Covivio Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

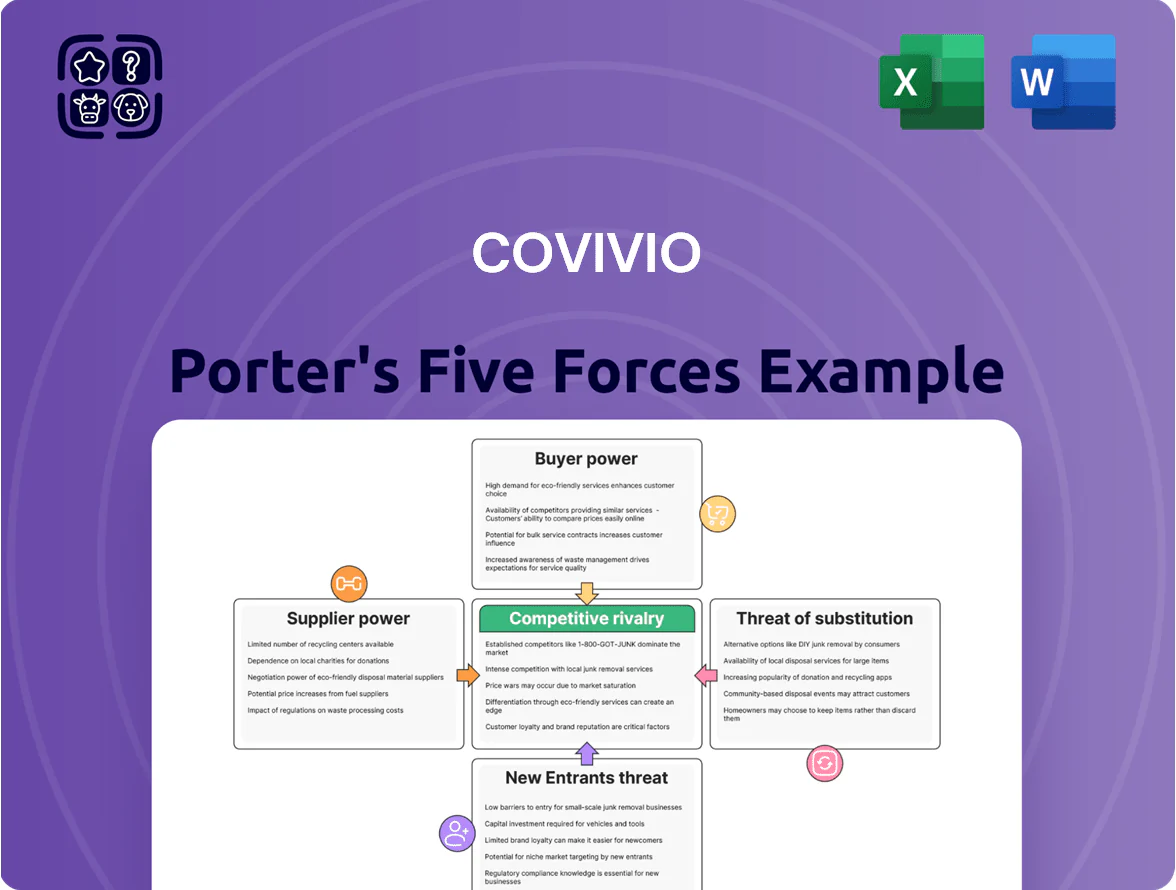

Covivio operates in a capital-intensive, regulation-tinged real estate sector where tenant bargaining power, high fixed costs, and moderate entrant threats shape margins and strategy; its diversified portfolio and scale mitigate some pressures but exposure to cyclical demand and financing risk remains material.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Covivio’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Construction and Material Costs

The cost of raw materials and skilled labor remains a major input for Covivio development projects in late 2025; steel and timber prices rose 4.8% and 3.2% year-on-year in 2024, keeping margins tight. Global supply chains normalized, but specialized sustainable contractors command pricing power amid a 12% EU skilled-construction labor shortfall. Covivio must use multi-year contracts and JV partnerships to lock rates and protect project IRRs.

Access to Debt Financing

Financial institutions and bond markets are key capital suppliers for Covivio; by end-2025 European real estate debt spreads averaged ~180 bps over swaps, lifting funding costs. Lenders now push stricter covenants and ESG-linked terms—about 60% of new CMBS and bank loans include sustainability KPIs in 2025. Covivio must keep leverage and interest coverage near peer bests (LTV ≤40%, ICR ≥3.0x) to win lower-rate financing for urban regeneration.

