China Resources Cement Holdings Business Model Canvas

China Resources Cement BMC: Integrated Supply Chain, Scale & Strategic Value

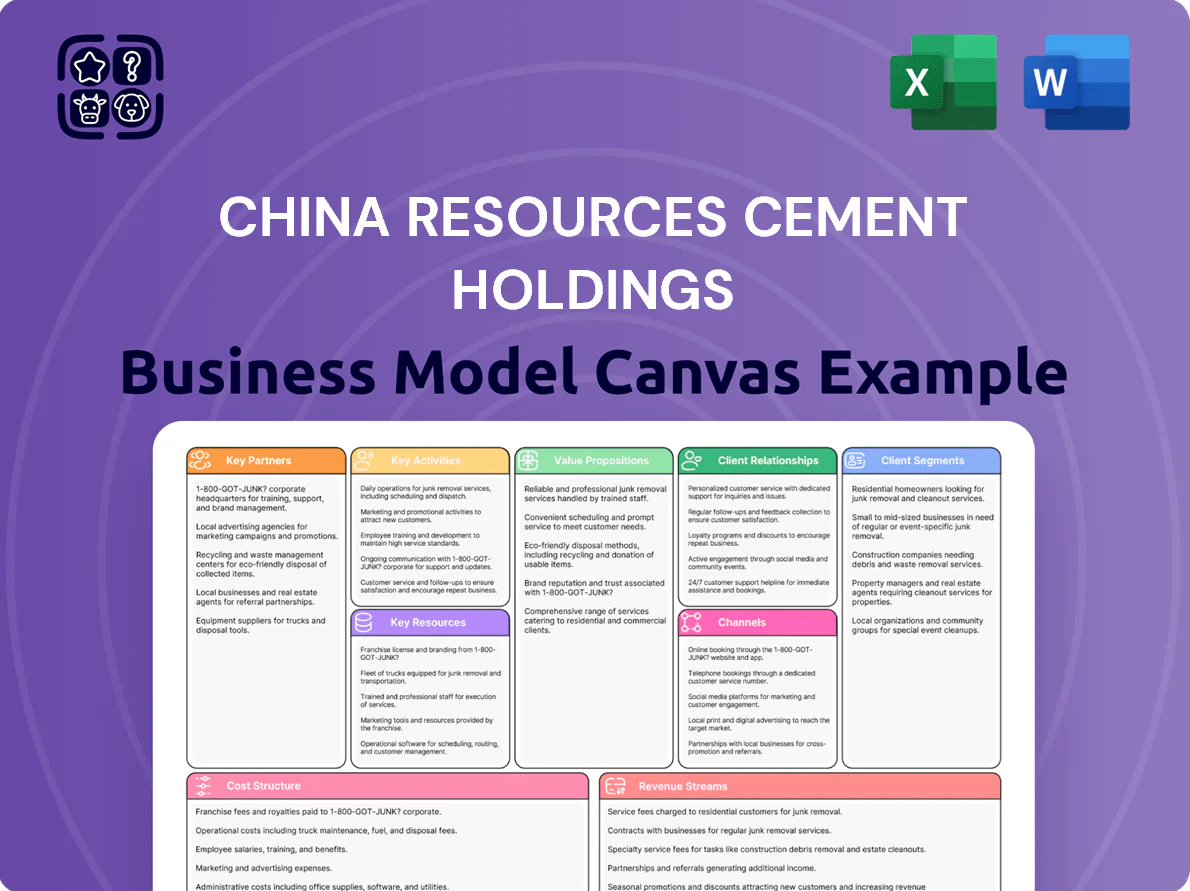

Unlock the full strategic blueprint behind China Resources Cement Holdings: this concise Business Model Canvas shows how the company creates value through integrated supply chains, diversified customer segments, and scale-driven cost advantages—ideal for investors, consultants, and strategists seeking actionable insights.

Partnerships

Strategic Alliance with Local Government Entities

Collaboration with municipal and provincial authorities in Southern China aligns China Resources Cement with regional plans—helping secure mining rights and land permits that cover ~72% of the company’s 2024 clinker capacity in Guangdong and Guangxi, and supporting long-term production stability.

By backing state-funded urbanization projects (China's 2024 urban construction spend ~CNY 3.2 trillion), these ties reinforce CR Cement’s role as a preferred supplier for local infrastructure, stabilizing FY2024 sales in the region at CNY 9.1 billion.

Synergy with China Resources Group Subsidiaries

China Resources Cement leverages China Resources Group affiliation for intra-group procurement and cross-sector projects, supplying steady demand from sister property and infrastructure units that accounted for ~22% of 2024 domestic sales (CR Cement annual report 2024). This integration cuts marketing spend, boosts supply-chain resilience via shared logistics and financing, and benefits from China Resources Group’s A1 credit support and RMB 4.5bn intercompany receivables buffer.

