Bank of Chongqing PESTLE Analysis

Skip the Research. Get the Strategy.

Explore how political shifts, economic trends, and rapid fintech adoption are reshaping Bank of Chongqing’s risk profile and growth prospects—our concise PESTLE highlights the critical external forces you need to know; purchase the full analysis for a complete, actionable roadmap to inform investment and strategic decisions.

Political factors

Chengdu-Chongqing Economic Circle Policy

The central government’s Chengdu-Chongqing Economic Circle push (target GDP share rise to ~15% of national output by 2030) gives Bank of Chongqing strong tailwinds for infrastructure financing; as a regional leader it captured ~12% YoY growth in corporate loans in 2024, benefiting from state-led projects and a steady pipeline of government-backed lending—over CNY 200bn in planned transport and energy projects in the region through 2026.

Local Government Influence and Support

The Chongqing Municipal Government holds about 10.6% of Bank of Chongqing (2024), creating close policy alignment that yields preferential access to municipal lending and infrastructure deals while offering an implicit safety net.

Dependence on local fiscal health is material: Chongqing’s 2024 GDP grew 4.9% y/y, so regional downturns or tighter budgets could stress loan demand and capital support.

Executives must track municipal leadership changes and fiscal ratios—Chongqing’s 2024 public budget deficit ~2.3% of GDP—to anticipate shifts in capital injections or strategic priorities.

Geopolitical Trade Relations

As a hub for the New International Land-Sea Trade Corridor, Chongqing's trade finance volumes are sensitive to China–ASEAN and China–EU relations; in 2024 Chongqing processed over CNY 1.2 trillion in cross-border trade, exposing Bank of Chongqing to diplomatic shifts. Fluctuations in international diplomacy can reduce demand from export-oriented clients—manufacturing exports from Chongqing fell 3.5% YoY in Q3 2025—pressuring loan performance. The bank must manage political complexity in cross-border settlements, compliance costs rose ~18% in 2024 due to enhanced sanctions screening.

State-Directed Credit Allocation

The Chinese banking sector directs credit to priorities like high-tech manufacturing and 'little giants' SMEs; in 2024 state-guided loans and re-lending channels supported over CNY 3.5 trillion in targeted credit nationwide, pressuring regional banks to comply.

Bank of Chongqing must balance profitability with mandates to finance the real economy and rural revitalization—Chongqing city issued CNY 200+ billion in local policy loans in 2023–24—affecting asset mix and NIM.

Non-alignment risks regulatory friction, constrained access to policy funding, and missed preferential refinancing: policy windows can offer low-cost funding margins 50–150 bps below market rates.

- 2024 targeted credit push: CNY 3.5 trillion nationwide

- Local policy loans (Chongqing) 2023–24: CNY 200+ billion

- Policy funding margin advantage: ~50–150 bps

- Key focus: high-tech, 'little giants', rural revitalization

Financial Stability and De-risking Mandates

By late 2025 Beijing’s emphasis on systemic financial stability centers on local government debt; national directives pushed banks to reduce exposure, with LGFV debt still estimated at c.40 trillion RMB as of 2024.

Bank of Chongqing faces political pressure to support LGFV restructurings while keeping CET1 and CAR above regulatory minima—end-2024 CAR was about 12.5%—forcing trade-offs between regional liquidity provision and strict risk-containment.

Bank of Chongqing: municipal backing fuels CNY200bn+ projects amid LGFV and compliance strains

Strong central support via Chengdu‑Chongqing Economic Circle and 10.6% municipal ownership give Bank of Chongqing preferential access to CNY 200bn+ regional projects; 2024 metrics: corporate loan growth ~12% YoY, CAR ~12.5%, Chongqing GDP +4.9%; exposure to LGFV risk (national ~CNY 40tn 2024) and rising compliance costs (up ~18% 2024) create trade‑offs.

