CP Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

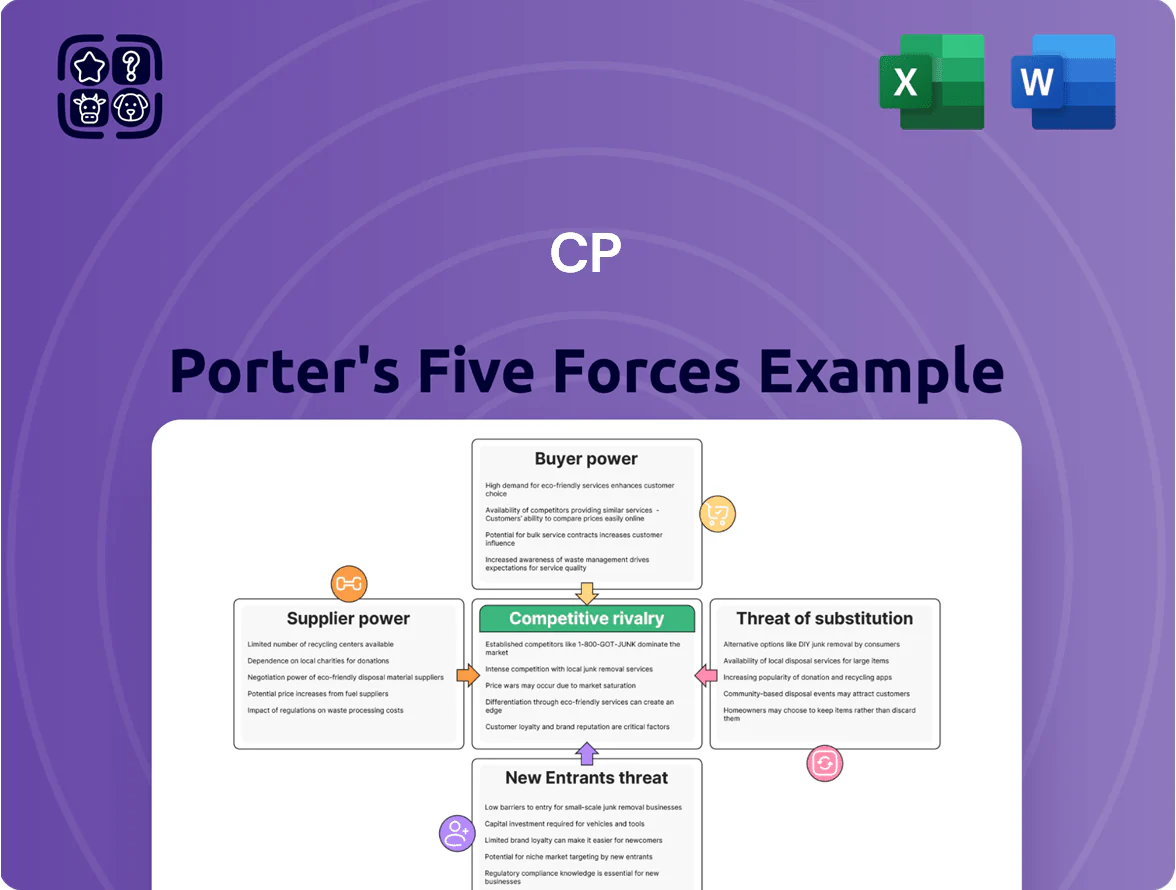

CP’s Porter’s Five Forces snapshot highlights supplier leverage, buyer bargaining, competitive rivalry, substitute threats, and entry barriers—briefly showing where CP stands in its market and which pressures matter most.

Suppliers Bargaining Power

Limited Number of Locomotive Manufacturers

The market for high-performance locomotives is concentrated among a few suppliers—Wabtec (now part of Wabtec Corporation) and Progress Rail (a Caterpillar company)—which restricts CPKC’s bargaining on price and tech; these two firms held roughly 60–70% of North American locomotive production capacity in 2024. These vendors supply specialized cross-border equipment, giving them leverage during multi-year procurement cycles and warranty negotiations. As CPKC targets fuel-efficient and hydrogen-ready engines by late 2025, dependency on these manufacturers remains high, raising capex and lead-time risks.

Labor Union Influence and Collective Bargaining

A large portion of CPKC’s workforce is unionized, giving labor a strong supplier role via collective agreements—about 70% of operations staff were union members in 2024, per company filings.

Strikes can freeze the single-line network, so CPKC must offer competitive wages; 2024 labor costs rose ~6% after bargaining, showing negotiation leverage.

By 2025, integrating Canadian, US, and Mexican labor pools adds complexity to cost and reliability management, with cross-border contracts and differing regulations driving variability in wage inflation and service risk.

