Canadian Pacific Kansas City PESTLE Analysis

Your Competitive Advantage Starts with This Report

Gain a strategic advantage with our targeted PESTLE Analysis of Canadian Pacific Kansas City—uncover how political shifts, economic cycles, and environmental regulations will shape rail logistics and profitability; buy the full report now for actionable insights, editable formats, and the intelligence you need to inform investment, strategy, or competitive planning.

Political factors

USMCA Trade Framework Stability

The USMCA provides CPKC with a stable trilateral trade framework covering roughly US$1.6 trillion in annual goods trade among the three countries, underpinning its 20,000-mile single-line network; by end-2025 political stability on tariffs and cross-border flow remains critical as 15–20% disruption in border throughput could cut intermodal volumes materially; any protectionist move in the US, Canada, or Mexico risks higher dwell times and revenue pressure for CPKC.

Mexican Infrastructure and Energy Policy

The Mexican government’s 2024 fiscal plan allocates over MXN 250 billion to strategic infrastructure, including projects that can both complement and compete with private rail investment, affecting CPKC freight routings and capacity utilization.

Decisions on the Interoceanic Corridor and state-run passenger rail—budgeted at roughly MXN 150–200 billion across 2023–2025—shift track priority and scheduling, potentially reducing CPKC’s access or increasing transit times on shared corridors.

Securing long-term concessions and permits requires active engagement with federal and state authorities; CPKC must manage regulatory risk as Mexico advances infrastructure projects that could reallocate land use and right-of-way, impacting asset valuation and ROI.

Canadian Labor Relations Intervention

The Canadian federal government has increasingly intervened in rail labor disputes to avert GDP shocks; in 2024 intervention averted estimated supply-chain losses of C$1.2–1.5 billion weekly. As of late 2025 the looming threat of strikes remains a recurring political risk for CPKC, prompting mandatory mediation to protect freight flows that move ~70% of Western Canada bulk exports. Political pressure from energy, agriculture, and manufacturing sectors often leads Ottawa to impose binding arbitration during stalemates.

Cross-Border Customs Harmonization

Political cooperation between US CBP and Mexico SAT underpins CPKC’s speed proposition; coordinated inspections and data-sharing have reduced average border dwell time—US-Mexico rail border crossings saw a 12% decrease in dwell time in 2024 where pilot harmonization was applied.

Digitization mandates like the USMCA-driven Trusted Trader expansions and Mexico’s Ventanilla Única push aim to standardize manifests; governments cite trade facilitation targets to boost North American exports, which totaled over US$1.9 trillion in 2024.

Political delays over harmonized security protocols can create chokepoints at Laredo and Eagle Pass; a 2023 CBP report flagged that protocol disputes contributed to a 15% spike in rail congestion days at Laredo in peak months.

- CBP–SAT cooperation reduced pilot border dwell times by ~12% (2024)

- North American exports exceeded US$1.9 trillion (2024)

- Protocol disputes linked to a 15% rise in Laredo rail congestion days (2023)

Geopolitical Nearshoring Incentives

- CHIPS Act ~$280bn; Canada ITC expansions

- Projected 5–7% rail volume lift in key lanes

- Opportunity: capture nearshore supply chains in autos, semiconductors, EVs

Stable USMCA backs CPKC network amid border risks, MX spend and tech-driven lane growth

Stable USMCA rules support CPKC’s 20,000‑mile network amid risks: 15–20% border disruption could cut intermodal volumes; MX infrastructure spending (≈MXN 250bn) and Interoceanic Corridor budgets (MXN 150–200bn) may reallocate track priority; 2024 CBP–SAT cooperation cut dwell times ~12% while 2023 protocol disputes raised Laredo congestion days 15%; CHIPS Act ~$280bn and Canada ITC drive 5–7% lane volume CAGR.

| Metric | Value |

|---|---|

| Border dwell reduction (pilot) | ~12% (2024) |

| Laredo congestion spike | +15% days (2023) |

| MX infrastructure spend | ≈MXN 250bn (2024) |

| Interoceanic Corridor | MXN 150–200bn (2023–25) |

| CHIPS Act | ~$280bn (since 2022) |

| Projected rail volume lift | 5–7% CAGR (to 2025) |

What is included in the product

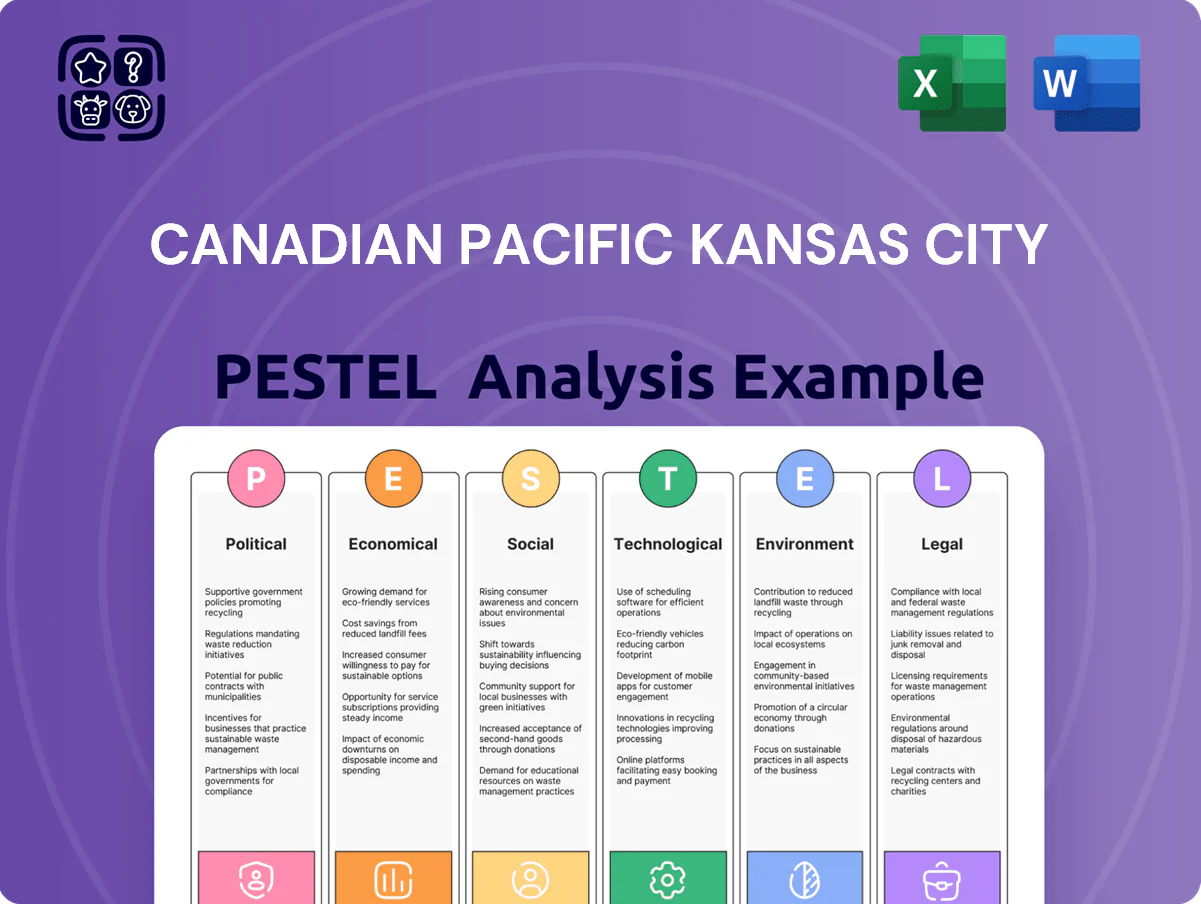

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Canadian Pacific Kansas City, using current regional data and industry trends to identify strategic risks and opportunities.

A concise, visually segmented PESTLE summary for Canadian Pacific Kansas City that can be dropped into presentations or shared across teams to quickly align on regulatory, economic, and operational risks and opportunities.

Economic factors

Mexican Manufacturing and Nearshoring Boom

Nearshoring has propelled Mexico into a manufacturing hub—auto and electronics output grew 6.8% y/y in 2024, with auto exports reaching $74.5B in 2024. CPKC, as the sole single-line rail between Mexican factories and US/Canadian markets, captures higher-margin intermodal and automotive flows. Management projects intermodal and auto volumes to grow mid-to-high single digits through 2025, supporting margin expansion and stronger freight yields.

Currency Exchange Rate Volatility

Operating across Canada, the US and Mexico exposes CPKC to CAD–USD–MXN swings; in 2024 USD appreciated ~6% vs MXN and ~5% vs CAD, amplifying translation and transaction risk for cross-border freight revenues.

Revenue earned in MXN or CAD must offset USD-denominated debt and capex—CPKC held about US$4.8bn of long-term debt at end-2024—creating a complex hedging need across FX forwards and natural hedges.

Sharp MXN or CAD depreciation can compress reported net income and cash flow; economic instability in any currency complicates budgeting, capital allocation and dividend planning for the railroad.

Commodity Price Fluctuations

CPKC earns a large share of revenue from bulk commodities—grain, potash, and energy—handling ~65% of Canadian grain exports and moving ~30% of North American crude-by-rail volumes; 2024 grain shipments fell ~7% YoY amid lower export prices, directly reducing carloads and revenue. Global commodity price drops and weaker construction/ag demand can quickly cut freight volumes and pressure producer cashflows, constraining rail pricing power and margins.

Inflationary Pressures on Operational Costs

Persistent inflation through 2025 raised diesel fuel prices ~15% YoY and steel pipe/rail mill product prices ~10–12% in 2024, increasing CPKC’s primary operating costs for fuel, track materials, and wages.

Fuel surcharges and contractual rate adjustments partially offset higher expenses, but rapid inflation risks margin compression if revenue per carload cannot rise equally; CPKC reported 2024 operating ratio ~65–67%.

Higher interest rates (Canada prime ~5.0%–5.25% in 2024–25) elevate cost of capital, complicating financing for CPKC’s multibillion-dollar infrastructure projects and rolling-stock renewals.

- Fuel +15% YoY (2024)

- Steel +10–12% (2024)

- Operating ratio ~65–67% (2024)

- Canada prime ~5.0–5.25% (2024–25)

Intermodal Competition with Trucking

Diesel averaged about US$3.50/gal in Canada in 2025 Q4, and driver shortages left 27% of long‑haul trucking capacity constrained, boosting trucking rates 8–12% year-over-year; CPKC must keep intermodal pricing below these effective trucking costs to retain shippers.

Highway congestion raised average truck door-to-door times by ~15% on major corridors in 2024, favoring CPKC’s faster long-distance unit trains and lowering per-ton-mile costs versus truck alternatives.

- Diesel ~US$3.50/gal (2025 Q4)

- Driver shortages constrain ~27% capacity

- Trucking rates up 8–12% YoY

- Road delays +15% travel times (2024)

Nearshoring Fuels Rail Volume & Pricing Power Amid FX, Fuel, Steel, and Grain Headwinds

Nearshoring boosts intermodal/auto volume growth mid‑high single digits through 2025; FX volatility (USD +6% vs MXN, +5% vs CAD in 2024) and US$4.8bn debt raise hedging needs; commodity/ grain declines cut carloads (~7% YoY grain 2024); fuel +15% and steel +10–12% (2024) pressure OR ~65–67%; trucking disruptions (27% capacity constrained) support rail pricing power.

| Metric | 2024/25 |

|---|---|

| USD vs MXN/CAD | +6% / +5% |

| Long‑term debt | US$4.8bn |

| Grain shipments | -7% YoY |

| Fuel | +15% YoY |

| Operating ratio | 65–67% |

| Trucking capacity constrained | 27% |

Same Document Delivered

Canadian Pacific Kansas City PESTLE Analysis

The preview shown here is the exact Canadian Pacific Kansas City PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Your Competitive Advantage Starts with This Report

Gain a strategic advantage with our targeted PESTLE Analysis of Canadian Pacific Kansas City—uncover how political shifts, economic cycles, and environmental regulations will shape rail logistics and profitability; buy the full report now for actionable insights, editable formats, and the intelligence you need to inform investment, strategy, or competitive planning.

Political factors

USMCA Trade Framework Stability

The USMCA provides CPKC with a stable trilateral trade framework covering roughly US$1.6 trillion in annual goods trade among the three countries, underpinning its 20,000-mile single-line network; by end-2025 political stability on tariffs and cross-border flow remains critical as 15–20% disruption in border throughput could cut intermodal volumes materially; any protectionist move in the US, Canada, or Mexico risks higher dwell times and revenue pressure for CPKC.

Mexican Infrastructure and Energy Policy

The Mexican government’s 2024 fiscal plan allocates over MXN 250 billion to strategic infrastructure, including projects that can both complement and compete with private rail investment, affecting CPKC freight routings and capacity utilization.

Decisions on the Interoceanic Corridor and state-run passenger rail—budgeted at roughly MXN 150–200 billion across 2023–2025—shift track priority and scheduling, potentially reducing CPKC’s access or increasing transit times on shared corridors.

Securing long-term concessions and permits requires active engagement with federal and state authorities; CPKC must manage regulatory risk as Mexico advances infrastructure projects that could reallocate land use and right-of-way, impacting asset valuation and ROI.

Canadian Labor Relations Intervention

The Canadian federal government has increasingly intervened in rail labor disputes to avert GDP shocks; in 2024 intervention averted estimated supply-chain losses of C$1.2–1.5 billion weekly. As of late 2025 the looming threat of strikes remains a recurring political risk for CPKC, prompting mandatory mediation to protect freight flows that move ~70% of Western Canada bulk exports. Political pressure from energy, agriculture, and manufacturing sectors often leads Ottawa to impose binding arbitration during stalemates.

Cross-Border Customs Harmonization

Political cooperation between US CBP and Mexico SAT underpins CPKC’s speed proposition; coordinated inspections and data-sharing have reduced average border dwell time—US-Mexico rail border crossings saw a 12% decrease in dwell time in 2024 where pilot harmonization was applied.

Digitization mandates like the USMCA-driven Trusted Trader expansions and Mexico’s Ventanilla Única push aim to standardize manifests; governments cite trade facilitation targets to boost North American exports, which totaled over US$1.9 trillion in 2024.

Political delays over harmonized security protocols can create chokepoints at Laredo and Eagle Pass; a 2023 CBP report flagged that protocol disputes contributed to a 15% spike in rail congestion days at Laredo in peak months.

- CBP–SAT cooperation reduced pilot border dwell times by ~12% (2024)

- North American exports exceeded US$1.9 trillion (2024)

- Protocol disputes linked to a 15% rise in Laredo rail congestion days (2023)

Geopolitical Nearshoring Incentives

- CHIPS Act ~$280bn; Canada ITC expansions

- Projected 5–7% rail volume lift in key lanes

- Opportunity: capture nearshore supply chains in autos, semiconductors, EVs

Stable USMCA backs CPKC network amid border risks, MX spend and tech-driven lane growth

Stable USMCA rules support CPKC’s 20,000‑mile network amid risks: 15–20% border disruption could cut intermodal volumes; MX infrastructure spending (≈MXN 250bn) and Interoceanic Corridor budgets (MXN 150–200bn) may reallocate track priority; 2024 CBP–SAT cooperation cut dwell times ~12% while 2023 protocol disputes raised Laredo congestion days 15%; CHIPS Act ~$280bn and Canada ITC drive 5–7% lane volume CAGR.

| Metric | Value |

|---|---|

| Border dwell reduction (pilot) | ~12% (2024) |

| Laredo congestion spike | +15% days (2023) |

| MX infrastructure spend | ≈MXN 250bn (2024) |

| Interoceanic Corridor | MXN 150–200bn (2023–25) |

| CHIPS Act | ~$280bn (since 2022) |

| Projected rail volume lift | 5–7% CAGR (to 2025) |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal forces uniquely impact Canadian Pacific Kansas City, using current regional data and industry trends to identify strategic risks and opportunities.

A concise, visually segmented PESTLE summary for Canadian Pacific Kansas City that can be dropped into presentations or shared across teams to quickly align on regulatory, economic, and operational risks and opportunities.