| Metric | Value (2024) |

|---|---|

| Municipal ownership | 10.6% |

| Corp loan growth | ~12% YoY |

| CAR | ~12.5% |

| Chongqing GDP growth | 4.9% |

| Regional projects | CNY 200bn+ |

| LGFV stock | CNY 40tn |

What is included in the product

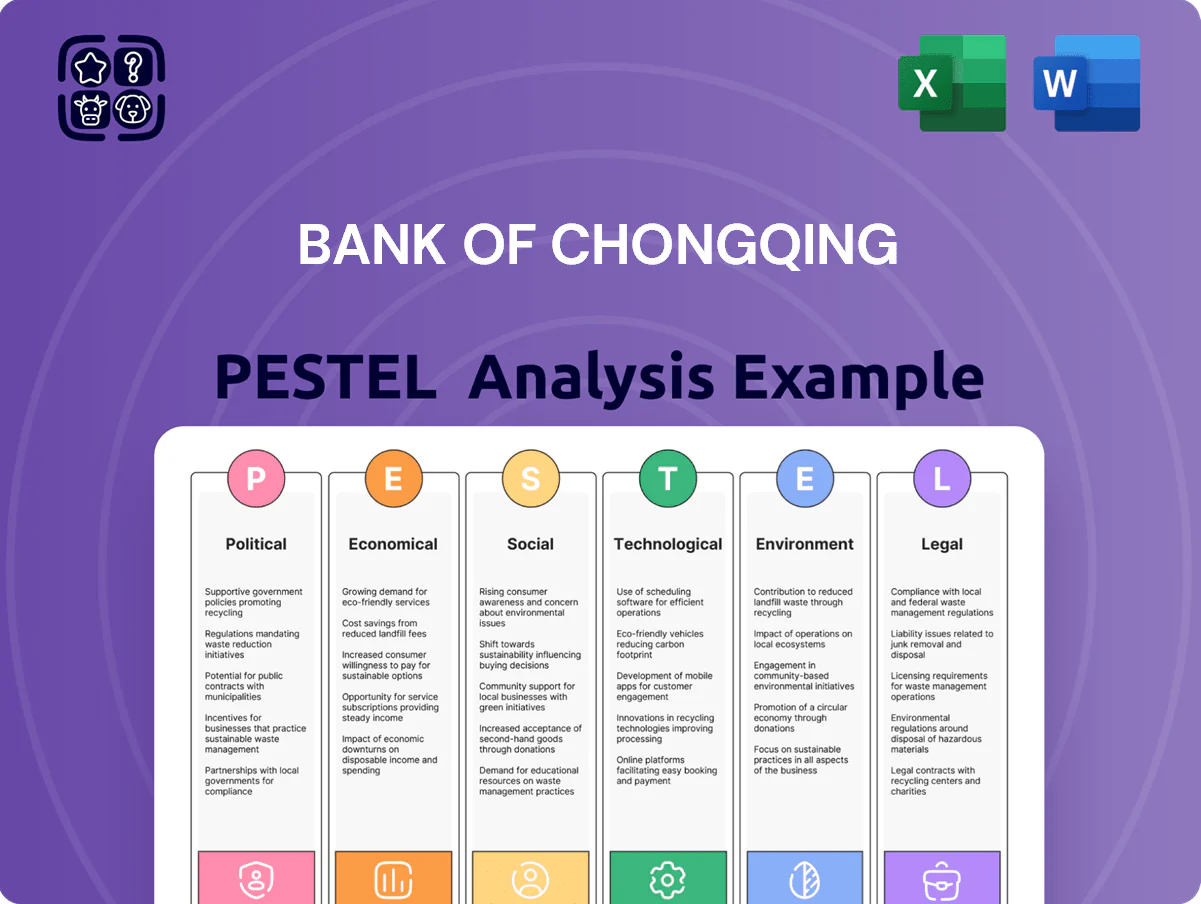

Explores how macro factors—Political, Economic, Social, Technological, Environmental, and Legal—specifically influence Bank of Chongqing, with data-backed trends and forward-looking insights to identify risks and opportunities for executives, investors, and strategists.

A concise PESTLE snapshot of Bank of Chongqing that’s visually segmented for quick interpretation, easily dropped into presentations or shared across teams to streamline external risk discussions and strategic alignment.

Economic factors

Regional GDP Growth Trends

Chongqing grew 6.1% in 2023 and 5.8% in 2024 versus China's national GDP growth of 5.2% (2023) and ~4.9% (2024 provisional), supporting stronger loan demand and generally better asset quality for Bank of Chongqing.

Transition from heavy industry to advanced manufacturing and services—services now ~48% of Chongqing GDP (2024)—requires the bank to shift credit toward tech, automotive supply chains and services to capture new growth drivers.

