Bank of Chongqing Business Model Canvas

Bank of Chongqing: Business Model Canvas—Retail, SME, Digital Strategies Unpacked

Unlock the full strategic blueprint behind Bank of Chongqing's business model—discover how targeted retail banking, SME lending, and digital channels combine to drive growth and customer loyalty.

This in-depth Business Model Canvas breaks down value propositions, key partnerships, revenue streams, and cost structure for practical benchmarking and strategic planning.

Download the complete Word/Excel canvas to get company-specific insights and ready-to-use frameworks for investors, consultants, and executives.

Partnerships

Local Government Entities

The bank holds strategic alliances with the Chongqing municipal government and district authorities to finance regional infrastructure and development projects, channeling government-backed loans—BoC reported RMB 68.7 billion in policy and local government lending in 2024—while managing fiscal deposits exceeding RMB 120 billion. These partnerships align BoC’s growth with the Chengdu-Chongqing Economic Circle, supporting coordinated urbanization and transport projects that target a 5–7% regional GDP uplift through 2025.

Interbank and Financial Institutions

Collaborations with major national banks and international institutions let Bank of Chongqing manage liquidity and join syndicated loans—China interbank market lending lines exceeded CNY 12 trillion in 2024, enabling broader access to funding.

These ties support clearing, FX services, and footprint expansion; partnerships grant access to derivatives and global market intel, aiding cross-border business as Chongqing outbound trade grew 9.8% in 2024.

Fintech and Technology Providers

Strategic cooperation with fintech and tech providers lets Bank of Chongqing modernize digital infrastructure and deploy advanced analytics; by 2024 the bank reported a 28% rise in mobile transactions year-over-year and a 15% cut in loan processing time after API-led platform upgrades with partners like iFlytek and Huawei Cloud.

Corporate Strategic Clients

The bank secures long-term ties with SOEs and major private manufacturers/logistics firms, generating repeat high-value corporate deposits and lending—about 28% of corporate loan book in 2024 (RMB figure: ~RMB 120bn of targeted clients).

These clients drive supply-chain finance and tailored cash-management products, increasing fee income and lowering NPLs through integrated operational workflows.

- 28% of corporate loans from strategic clients (2024)

- ~RMB 120bn exposure to target sectors

- Higher fee income via supply-chain finance

- Customized solutions tied to client ERP/workflow

Regulatory and Compliance Bodies

Maintaining close ties with the People’s Bank of China and the China Banking and Insurance Regulatory Commission gives Bank of Chongqing operational legitimacy and helps it adapt to capital and macro‑prudential rule changes (PBOC reserve ratio tweaks in 2024 averaged 25–50 bps; CBIRC tightened provisioning guidance in 2025).

Frequent communication reduces legal risk and speeds compliance: quarterly supervisory meetings, timely reporting of NPLs (Bank of Chongqing reported 1.32% NPL ratio in 2024) and stress‑test coordination.

- Operational legitimacy via PBOC & CBIRC

- Stay ahead of capital rule shifts (2024–25: 25–50 bps RRR moves)

- Quarterly supervisory meetings and reporting

- Leads to lower regulatory/legal risk; NPL ratio 1.32% (2024)

BoC anchors Chongqing growth: RMB policy loans, CNY12tn liquidity, fintech gains

BoC partners with Chongqing government (RMB 68.7bn policy lending, fiscal deposits >RMB 120bn in 2024), major banks/interbank lines (CNY 12tn market in 2024), fintechs (28% y/y mobile tx growth; 15% faster loan processing), SOEs/private clients (~RMB 120bn exposure; 28% of corporate loans), and regulators (NPL 1.32% in 2024; PBOC RRR moves 25–50bps 2024–25).