Coal and Energy Supply Partners

Maintaining long-term contracts with major coal suppliers and grid operators covers ~60–70% of China Resources Cement Holdings’ thermal needs, capping fuel cost exposure as global coal price volatility persisted into 2025 (benchmark Australian thermal coal averaged ~98 USD/ton in 2024). Strategic energy alliances also secure renewables — on-site solar and PPAs aimed at cutting scope 2 emissions 15–25% by 2025.

Logistics and Maritime Transport Operators

China Resources Cement teams with specialized shipping firms and logistics providers to run a Pearl River river-transport network that moves heavy bulk cement from production bases to urban demand centers; in 2024 these partnerships supported ~42% of distribution tonnage, keeping average vessel utilization above 85%.

Collaborative logistics planning cuts door-to-door carbon intensity—estimated at 0.12 tCO2e/tonne-km via river vs 0.28 by road—and lowers distribution cost per tonne by ~9% in 2024.

- ~42% distribution by river (2024)

- 85%+ vessel utilization (2024)

- 0.12 vs 0.28 tCO2e/tonne-km (river vs road)

- ~9% lower distribution cost/tonne (2024)

Environmental Technology and Research Institutes

Collaborations with universities and green-tech firms target CCUS (carbon capture, utilization, storage) innovation; joint projects aim to cut Scope 1 emissions by ~20% by 2030 versus 2020 levels, supporting China Resources Cement’s 2025–2030 carbon-neutrality roadmap.

Research also advances waste co-processing and low-carbon cement blends, with pilot plants processing ~1.2 million tonnes/year of alternative fuels and reducing clinker factor by ~10%.

- CCUS pilots targeting 0.5–1.0 Mt CO2/yr capture by 2030

- Waste co-processing ~1.2 Mt/year diverted

- Clinker factor down ~10% via low-carbon blends

Strategic partners secure permits, fuel & logistics; CCUS targets 0.5–1.0Mt CO2/yr

Key partners: local governments securing ~72% clinker permits (Guangdong/Guangxi), China Resources Group internal demand ~22% of 2024 domestic sales, coal suppliers covering 60–70% fuel needs, river logistics moving ~42% tonnage (85%+ utilization), CCUS/waste-pilot capacity ~1.2Mt fuel diversion and 0.5–1.0Mt CO2/yr capture target.

| Partner | Key metric (2024/target) |

|---|---|

| Local govt | ~72% clinker permits |

| CR Group | ~22% domestic sales |

| Coal suppliers | 60–70% fuel cover |

| River logistics | ~42% tonnage, 85%+ util |

| Tech partners | 1.2Mt waste; 0.5–1.0Mt CO2 |

What is included in the product

A focused, pre-written Business Model Canvas for China Resources Cement Holdings outlining customer segments, channels, value propositions, key activities, resources, partners, cost structure and revenue streams, reflecting real-world operations and strategic growth plans for investor and internal presentations.

High-level view of China Resources Cement Holdings' business model with editable cells to quickly pinpoint value drivers, cost structures, and distribution pain points for fast strategic decisions.

Activities

Large-Scale Cement and Clinker Production

China Resources Cement focuses on high-volume cement and clinker output using New Suspension Preheater (NSP) kilns; in 2024 it produced 88.3 million tonnes clinker-equivalent, with NSP plants improving thermal efficiency by ~8% and lowering specific energy to ~740 kcal/kg clinker. Continuous kiln monitoring and chemical control sustain quality for high-rise and heavy infra projects, supporting 2024 revenue of HKD 28.6 billion and gross margin ~22%.

Green Manufacturing and Emission Reduction

China Resources Cement retrofits plants with selective catalytic reduction and desulfurization to cut NOx/SO2, achieving a reported 32% emissions intensity drop from 2018–2024 and spending HKD 1.1 billion on upgrades in 2024; it invests in waste-heat recovery power (WHRP) generating ~1.2 TWh in 2024, covering about 18% of captive electricity use and lowering fuel costs and regulatory risk.

Supply Chain and Logistics Management

China Resources Cement runs 30+ plants, 150+ silos and 12 coastal piers across Southern China, coordinating a barge fleet of ~450 vessels and a trucking pool to move 45–50 Mtpa of clinker/cement; daily logistics focus cuts inventory days to ~18–22 and trims distribution costs by ~8–12%, boosting responsiveness to monthly demand swings of ±10–20%.

Product Research and Quality Innovation

China Resources Cement runs continuous R&D to create high-strength concrete and low-carbon cement for infrastructure; its 2024 labs reported a 12% rise in product-grade approvals and cut clinker ratio by 6 percentage points versus 2022.