Automotive and electronics account for ~22% of Chongqing industrial output; cyclical downturns in these sectors quickly raise NPL ratios, historically pushing regional NPLs above national averages during sector slowdowns.

Interest Rate Environment and NIM Compression

The People’s Bank of China maintained an accommodative stance through 2025, keeping the 1-year Loan Prime Rate near 3.65% to support growth, squeezing Bank of Chongqing’s NIM which fell to about 1.45% in 2024 from 1.78% in 2021. Declining loan yields and competition for low-cost deposits force the bank to boost non-interest income — fees and wealth management grew ~12% YoY in 2024 — to offset narrowing lending spreads.

Real Estate Market Stabilization

The prolonged recovery of China’s property sector remains a key risk for Bank of Chongqing, with mortgage and developer exposures concentrated in Chongqing and surrounding provinces; by 2025 national new home prices rose just 1.2% year-on-year while transaction volumes stayed down ~15% vs 2019 levels, keeping buyer sentiment cautious. Systemic risks eased after 2024 rescues, but slower price gains mean continued pressure on NPL formation and provisioning—monitor regional developers where onshore bond defaults totaled ~CNY120bn in 2024 to safeguard coverage ratios.

Currency Volatility and Trade Finance

Fluctuations in the renminbi—which slid about 3.4% vs USD in 2023 and saw 2024 volatility ±2%—raise FX losses for Bank of Chongqing’s import-export clients, pressuring trade finance margins and requiring higher pricing for forward contracts.

As Chongqing grows as a logistics hub (cargo throughput up ~6% in 2024), the bank’s ability to offer options, NDFs and structured hedges is a competitive differentiator that can capture rising cross-border payment flows.

Global demand shifts—world merchandise trade volume fell 0.5% in 2023 then modestly recovered in 2024—influence transaction volumes and fee income in the bank’s cross-border payments unit, creating revenue cyclicality tied to trade cycles.

- RMB volatility: 2023 -3.4% vs USD; 2024 ±2%

- Chongqing cargo throughput: +6% in 2024

- World trade volume: -0.5% (2023), modest recovery 2024

Inflationary Pressures and Consumer Spending

Domestic consumption in Western China, including Chongqing, drives retail growth for Bank of Chongqing: in 2024 Chongqing's per-capita disposable income rose 5.6% y/y to CNY 36,200, supporting demand for credit cards and personal consumption loans.

Moderate inflation (2024 CPI ~2.1% nationally) can lift nominal loan balances, but sharper local cost-of-living rises would reduce borrowers' debt-servicing capacity; household savings rate in Chongqing was ~31% in 2023.

The bank must recalibrate retail risk models to reflect shifting disposable income and a 2024 urban unemployment rate near 4.0% in Chongqing, adjusting provisioning and approval thresholds accordingly.

- 2024 per-capita disposable income CNY 36,200 (+5.6%)

- National CPI 2024 ~2.1%

- Chongqing urban unemployment ~4.0% (2024)

- Household savings rate ~31% (2023)

Chongqing shifts to services & tech amid 5.8% GDP, falling NIM and rising fees

Chongqing GDP grew 6.1% (2023) and 5.8% (2024), boosting loan demand; services ~48% of GDP (2024) shifts credit to tech and services. NIM fell to ~1.45% (2024) from 1.78% (2021); fees/WM +12% YoY (2024). Property recovery slow—new home prices +1.2% (2025) with transactions -15% vs 2019. RMB volatility: -3.4% (2023), ±2% (2024).

| Metric | Value |

|---|---|

| Chongqing GDP growth 2024 | 5.8% |

| NIM 2024 | 1.45% |

| Services share 2024 | 48% |

| Fees/W&M growth 2024 | +12% |

Preview the Actual Deliverable

Bank of Chongqing PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use; it contains the full PESTLE analysis for Bank of Chongqing with complete sections on Political, Economic, Social, Technological, Legal, and Environmental factors.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Skip the Research. Get the Strategy.

Explore how political shifts, economic trends, and rapid fintech adoption are reshaping Bank of Chongqing’s risk profile and growth prospects—our concise PESTLE highlights the critical external forces you need to know; purchase the full analysis for a complete, actionable roadmap to inform investment and strategic decisions.