Availability of Prime Land

Municipalities in Paris, Berlin and Milan control scarce prime land, giving suppliers high bargaining power; Paris saw land transactions fall 12% in 2024 while central Berlin vacancy stayed below 3% in 2025. Covivio reduces supplier leverage by being a preferred partner on complex mixed-use deals—its 2024 €4.1bn development pipeline and 15 active public-private projects strengthen access to regulated sites.

Energy and Utility Providers

Energy suppliers wield moderate bargaining power as EU green rules push shifts: by end-2024 Covivio had 125 GWh/year of on-site renewables under development, cutting grid purchases by ~8% vs 2022, yet 100% of large-scale grid connections and 90% of water management remain outsourced.

- 125 GWh/year renewables pipeline (2024)

- ~8% reduction in grid energy purchases vs 2022

- 100% large-grid connectivity outsourced

- 90% water services outsourced

Specialized PropTech Vendors

Suppliers of smart-building tech and property-management software now hold real sway as digital features become core: Covivio reported €1.9bn in PropTech-related CapEx from 2020–2024, raising reliance on vendors that enable integrated living and working services.

The specialized platforms create vendor lock-in—migration costs and data integration raise switching expenses, giving suppliers bargaining leverage and pressuring margins on service-heavy assets.

- €1.9bn PropTech CapEx (2020–2024)

- High switching costs from proprietary integrations

- Vendors control key data and service roadmaps

Rising supplier power squeezes margins: materials, labor, finance & PropTech lock-in

Suppliers exert moderate-to-high power: materials and skilled labor squeeze margins (steel +4.8%, timber +3.2% in 2024; EU construction labor shortfall ~12% in 2025), financiers demand tighter covenants (2025 EU real-estate debt spreads ~180bps; ~60% ESG-linked loans), municipalities limit prime land (Paris transactions -12% in 2024), and PropTech vendors drive lock-in after €1.9bn CapEx (2020–2024).

| Metric | Value |

|---|---|

| Steel price change (2024) | +4.8% |

| Timber price change (2024) | +3.2% |

| EU skilled labor gap (2025) | ~12% |

| Debt spread (2025) | ~180 bps |

| ESG-linked loans (2025) | ~60% |

| PropTech CapEx (2020–2024) | €1.9bn |

| Paris land transactions (2024) | -12% |

What is included in the product

Provides a concise Porter’s Five Forces review of Covivio, highlighting competitive rivalry, buyer and supplier bargaining power, entry barriers, and substitution risks with actionable insights tailored to its real estate portfolio.

One-sheet Porter's Five Forces for Covivio—quickly spot competitive pressures and investment risks for fast, board-ready decisions.

Customers Bargaining Power

Corporate Office Tenant Leverage

Large corporate tenants demand flexible, high-quality, ESG-compliant offices to attract talent in a hybrid world, and they can trim space or select premium assets—giving them strong bargaining power; European corporate renewals fell 8% in 2024 vs 2019, pushing firms to compete on flexibility. Covivio counters with tailored services, tech-enabled amenities, and ESG certifications (BREEAM/LEED) across ~13.5 million m² of office assets, boosting retention and supporting 5–10% premium rents in core markets.

Residential Tenant Protections

In Germany Covivio faces strong tenant protections and rent brake (Mietpreisbremse) measures that cap initial rent increases; in 2024 average regulated rents rose ~1.2% YoY vs 3.5% market rents in other EU cities, limiting revenue upside.

Legal eviction hurdles and long notice periods boost tenants' bargaining power, forcing Covivio to rely on service quality and maintenance to retain occupancy; German vacancy rate in 2024 was ~1.8%, so retention matters.

Regulation pressures margins: Covivio reported residential NOI margin of ~60% in 2024, so operational efficiency and targeted CapEx on maintenance are key to protect returns.

Hotel Operator Negotiations

Covivio partners with major brands like Accor and Marriott, whose strong brand equity and market data let them negotiate favorable leases or management contracts tied to projected tourism flows; Accor and Marriott together represented over 40% of European chain rooms in 2024.

The partnership model shares operating risk, but Covivio must invest to meet brand standards—Covivio spent €230m on hotel capex in 2024 to upgrade assets and retain operator agreements.