Volatility in Energy and Fuel Supply

Fuel is one of CPKC’s largest operating costs—diesel accounted for roughly 12–15% of operating expenses in 2024—so suppliers and global oil markets hold strong bargaining power despite fuel surcharges that recovered ~90% of price swings in 2024; refinery constraints and Brent crude volatility (±25% in 2024) keep price exposure material. CPKC is shifting toward battery, hydrogen, and biofuel pilots, but diesel remained the primary energy source in 2025, keeping supplier leverage intact.

Specialized Infrastructure and Maintenance Material Providers

Specialized suppliers of steel rails, ties, and ballast have strong leverage over CPKC because few North American producers meet volume and spec needs; global rail steel capacity tightened in 2024, pushing rail prices up about 12% year-over-year.

High demand from infrastructure and energy projects raised lead times to 6–9 months in 2024, forcing CPKC to lock multiyear contracts and strategic inventory to protect safety and expansion schedules.

- Limited supplier pool raises price risk

- Rail prices +12% in 2024

- Lead times 6–9 months

- Multiyear contracts and inventory critical

Technological and Software Service Dependencies

CPKC depends on specialized dispatch, logistics, and Positive Train Control software from a few vendors; replacement risks major disruption on its single-line network and can cost tens of millions and months of downtime.

As CPKC rolls out AI-driven logistics in 2025, vendor leverage stays high: SaaS fees, integration and custom model work can raise annual tech OPEX by an estimated 5–10% of current IT spend (~$10–20M range).

What this hides: switching also risks regulatory delays for PTC certification and potential service interruptions that impact revenue per carload.

- Few specialist vendors = high switching cost

- PTC regulatory ties increase supplier leverage

- AI roll-out 2025 raises OPEX ~5–10% (~$10–20M)

High supplier power: concentrated OEMs, volatile diesel, long lead times, elevated switching risk

Supplier power is high: a few locomotive makers (Wabtec, Progress Rail) held ~60–70% capacity in 2024, diesel was 12–15% of OPEX with Brent ±25% volatility, rail steel prices +12% y/y, lead times 6–9 months, and ~70% unionized labor; multiyear contracts, inventory, and tech vendor dependence (PTC/AI) keep switching costs and capex/time risk elevated.

| Metric | 2024–25 |

|---|---|

| Locomotive share | 60–70% |

| Diesel OPEX | 12–15% |

| Brent vol | ±25% |

| Rail price change | +12% |

| Lead times | 6–9 mo |

| Unionized staff | ~70% |

What is included in the product

Tailored Five Forces analysis for CP that uncovers competitive drivers, supplier and buyer power, substitute threats, and barriers to entry, identifying disruptive risks and strategic levers to protect market share; delivered in fully editable Word format for easy integration into investor decks, business plans, or internal strategy work.

Clear, one-sheet Porter’s Five Forces summary that quantifies competitive pressure and speeds strategic decisions for investors and managers.

Customers Bargaining Power

Concentration of Bulk Commodity Shippers

Intermodal Price Sensitivity and Competition

Intermodal customers—retail giants and 3PLs—have strong bargaining power because they can shift to trucking for short hauls; US surface freight rate spreads show trucking under 500 miles often cheaper by 10–25% in 2024.

CPKC must keep intermodal rates competitive and on-time performance high—targeting <90% on-time intermodal moves—to retain these cost- and time-sensitive shippers.

Through 2025 CPKC leverages the efficient Canada–US–Mexico corridor (freight volumes up ~6% YoY in 2024) to defend pricing power and win lane share.

Captive Shipper Dynamics

Certain industrial customers sit on lines served only by Canadian Pacific Kansas City (CPKC), leaving them effectively captive and with low bargaining power; roughly 12–15% of North American carloads originate/terminate at such single-carrier locations, concentrating pricing leverage.

These shippers face CPKC standard tariffs, but Canadian and US regulators (e.g., Canadian Transportation Agency, STB) cap abusive fares and handled 18 tariff complaints against Class I rails in 2023–2024, limiting monopoly pricing.

CPKC must weigh short-term revenue from captive shippers—which can yield 5–12% higher yield per carload versus competitive lanes—against regulatory scrutiny and the long-term risk of customer relocation or modal shift to trucks if rates rise.

Availability of Alternative Transportation Corridors

Customers moving freight between major hubs can shift to Class I rivals like CN or Union Pacific or to maritime routes if CPKC service slips or rates climb, keeping pricing constrained.

Ability to divert traffic—CPKC saw interline exposure of ~28% in 2024—means single-line pricing power is limited across corridors.

By 2025 CPKC emphasizes single-line reliability to retain traffic; on-time initiatives target a >90% terminal dwell reduction to deter diversions.

