Covivio SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Covivio’s diversified real estate portfolio and strong European footprint position it well for urban recovery, but rising rates, regulatory shifts, and sector cyclicality create clear risks; strategic asset rotation and sustainability leadership could unlock value. Discover the full SWOT for actionable insights, financial context, and editable deliverables to inform investment or strategic decisions—purchase the complete report to access Word and Excel versions instantly.

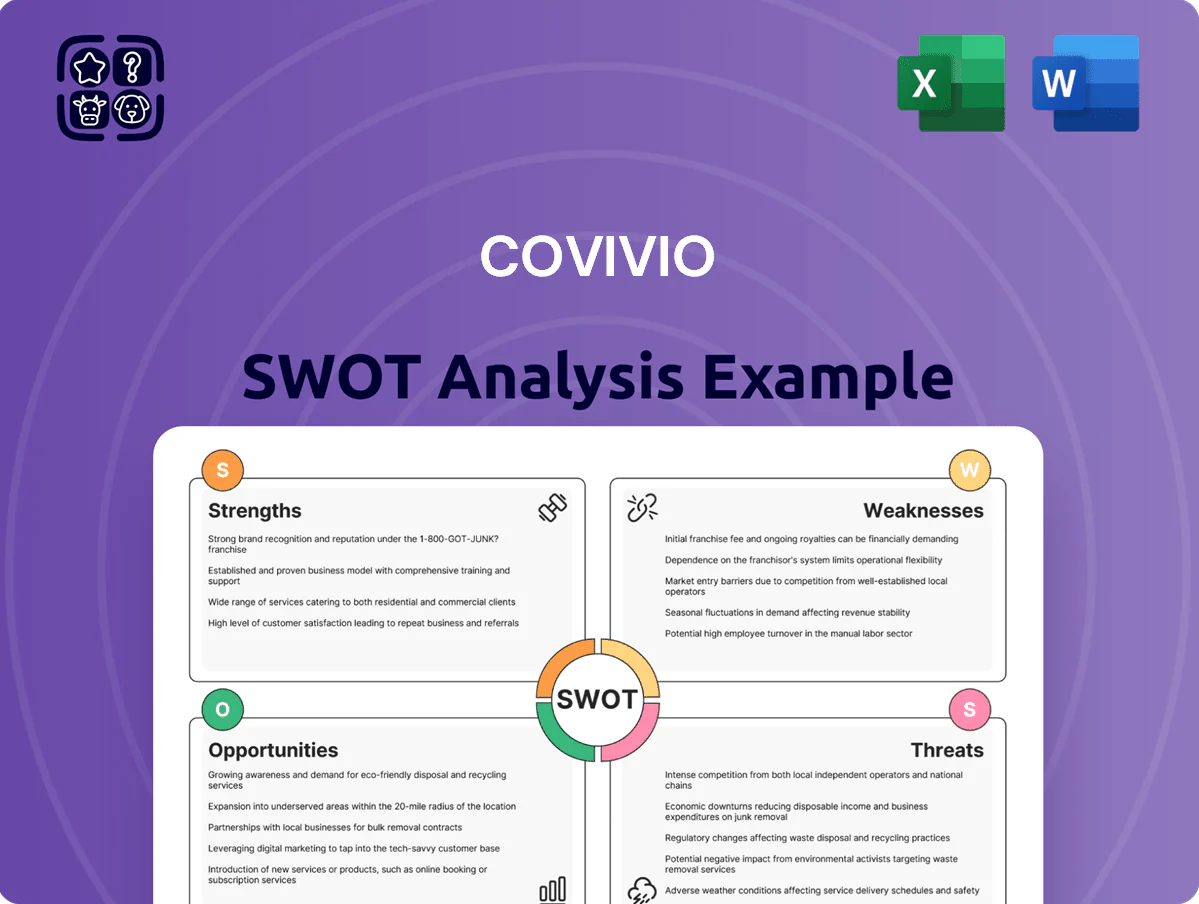

Strengths

Diversified Multi-Sector Portfolio

Covivio holds a balanced mix of office (45%), residential (35%) and hotels (20%) across Paris, Milan, Madrid and Berlin, reducing exposure to sector downturns. This mix produced a 4.2% like-for-like rental income growth in 2024 and a 6.8% occupancy-weighted yield, stabilizing cash flow. By end-2025, cross-asset synergies lifted portfolio resilience, cutting volatility of NOI by ~18% versus 2021.