Political factors

Chengdu-Chongqing Economic Circle Policy

The central government’s Chengdu-Chongqing Economic Circle push (target GDP share rise to ~15% of national output by 2030) gives Bank of Chongqing strong tailwinds for infrastructure financing; as a regional leader it captured ~12% YoY growth in corporate loans in 2024, benefiting from state-led projects and a steady pipeline of government-backed lending—over CNY 200bn in planned transport and energy projects in the region through 2026.

Local Government Influence and Support

The Chongqing Municipal Government holds about 10.6% of Bank of Chongqing (2024), creating close policy alignment that yields preferential access to municipal lending and infrastructure deals while offering an implicit safety net.

Dependence on local fiscal health is material: Chongqing’s 2024 GDP grew 4.9% y/y, so regional downturns or tighter budgets could stress loan demand and capital support.

Executives must track municipal leadership changes and fiscal ratios—Chongqing’s 2024 public budget deficit ~2.3% of GDP—to anticipate shifts in capital injections or strategic priorities.

Geopolitical Trade Relations

As a hub for the New International Land-Sea Trade Corridor, Chongqing's trade finance volumes are sensitive to China–ASEAN and China–EU relations; in 2024 Chongqing processed over CNY 1.2 trillion in cross-border trade, exposing Bank of Chongqing to diplomatic shifts. Fluctuations in international diplomacy can reduce demand from export-oriented clients—manufacturing exports from Chongqing fell 3.5% YoY in Q3 2025—pressuring loan performance. The bank must manage political complexity in cross-border settlements, compliance costs rose ~18% in 2024 due to enhanced sanctions screening.

State-Directed Credit Allocation

The Chinese banking sector directs credit to priorities like high-tech manufacturing and 'little giants' SMEs; in 2024 state-guided loans and re-lending channels supported over CNY 3.5 trillion in targeted credit nationwide, pressuring regional banks to comply.

Bank of Chongqing must balance profitability with mandates to finance the real economy and rural revitalization—Chongqing city issued CNY 200+ billion in local policy loans in 2023–24—affecting asset mix and NIM.

Non-alignment risks regulatory friction, constrained access to policy funding, and missed preferential refinancing: policy windows can offer low-cost funding margins 50–150 bps below market rates.

- 2024 targeted credit push: CNY 3.5 trillion nationwide

- Local policy loans (Chongqing) 2023–24: CNY 200+ billion

- Policy funding margin advantage: ~50–150 bps

- Key focus: high-tech, 'little giants', rural revitalization

Financial Stability and De-risking Mandates

By late 2025 Beijing’s emphasis on systemic financial stability centers on local government debt; national directives pushed banks to reduce exposure, with LGFV debt still estimated at c.40 trillion RMB as of 2024.

Bank of Chongqing faces political pressure to support LGFV restructurings while keeping CET1 and CAR above regulatory minima—end-2024 CAR was about 12.5%—forcing trade-offs between regional liquidity provision and strict risk-containment.

Bank of Chongqing: municipal backing fuels CNY200bn+ projects amid LGFV and compliance strains

Strong central support via Chengdu‑Chongqing Economic Circle and 10.6% municipal ownership give Bank of Chongqing preferential access to CNY 200bn+ regional projects; 2024 metrics: corporate loan growth ~12% YoY, CAR ~12.5%, Chongqing GDP +4.9%; exposure to LGFV risk (national ~CNY 40tn 2024) and rising compliance costs (up ~18% 2024) create trade‑offs.

| Metric | Value (2024) |

|---|---|

| Municipal ownership | 10.6% |

| Corp loan growth | ~12% YoY |

| CAR | ~12.5% |

| Chongqing GDP growth | 4.9% |

| Regional projects | CNY 200bn+ |

| LGFV stock | CNY 40tn |

What is included in the product

Explores how macro factors—Political, Economic, Social, Technological, Environmental, and Legal—specifically influence Bank of Chongqing, with data-backed trends and forward-looking insights to identify risks and opportunities for executives, investors, and strategists.

A concise PESTLE snapshot of Bank of Chongqing that’s visually segmented for quick interpretation, easily dropped into presentations or shared across teams to streamline external risk discussions and strategic alignment.

