Chongqing Rural Bank Business Model Canvas

Chongqing Rural Bank: Concise Business Model Canvas for SME & Retail Strategy

Unlock the full strategic blueprint behind Chongqing Rural Bank’s business model—this concise Business Model Canvas exposes how it serves local SMEs and retail customers, leverages digital channels and township partnerships, and balances risk with community-focused lending; ideal for investors, strategists, and consultants seeking actionable, sector-specific insights—download the full Word/Excel canvas to benchmark, adapt, and execute with confidence.

Partnerships

Strategic Government Alliances

The bank maintains deep ties with Chongqing municipal and district governments to align lending with regional goals, channeling over CNY 12.4 billion in government-backed rural loans in 2024 and supporting 18 district-level rural revitalization projects. By administering subsidized credit and municipal infrastructure financing, Chongqing Rural Bank serves as a primary intermediary for public social and infrastructure projects, holding a 32% share of rural government-directed lending in the municipality.

Fintech and Technology Providers

Collaborations with Chinese tech firms like Alibaba Cloud and Tencent Cloud power Chongqing Rural Bank’s digital transformation, supplying cloud infrastructure that cut IT costs by ~28% in 2024 and support AI credit models that boosted small-loan approvals 18% year-over-year. These partners enable secure mobile payments (handling 1.2M transactions/month in 2025) and advanced analytics, letting the bank match national rivals with modern, efficient digital services for rural and urban customers.

Agricultural Cooperatives and Industrial Unions

Chongqing Rural Bank partners with over 1,200 local agricultural cooperatives and 350 rural industrial unions, reaching roughly 420,000 farming households as of 2025; these links let the bank source and vet creditworthy smallholders and specialized agri-enterprises that often lack formal records. The network enables targeted microloans (average loan size RMB 28,000 in 2024) and on-site financial training, cutting default rates by 1.8 percentage points versus unpartnered lending.

Interbank and Financial Institution Networks

Membership in China’s national interbank trading and clearing systems (CNAPS, CIPS) lets Chongqing Rural Commercial Bank manage intraday liquidity and access wholesale funding; at end-2024 the bank reported RMB 12.8 billion in interbank borrowings, aiding a 3.6% CET1-equivalent liquidity buffer.

Strategic ties with large state-owned banks and select international banks support treasury operations and trade finance—co-financing and syndication helped the bank expand FX and import letters of credit volume by 22% in 2024—diversifying assets and smoothing volatility.

- RMB 12.8B interbank borrowings (2024)

- 3.6% CET1-equivalent liquidity buffer

- 22% YoY rise in trade finance volume (2024)

- Access to CNAPS/CIPS and major SOE banks

Third-Party Service and Insurance Providers

The bank partners with insurance companies and wealth managers to sell third-party products, earning commission fees (≈RMB 120–180 million in 2024) while extending risk protection and investment choices to rural clients.

Integrating these services converts branches into one-stop financial centers across Chongqing, boosting noninterest income and cross-sell rates (cross-sell up ~15% YoY in 2024).

- Commission income ~RMB 120–180M (2024)

- Cross-sell +15% YoY (2024)

- Branch reach: >300 outlets in Chongqing

Chongqing Rural Bank: Govt-backed CNY12.4B rural loans fuel digital growth and +15% cross-sell

Chongqing Rural Bank relies on government ties, tech giants (Alibaba/Tencent Cloud), 1,200+ cooperatives, CNAPS/CIPS access and SOE bank syndication to channel CNY 12.4B govt rural loans (2024), hold CNY 12.8B interbank debt and earn CNY 120–180M commissions, boosting cross-sell +15% and digital transactions to 1.2M/month (2025).

| Metric | Value |

|---|---|

| Govt rural loans (2024) | CNY 12.4B |

| Interbank borrowings (2024) | CNY 12.8B |

| Commission income (2024) | CNY 120–180M |

| Cross-sell growth (2024) | +15% YoY |

| Digital txns (2025) | 1.2M/month |

What is included in the product

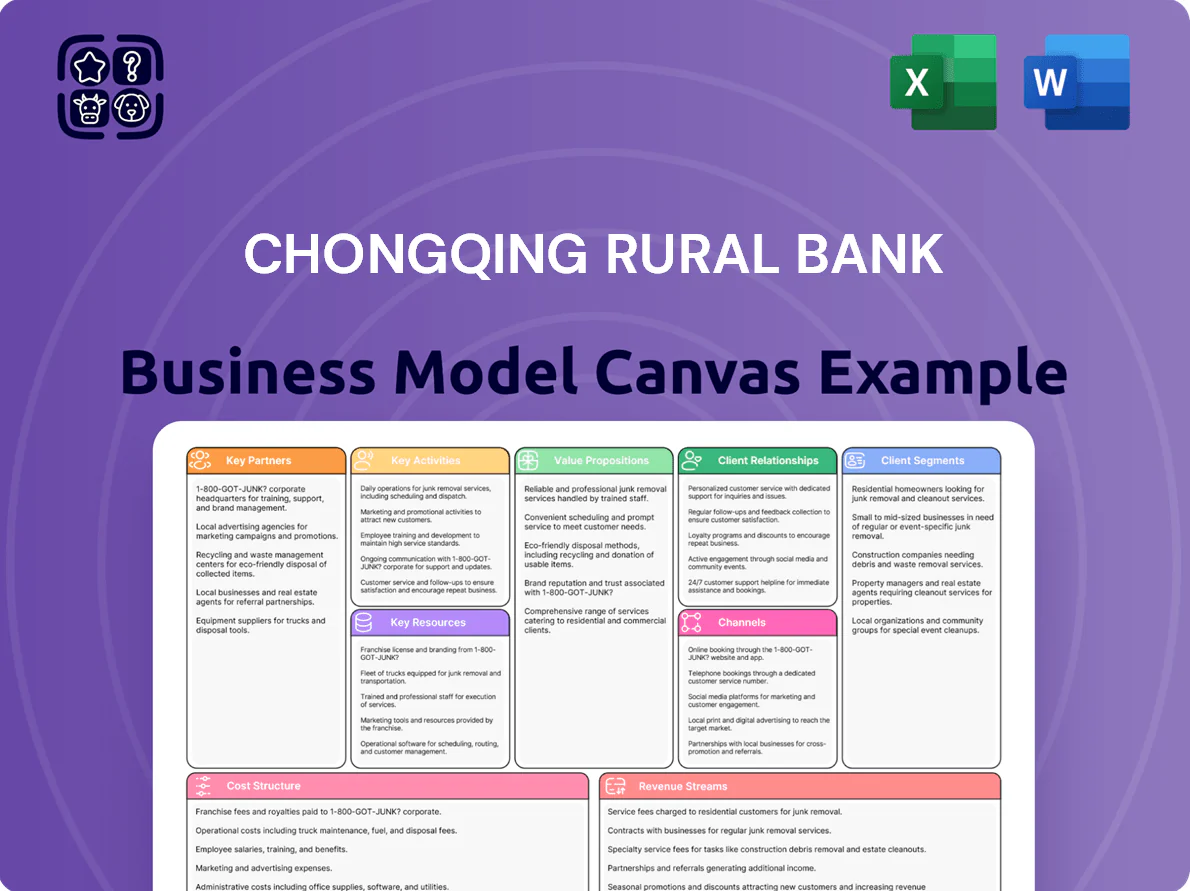

A concise Business Model Canvas for Chongqing Rural Commercial Bank outlining nine BMC blocks—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, key activities, key partners, and cost structure—built from real operations to support presentations, investor pitches, SWOT-linked insights, and strategic decision-making for entrepreneurs and analysts.

Condenses Chongqing Rural Bank’s strategy into a digestible one-page Business Model Canvas, saving hours of structuring while enabling quick comparison, team collaboration, and fast executive summaries for boardrooms or internal planning.

Activities

Credit and Loan Management

The bank rigorously assesses, disburses, and monitors loans to individuals, SMEs, and corporates, targeting a mix of higher-yield rural lending and lower-risk urban corporate credit to keep the loan-to-deposit ratio near 65% (2024 YE).

Ongoing asset-quality checks and NPL (non-performing loan) management are prioritized—Chongqing Rural Commercial Bank reported an NPL ratio of 1.9% in 2024, with targeted recoveries and provisions to preserve long-term health.

Digital Banking Development

As of late 2025 Chongqing Rural Commercial Bank has invested ~RMB 420m into mobile and online platform upgrades, rolling out biometric logins, automated loan decisioning (cutting approval time from 5 days to <24 hours) and advanced SOC cybersecurity tools; these moves aim to lower cost-to-serve by ~18% and grow digital customers by 32% to reach 1.6m, expanding services into remote counties without new branches.

Rural Revitalization Support

Chongqing Rural Bank designs and runs rural-revitalization finance aligned with China’s strategy, issuing green-agriculture, rural-tourism, and agri-tech loans—over CNY 4.2 billion disbursed in 2024 (up 18% YoY), financing 1,120 projects. These targeted products strengthen its position as Chongqing’s leading rural lender, holding ~26% local rural market share by outstanding loan balance as of Dec 31, 2024.

Comprehensive Risk Management

Comprehensive risk management enforces Basel III capital and liquidity ratios (CET1 ≥ 10.5% target; LCR ≥ 120% in 2025) and local CBIRC rules through monthly liquidity coverage monitoring, quarterly macro stress tests showing resilience to a 15% regional GDP shock, and daily market-risk VaR limits.

- Monthly LCR ≥120%

- CET1 target 10.5%+

- Quarterly stress tests: 15% GDP shock

- Daily VaR limits for trading book

- Internal controls, KRI dashboards, incident SLAs

Wealth Management and Advisory

The bank is shifting to fee income: wealth management and advisory now target the rising Chongqing middle class with curated portfolios, retirement planning, and private banking to cut reliance on net interest margin; fee income grew 18% y/y to 1.2 billion CNY in 2024 (12% of non-interest revenue).

- Fee income +18% y/y to 1.2bn CNY (2024)

- Wealth fees ≈12% of non-interest revenue

- Services: portfolios, retirement, private banking

- Goal: diversify from interest-margin dependency

Balanced growth: strong digital expansion, rural lending scale, tight asset quality

Key activities: loan origination & monitoring (L/D ~65% 2024), NPL control (1.9% NPL 2024), digital platform ops (RMB420m invested; digital customers 1.6m, +32%), rural revitalize lending (CNY4.2bn 2024; 1,120 projects; ~26% local rural share), risk & liquidity controls (CET1 target 10.5%, LCR ≥120%), fee-income growth (fee income CNY1.2bn, +18% YoY).

| Metric | 2024/late‑2025 |

|---|---|

| Loan‑to‑deposit | ~65% |

| NPL ratio | 1.9% |

| Digital spend | RMB420m |

| Digital customers | 1.6m (+32%) |

| Rural loans | CNY4.2bn (1,120 projects) |

| Rural market share | ~26% |

| CET1 target | 10.5%+ |

| LCR | ≥120% |

| Fee income | CNY1.2bn (+18%) |

Preview Before You Purchase

Business Model Canvas

The preview you see is the actual Chongqing Rural Bank Business Model Canvas—not a mockup—and it’s the same document you’ll receive after purchase; upon completing your order you’ll download the full, editable file formatted exactly as shown, ready for presentation, analysis, or modification.

Original: $10.00

-65%$10.00

$3.50Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

Chongqing Rural Bank: Concise Business Model Canvas for SME & Retail Strategy

Unlock the full strategic blueprint behind Chongqing Rural Bank’s business model—this concise Business Model Canvas exposes how it serves local SMEs and retail customers, leverages digital channels and township partnerships, and balances risk with community-focused lending; ideal for investors, strategists, and consultants seeking actionable, sector-specific insights—download the full Word/Excel canvas to benchmark, adapt, and execute with confidence.

