Canadian Pacific Kansas City Porter's Five Forces Analysis

Don't Miss the Bigger Picture

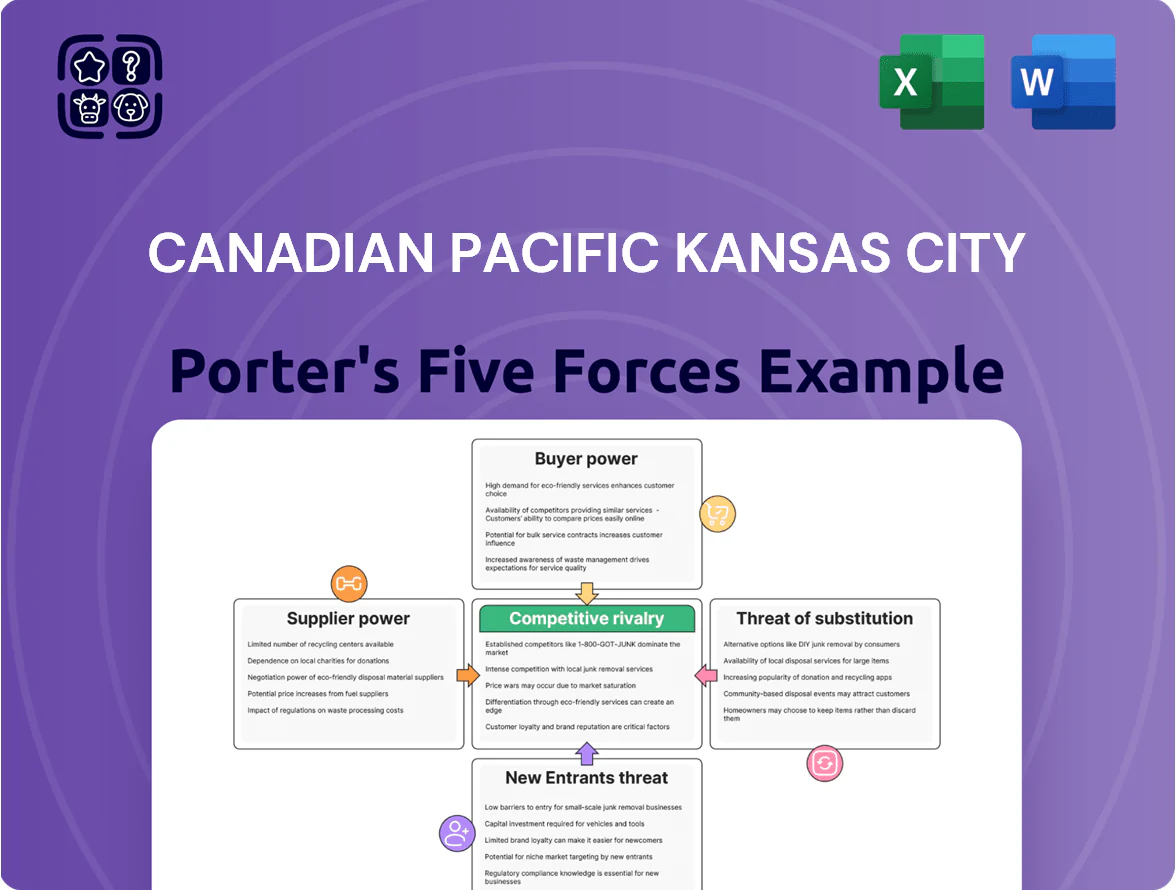

Canadian Pacific Kansas City navigates a concentrated freight rail market where high barriers to entry and strong supplier ties shape pricing power, while shippers’ bargaining clout and modal competition pressure margins.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Canadian Pacific Kansas City’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Locomotive and Railcar Manufacturers

A handful of suppliers—Wabtec (now part of Wabtec Corporation) and Progress Rail (a Caterpillar company)—dominate advanced locomotive and railcar supply for Class 1 railroads, giving them strong bargaining power over CPKC. Their engines and PTC-compatible systems directly affect fuel efficiency and compliance with Canada/US greenhouse gas rules; a modern Tier 4 locomotive can cut NOx by ~90% and save 5–15% fuel. CPKC must lock multiyear contracts and parts agreements to secure fleet modernization and minimize downtime.

Unionized Labor Force

Fuel and Energy Providers

Diesel fuel is one of CPKC’s largest operating costs—fuel accounted for about 22% of U.S. Class I railroad operating expenses in 2023—leaving CPKC a price taker in the global oil market and exposed to Brent/diesel swings. CPKC hedges fuel (reported $/gallon contracts in 2024) to cut volatility but still depends on a small set of major suppliers for massive volumes. A shift to hydrogen or battery locomotives would add specialized utility suppliers and capex, changing supplier dynamics and long-term bargaining power.

Steel and Infrastructure Material Suppliers

Steel and infrastructure material suppliers wield high bargaining power over Canadian Pacific Kansas City because maintaining a transcontinental network needs vast volumes of rail steel, ties, and ballast, and only a few global firms meet heavy‑haul specs.

Global steel price swings drove US rail steel costs up ~22% in 2023–2024, directly raising CPKC capital and maintenance outlays and compressing margins on infrastructure projects.

- Few qualified suppliers → limited alternatives

- 2023–24 steel price rise ~22% → higher CapEx

- Specialized specs increase switching costs

Proprietary Technology and Software Vendors

Proprietary rail software for dispatching, positive train control (PTC), and logistics gives suppliers strong leverage over CPKC because switching costs are high and integrations are deeply embedded in operations.

CPKC’s push toward automation—projects announced in 2024 targeting 10–15% efficiency gains—raises dependency on niche vendors and increases supplier bargaining power.

- High switching costs: multi-year integrations

- Specialized PTC vendors control safety-critical tech

- Automation plans (2024) raise vendor reliance

Suppliers Squeeze Margins: Labor, Fuel, Steel & Vendors Drive Costs Up

Suppliers hold high bargaining power: a few locomotive/vendors (Wabtec, Progress Rail), steel producers, fuel majors, and niche PTC/software firms create limited alternatives, high switching costs, and material price exposure; labor unions add leverage—labor/fringe costs $2.9B in 2024. Fuel ~22% of Opex (2023); steel costs rose ~22% in 2023–24; automation plans (2024) increase vendor reliance.

| Supplier | Key stat |

|---|---|

| Labor | $2.9B labor/fringe (2024) |

| Fuel | ~22% of Opex (2023) |

| Steel | +22% price rise (2023–24) |

| Vendors | Wabtec, Progress Rail dominate |

What is included in the product

Tailored exclusively for Canadian Pacific Kansas City, this Porter's Five Forces analysis uncovers key drivers of competition, customer and supplier influence, entry barriers, substitutes, and emerging threats shaping its pricing power and profitability.

Clear, one-sheet Porter’s Five Forces for Canadian Pacific Kansas City—instantly spot competitive pressures and relief points for routing, pricing, and network integration decisions.

Customers Bargaining Power

Concentration of High-Volume Shippers

Major grain, automotive, and energy shippers make up roughly 45–55% of Canadian Pacific Kansas City’s (CPKC) freight revenue, giving them strong leverage to demand lower volume rates and tight service-level clauses; for example, a single grain exporter can represent 3–6% of annual carloads.

The loss of one large contract to CN or to trucking/ensemble intermodal could cut operating revenue materially—each 1% drop in volumes roughly equals a $35–50 million revenue hit based on CPKC’s 2024 revenue of ~$5.2 billion.

Availability of Alternative Transportation Modes

Customers shipping high-value or time-sensitive goods can often switch to trucking if CPKC rail rates rise; in Canada and the US trucking carries about 70% of freight tonnage by value, pressuring rail pricing.

For bulk commodities like grain or coal, barge and maritime options handle up to 30% of grain exports in the Prairies and Great Lakes regions, creating regional substitute threats.

This substitute availability forces CPKC to keep rates competitive while selling its single-line efficiency—CPKC claims up to 20% faster transit times across its merged network—so shippers weigh cost vs reliability.

Captive Shipper Regulatory Environment

In many regions CPKC (Canadian Pacific Kansas City) is the sole rail provider, leaving shippers captive with little direct bargaining power; captive traffic made up about 35% of North American carloads in 2024 per AAR-style breakdowns. Regulatory bodies—the Canadian Transportation Agency and the U.S. Surface Transportation Board—routinely review rates and service complaints, imposing remedies and service metrics. This oversight effectively stands in for customer power, capping CPKC’s pricing freedom and reducing revenue levers during 2024–2025 rate cycles. Recent STB enforcement actions and CTA interventions show regulators can force service agreements and rate adjustments within months.

Single-Line Service Value Proposition

CPKC’s single-line North American route—launched after the 2023 merger—cuts average cross-border rail transit times by about 10–20% versus interline moves, lowering border friction and switching costs for shippers.

That exclusivity weakens customer bargaining power for firms needing seamless Canada‑US‑Mexico service; CPKC captured ~11% of North American freight tonnage in 2024 on key corridors, letting it command premiums.

Shippers pay higher rates for faster, reliable transit: CPKC reported a 6% yield uplift in 2024, showing price tolerance for integrated network benefits.

- Only single-line Canada–US–Mexico network

- Transit time cut ~10–20% vs interline

- ~11% corridor tonnage share (2024)

- 6% yield uplift reported in 2024

Customer Sensitivity to Economic Cycles

Many of CPKC’s customers are in cyclical sectors—construction, mining, and manufacturing—where freight volumes fell by about 12% in 2023 US manufacturing downturns and capex cuts, making shippers highly price-sensitive on transport costs.

In recessions shippers push for lower rates; CPKC needs targeted price concessions to retain volume while protecting operating ratio (CPKC’s reported 2024 operating ratio target ~57–59%), or margin erosion follows.

- Key customers cyclical: construction, commodities, manufacturing

- Freight volume risk: ~-12% in weak 2023 demand

- CPKC operating ratio target ~57–59%—price cuts hurt margins

CPKC’s single-line boosts corridor share 11% and cuts transit 10–20%, but regs cap pricing

Large grain/auto/energy shippers (45–55% revenue) hold strong leverage; losing 1% volume ≈ $35–50M of 2024 revenue (~$5.2B). Trucking moves ~70% tonnage-by-value; barge handles up to 30% regional grain exports. CPKC’s single-line gave ~10–20% faster transit and ~11% corridor tonnage share in 2024, with a 6% yield uplift; regulators (STB/CTA) limit pricing power.

| Metric | 2024 value |

|---|---|

| Revenue | $5.2B |

| Shipper concentration | 45–55% |

| Trucking share by value | ~70% |

| Transit time cut | 10–20% |

| Corridor share | ~11% |

| Yield uplift | 6% |

Full Version Awaits

Canadian Pacific Kansas City Porter's Five Forces Analysis

This preview shows the exact Canadian Pacific Kansas City Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the same professionally written, fully formatted file ready for download and use the moment you buy. You're looking at the actual deliverable; once payment is complete you'll get instant access to this precise document. No mockups or samples—what you see is what you get.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Don't Miss the Bigger Picture

Canadian Pacific Kansas City navigates a concentrated freight rail market where high barriers to entry and strong supplier ties shape pricing power, while shippers’ bargaining clout and modal competition pressure margins.

This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Canadian Pacific Kansas City’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Specialized Locomotive and Railcar Manufacturers

A handful of suppliers—Wabtec (now part of Wabtec Corporation) and Progress Rail (a Caterpillar company)—dominate advanced locomotive and railcar supply for Class 1 railroads, giving them strong bargaining power over CPKC. Their engines and PTC-compatible systems directly affect fuel efficiency and compliance with Canada/US greenhouse gas rules; a modern Tier 4 locomotive can cut NOx by ~90% and save 5–15% fuel. CPKC must lock multiyear contracts and parts agreements to secure fleet modernization and minimize downtime.

Unionized Labor Force

Fuel and Energy Providers

Diesel fuel is one of CPKC’s largest operating costs—fuel accounted for about 22% of U.S. Class I railroad operating expenses in 2023—leaving CPKC a price taker in the global oil market and exposed to Brent/diesel swings. CPKC hedges fuel (reported $/gallon contracts in 2024) to cut volatility but still depends on a small set of major suppliers for massive volumes. A shift to hydrogen or battery locomotives would add specialized utility suppliers and capex, changing supplier dynamics and long-term bargaining power.

Steel and Infrastructure Material Suppliers

Steel and infrastructure material suppliers wield high bargaining power over Canadian Pacific Kansas City because maintaining a transcontinental network needs vast volumes of rail steel, ties, and ballast, and only a few global firms meet heavy‑haul specs.

Global steel price swings drove US rail steel costs up ~22% in 2023–2024, directly raising CPKC capital and maintenance outlays and compressing margins on infrastructure projects.

- Few qualified suppliers → limited alternatives

- 2023–24 steel price rise ~22% → higher CapEx

- Specialized specs increase switching costs

Proprietary Technology and Software Vendors

Proprietary rail software for dispatching, positive train control (PTC), and logistics gives suppliers strong leverage over CPKC because switching costs are high and integrations are deeply embedded in operations.

CPKC’s push toward automation—projects announced in 2024 targeting 10–15% efficiency gains—raises dependency on niche vendors and increases supplier bargaining power.

- High switching costs: multi-year integrations

- Specialized PTC vendors control safety-critical tech

- Automation plans (2024) raise vendor reliance

Suppliers Squeeze Margins: Labor, Fuel, Steel & Vendors Drive Costs Up

Suppliers hold high bargaining power: a few locomotive/vendors (Wabtec, Progress Rail), steel producers, fuel majors, and niche PTC/software firms create limited alternatives, high switching costs, and material price exposure; labor unions add leverage—labor/fringe costs $2.9B in 2024. Fuel ~22% of Opex (2023); steel costs rose ~22% in 2023–24; automation plans (2024) increase vendor reliance.

| Supplier | Key stat |

|---|---|

| Labor | $2.9B labor/fringe (2024) |

| Fuel | ~22% of Opex (2023) |

| Steel | +22% price rise (2023–24) |

| Vendors | Wabtec, Progress Rail dominate |

What is included in the product

Tailored exclusively for Canadian Pacific Kansas City, this Porter's Five Forces analysis uncovers key drivers of competition, customer and supplier influence, entry barriers, substitutes, and emerging threats shaping its pricing power and profitability.