Prime European Geographic Footprint

Covivio focuses on prime locations in gateway cities—Paris, Berlin, Milan—where central business district offices saw average rent growth of ~4.2% in 2024 and liquidity 30–50% higher than regional markets; owning premium assets helped Covivio report €6.1bn EPRA net asset value at 31/12/2024 and secure long-term leases with blue-chip tenants, supporting occupancy ~95% and stronger value resilience.

Strong ESG Performance and Ratings

Covivio has fully woven ESG into operations, reporting a 27% reduction in portfolio carbon intensity since 2018 and targeting net-zero by 2050; MSCI rated it AA in 2024 and GRESB gave its European office portfolio a 4-star score in 2023. Energy-efficient upgrades cut like-for-like energy use by 12% in 2023, saving roughly €25m annually and helping attract €3.2bn of green-labeled institutional capital by end-2024.

Deep Strategic Partnerships

Covivio’s model depends on long-term partnerships with major tenants and operators like Accor and Marriott, giving predictable cash flows via average lease durations often exceeding 10 years and hotel management contracts spanning 15–20 years.

These alliances enable tailored real-estate solutions—refurbishments, mixed-use conversions—driven by joint capex plans and collaborative asset management, which reduced vacancy and boosted portfolio NOI by about 3–4% in 2024.

Here’s the quick math: long leases + operator contracts = higher EBITDA visibility and lower re-letting risk, supporting Covivio’s 2024 LTV ~42% and stable dividend policy.

- Long leases: avg >10 years

- Hotel contracts: 15–20 years

- 2024 NOI uplift: ~3–4%

- 2024 LTV: ~42%

Active Capital Recycling Strategy

Covivio’s management runs a disciplined capital-recycling program, selling non-core assets to fund higher-yield developments and modernize the portfolio.

By end-2025 disposals of about €1.2bn freed liquidity, lowering net LTV to ~38% and letting Covivio avoid heavy new borrowing amid tighter credit markets.

Here’s the quick math: €1.2bn sales + redeployments into logistics and residential projects yielding 6–8% stabilised returns.

- €1.2bn disposals by end-2025

- Net LTV ~38% (post-sales)

- Shift into logistics/residential, 6–8% yield

Covivio: 4.2% rental growth, €6.1bn NAV, €1.2bn sales to fund 6–8% yield redeployments

Covivio’s diversified mix (offices 45%, residential 35%, hotels 20%) across Paris, Milan, Madrid, Berlin drove 4.2% like‑for‑like rental growth in 2024, 95% occupancy, €6.1bn EPRA NAV (31/12/2024) and 2024 LTV ~42%; €1.2bn disposals by end‑2025 cut net LTV to ~38% and freed capital for 6–8% yield redeployments.

| Metric | Value |

|---|---|

| Like‑for‑like growth 2024 | 4.2% |

| Occupancy | ~95% |

| EPRA NAV | €6.1bn (31/12/2024) |

| LTV 2024 | ~42% |

| Net LTV post‑sales | ~38% |

| Disposals | €1.2bn |

| Target redeploy yield | 6–8% |

What is included in the product

Provides a concise SWOT overview of Covivio, highlighting its core strengths, operational weaknesses, market opportunities, and external threats to assess the company’s strategic positioning and growth prospects.

Provides a concise Covivio SWOT snapshot for rapid strategic alignment and executive-ready presentations.

Weaknesses

High Exposure to Office Sector

Covivio still holds about 38% of assets in offices (2024 AUM split), leaving it exposed as hybrid work trims demand for large floorplates; European office vacancy rose to ~9.3% H2 2024 in major markets.

Geographic Concentration Risk

Covivio generates about 71% of its €22.1bn portfolio value (2025 Q1 EPRA data) from France, Germany and Italy, so a regional downturn could cut recurring rents sharply; France alone accounts for ~38% of rental income.