- Direct rivals: CN, Union Pacific

- Interline exposure ~28% (2024)

- 2025 goal: >90% reduce dwell

Impact of Economic Cycles on Shipping Demand

During downturns freight demand falls—shippers cut volumes and CPKC faces pressure on rates; North American intermodal volumes slid ~7% in 2023 and lingered unevenly into 2024, boosting shipper leverage.

In strong-growth phases with port and rail congestion, CPKC gains price power as capacity tightens; 2024 US container dwell times rose 12% at peak ports, lifting rail premiums.

In 2025 fluctuating consumer demand keeps bargaining power fluid: retail, energy and bulk segments show varied elasticity, so contract length and spot exposure determine shipper influence.

- Downturns: shippers gain; volumes down ~7% (2023 baseline).

- Congestion: CPKC gains; dwell times +12% (2024 peak).

- 2025: segment-specific elasticity; contract term matters.

CPKC: Strong corridor share, captive base vs. shippers' leverage; volumes up, on-time push

| Metric | 2023–24 | 2024 | 2025 target |

|---|---|---|---|

| Bulk revenue share | — | 30–45% | — |

| Corridor share | — | ≈60% | — |

| Interline exposure | — | 28% | — |

| Ports/volumes | — | +6% YoY | — |

| On-time goal | — | — | >90% |

Preview Before You Purchase

CP Porter's Five Forces Analysis

This preview shows the exact CP Porter's Five Forces analysis you'll receive after purchase—fully formatted, complete, and ready for immediate download with no placeholders or mockups.

You're viewing the final, professionally written document; once you buy, the same file will be available instantly for use in reports, presentations, or strategic planning.

No samples or excerpts—what you see here is precisely the deliverable, complete and ready for application in your decision-making.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Go Beyond the Preview—Access the Full Strategic Report

CP’s Porter’s Five Forces snapshot highlights supplier leverage, buyer bargaining, competitive rivalry, substitute threats, and entry barriers—briefly showing where CP stands in its market and which pressures matter most.

Suppliers Bargaining Power

Limited Number of Locomotive Manufacturers

The market for high-performance locomotives is concentrated among a few suppliers—Wabtec (now part of Wabtec Corporation) and Progress Rail (a Caterpillar company)—which restricts CPKC’s bargaining on price and tech; these two firms held roughly 60–70% of North American locomotive production capacity in 2024. These vendors supply specialized cross-border equipment, giving them leverage during multi-year procurement cycles and warranty negotiations. As CPKC targets fuel-efficient and hydrogen-ready engines by late 2025, dependency on these manufacturers remains high, raising capex and lead-time risks.

Labor Union Influence and Collective Bargaining

A large portion of CPKC’s workforce is unionized, giving labor a strong supplier role via collective agreements—about 70% of operations staff were union members in 2024, per company filings.

Strikes can freeze the single-line network, so CPKC must offer competitive wages; 2024 labor costs rose ~6% after bargaining, showing negotiation leverage.

By 2025, integrating Canadian, US, and Mexican labor pools adds complexity to cost and reliability management, with cross-border contracts and differing regulations driving variability in wage inflation and service risk.

Volatility in Energy and Fuel Supply

Fuel is one of CPKC’s largest operating costs—diesel accounted for roughly 12–15% of operating expenses in 2024—so suppliers and global oil markets hold strong bargaining power despite fuel surcharges that recovered ~90% of price swings in 2024; refinery constraints and Brent crude volatility (±25% in 2024) keep price exposure material. CPKC is shifting toward battery, hydrogen, and biofuel pilots, but diesel remained the primary energy source in 2025, keeping supplier leverage intact.

Specialized Infrastructure and Maintenance Material Providers

Specialized suppliers of steel rails, ties, and ballast have strong leverage over CPKC because few North American producers meet volume and spec needs; global rail steel capacity tightened in 2024, pushing rail prices up about 12% year-over-year.

High demand from infrastructure and energy projects raised lead times to 6–9 months in 2024, forcing CPKC to lock multiyear contracts and strategic inventory to protect safety and expansion schedules.

- Limited supplier pool raises price risk

- Rail prices +12% in 2024

- Lead times 6–9 months

- Multiyear contracts and inventory critical

Technological and Software Service Dependencies

CPKC depends on specialized dispatch, logistics, and Positive Train Control software from a few vendors; replacement risks major disruption on its single-line network and can cost tens of millions and months of downtime.

As CPKC rolls out AI-driven logistics in 2025, vendor leverage stays high: SaaS fees, integration and custom model work can raise annual tech OPEX by an estimated 5–10% of current IT spend (~$10–20M range).

What this hides: switching also risks regulatory delays for PTC certification and potential service interruptions that impact revenue per carload.