Clear, one-sheet Porter’s Five Forces for Canadian Pacific Kansas City—instantly spot competitive pressures and relief points for routing, pricing, and network integration decisions.

Customers Bargaining Power

Concentration of High-Volume Shippers

Major grain, automotive, and energy shippers make up roughly 45–55% of Canadian Pacific Kansas City’s (CPKC) freight revenue, giving them strong leverage to demand lower volume rates and tight service-level clauses; for example, a single grain exporter can represent 3–6% of annual carloads.

The loss of one large contract to CN or to trucking/ensemble intermodal could cut operating revenue materially—each 1% drop in volumes roughly equals a $35–50 million revenue hit based on CPKC’s 2024 revenue of ~$5.2 billion.

Availability of Alternative Transportation Modes

Customers shipping high-value or time-sensitive goods can often switch to trucking if CPKC rail rates rise; in Canada and the US trucking carries about 70% of freight tonnage by value, pressuring rail pricing.

For bulk commodities like grain or coal, barge and maritime options handle up to 30% of grain exports in the Prairies and Great Lakes regions, creating regional substitute threats.

This substitute availability forces CPKC to keep rates competitive while selling its single-line efficiency—CPKC claims up to 20% faster transit times across its merged network—so shippers weigh cost vs reliability.

Captive Shipper Regulatory Environment

In many regions CPKC (Canadian Pacific Kansas City) is the sole rail provider, leaving shippers captive with little direct bargaining power; captive traffic made up about 35% of North American carloads in 2024 per AAR-style breakdowns. Regulatory bodies—the Canadian Transportation Agency and the U.S. Surface Transportation Board—routinely review rates and service complaints, imposing remedies and service metrics. This oversight effectively stands in for customer power, capping CPKC’s pricing freedom and reducing revenue levers during 2024–2025 rate cycles. Recent STB enforcement actions and CTA interventions show regulators can force service agreements and rate adjustments within months.

Single-Line Service Value Proposition

CPKC’s single-line North American route—launched after the 2023 merger—cuts average cross-border rail transit times by about 10–20% versus interline moves, lowering border friction and switching costs for shippers.

That exclusivity weakens customer bargaining power for firms needing seamless Canada‑US‑Mexico service; CPKC captured ~11% of North American freight tonnage in 2024 on key corridors, letting it command premiums.

Shippers pay higher rates for faster, reliable transit: CPKC reported a 6% yield uplift in 2024, showing price tolerance for integrated network benefits.

- Only single-line Canada–US–Mexico network

- Transit time cut ~10–20% vs interline

- ~11% corridor tonnage share (2024)

- 6% yield uplift reported in 2024

Customer Sensitivity to Economic Cycles

Many of CPKC’s customers are in cyclical sectors—construction, mining, and manufacturing—where freight volumes fell by about 12% in 2023 US manufacturing downturns and capex cuts, making shippers highly price-sensitive on transport costs.

In recessions shippers push for lower rates; CPKC needs targeted price concessions to retain volume while protecting operating ratio (CPKC’s reported 2024 operating ratio target ~57–59%), or margin erosion follows.

- Key customers cyclical: construction, commodities, manufacturing

- Freight volume risk: ~-12% in weak 2023 demand

- CPKC operating ratio target ~57–59%—price cuts hurt margins

CPKC’s single-line boosts corridor share 11% and cuts transit 10–20%, but regs cap pricing

Large grain/auto/energy shippers (45–55% revenue) hold strong leverage; losing 1% volume ≈ $35–50M of 2024 revenue (~$5.2B). Trucking moves ~70% tonnage-by-value; barge handles up to 30% regional grain exports. CPKC’s single-line gave ~10–20% faster transit and ~11% corridor tonnage share in 2024, with a 6% yield uplift; regulators (STB/CTA) limit pricing power.

| Metric | 2024 value |

|---|---|

| Revenue | $5.2B |

| Shipper concentration | 45–55% |

| Trucking share by value | ~70% |

| Transit time cut | 10–20% |

| Corridor share | ~11% |

| Yield uplift | 6% |

Full Version Awaits

Canadian Pacific Kansas City Porter's Five Forces Analysis

This preview shows the exact Canadian Pacific Kansas City Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is the same professionally written, fully formatted file ready for download and use the moment you buy. You're looking at the actual deliverable; once payment is complete you'll get instant access to this precise document. No mockups or samples—what you see is what you get.