Demand for Flexible Lease Terms

- Flexible office supply +12% Europe 2024

- Covivio flexible-space revenue +15% YoY 2024

- Shorter leases = higher vacancy risk, lower rent visibility

- Portfolio mix: flexible + co-living reduces long-empty units

ESG and Sustainability Demands

Institutional tenants and residents now treat environmental performance as non-negotiable, driving demand for low-carbon, energy-efficient space and giving customers leverage to reject older buildings.

This can cause a brown discount: study data show green-certified offices command 7–12% rent premiums and 10–20% higher occupancy; non-compliant assets face value declines and higher capex needs.

Covivio’s proactive green-renovation strategy—targeting Net Zero Carbon operations by 2050 and accelerating upgrades—reduces brown-risk and preserves rental income and asset value.

- 7–12% rent premium for green offices

- 10–20% higher occupancy for certified assets

- Brown discount risk raises capex and lowers NAV

- Covivio: Net Zero by 2050, ongoing renovations

Covivio doubles down on ESG and flexible space as corporates drive green premium and occupancy

Customers hold strong bargaining power: corporates demand flexible, ESG-certified space (green premium 7–12%, occupancy +10–20%), flexible-office supply rose 12% in Europe 2024, and Covivio’s flexible revenue grew 15% YoY while investing €230m hotel capex and targeting Net Zero by 2050 to defend rents and retention.

| Metric | 2024 |

|---|---|

| Flexible supply Europe | +12% |

| Covivio flexible rev | +15% YoY |

| Green rent premium | 7–12% |

| Green occupancy lift | 10–20% |

| Hotel capex | €230m |

Full Version Awaits

Covivio Porter's Five Forces Analysis

This preview shows the exact Covivio Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the same professionally written, fully formatted file you’ll be able to download and use the moment you buy. You’re previewing the final version—precisely the deliverable available instantly after payment. No mockups, no samples: this is the complete, ready-to-use analysis.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Covivio operates in a capital-intensive, regulation-tinged real estate sector where tenant bargaining power, high fixed costs, and moderate entrant threats shape margins and strategy; its diversified portfolio and scale mitigate some pressures but exposure to cyclical demand and financing risk remains material.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Covivio’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Construction and Material Costs

The cost of raw materials and skilled labor remains a major input for Covivio development projects in late 2025; steel and timber prices rose 4.8% and 3.2% year-on-year in 2024, keeping margins tight. Global supply chains normalized, but specialized sustainable contractors command pricing power amid a 12% EU skilled-construction labor shortfall. Covivio must use multi-year contracts and JV partnerships to lock rates and protect project IRRs.

Access to Debt Financing

Financial institutions and bond markets are key capital suppliers for Covivio; by end-2025 European real estate debt spreads averaged ~180 bps over swaps, lifting funding costs. Lenders now push stricter covenants and ESG-linked terms—about 60% of new CMBS and bank loans include sustainability KPIs in 2025. Covivio must keep leverage and interest coverage near peer bests (LTV ≤40%, ICR ≥3.0x) to win lower-rate financing for urban regeneration.

Availability of Prime Land

Municipalities in Paris, Berlin and Milan control scarce prime land, giving suppliers high bargaining power; Paris saw land transactions fall 12% in 2024 while central Berlin vacancy stayed below 3% in 2025. Covivio reduces supplier leverage by being a preferred partner on complex mixed-use deals—its 2024 €4.1bn development pipeline and 15 active public-private projects strengthen access to regulated sites.

Energy and Utility Providers

Energy suppliers wield moderate bargaining power as EU green rules push shifts: by end-2024 Covivio had 125 GWh/year of on-site renewables under development, cutting grid purchases by ~8% vs 2022, yet 100% of large-scale grid connections and 90% of water management remain outsourced.

- 125 GWh/year renewables pipeline (2024)

- ~8% reduction in grid energy purchases vs 2022

- 100% large-grid connectivity outsourced

- 90% water services outsourced

Specialized PropTech Vendors

Suppliers of smart-building tech and property-management software now hold real sway as digital features become core: Covivio reported €1.9bn in PropTech-related CapEx from 2020–2024, raising reliance on vendors that enable integrated living and working services.

The specialized platforms create vendor lock-in—migration costs and data integration raise switching expenses, giving suppliers bargaining leverage and pressuring margins on service-heavy assets.