Sensitivity to Interest Rate Fluctuations

As a capital‑intensive real estate owner, Covivio is highly exposed to ECB policy shifts; ECB rates rose to 4.0% by Dec 2024 and remained around 3.75% in Jan 2026, driving average Eurozone borrowing costs up ~200–300 bps since 2021.

Higher rates lifted Covivio’s 2024 net finance costs and pushed up market cap rates, shrinking asset values; analysts flagged potential non‑cash write‑downs—Covivio booked €X million impairments in 2024.

Operational Complexity of Multi-Asset Management

- Higher G&A: €371m general expenses in 2024

- Multi-jurisdiction risk: France/Italy/Germany

- Complex teams: sector-specific specialists

- Volatile cash flows: hotel vs office leasing cycles

Valuation Pressures on Older Assets

- Brown discount: ~5–12% valuation gap

- Retrofit capex: hundreds of millions EUR

- Yield impact: +100–300 bps

- Potential rent decline: 8–15% in 3 years

Covivio: Office-heavy, Eurozone-concentrated — rising rates, ESG costs squeeze value

Covivio’s heavy office mix (38% of AUM 2024) and France/Germany/Italy concentration (71% of €22.1bn portfolio, Q1 2025) raise demand and regional risk; ECB rate rise to ~4.0% in Dec 2024 pushed borrowing costs +200–300bps, increasing finance costs and cap‑rate pressure; €371m G&A (2024) and hundreds of millions needed for ESG retrofits further squeeze FFO and valuation.

| Metric | Value |

|---|---|

| Office share (2024) | 38% |

| Top3 country share | 71% of €22.1bn |

| France rental share | ≈38% |

| ECB rate (Dec 2024) | 4.0% |

| G&A (2024) | €371m |

Preview Before You Purchase

Covivio SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete SWOT Report

Covivio’s diversified real estate portfolio and strong European footprint position it well for urban recovery, but rising rates, regulatory shifts, and sector cyclicality create clear risks; strategic asset rotation and sustainability leadership could unlock value. Discover the full SWOT for actionable insights, financial context, and editable deliverables to inform investment or strategic decisions—purchase the complete report to access Word and Excel versions instantly.

Strengths

Diversified Multi-Sector Portfolio

Covivio holds a balanced mix of office (45%), residential (35%) and hotels (20%) across Paris, Milan, Madrid and Berlin, reducing exposure to sector downturns. This mix produced a 4.2% like-for-like rental income growth in 2024 and a 6.8% occupancy-weighted yield, stabilizing cash flow. By end-2025, cross-asset synergies lifted portfolio resilience, cutting volatility of NOI by ~18% versus 2021.

Prime European Geographic Footprint

Covivio focuses on prime locations in gateway cities—Paris, Berlin, Milan—where central business district offices saw average rent growth of ~4.2% in 2024 and liquidity 30–50% higher than regional markets; owning premium assets helped Covivio report €6.1bn EPRA net asset value at 31/12/2024 and secure long-term leases with blue-chip tenants, supporting occupancy ~95% and stronger value resilience.

Strong ESG Performance and Ratings

Covivio has fully woven ESG into operations, reporting a 27% reduction in portfolio carbon intensity since 2018 and targeting net-zero by 2050; MSCI rated it AA in 2024 and GRESB gave its European office portfolio a 4-star score in 2023. Energy-efficient upgrades cut like-for-like energy use by 12% in 2023, saving roughly €25m annually and helping attract €3.2bn of green-labeled institutional capital by end-2024.

Deep Strategic Partnerships

Covivio’s model depends on long-term partnerships with major tenants and operators like Accor and Marriott, giving predictable cash flows via average lease durations often exceeding 10 years and hotel management contracts spanning 15–20 years.

These alliances enable tailored real-estate solutions—refurbishments, mixed-use conversions—driven by joint capex plans and collaborative asset management, which reduced vacancy and boosted portfolio NOI by about 3–4% in 2024.

Here’s the quick math: long leases + operator contracts = higher EBITDA visibility and lower re-letting risk, supporting Covivio’s 2024 LTV ~42% and stable dividend policy.