| Partner | Key metric (2024–25) |

|---|---|

| Chongqing govt | RMB 68.7bn policy loans; fiscal deposits >RMB 120bn |

| Interbank/national banks | CNY 12tn market liquidity |

| Fintech/tech | Mobile tx +28% YoY; loan time -15% |

| Corporate clients | ~RMB 120bn exposure; 28% corp loans |

| Regulators | NPL 1.32%; RRR moves 25–50bps |

What is included in the product

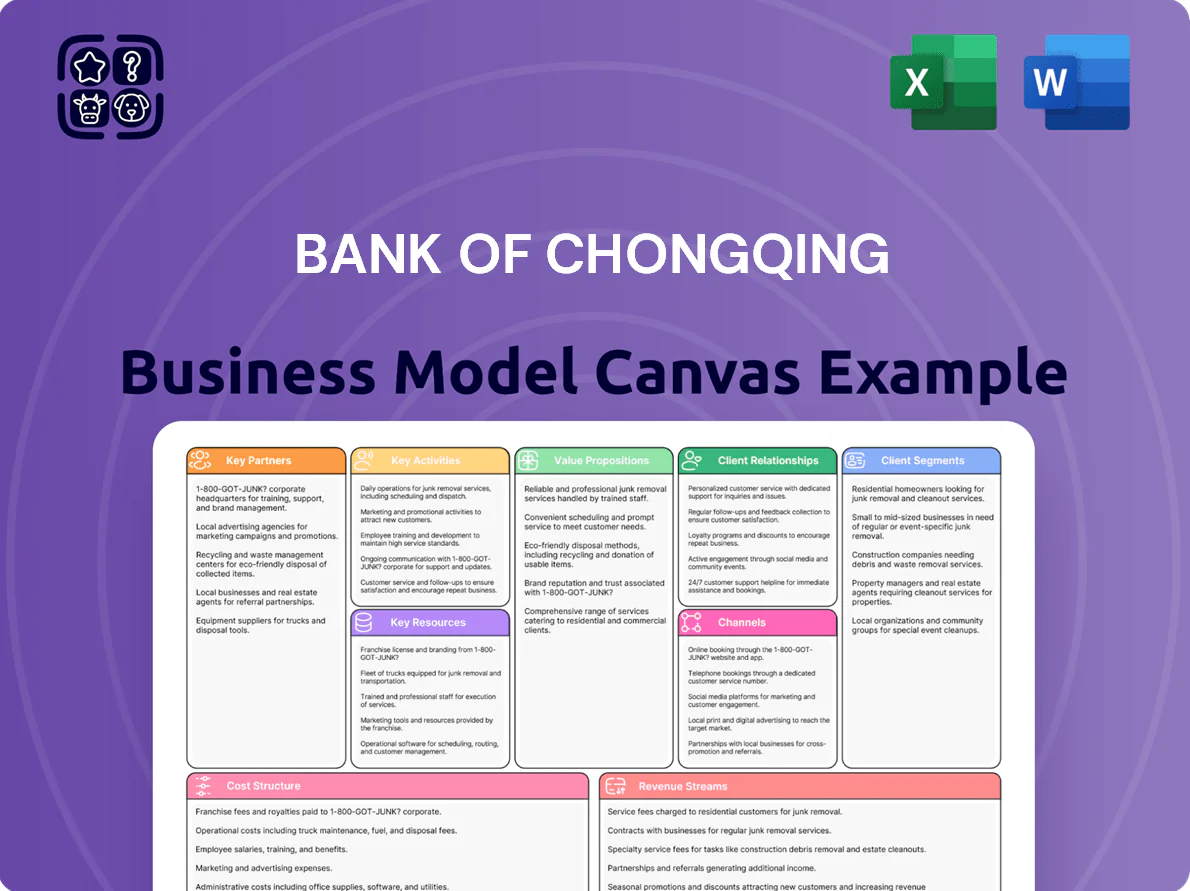

A comprehensive, pre-written Business Model Canvas for Bank of Chongqing that maps its nine BMC blocks—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, key activities, key partners, and cost structure—reflecting real-world operations, competitive advantages, SWOT-linked insights, and polished narratives ideal for presentations, investor funding discussions, and strategic decision-making.

Condenses Bank of Chongqing’s strategy into a digestible one-page Business Model Canvas, saving hours of structuring and enabling quick comparisons, team collaboration, and board-ready presentations.