Partnerships

Strategic Government Alliances

The bank maintains deep ties with Chongqing municipal and district governments to align lending with regional goals, channeling over CNY 12.4 billion in government-backed rural loans in 2024 and supporting 18 district-level rural revitalization projects. By administering subsidized credit and municipal infrastructure financing, Chongqing Rural Bank serves as a primary intermediary for public social and infrastructure projects, holding a 32% share of rural government-directed lending in the municipality.

Fintech and Technology Providers

Collaborations with Chinese tech firms like Alibaba Cloud and Tencent Cloud power Chongqing Rural Bank’s digital transformation, supplying cloud infrastructure that cut IT costs by ~28% in 2024 and support AI credit models that boosted small-loan approvals 18% year-over-year. These partners enable secure mobile payments (handling 1.2M transactions/month in 2025) and advanced analytics, letting the bank match national rivals with modern, efficient digital services for rural and urban customers.

Agricultural Cooperatives and Industrial Unions

Chongqing Rural Bank partners with over 1,200 local agricultural cooperatives and 350 rural industrial unions, reaching roughly 420,000 farming households as of 2025; these links let the bank source and vet creditworthy smallholders and specialized agri-enterprises that often lack formal records. The network enables targeted microloans (average loan size RMB 28,000 in 2024) and on-site financial training, cutting default rates by 1.8 percentage points versus unpartnered lending.

Interbank and Financial Institution Networks

Membership in China’s national interbank trading and clearing systems (CNAPS, CIPS) lets Chongqing Rural Commercial Bank manage intraday liquidity and access wholesale funding; at end-2024 the bank reported RMB 12.8 billion in interbank borrowings, aiding a 3.6% CET1-equivalent liquidity buffer.

Strategic ties with large state-owned banks and select international banks support treasury operations and trade finance—co-financing and syndication helped the bank expand FX and import letters of credit volume by 22% in 2024—diversifying assets and smoothing volatility.

- RMB 12.8B interbank borrowings (2024)

- 3.6% CET1-equivalent liquidity buffer

- 22% YoY rise in trade finance volume (2024)

- Access to CNAPS/CIPS and major SOE banks

Third-Party Service and Insurance Providers

The bank partners with insurance companies and wealth managers to sell third-party products, earning commission fees (≈RMB 120–180 million in 2024) while extending risk protection and investment choices to rural clients.

Integrating these services converts branches into one-stop financial centers across Chongqing, boosting noninterest income and cross-sell rates (cross-sell up ~15% YoY in 2024).

- Commission income ~RMB 120–180M (2024)

- Cross-sell +15% YoY (2024)

- Branch reach: >300 outlets in Chongqing

Chongqing Rural Bank: Govt-backed CNY12.4B rural loans fuel digital growth and +15% cross-sell

Chongqing Rural Bank relies on government ties, tech giants (Alibaba/Tencent Cloud), 1,200+ cooperatives, CNAPS/CIPS access and SOE bank syndication to channel CNY 12.4B govt rural loans (2024), hold CNY 12.8B interbank debt and earn CNY 120–180M commissions, boosting cross-sell +15% and digital transactions to 1.2M/month (2025).

| Metric | Value |

|---|---|

| Govt rural loans (2024) | CNY 12.4B |

| Interbank borrowings (2024) | CNY 12.8B |

| Commission income (2024) | CNY 120–180M |

| Cross-sell growth (2024) | +15% YoY |

| Digital txns (2025) | 1.2M/month |

What is included in the product

A concise Business Model Canvas for Chongqing Rural Commercial Bank outlining nine BMC blocks—customer segments, value propositions, channels, customer relationships, revenue streams, key resources, key activities, key partners, and cost structure—built from real operations to support presentations, investor pitches, SWOT-linked insights, and strategic decision-making for entrepreneurs and analysts.