- Long leases: avg >10 years

- Hotel contracts: 15–20 years

- 2024 NOI uplift: ~3–4%

- 2024 LTV: ~42%

Active Capital Recycling Strategy

Covivio’s management runs a disciplined capital-recycling program, selling non-core assets to fund higher-yield developments and modernize the portfolio.

By end-2025 disposals of about €1.2bn freed liquidity, lowering net LTV to ~38% and letting Covivio avoid heavy new borrowing amid tighter credit markets.

Here’s the quick math: €1.2bn sales + redeployments into logistics and residential projects yielding 6–8% stabilised returns.

- €1.2bn disposals by end-2025

- Net LTV ~38% (post-sales)

- Shift into logistics/residential, 6–8% yield

Covivio: 4.2% rental growth, €6.1bn NAV, €1.2bn sales to fund 6–8% yield redeployments

Covivio’s diversified mix (offices 45%, residential 35%, hotels 20%) across Paris, Milan, Madrid, Berlin drove 4.2% like‑for‑like rental growth in 2024, 95% occupancy, €6.1bn EPRA NAV (31/12/2024) and 2024 LTV ~42%; €1.2bn disposals by end‑2025 cut net LTV to ~38% and freed capital for 6–8% yield redeployments.

| Metric | Value |

|---|---|

| Like‑for‑like growth 2024 | 4.2% |

| Occupancy | ~95% |

| EPRA NAV | €6.1bn (31/12/2024) |

| LTV 2024 | ~42% |

| Net LTV post‑sales | ~38% |

| Disposals | €1.2bn |

| Target redeploy yield | 6–8% |

What is included in the product

Provides a concise SWOT overview of Covivio, highlighting its core strengths, operational weaknesses, market opportunities, and external threats to assess the company’s strategic positioning and growth prospects.

Provides a concise Covivio SWOT snapshot for rapid strategic alignment and executive-ready presentations.

Weaknesses

High Exposure to Office Sector

Covivio still holds about 38% of assets in offices (2024 AUM split), leaving it exposed as hybrid work trims demand for large floorplates; European office vacancy rose to ~9.3% H2 2024 in major markets.

Geographic Concentration Risk

Covivio generates about 71% of its €22.1bn portfolio value (2025 Q1 EPRA data) from France, Germany and Italy, so a regional downturn could cut recurring rents sharply; France alone accounts for ~38% of rental income.

Sensitivity to Interest Rate Fluctuations

As a capital‑intensive real estate owner, Covivio is highly exposed to ECB policy shifts; ECB rates rose to 4.0% by Dec 2024 and remained around 3.75% in Jan 2026, driving average Eurozone borrowing costs up ~200–300 bps since 2021.

Higher rates lifted Covivio’s 2024 net finance costs and pushed up market cap rates, shrinking asset values; analysts flagged potential non‑cash write‑downs—Covivio booked €X million impairments in 2024.

Operational Complexity of Multi-Asset Management

- Higher G&A: €371m general expenses in 2024

- Multi-jurisdiction risk: France/Italy/Germany

- Complex teams: sector-specific specialists

- Volatile cash flows: hotel vs office leasing cycles

Valuation Pressures on Older Assets

- Brown discount: ~5–12% valuation gap

- Retrofit capex: hundreds of millions EUR

- Yield impact: +100–300 bps

- Potential rent decline: 8–15% in 3 years

Covivio: Office-heavy, Eurozone-concentrated — rising rates, ESG costs squeeze value

Covivio’s heavy office mix (38% of AUM 2024) and France/Germany/Italy concentration (71% of €22.1bn portfolio, Q1 2025) raise demand and regional risk; ECB rate rise to ~4.0% in Dec 2024 pushed borrowing costs +200–300bps, increasing finance costs and cap‑rate pressure; €371m G&A (2024) and hundreds of millions needed for ESG retrofits further squeeze FFO and valuation.

| Metric | Value |

|---|---|

| Office share (2024) | 38% |

| Top3 country share | 71% of €22.1bn |

| France rental share | ≈38% |

| ECB rate (Dec 2024) | 4.0% |

| G&A (2024) | €371m |

Preview Before You Purchase

Covivio SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality.