China Power International Development SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

China Power International Development faces solid state-backed scale and a growing renewables pipeline, yet contends with commodity volatility and regulatory shifts that could affect margins.

Want the full story behind the company’s strengths, risks, and growth drivers? Purchase the complete SWOT analysis to gain access to a professionally written, fully editable report designed to support planning, pitches, and research.

Don’t settle for a snapshot—unlock the full SWOT report to gain detailed strategic insights, editable tools, and a high-level summary in Excel. Perfect for smart, fast decision-making.

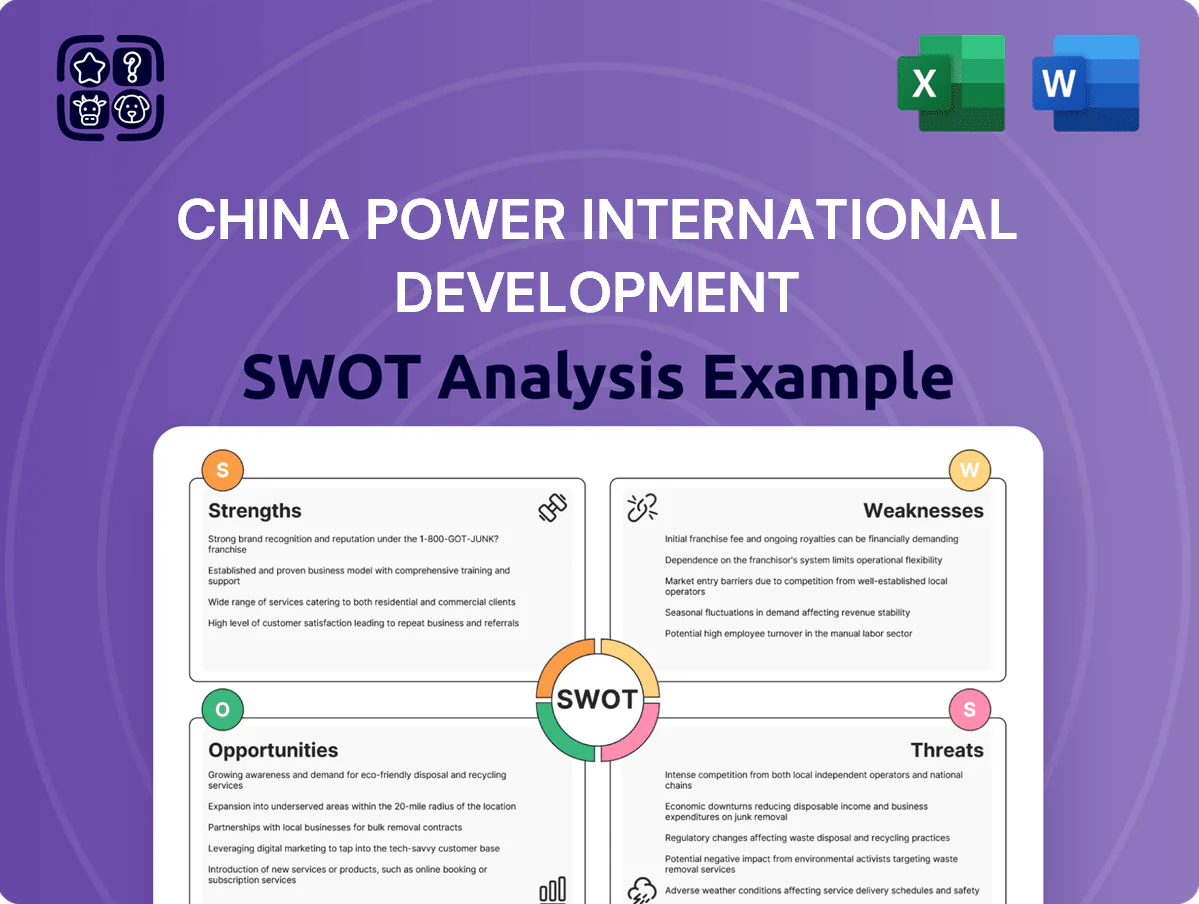

Strengths

Dominant Clean Energy Portfolio

By late 2025 China Power International Development has shifted to a majority-clean portfolio: renewables (wind, solar, hydro) made up roughly 62% of installed capacity (~28.4 GW of 45.9 GW), aligning with China’s 2060 carbon-neutral pathway and giving a clear edge versus coal-heavy peers.

Strong State-Owned Enterprise Support

As a core subsidiary of State Power Investment Corporation (SPIC), China Power International Development (CPID) benefits from sovereign-backed support—SPIC reported RMB 603.4 billion in assets and RMB 50.2 billion net profit in 2024—easing financing for large projects.

This link yields preferential positioning in national energy plans, helping CPID secure utility-scale projects; SPIC’s 2024 capital injections and group-level bidding wins drove 18% capacity additions year-on-year.

SPIC provides a capital safety net for CPID’s capital-intensive transitions and tech sharing across generation, grids, and renewables, lowering project WACC and speeding deployment.

Integrated Energy Storage Capabilities

China Power International Development has pioneered large-scale battery and pumped storage integration at its wind and solar farms, adding about 1.2 GW/4.8 GWh of storage capacity by end-2025 to cut intermittency and smooth output.

Those assets improved grid stability and enabled capturing higher peak-load prices, increasing renewable merchant revenue by an estimated CNY 1.1 billion in 2025.

This technical expertise and integrated capex—roughly CNY 8.6 billion invested since 2022—create a high barrier to entry for smaller rivals without similar infrastructure.

Geographic Diversification within China

- 20+ provinces: diversified demand exposure

- 45% of 90 TWh (2024) from renewables

- Sites across climates: solar, wind, hydro mix

- Proximity to Guangdong/Jiangsu/Shandong hubs

Favorable Financing and Credit Profile

China Power International Development (state-owned) benefits from AA-/A+ sovereign-linked credit context and issued RMB 6.8 billion green bonds in 2023, giving access to cheaper green financing and sustainability-linked loans.

This lowers blended interest costs—about 2.9% vs ~4.5% for private peers—supporting heavy capex for 2024–26 expansion and lifting 2024 net margin by ~1.2 ppt vs peers.

SPIC-backed 62% renewable fleet (45.9GW) — cheap capital, 90TWh nation‑wide

Majority-clean fleet: 62% renewables (28.4 GW/45.9 GW) by late-2025; 1.2 GW/4.8 GWh storage added. Sovereign-backed via SPIC (RMB 603.4bn assets; RMB 50.2bn net profit 2024) enabling cheap capital—RMB 6.8bn green bonds (2023), blended cost ~2.9%. Nationwide footprint: 20+ provinces, 90 TWh gen (45% renewables, 2024); strategic hubs near Guangdong/Jiangsu/Shandong.

| Metric | Value |

|---|---|

| Installed capacity | 45.9 GW |

| Renewables | 28.4 GW (62%) |

| Storage | 1.2 GW / 4.8 GWh |

| Generation | 90 TWh (45% renew) |

| SPIC assets | RMB 603.4bn |

| SPIC net profit 2024 | RMB 50.2bn |

| Green bonds (2023) | RMB 6.8bn |

| Blended cost | ~2.9% |

| Provincial reach | 20+ |

What is included in the product

Provides a concise SWOT overview of China Power International Development, outlining its core strengths and weaknesses alongside market opportunities and external threats shaping its strategic outlook.

Delivers a concise SWOT matrix for China Power International Development to speed strategic alignment and decision-making across teams.

Weaknesses

Residual Coal Exposure

Despite a push into renewables, about 28% of China Power International Development’s 2024 installed capacity remained coal-fired (Wind & Solar 2024 report), exposing the firm to volatile thermal coal prices (spot up 46% in 2023–24) and rising China carbon prices (national ETS average ~54 CNY/t in 2024), which can cut margins; management must retire plants carefully to preserve baseload reliability while managing stranded-asset risk and closure costs.

High Debt-to-Equity Levels

Rapid expansion into wind and solar forced China Power International Development to borrow heavily; net debt rose to HKD 72.3 billion by FY2024 (Dec 31, 2024), leaving a debt-to-equity ratio near 1.8x and a leverage profile above industry peers. While interest rates stayed moderate—effective borrowing cost ~4.6% in 2024—high leverage reduces agility to absorb market shocks and constrains capital reallocation. Debt service consumed roughly 28% of 2024 operating cash flow, limiting reinvestment.

Dependence on Government Subsidies

Operational Rigidity of Large Scale Assets

The company’s 2025 fleet—about 20 GW hydro and 15 GW thermal—creates operational inertia, so integrating new tech is slow and costly compared with modular competitors.

Upgrades to dam and coal-fired units need multi-year engineering and CAPEX; a single large retrofit can exceed CNY billions and take 3–5 years, limiting quick pivots to SMRs or advanced biomass.

- 20 GW hydro, 15 GW thermal (2025)

- Major retrofits: CNY billions, 3–5 years

- Hard to adopt niche tech fast (SMRs, advanced biomass)

Sensitivity to Power Dispatch Policies

China Power International Developments revenue depends heavily on dispatch priority from regional grid operators and provincial governments, with 2024 renewables curtailment in some provinces reaching double-digit percentages (e.g., 11% in Northwest regions), directly cutting sellable output.

Local protectionism and shifting grid priorities can force curtailment, as seen in 2023–24 where curtailed wind/solar reduced group generation forecasts by several percentage points, raising volatility in annual revenue projections.

This reliance on external administrative dispatch adds uncertainty to production forecasts and cash flow planning, making sensitivity to policy shifts a material operational risk for investors.

- 2024 regional curtailment up to 11%

- Revenue tied to provincial dispatch rules

- Forecast variance of several percentage points

- Policy changes create cash-flow volatility

High coal exposure, HKD72.3bn debt and rising carbon costs threaten cash flows

Heavy coal legacy (15 GW thermal, 28% capacity coal in 2024) and HKD 72.3bn net debt (Dec 31, 2024) raise stranded-asset and leverage risk; carbon price (~54 CNY/t in 2024) and 2023–24 spot coal +46% squeeze margins; subsidy rollback (20–30% legacy tariffs) and up to 11% regional curtailment in 2024 add cash‑flow volatility.

| Metric | Value |

|---|---|

| Coal share (2024) | 28% |

| Thermal capacity (2025) | 15 GW |

| Net debt (FY2024) | HKD 72.3 bn |

| Carbon price (2024) | ~54 CNY/t |

| Coal spot change (2023–24) | +46% |

| Legacy tariff exposure | 20–30% |

| Max regional curtailment (2024) | 11% |

What You See Is What You Get

China Power International Development SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; it’s a real excerpt from the complete, editable file. You’re viewing a live preview of the same analysis document included in your download—buy now to unlock the full, detailed version.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Elevate Your Analysis with the Complete SWOT Report

China Power International Development faces solid state-backed scale and a growing renewables pipeline, yet contends with commodity volatility and regulatory shifts that could affect margins.

Want the full story behind the company’s strengths, risks, and growth drivers? Purchase the complete SWOT analysis to gain access to a professionally written, fully editable report designed to support planning, pitches, and research.

Don’t settle for a snapshot—unlock the full SWOT report to gain detailed strategic insights, editable tools, and a high-level summary in Excel. Perfect for smart, fast decision-making.

Strengths

Dominant Clean Energy Portfolio

By late 2025 China Power International Development has shifted to a majority-clean portfolio: renewables (wind, solar, hydro) made up roughly 62% of installed capacity (~28.4 GW of 45.9 GW), aligning with China’s 2060 carbon-neutral pathway and giving a clear edge versus coal-heavy peers.

Strong State-Owned Enterprise Support

As a core subsidiary of State Power Investment Corporation (SPIC), China Power International Development (CPID) benefits from sovereign-backed support—SPIC reported RMB 603.4 billion in assets and RMB 50.2 billion net profit in 2024—easing financing for large projects.

This link yields preferential positioning in national energy plans, helping CPID secure utility-scale projects; SPIC’s 2024 capital injections and group-level bidding wins drove 18% capacity additions year-on-year.

SPIC provides a capital safety net for CPID’s capital-intensive transitions and tech sharing across generation, grids, and renewables, lowering project WACC and speeding deployment.

Integrated Energy Storage Capabilities

China Power International Development has pioneered large-scale battery and pumped storage integration at its wind and solar farms, adding about 1.2 GW/4.8 GWh of storage capacity by end-2025 to cut intermittency and smooth output.

Those assets improved grid stability and enabled capturing higher peak-load prices, increasing renewable merchant revenue by an estimated CNY 1.1 billion in 2025.

This technical expertise and integrated capex—roughly CNY 8.6 billion invested since 2022—create a high barrier to entry for smaller rivals without similar infrastructure.

Geographic Diversification within China

- 20+ provinces: diversified demand exposure

- 45% of 90 TWh (2024) from renewables

- Sites across climates: solar, wind, hydro mix

- Proximity to Guangdong/Jiangsu/Shandong hubs

Favorable Financing and Credit Profile

China Power International Development (state-owned) benefits from AA-/A+ sovereign-linked credit context and issued RMB 6.8 billion green bonds in 2023, giving access to cheaper green financing and sustainability-linked loans.

This lowers blended interest costs—about 2.9% vs ~4.5% for private peers—supporting heavy capex for 2024–26 expansion and lifting 2024 net margin by ~1.2 ppt vs peers.

SPIC-backed 62% renewable fleet (45.9GW) — cheap capital, 90TWh nation‑wide

Majority-clean fleet: 62% renewables (28.4 GW/45.9 GW) by late-2025; 1.2 GW/4.8 GWh storage added. Sovereign-backed via SPIC (RMB 603.4bn assets; RMB 50.2bn net profit 2024) enabling cheap capital—RMB 6.8bn green bonds (2023), blended cost ~2.9%. Nationwide footprint: 20+ provinces, 90 TWh gen (45% renewables, 2024); strategic hubs near Guangdong/Jiangsu/Shandong.

| Metric | Value |

|---|---|

| Installed capacity | 45.9 GW |

| Renewables | 28.4 GW (62%) |

| Storage | 1.2 GW / 4.8 GWh |

| Generation | 90 TWh (45% renew) |

| SPIC assets | RMB 603.4bn |

| SPIC net profit 2024 | RMB 50.2bn |

| Green bonds (2023) | RMB 6.8bn |

| Blended cost | ~2.9% |

| Provincial reach | 20+ |

What is included in the product

Provides a concise SWOT overview of China Power International Development, outlining its core strengths and weaknesses alongside market opportunities and external threats shaping its strategic outlook.

Delivers a concise SWOT matrix for China Power International Development to speed strategic alignment and decision-making across teams.

Weaknesses

Residual Coal Exposure

Despite a push into renewables, about 28% of China Power International Development’s 2024 installed capacity remained coal-fired (Wind & Solar 2024 report), exposing the firm to volatile thermal coal prices (spot up 46% in 2023–24) and rising China carbon prices (national ETS average ~54 CNY/t in 2024), which can cut margins; management must retire plants carefully to preserve baseload reliability while managing stranded-asset risk and closure costs.

High Debt-to-Equity Levels

Rapid expansion into wind and solar forced China Power International Development to borrow heavily; net debt rose to HKD 72.3 billion by FY2024 (Dec 31, 2024), leaving a debt-to-equity ratio near 1.8x and a leverage profile above industry peers. While interest rates stayed moderate—effective borrowing cost ~4.6% in 2024—high leverage reduces agility to absorb market shocks and constrains capital reallocation. Debt service consumed roughly 28% of 2024 operating cash flow, limiting reinvestment.

Dependence on Government Subsidies

Operational Rigidity of Large Scale Assets

The company’s 2025 fleet—about 20 GW hydro and 15 GW thermal—creates operational inertia, so integrating new tech is slow and costly compared with modular competitors.

Upgrades to dam and coal-fired units need multi-year engineering and CAPEX; a single large retrofit can exceed CNY billions and take 3–5 years, limiting quick pivots to SMRs or advanced biomass.

- 20 GW hydro, 15 GW thermal (2025)

- Major retrofits: CNY billions, 3–5 years

- Hard to adopt niche tech fast (SMRs, advanced biomass)

Sensitivity to Power Dispatch Policies

China Power International Developments revenue depends heavily on dispatch priority from regional grid operators and provincial governments, with 2024 renewables curtailment in some provinces reaching double-digit percentages (e.g., 11% in Northwest regions), directly cutting sellable output.

Local protectionism and shifting grid priorities can force curtailment, as seen in 2023–24 where curtailed wind/solar reduced group generation forecasts by several percentage points, raising volatility in annual revenue projections.

This reliance on external administrative dispatch adds uncertainty to production forecasts and cash flow planning, making sensitivity to policy shifts a material operational risk for investors.

- 2024 regional curtailment up to 11%

- Revenue tied to provincial dispatch rules

- Forecast variance of several percentage points

- Policy changes create cash-flow volatility

High coal exposure, HKD72.3bn debt and rising carbon costs threaten cash flows

Heavy coal legacy (15 GW thermal, 28% capacity coal in 2024) and HKD 72.3bn net debt (Dec 31, 2024) raise stranded-asset and leverage risk; carbon price (~54 CNY/t in 2024) and 2023–24 spot coal +46% squeeze margins; subsidy rollback (20–30% legacy tariffs) and up to 11% regional curtailment in 2024 add cash‑flow volatility.

| Metric | Value |

|---|---|

| Coal share (2024) | 28% |

| Thermal capacity (2025) | 15 GW |

| Net debt (FY2024) | HKD 72.3 bn |

| Carbon price (2024) | ~54 CNY/t |

| Coal spot change (2023–24) | +46% |

| Legacy tariff exposure | 20–30% |

| Max regional curtailment (2024) | 11% |

What You See Is What You Get

China Power International Development SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get; it’s a real excerpt from the complete, editable file. You’re viewing a live preview of the same analysis document included in your download—buy now to unlock the full, detailed version.