- €1.9bn PropTech CapEx (2020–2024)

- High switching costs from proprietary integrations

- Vendors control key data and service roadmaps

Rising supplier power squeezes margins: materials, labor, finance & PropTech lock-in

Suppliers exert moderate-to-high power: materials and skilled labor squeeze margins (steel +4.8%, timber +3.2% in 2024; EU construction labor shortfall ~12% in 2025), financiers demand tighter covenants (2025 EU real-estate debt spreads ~180bps; ~60% ESG-linked loans), municipalities limit prime land (Paris transactions -12% in 2024), and PropTech vendors drive lock-in after €1.9bn CapEx (2020–2024).

| Metric | Value |

|---|---|

| Steel price change (2024) | +4.8% |

| Timber price change (2024) | +3.2% |

| EU skilled labor gap (2025) | ~12% |

| Debt spread (2025) | ~180 bps |

| ESG-linked loans (2025) | ~60% |

| PropTech CapEx (2020–2024) | €1.9bn |

| Paris land transactions (2024) | -12% |

What is included in the product

Provides a concise Porter’s Five Forces review of Covivio, highlighting competitive rivalry, buyer and supplier bargaining power, entry barriers, and substitution risks with actionable insights tailored to its real estate portfolio.

One-sheet Porter's Five Forces for Covivio—quickly spot competitive pressures and investment risks for fast, board-ready decisions.

Customers Bargaining Power

Corporate Office Tenant Leverage

Large corporate tenants demand flexible, high-quality, ESG-compliant offices to attract talent in a hybrid world, and they can trim space or select premium assets—giving them strong bargaining power; European corporate renewals fell 8% in 2024 vs 2019, pushing firms to compete on flexibility. Covivio counters with tailored services, tech-enabled amenities, and ESG certifications (BREEAM/LEED) across ~13.5 million m² of office assets, boosting retention and supporting 5–10% premium rents in core markets.

Residential Tenant Protections

In Germany Covivio faces strong tenant protections and rent brake (Mietpreisbremse) measures that cap initial rent increases; in 2024 average regulated rents rose ~1.2% YoY vs 3.5% market rents in other EU cities, limiting revenue upside.

Legal eviction hurdles and long notice periods boost tenants' bargaining power, forcing Covivio to rely on service quality and maintenance to retain occupancy; German vacancy rate in 2024 was ~1.8%, so retention matters.

Regulation pressures margins: Covivio reported residential NOI margin of ~60% in 2024, so operational efficiency and targeted CapEx on maintenance are key to protect returns.

Hotel Operator Negotiations

Covivio partners with major brands like Accor and Marriott, whose strong brand equity and market data let them negotiate favorable leases or management contracts tied to projected tourism flows; Accor and Marriott together represented over 40% of European chain rooms in 2024.

The partnership model shares operating risk, but Covivio must invest to meet brand standards—Covivio spent €230m on hotel capex in 2024 to upgrade assets and retain operator agreements.

Demand for Flexible Lease Terms

- Flexible office supply +12% Europe 2024

- Covivio flexible-space revenue +15% YoY 2024

- Shorter leases = higher vacancy risk, lower rent visibility

- Portfolio mix: flexible + co-living reduces long-empty units

ESG and Sustainability Demands

Institutional tenants and residents now treat environmental performance as non-negotiable, driving demand for low-carbon, energy-efficient space and giving customers leverage to reject older buildings.

This can cause a brown discount: study data show green-certified offices command 7–12% rent premiums and 10–20% higher occupancy; non-compliant assets face value declines and higher capex needs.

Covivio’s proactive green-renovation strategy—targeting Net Zero Carbon operations by 2050 and accelerating upgrades—reduces brown-risk and preserves rental income and asset value.

- 7–12% rent premium for green offices

- 10–20% higher occupancy for certified assets

- Brown discount risk raises capex and lowers NAV

- Covivio: Net Zero by 2050, ongoing renovations

Covivio doubles down on ESG and flexible space as corporates drive green premium and occupancy

Customers hold strong bargaining power: corporates demand flexible, ESG-certified space (green premium 7–12%, occupancy +10–20%), flexible-office supply rose 12% in Europe 2024, and Covivio’s flexible revenue grew 15% YoY while investing €230m hotel capex and targeting Net Zero by 2050 to defend rents and retention.

| Metric | 2024 |

|---|---|

| Flexible supply Europe | +12% |

| Covivio flexible rev | +15% YoY |

| Green rent premium | 7–12% |

| Green occupancy lift | 10–20% |

| Hotel capex | €230m |

Full Version Awaits

Covivio Porter's Five Forces Analysis

This preview shows the exact Covivio Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the same professionally written, fully formatted file you’ll be able to download and use the moment you buy. You’re previewing the final version—precisely the deliverable available instantly after payment. No mockups, no samples: this is the complete, ready-to-use analysis.