Economic factors

Regional GDP Growth Trends

Chongqing grew 6.1% in 2023 and 5.8% in 2024 versus China's national GDP growth of 5.2% (2023) and ~4.9% (2024 provisional), supporting stronger loan demand and generally better asset quality for Bank of Chongqing.

Transition from heavy industry to advanced manufacturing and services—services now ~48% of Chongqing GDP (2024)—requires the bank to shift credit toward tech, automotive supply chains and services to capture new growth drivers.

Automotive and electronics account for ~22% of Chongqing industrial output; cyclical downturns in these sectors quickly raise NPL ratios, historically pushing regional NPLs above national averages during sector slowdowns.

Interest Rate Environment and NIM Compression

The People’s Bank of China maintained an accommodative stance through 2025, keeping the 1-year Loan Prime Rate near 3.65% to support growth, squeezing Bank of Chongqing’s NIM which fell to about 1.45% in 2024 from 1.78% in 2021. Declining loan yields and competition for low-cost deposits force the bank to boost non-interest income — fees and wealth management grew ~12% YoY in 2024 — to offset narrowing lending spreads.

Real Estate Market Stabilization

The prolonged recovery of China’s property sector remains a key risk for Bank of Chongqing, with mortgage and developer exposures concentrated in Chongqing and surrounding provinces; by 2025 national new home prices rose just 1.2% year-on-year while transaction volumes stayed down ~15% vs 2019 levels, keeping buyer sentiment cautious. Systemic risks eased after 2024 rescues, but slower price gains mean continued pressure on NPL formation and provisioning—monitor regional developers where onshore bond defaults totaled ~CNY120bn in 2024 to safeguard coverage ratios.

Currency Volatility and Trade Finance

Fluctuations in the renminbi—which slid about 3.4% vs USD in 2023 and saw 2024 volatility ±2%—raise FX losses for Bank of Chongqing’s import-export clients, pressuring trade finance margins and requiring higher pricing for forward contracts.

As Chongqing grows as a logistics hub (cargo throughput up ~6% in 2024), the bank’s ability to offer options, NDFs and structured hedges is a competitive differentiator that can capture rising cross-border payment flows.

Global demand shifts—world merchandise trade volume fell 0.5% in 2023 then modestly recovered in 2024—influence transaction volumes and fee income in the bank’s cross-border payments unit, creating revenue cyclicality tied to trade cycles.

- RMB volatility: 2023 -3.4% vs USD; 2024 ±2%

- Chongqing cargo throughput: +6% in 2024

- World trade volume: -0.5% (2023), modest recovery 2024

Inflationary Pressures and Consumer Spending

Domestic consumption in Western China, including Chongqing, drives retail growth for Bank of Chongqing: in 2024 Chongqing's per-capita disposable income rose 5.6% y/y to CNY 36,200, supporting demand for credit cards and personal consumption loans.

Moderate inflation (2024 CPI ~2.1% nationally) can lift nominal loan balances, but sharper local cost-of-living rises would reduce borrowers' debt-servicing capacity; household savings rate in Chongqing was ~31% in 2023.

The bank must recalibrate retail risk models to reflect shifting disposable income and a 2024 urban unemployment rate near 4.0% in Chongqing, adjusting provisioning and approval thresholds accordingly.

- 2024 per-capita disposable income CNY 36,200 (+5.6%)

- National CPI 2024 ~2.1%

- Chongqing urban unemployment ~4.0% (2024)

- Household savings rate ~31% (2023)

Chongqing shifts to services & tech amid 5.8% GDP, falling NIM and rising fees

Chongqing GDP grew 6.1% (2023) and 5.8% (2024), boosting loan demand; services ~48% of GDP (2024) shifts credit to tech and services. NIM fell to ~1.45% (2024) from 1.78% (2021); fees/WM +12% YoY (2024). Property recovery slow—new home prices +1.2% (2025) with transactions -15% vs 2019. RMB volatility: -3.4% (2023), ±2% (2024).

| Metric | Value |

|---|---|

| Chongqing GDP growth 2024 | 5.8% |

| NIM 2024 | 1.45% |

| Services share 2024 | 48% |

| Fees/W&M growth 2024 | +12% |

Preview the Actual Deliverable

Bank of Chongqing PESTLE Analysis

The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use; it contains the full PESTLE analysis for Bank of Chongqing with complete sections on Political, Economic, Social, Technological, Legal, and Environmental factors.