Testing teams focus on durability in marine and high-pressure sites, and R&D now targets circular-economy inputs, using >18% industrial waste substitution in some plants to lower CO2 intensity.

- 12% more product approvals (2024)

- 6 pp drop in clinker ratio since 2022

- >18% industrial-waste substitution in select plants

Market Expansion and Customer Acquisition

- 6.8% 2024 Greater Bay demand growth

- RMB 3.2bn large contracts in 2024

- 18% lower clinker factor, 12% emissions cut

- Regional sales +4% YoY targeting hotspots

High-volume NSP cement leader: 88.3Mt clinkereq, HKD1.1bn upgrades, 1.2TWh WHRP

Key activities: high-volume NSP kiln cement/clinker production (88.3 Mtce 2024), plant retrofits for NOx/SO2 and WHRP (HKD 1.1bn capex, 1.2 TWh WHRP), logistics network (30+ plants, 150+ silos, 450 barges) and R&D for low-clinker, waste-substitution products (6 pp clinker drop since 2022, >18% waste in select plants).

| Metric | 2024 |

|---|---|

| Clinker-equivalent | 88.3 Mt |

| Revenue | HKD 28.6bn |

| WHRP | 1.2 TWh |

| Capex (upgrades) | HKD 1.1bn |

Delivered as Displayed

Business Model Canvas

The Business Model Canvas for China Resources Cement Holdings you see here is the actual deliverable, not a mockup; it’s a direct snapshot of the file you’ll receive after purchase.

When you complete your order, you’ll get the identical, fully editable document—structured and formatted as shown—ready for presentation or customization in Word and Excel formats.

Product Information

Product Information

Shipping & Returns

Shipping & Returns

Description

China Resources Cement BMC: Integrated Supply Chain, Scale & Strategic Value

Unlock the full strategic blueprint behind China Resources Cement Holdings: this concise Business Model Canvas shows how the company creates value through integrated supply chains, diversified customer segments, and scale-driven cost advantages—ideal for investors, consultants, and strategists seeking actionable insights.

Partnerships

Strategic Alliance with Local Government Entities

Collaboration with municipal and provincial authorities in Southern China aligns China Resources Cement with regional plans—helping secure mining rights and land permits that cover ~72% of the company’s 2024 clinker capacity in Guangdong and Guangxi, and supporting long-term production stability.

By backing state-funded urbanization projects (China's 2024 urban construction spend ~CNY 3.2 trillion), these ties reinforce CR Cement’s role as a preferred supplier for local infrastructure, stabilizing FY2024 sales in the region at CNY 9.1 billion.

Synergy with China Resources Group Subsidiaries

China Resources Cement leverages China Resources Group affiliation for intra-group procurement and cross-sector projects, supplying steady demand from sister property and infrastructure units that accounted for ~22% of 2024 domestic sales (CR Cement annual report 2024). This integration cuts marketing spend, boosts supply-chain resilience via shared logistics and financing, and benefits from China Resources Group’s A1 credit support and RMB 4.5bn intercompany receivables buffer.

Coal and Energy Supply Partners

Maintaining long-term contracts with major coal suppliers and grid operators covers ~60–70% of China Resources Cement Holdings’ thermal needs, capping fuel cost exposure as global coal price volatility persisted into 2025 (benchmark Australian thermal coal averaged ~98 USD/ton in 2024). Strategic energy alliances also secure renewables — on-site solar and PPAs aimed at cutting scope 2 emissions 15–25% by 2025.

Logistics and Maritime Transport Operators

China Resources Cement teams with specialized shipping firms and logistics providers to run a Pearl River river-transport network that moves heavy bulk cement from production bases to urban demand centers; in 2024 these partnerships supported ~42% of distribution tonnage, keeping average vessel utilization above 85%.

Collaborative logistics planning cuts door-to-door carbon intensity—estimated at 0.12 tCO2e/tonne-km via river vs 0.28 by road—and lowers distribution cost per tonne by ~9% in 2024.

- ~42% distribution by river (2024)

- 85%+ vessel utilization (2024)

- 0.12 vs 0.28 tCO2e/tonne-km (river vs road)

- ~9% lower distribution cost/tonne (2024)

Environmental Technology and Research Institutes

Collaborations with universities and green-tech firms target CCUS (carbon capture, utilization, storage) innovation; joint projects aim to cut Scope 1 emissions by ~20% by 2030 versus 2020 levels, supporting China Resources Cement’s 2025–2030 carbon-neutrality roadmap.

Research also advances waste co-processing and low-carbon cement blends, with pilot plants processing ~1.2 million tonnes/year of alternative fuels and reducing clinker factor by ~10%.