Activities

Credit and Loan Management

Credit and loan management covers assessment, disbursement, and monitoring of corporate and retail loans; Bank of Chongqing reported net loans of CNY 840.3 billion as of 2024-12-31, driving ~65% of 2024 interest income.

The bank uses advanced credit models and quarterly collateral revaluations; 2024 NPL ratio stood at 1.42% and coverage ratio at 207%, protecting asset quality.

Deposit Mobilization and Management

Bank of Chongqing boosts deposits via tiered savings, high-yield time deposits, and liquidity pools for corporates; deposits rose 6.8% y/y to RMB 1.12 trillion at end-2024, providing a low-cost funding base for loans.

Marketing, branch promos, and dynamic rate ladders target retail and SME clients; management cut average deposit cost by 12 bps in 2024 to support NIMs while maintaining CASA growth.

Wealth Management and Investment Services

Designs and distributes mutual funds and insurance products targeting Chongqing’s expanding middle class—household financial assets in China rose to RMB 300 trillion in 2024, with Chongqing retail investment flows up ~9% YoY—while acting as intermediary and providing advisory services to meet client goals. This wealth-management hub generates fee income (Bank of Chongqing reported non-interest income growth of 7.2% in 2024), diversifying revenue away from lending.

Digital Transformation and IT Operations

Bank of Chongqing invests continuously in digital banking infrastructure—upgrading secure data centers, rolling out mobile apps, and embedding AI chatbots—cutting transaction costs and boosting service speed; in 2024 digital transactions rose ~28% y/y, now >45% of retail volume.

- Secure data centers: multi-site resilience, 99.99% uptime target

- Mobile apps: user-centric updates, 4.6 avg rating (2024)

- AI: automated service handles ~30% of queries

- Cost impact: digital channel cost-per-transaction down ~40% since 2021

Risk Management and Internal Control

Risk management and internal control at Bank of Chongqing center on frameworks that identify, measure, and mitigate financial, operational, and reputational risks, using quarterly stress tests and internal audits to meet CBIRC (China Banking and Insurance Regulatory Commission) standards; AML compliance covers transaction monitoring across ¥1.2 trillion in 2024 deposits.

Strong internal controls sustain investor confidence and regulatory standing, with the bank reporting a 12.6% CET1 ratio and a nonperforming loan ratio of 1.25% at end-2024.

- Quarterly stress tests and internal audits

- AML transaction monitoring across ¥1.2 trillion deposits (2024)

- CET1 ratio 12.6% (2024)

- NPL ratio 1.25% (2024)

Stable credit growth, strong deposits & digital surge—healthy capital and risk metrics

Core activities: credit origination/monitoring (net loans CNY 840.3bn, NPL 1.42%, coverage 207% at 2024-12-31), deposit gathering (deposits CNY 1.12tn, +6.8% y/y; deposit cost -12bps in 2024), wealth products (non-interest income +7.2% in 2024), digital ops (digital transactions +28% y/y; >45% retail volume), and risk/regs (CET1 12.6%, AML monitoring ¥1.2tn).

| Metric | 2024 value |

|---|---|

| Net loans | CNY 840.3bn |

| Deposits | CNY 1.12tn |

| NPL ratio | 1.42% |

| Coverage ratio | 207% |

| CET1 ratio | 12.6% |

| Non-interest income growth | +7.2% |

| Digital transactions growth | +28% y/y |

| AML monitored deposits | ¥1.2tn |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the actual Bank of Chongqing Business Model Canvas you’ll receive—no mockup or sample. Upon purchase, you’ll get this same, complete file ready for editing, presenting, and sharing. The preview matches the final deliverable in content and format, so there are no surprises. Instant download in editable format is provided after checkout.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Bank of Chongqing: Business Model Canvas—Retail, SME, Digital Strategies Unpacked

Unlock the full strategic blueprint behind Bank of Chongqing's business model—discover how targeted retail banking, SME lending, and digital channels combine to drive growth and customer loyalty.

This in-depth Business Model Canvas breaks down value propositions, key partnerships, revenue streams, and cost structure for practical benchmarking and strategic planning.

Download the complete Word/Excel canvas to get company-specific insights and ready-to-use frameworks for investors, consultants, and executives.

Partnerships

Local Government Entities

The bank holds strategic alliances with the Chongqing municipal government and district authorities to finance regional infrastructure and development projects, channeling government-backed loans—BoC reported RMB 68.7 billion in policy and local government lending in 2024—while managing fiscal deposits exceeding RMB 120 billion. These partnerships align BoC’s growth with the Chengdu-Chongqing Economic Circle, supporting coordinated urbanization and transport projects that target a 5–7% regional GDP uplift through 2025.

Interbank and Financial Institutions

Collaborations with major national banks and international institutions let Bank of Chongqing manage liquidity and join syndicated loans—China interbank market lending lines exceeded CNY 12 trillion in 2024, enabling broader access to funding.

These ties support clearing, FX services, and footprint expansion; partnerships grant access to derivatives and global market intel, aiding cross-border business as Chongqing outbound trade grew 9.8% in 2024.

Fintech and Technology Providers

Strategic cooperation with fintech and tech providers lets Bank of Chongqing modernize digital infrastructure and deploy advanced analytics; by 2024 the bank reported a 28% rise in mobile transactions year-over-year and a 15% cut in loan processing time after API-led platform upgrades with partners like iFlytek and Huawei Cloud.

Corporate Strategic Clients

The bank secures long-term ties with SOEs and major private manufacturers/logistics firms, generating repeat high-value corporate deposits and lending—about 28% of corporate loan book in 2024 (RMB figure: ~RMB 120bn of targeted clients).

These clients drive supply-chain finance and tailored cash-management products, increasing fee income and lowering NPLs through integrated operational workflows.

- 28% of corporate loans from strategic clients (2024)

- ~RMB 120bn exposure to target sectors

- Higher fee income via supply-chain finance

- Customized solutions tied to client ERP/workflow

Regulatory and Compliance Bodies

Maintaining close ties with the People’s Bank of China and the China Banking and Insurance Regulatory Commission gives Bank of Chongqing operational legitimacy and helps it adapt to capital and macro‑prudential rule changes (PBOC reserve ratio tweaks in 2024 averaged 25–50 bps; CBIRC tightened provisioning guidance in 2025).

Frequent communication reduces legal risk and speeds compliance: quarterly supervisory meetings, timely reporting of NPLs (Bank of Chongqing reported 1.32% NPL ratio in 2024) and stress‑test coordination.

- Operational legitimacy via PBOC & CBIRC

- Stay ahead of capital rule shifts (2024–25: 25–50 bps RRR moves)

- Quarterly supervisory meetings and reporting

- Leads to lower regulatory/legal risk; NPL ratio 1.32% (2024)

BoC anchors Chongqing growth: RMB policy loans, CNY12tn liquidity, fintech gains

BoC partners with Chongqing government (RMB 68.7bn policy lending, fiscal deposits >RMB 120bn in 2024), major banks/interbank lines (CNY 12tn market in 2024), fintechs (28% y/y mobile tx growth; 15% faster loan processing), SOEs/private clients (~RMB 120bn exposure; 28% of corporate loans), and regulators (NPL 1.32% in 2024; PBOC RRR moves 25–50bps 2024–25).

| Partner | Key metric (2024–25) |

|---|---|

| Chongqing govt | RMB 68.7bn policy loans; fiscal deposits >RMB 120bn |

| Interbank/national banks | CNY 12tn market liquidity |

| Fintech/tech | Mobile tx +28% YoY; loan time -15% |

| Corporate clients | ~RMB 120bn exposure; 28% corp loans |

| Regulators | NPL 1.32%; RRR moves 25–50bps |

What is included in the product

A comprehensive, pre-written Business Model Canvas for Bank of Chongqing that maps its nine BMC blocks—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, key activities, key partners, and cost structure—reflecting real-world operations, competitive advantages, SWOT-linked insights, and polished narratives ideal for presentations, investor funding discussions, and strategic decision-making.

Condenses Bank of Chongqing’s strategy into a digestible one-page Business Model Canvas, saving hours of structuring and enabling quick comparisons, team collaboration, and board-ready presentations.

Activities

Credit and Loan Management

Credit and loan management covers assessment, disbursement, and monitoring of corporate and retail loans; Bank of Chongqing reported net loans of CNY 840.3 billion as of 2024-12-31, driving ~65% of 2024 interest income.

The bank uses advanced credit models and quarterly collateral revaluations; 2024 NPL ratio stood at 1.42% and coverage ratio at 207%, protecting asset quality.

Deposit Mobilization and Management

Bank of Chongqing boosts deposits via tiered savings, high-yield time deposits, and liquidity pools for corporates; deposits rose 6.8% y/y to RMB 1.12 trillion at end-2024, providing a low-cost funding base for loans.

Marketing, branch promos, and dynamic rate ladders target retail and SME clients; management cut average deposit cost by 12 bps in 2024 to support NIMs while maintaining CASA growth.

Wealth Management and Investment Services

Designs and distributes mutual funds and insurance products targeting Chongqing’s expanding middle class—household financial assets in China rose to RMB 300 trillion in 2024, with Chongqing retail investment flows up ~9% YoY—while acting as intermediary and providing advisory services to meet client goals. This wealth-management hub generates fee income (Bank of Chongqing reported non-interest income growth of 7.2% in 2024), diversifying revenue away from lending.

Digital Transformation and IT Operations

Bank of Chongqing invests continuously in digital banking infrastructure—upgrading secure data centers, rolling out mobile apps, and embedding AI chatbots—cutting transaction costs and boosting service speed; in 2024 digital transactions rose ~28% y/y, now >45% of retail volume.

- Secure data centers: multi-site resilience, 99.99% uptime target

- Mobile apps: user-centric updates, 4.6 avg rating (2024)

- AI: automated service handles ~30% of queries

- Cost impact: digital channel cost-per-transaction down ~40% since 2021

Risk Management and Internal Control

Risk management and internal control at Bank of Chongqing center on frameworks that identify, measure, and mitigate financial, operational, and reputational risks, using quarterly stress tests and internal audits to meet CBIRC (China Banking and Insurance Regulatory Commission) standards; AML compliance covers transaction monitoring across ¥1.2 trillion in 2024 deposits.

Strong internal controls sustain investor confidence and regulatory standing, with the bank reporting a 12.6% CET1 ratio and a nonperforming loan ratio of 1.25% at end-2024.

- Quarterly stress tests and internal audits

- AML transaction monitoring across ¥1.2 trillion deposits (2024)

- CET1 ratio 12.6% (2024)

- NPL ratio 1.25% (2024)

Stable credit growth, strong deposits & digital surge—healthy capital and risk metrics

Core activities: credit origination/monitoring (net loans CNY 840.3bn, NPL 1.42%, coverage 207% at 2024-12-31), deposit gathering (deposits CNY 1.12tn, +6.8% y/y; deposit cost -12bps in 2024), wealth products (non-interest income +7.2% in 2024), digital ops (digital transactions +28% y/y; >45% retail volume), and risk/regs (CET1 12.6%, AML monitoring ¥1.2tn).

| Metric | 2024 value |

|---|---|

| Net loans | CNY 840.3bn |

| Deposits | CNY 1.12tn |

| NPL ratio | 1.42% |

| Coverage ratio | 207% |

| CET1 ratio | 12.6% |

| Non-interest income growth | +7.2% |

| Digital transactions growth | +28% y/y |

| AML monitored deposits | ¥1.2tn |

Delivered as Displayed

Business Model Canvas

The document you're previewing is the actual Bank of Chongqing Business Model Canvas you’ll receive—no mockup or sample. Upon purchase, you’ll get this same, complete file ready for editing, presenting, and sharing. The preview matches the final deliverable in content and format, so there are no surprises. Instant download in editable format is provided after checkout.