Economic factors

Mexican Manufacturing and Nearshoring Boom

Nearshoring has propelled Mexico into a manufacturing hub—auto and electronics output grew 6.8% y/y in 2024, with auto exports reaching $74.5B in 2024. CPKC, as the sole single-line rail between Mexican factories and US/Canadian markets, captures higher-margin intermodal and automotive flows. Management projects intermodal and auto volumes to grow mid-to-high single digits through 2025, supporting margin expansion and stronger freight yields.

Currency Exchange Rate Volatility

Operating across Canada, the US and Mexico exposes CPKC to CAD–USD–MXN swings; in 2024 USD appreciated ~6% vs MXN and ~5% vs CAD, amplifying translation and transaction risk for cross-border freight revenues.

Revenue earned in MXN or CAD must offset USD-denominated debt and capex—CPKC held about US$4.8bn of long-term debt at end-2024—creating a complex hedging need across FX forwards and natural hedges.

Sharp MXN or CAD depreciation can compress reported net income and cash flow; economic instability in any currency complicates budgeting, capital allocation and dividend planning for the railroad.

Commodity Price Fluctuations

CPKC earns a large share of revenue from bulk commodities—grain, potash, and energy—handling ~65% of Canadian grain exports and moving ~30% of North American crude-by-rail volumes; 2024 grain shipments fell ~7% YoY amid lower export prices, directly reducing carloads and revenue. Global commodity price drops and weaker construction/ag demand can quickly cut freight volumes and pressure producer cashflows, constraining rail pricing power and margins.

Inflationary Pressures on Operational Costs

Persistent inflation through 2025 raised diesel fuel prices ~15% YoY and steel pipe/rail mill product prices ~10–12% in 2024, increasing CPKC’s primary operating costs for fuel, track materials, and wages.

Fuel surcharges and contractual rate adjustments partially offset higher expenses, but rapid inflation risks margin compression if revenue per carload cannot rise equally; CPKC reported 2024 operating ratio ~65–67%.

Higher interest rates (Canada prime ~5.0%–5.25% in 2024–25) elevate cost of capital, complicating financing for CPKC’s multibillion-dollar infrastructure projects and rolling-stock renewals.

- Fuel +15% YoY (2024)

- Steel +10–12% (2024)

- Operating ratio ~65–67% (2024)

- Canada prime ~5.0–5.25% (2024–25)

Intermodal Competition with Trucking

Diesel averaged about US$3.50/gal in Canada in 2025 Q4, and driver shortages left 27% of long‑haul trucking capacity constrained, boosting trucking rates 8–12% year-over-year; CPKC must keep intermodal pricing below these effective trucking costs to retain shippers.

Highway congestion raised average truck door-to-door times by ~15% on major corridors in 2024, favoring CPKC’s faster long-distance unit trains and lowering per-ton-mile costs versus truck alternatives.

- Diesel ~US$3.50/gal (2025 Q4)

- Driver shortages constrain ~27% capacity

- Trucking rates up 8–12% YoY

- Road delays +15% travel times (2024)

Nearshoring Fuels Rail Volume & Pricing Power Amid FX, Fuel, Steel, and Grain Headwinds

Nearshoring boosts intermodal/auto volume growth mid‑high single digits through 2025; FX volatility (USD +6% vs MXN, +5% vs CAD in 2024) and US$4.8bn debt raise hedging needs; commodity/ grain declines cut carloads (~7% YoY grain 2024); fuel +15% and steel +10–12% (2024) pressure OR ~65–67%; trucking disruptions (27% capacity constrained) support rail pricing power.

| Metric | 2024/25 |

|---|---|

| USD vs MXN/CAD | +6% / +5% |

| Long‑term debt | US$4.8bn |

| Grain shipments | -7% YoY |

| Fuel | +15% YoY |

| Operating ratio | 65–67% |

| Trucking capacity constrained | 27% |

Same Document Delivered

Canadian Pacific Kansas City PESTLE Analysis

The preview shown here is the exact Canadian Pacific Kansas City PESTLE Analysis document you’ll receive after purchase—fully formatted, professionally structured, and ready to use with no placeholders or surprises.