Condenses Chongqing Rural Bank’s strategy into a digestible one-page Business Model Canvas, saving hours of structuring while enabling quick comparison, team collaboration, and fast executive summaries for boardrooms or internal planning.

Activities

Credit and Loan Management

The bank rigorously assesses, disburses, and monitors loans to individuals, SMEs, and corporates, targeting a mix of higher-yield rural lending and lower-risk urban corporate credit to keep the loan-to-deposit ratio near 65% (2024 YE).

Ongoing asset-quality checks and NPL (non-performing loan) management are prioritized—Chongqing Rural Commercial Bank reported an NPL ratio of 1.9% in 2024, with targeted recoveries and provisions to preserve long-term health.

Digital Banking Development

As of late 2025 Chongqing Rural Commercial Bank has invested ~RMB 420m into mobile and online platform upgrades, rolling out biometric logins, automated loan decisioning (cutting approval time from 5 days to <24 hours) and advanced SOC cybersecurity tools; these moves aim to lower cost-to-serve by ~18% and grow digital customers by 32% to reach 1.6m, expanding services into remote counties without new branches.

Rural Revitalization Support

Chongqing Rural Bank designs and runs rural-revitalization finance aligned with China’s strategy, issuing green-agriculture, rural-tourism, and agri-tech loans—over CNY 4.2 billion disbursed in 2024 (up 18% YoY), financing 1,120 projects. These targeted products strengthen its position as Chongqing’s leading rural lender, holding ~26% local rural market share by outstanding loan balance as of Dec 31, 2024.

Comprehensive Risk Management

Comprehensive risk management enforces Basel III capital and liquidity ratios (CET1 ≥ 10.5% target; LCR ≥ 120% in 2025) and local CBIRC rules through monthly liquidity coverage monitoring, quarterly macro stress tests showing resilience to a 15% regional GDP shock, and daily market-risk VaR limits.

- Monthly LCR ≥120%

- CET1 target 10.5%+

- Quarterly stress tests: 15% GDP shock

- Daily VaR limits for trading book

- Internal controls, KRI dashboards, incident SLAs

Wealth Management and Advisory

The bank is shifting to fee income: wealth management and advisory now target the rising Chongqing middle class with curated portfolios, retirement planning, and private banking to cut reliance on net interest margin; fee income grew 18% y/y to 1.2 billion CNY in 2024 (12% of non-interest revenue).

- Fee income +18% y/y to 1.2bn CNY (2024)

- Wealth fees ≈12% of non-interest revenue

- Services: portfolios, retirement, private banking

- Goal: diversify from interest-margin dependency

Balanced growth: strong digital expansion, rural lending scale, tight asset quality

Key activities: loan origination & monitoring (L/D ~65% 2024), NPL control (1.9% NPL 2024), digital platform ops (RMB420m invested; digital customers 1.6m, +32%), rural revitalize lending (CNY4.2bn 2024; 1,120 projects; ~26% local rural share), risk & liquidity controls (CET1 target 10.5%, LCR ≥120%), fee-income growth (fee income CNY1.2bn, +18% YoY).

| Metric | 2024/late‑2025 |

|---|---|

| Loan‑to‑deposit | ~65% |

| NPL ratio | 1.9% |

| Digital spend | RMB420m |

| Digital customers | 1.6m (+32%) |

| Rural loans | CNY4.2bn (1,120 projects) |

| Rural market share | ~26% |

| CET1 target | 10.5%+ |

| LCR | ≥120% |

| Fee income | CNY1.2bn (+18%) |

Preview Before You Purchase

Business Model Canvas

The preview you see is the actual Chongqing Rural Bank Business Model Canvas—not a mockup—and it’s the same document you’ll receive after purchase; upon completing your order you’ll download the full, editable file formatted exactly as shown, ready for presentation, analysis, or modification.