- Few specialist vendors = high switching cost

- PTC regulatory ties increase supplier leverage

- AI roll-out 2025 raises OPEX ~5–10% (~$10–20M)

High supplier power: concentrated OEMs, volatile diesel, long lead times, elevated switching risk

Supplier power is high: a few locomotive makers (Wabtec, Progress Rail) held ~60–70% capacity in 2024, diesel was 12–15% of OPEX with Brent ±25% volatility, rail steel prices +12% y/y, lead times 6–9 months, and ~70% unionized labor; multiyear contracts, inventory, and tech vendor dependence (PTC/AI) keep switching costs and capex/time risk elevated.

| Metric | 2024–25 |

|---|---|

| Locomotive share | 60–70% |

| Diesel OPEX | 12–15% |

| Brent vol | ±25% |

| Rail price change | +12% |

| Lead times | 6–9 mo |

| Unionized staff | ~70% |

What is included in the product

Tailored Five Forces analysis for CP that uncovers competitive drivers, supplier and buyer power, substitute threats, and barriers to entry, identifying disruptive risks and strategic levers to protect market share; delivered in fully editable Word format for easy integration into investor decks, business plans, or internal strategy work.

Clear, one-sheet Porter’s Five Forces summary that quantifies competitive pressure and speeds strategic decisions for investors and managers.

Customers Bargaining Power

Concentration of Bulk Commodity Shippers

Intermodal Price Sensitivity and Competition

Intermodal customers—retail giants and 3PLs—have strong bargaining power because they can shift to trucking for short hauls; US surface freight rate spreads show trucking under 500 miles often cheaper by 10–25% in 2024.

CPKC must keep intermodal rates competitive and on-time performance high—targeting <90% on-time intermodal moves—to retain these cost- and time-sensitive shippers.

Through 2025 CPKC leverages the efficient Canada–US–Mexico corridor (freight volumes up ~6% YoY in 2024) to defend pricing power and win lane share.

Captive Shipper Dynamics

Certain industrial customers sit on lines served only by Canadian Pacific Kansas City (CPKC), leaving them effectively captive and with low bargaining power; roughly 12–15% of North American carloads originate/terminate at such single-carrier locations, concentrating pricing leverage.

These shippers face CPKC standard tariffs, but Canadian and US regulators (e.g., Canadian Transportation Agency, STB) cap abusive fares and handled 18 tariff complaints against Class I rails in 2023–2024, limiting monopoly pricing.

CPKC must weigh short-term revenue from captive shippers—which can yield 5–12% higher yield per carload versus competitive lanes—against regulatory scrutiny and the long-term risk of customer relocation or modal shift to trucks if rates rise.

Availability of Alternative Transportation Corridors

Customers moving freight between major hubs can shift to Class I rivals like CN or Union Pacific or to maritime routes if CPKC service slips or rates climb, keeping pricing constrained.

Ability to divert traffic—CPKC saw interline exposure of ~28% in 2024—means single-line pricing power is limited across corridors.

By 2025 CPKC emphasizes single-line reliability to retain traffic; on-time initiatives target a >90% terminal dwell reduction to deter diversions.

- Direct rivals: CN, Union Pacific

- Interline exposure ~28% (2024)

- 2025 goal: >90% reduce dwell

Impact of Economic Cycles on Shipping Demand

During downturns freight demand falls—shippers cut volumes and CPKC faces pressure on rates; North American intermodal volumes slid ~7% in 2023 and lingered unevenly into 2024, boosting shipper leverage.

In strong-growth phases with port and rail congestion, CPKC gains price power as capacity tightens; 2024 US container dwell times rose 12% at peak ports, lifting rail premiums.

In 2025 fluctuating consumer demand keeps bargaining power fluid: retail, energy and bulk segments show varied elasticity, so contract length and spot exposure determine shipper influence.

- Downturns: shippers gain; volumes down ~7% (2023 baseline).

- Congestion: CPKC gains; dwell times +12% (2024 peak).

- 2025: segment-specific elasticity; contract term matters.

CPKC: Strong corridor share, captive base vs. shippers' leverage; volumes up, on-time push

| Metric | 2023–24 | 2024 | 2025 target |

|---|---|---|---|

| Bulk revenue share | — | 30–45% | — |

| Corridor share | — | ≈60% | — |

| Interline exposure | — | 28% | — |

| Ports/volumes | — | +6% YoY | — |

| On-time goal | — | — | >90% |

Preview Before You Purchase

CP Porter's Five Forces Analysis

This preview shows the exact CP Porter's Five Forces analysis you'll receive after purchase—fully formatted, complete, and ready for immediate download with no placeholders or mockups.

You're viewing the final, professionally written document; once you buy, the same file will be available instantly for use in reports, presentations, or strategic planning.

No samples or excerpts—what you see here is precisely the deliverable, complete and ready for application in your decision-making.