- CCUS pilots targeting 0.5–1.0 Mt CO2/yr capture by 2030

- Waste co-processing ~1.2 Mt/year diverted

- Clinker factor down ~10% via low-carbon blends

Strategic partners secure permits, fuel & logistics; CCUS targets 0.5–1.0Mt CO2/yr

Key partners: local governments securing ~72% clinker permits (Guangdong/Guangxi), China Resources Group internal demand ~22% of 2024 domestic sales, coal suppliers covering 60–70% fuel needs, river logistics moving ~42% tonnage (85%+ utilization), CCUS/waste-pilot capacity ~1.2Mt fuel diversion and 0.5–1.0Mt CO2/yr capture target.

| Partner | Key metric (2024/target) |

|---|---|

| Local govt | ~72% clinker permits |

| CR Group | ~22% domestic sales |

| Coal suppliers | 60–70% fuel cover |

| River logistics | ~42% tonnage, 85%+ util |

| Tech partners | 1.2Mt waste; 0.5–1.0Mt CO2 |

What is included in the product

A focused, pre-written Business Model Canvas for China Resources Cement Holdings outlining customer segments, channels, value propositions, key activities, resources, partners, cost structure and revenue streams, reflecting real-world operations and strategic growth plans for investor and internal presentations.

High-level view of China Resources Cement Holdings' business model with editable cells to quickly pinpoint value drivers, cost structures, and distribution pain points for fast strategic decisions.

Activities

Large-Scale Cement and Clinker Production

China Resources Cement focuses on high-volume cement and clinker output using New Suspension Preheater (NSP) kilns; in 2024 it produced 88.3 million tonnes clinker-equivalent, with NSP plants improving thermal efficiency by ~8% and lowering specific energy to ~740 kcal/kg clinker. Continuous kiln monitoring and chemical control sustain quality for high-rise and heavy infra projects, supporting 2024 revenue of HKD 28.6 billion and gross margin ~22%.

Green Manufacturing and Emission Reduction

China Resources Cement retrofits plants with selective catalytic reduction and desulfurization to cut NOx/SO2, achieving a reported 32% emissions intensity drop from 2018–2024 and spending HKD 1.1 billion on upgrades in 2024; it invests in waste-heat recovery power (WHRP) generating ~1.2 TWh in 2024, covering about 18% of captive electricity use and lowering fuel costs and regulatory risk.

Supply Chain and Logistics Management

China Resources Cement runs 30+ plants, 150+ silos and 12 coastal piers across Southern China, coordinating a barge fleet of ~450 vessels and a trucking pool to move 45–50 Mtpa of clinker/cement; daily logistics focus cuts inventory days to ~18–22 and trims distribution costs by ~8–12%, boosting responsiveness to monthly demand swings of ±10–20%.

Product Research and Quality Innovation

China Resources Cement runs continuous R&D to create high-strength concrete and low-carbon cement for infrastructure; its 2024 labs reported a 12% rise in product-grade approvals and cut clinker ratio by 6 percentage points versus 2022.

Testing teams focus on durability in marine and high-pressure sites, and R&D now targets circular-economy inputs, using >18% industrial waste substitution in some plants to lower CO2 intensity.

- 12% more product approvals (2024)

- 6 pp drop in clinker ratio since 2022

- >18% industrial-waste substitution in select plants

Market Expansion and Customer Acquisition

- 6.8% 2024 Greater Bay demand growth

- RMB 3.2bn large contracts in 2024

- 18% lower clinker factor, 12% emissions cut

- Regional sales +4% YoY targeting hotspots

High-volume NSP cement leader: 88.3Mt clinkereq, HKD1.1bn upgrades, 1.2TWh WHRP

Key activities: high-volume NSP kiln cement/clinker production (88.3 Mtce 2024), plant retrofits for NOx/SO2 and WHRP (HKD 1.1bn capex, 1.2 TWh WHRP), logistics network (30+ plants, 150+ silos, 450 barges) and R&D for low-clinker, waste-substitution products (6 pp clinker drop since 2022, >18% waste in select plants).

| Metric | 2024 |

|---|---|

| Clinker-equivalent | 88.3 Mt |

| Revenue | HKD 28.6bn |

| WHRP | 1.2 TWh |

| Capex (upgrades) | HKD 1.1bn |

Delivered as Displayed

Business Model Canvas

The Business Model Canvas for China Resources Cement Holdings you see here is the actual deliverable, not a mockup; it’s a direct snapshot of the file you’ll receive after purchase.

When you complete your order, you’ll get the identical, fully editable document—structured and formatted as shown—ready for presentation or customization in Word and Excel formats.