|---|

| 2024 revenue (total) | $3.2B |

| Product & services (2024) | $1.7B |

| Services/SaaS (2024) | $420M |

| Clinics (Q4 2025) | >15,000 |

| Customers / Countries | 150,000 / 100+ |

| On-time fill rate (2024) | 98% |

| Pharmacy growth (2024) | +12% |

| PE dry powder (2024) | >$150B |

What is included in the product

Delivers a strategic overview of Covetrus’s internal strengths and weaknesses and the external opportunities and threats shaping its competitive position in the animal-health and veterinary supply market.

Delivers a concise Covetrus SWOT matrix for rapid strategic alignment across veterinary channels, easing stakeholder briefings and decision-making.

Weaknesses

Substantial Debt Obligations

Following its 2022 take‑private, Covetrus carries roughly $1.8 billion of long‑term debt on the balance sheet; servicing costs rose as U.S. benchmark rates climbed, pushing interest expense above $160 million in FY2024. Higher rates through 2024–2025 have squeezed free cash flow, likely constraining R and D and product investment. This leverage raises bankruptcy and liquidity risk in a downturn and reduces flexibility versus lower‑debt peers.

Legacy System Integration Hurdles

Covetrus was formed by the 2022 merger of Henry Schein Animal Health and Vets First Choice, leaving a tangle of legacy IT stacks; as of Q4 2024 IT consolidation lagged, with management reporting a 15–20% CRM integration gap across markets.

Partial harmonization improved order routing and inventory accuracy, cutting fulfillment errors by 9% in 2024, but full platform sync across 25+ countries remains incomplete.

Inconsistent UX on older modules correlated with a 4% net revenue retention drag in 2024 and higher churn among small clinics, per company disclosures.

Low-Margin Distribution Dependence

A large share of Covetrus revenue—about 60% in FY2024 revenue of $3.6B—comes from third‑party product distribution, which yields materially lower gross margins (~18%) versus its SaaS/technology segment (~65%). This high-volume, low-margin mix makes earnings sensitive to fuel and logistics swings: U.S. diesel rose ~25% year‑over‑year in 2022–23, squeezing distribution margins. Moving mix to higher‑margin SaaS is gradual and needs continual product innovation and sales ramp time.

High Operational Complexity

Managing Covetrus’s global supply chain plus a software development arm creates organizational friction; in 2024 Covetrus reported $3.1B revenue split across distribution and tech services, forcing trade-offs in capital and talent.

The dual business model needs distinct expertise, causing misaligned priorities between logistics and product teams and slowing product-to-market timing in a fast-growing pet health market (global pet care market ~$325B in 2024).

Geographic Concentration in North America

- ~78% revenue from North America (2024)

- International revenue CAGR ~3% (2021–2024)

- Higher sensitivity to US regulation and macro shocks

- Slower-than-expected Asian/Latin American expansion

High Debt, Fragile Growth: 78% NA Revenue, Heavy Distribution, Margin & IT Strain

High leverage: $1.8B long‑term debt; interest expense >$160M FY2024, pressuring FCF. Legacy IT fragmentation: 15–20% CRM integration gap; 4% NRR drag in 2024. Revenue mix weak: 60% low‑margin distribution (≈18% gross); SaaS ~65% gross. Geographic concentration: ~78% revenue North America; intl CAGR ~3% (2021–2024).

| Metric | 2024 |

|---|---|

| Long‑term debt | $1.8B |

| Interest expense | $160M+ |

| Revenue | $3.6B |

| Distribution share | 60% |

| NA revenue share | 78% |

Preview the Actual Deliverable

Covetrus SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

The preview below is taken directly from the full SWOT report you'll get. Purchase unlocks the entire in-depth version.

This is a real excerpt from the complete document. Once purchased, you’ll receive the full, editable version.